- Specialty & Fine Chemicals

- High Performance Elastomers Market

High Performance Elastomers Market Size, Share, and Growth Forecast 2026 - 2033

High Performance Elastomers Market by Product Type (Silicone Elastomers (SiR), Fluorocarbon Elastomers (FKM), Perfluoroelastomers (FFKM), Fluorosilicone Elastomers (FVMQ), Polyacrylate Elastomers (ACM), Ethylene Acrylic Elastomers (AEM), Others), Processing Method (Injection Molding, Compression Molding, Extrusion, 3D Printing/Additive Manufacturing, Others), Application, End-use, and Regional Analysis, 2026 - 2033

High Performance Elastomers Market Size and Trend Analysis

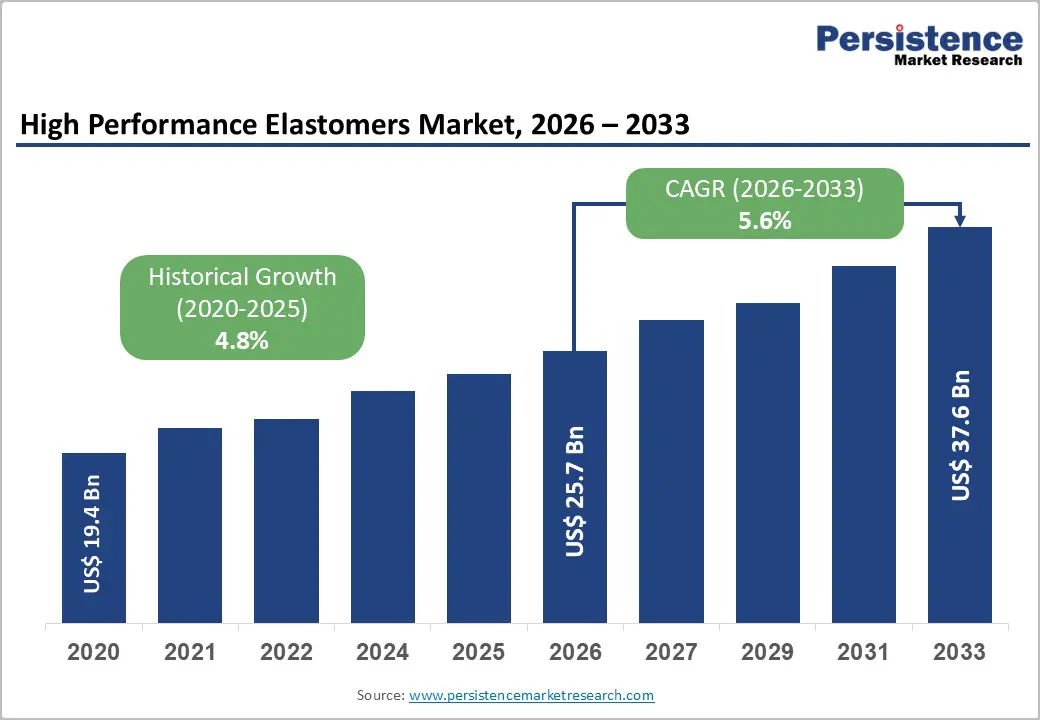

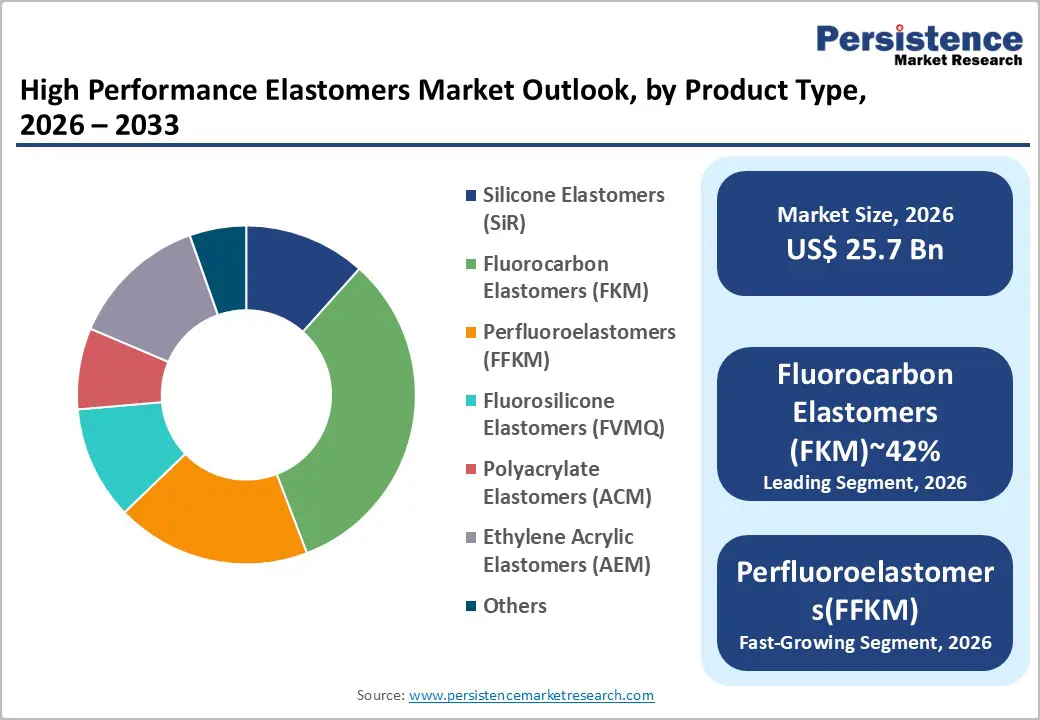

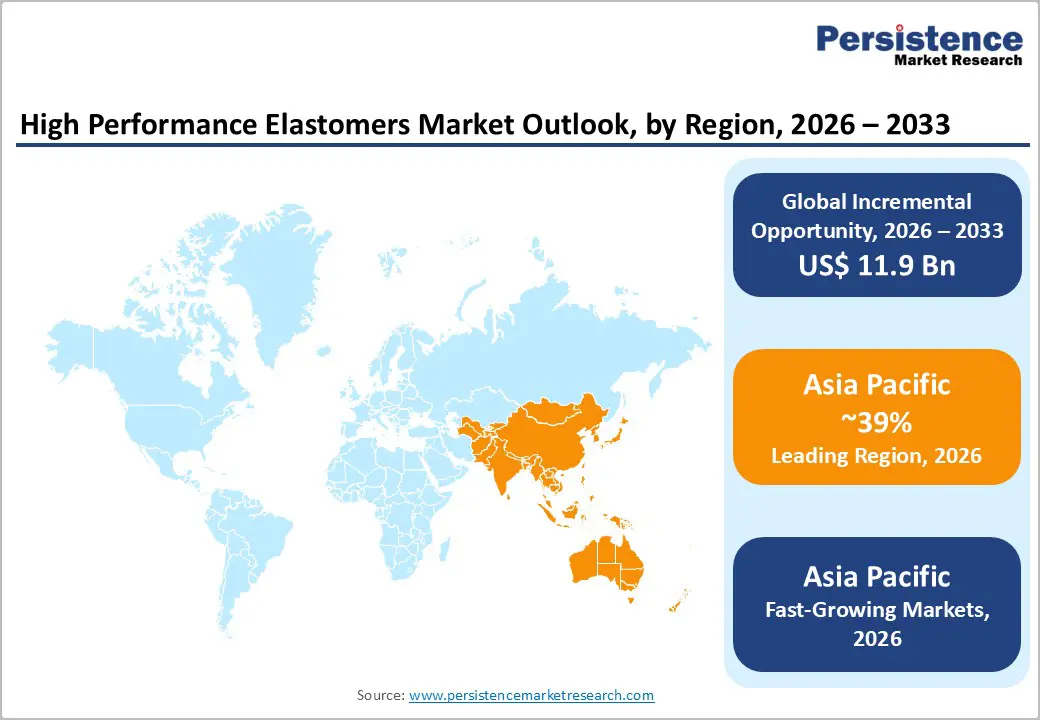

The global high performance elastomers market size is likely to be valued at US$ 25.7 Billion in 2026 and is expected to reach US$ 37.6 Billion by 2033, growing at a CAGR of 5.6% during the forecast period from 2026 and 2033.

Electrification across automotive and aerospace sectors, coupled with extreme environment demands in semiconductors and renewables, propels this growth. FKM and FFKM withstand 400°C and harsh chemicals, essential for EV battery seals and turbofan o-rings.

Key Industry Highlights:

- Leading Region: Asia Pacific leads the high-performance elastomers market with 39% share, due to its strong semiconductor and electric vehicle manufacturing base. Countries like China, Japan, and South Korea drive demand through large-scale production, advanced supply chains, and increasing investments in high-tech industrial applications.

- Fastest Growing Region: The Middle East is emerging as the fastest-growing region with rising CAGR of 7.8%, driven by oilfield modernization and increased adoption of advanced sealing technologies. Investments in upstream and downstream infrastructure are boosting demand for high-performance elastomers capable of withstanding harsh operational environments and extreme temperatures.

- Dominant Product Segment: Fluorocarbon elastomers (FKM) dominate the market with a 42% share, primarily due to their superior resistance to fuel, chemicals, and high temperatures. These properties make them essential for aerospace, automotive, and oil and gas applications requiring durability and long-term performance.

- Fastest Growing Segment: Perfluoroelastomers (FFKM) represent the fastest-growing segment, driven by increasing demand in semiconductor manufacturing, especially for advanced 2nm node processes. Their ultra-low outgassing and chemical resistance make them ideal for high-vacuum and high-purity wafer fabrication environments.

- Key Opportunity: Offshore wind energy presents a key growth opportunity, as turbines require high-performance static seals capable of enduring 20-year cyclic loads in harsh marine environments. Increasing global investments in offshore wind capacity are significantly boosting demand for durable elastomer sealing solutions.

| Key Insights | Details |

|---|---|

| High Performance Elastomers Market Size (2026E) | US$ 25.7 Billion |

| Market Value Forecast (2033F) | US$ 37.6 Billion |

| Projected Growth CAGR (2026 - 2033) | 5.6% |

| Historical Market Growth (2020 - 2025) | 4.8% |

Market Dynamics

Drivers - Rising Demand for High-Performance Elastomer Seals Driven by Advanced Turbofan Engines, Strict FAA Cycles, And Improved Durability Requirements

Next-generation turbofan engines such as the GE9X require high-performance FKM and FFKM O-rings that can withstand extreme conditions, including pressures of up to 1,500 psi and aviation fuel exposure at temperatures around 250°C. In addition, mandatory FAA recertification cycles every five years create consistent demand, resulting in approximately 20% replacement rates for sealing components. Aircraft programs like the Boeing 777X incorporate nearly 30 kg of elastomeric seals per aircraft, highlighting the scale of usage.

Advanced perfluoroelastomers significantly reduce swelling by up to 80% compared to conventional nitrile materials, which helps extend mean time between failures (MTBF) by nearly three times. Furthermore, Rolls-Royce’s UltraFan engine specifications require high-grade sealing solutions equivalent to Parker’s Kalrez, driving technological upgrades and market demand. Collectively, these factors are expected to support the aerospace sealing market, which industry estimates project to reach around US$ 2 billion by 2030.

Growing Electric Vehicle Production Drives Demand for Precision Sealing Solutions, Ensuring Battery Safety, Leakage Prevention, And Long-Term Performance Reliability

Electric vehicle battery systems typically operate at temperatures around 60°C, creating a need for reliable silicone and acrylic gaskets that can effectively prevent electrolyte leakage, even under continuous vibration and stress conditions. Additionally, industry standards such as SAE J2954 for wireless charging require advanced sealing solutions with IP69K ratings to ensure resistance against water and dust ingress. For example, Tesla’s 4680 battery cells utilize nearly 10 seals per battery pack, indicating strong volume demand.

According to IDRA projections, global EV battery production could reach 500 million units annually by 2033, generating demand for nearly 1 million tons of elastomer materials. Furthermore, advanced manufacturing techniques such as liquid injection molding allow precision levels of up to 0.1 mm, significantly improving product quality. These innovations also reduce failure rates by nearly 50%, making high-performance elastomer seals critical for long-term EV reliability and safety.

Restraints - Fluctuating Fluorochemical Prices, Supply Chain Concentration, And Regulatory Pressures Significantly Impact Production Costs and Availability of Elastomer Materials

The high-performance elastomer market faces significant challenges due to volatility in key raw materials, particularly fluorochemicals. For instance, hydrogen fluoride (HF) prices surged by nearly 40% in 2025, according to ICIS, directly impacting the production cost of FKM materials. In addition, shortages of tetrafluoroethylene (TFE) monomers have disrupted operations at major manufacturing facilities, including those operated by leading companies like DuPont.

The global supply chain is also highly concentrated, with around 70% of production capacity located in China and Japan, increasing exposure to geopolitical risks and trade uncertainties. Regulatory pressures further add complexity, as REACH restrictions on PFAS precursors are expected to impact nearly 20% of existing elastomer formulations by 2027. These combined factors not only increase production costs but also create supply instability, making it difficult for manufacturers to maintain consistent pricing, secure long-term contracts, and ensure uninterrupted supply to end-use industries.

High Manufacturing Complexity, Expensive Tooling, And Production Inefficiencies Limit Scalability and Increase Operational Costs for Elastomer Manufacturers

The manufacturing of high-performance elastomers involves complex processes and high capital investment, which act as key barriers for market growth. For example, compression molding for FFKM materials requires specialized molds costing around US$ 500,000, with a limited lifespan of approximately 10,000 production cycles. Similarly, extrusion processes demand extremely high precision, often at micron-level tolerances, increasing operational complexity.

Emerging technologies such as 3D printing have not yet achieved TÜV certification for critical aerospace components, limiting their adoption to only about 5% in such high-reliability applications. In addition, production inefficiencies, including scrap rates of nearly 15%, further reduce profitability for manufacturers. These challenges increase overall production costs and limit scalability, particularly for smaller players, while also slowing down the adoption of innovative manufacturing methods across industries that require strict quality and safety standards.

Opportunities - Advancements in Semiconductor Manufacturing Create Demand for Ultra-Pure, High-Performance Sealing Solutions Supporting Extreme Vacuum and Chemical Environments

The rapid advancement of semiconductor manufacturing, particularly at the 2nm node level, is creating strong demand for ultra-high-performance sealing solutions. Extreme ultraviolet (EUV) lithography processes require vacuum environments with extremely low outgassing, making advanced FFKM materials such as Chemours Kalrez highly suitable. These materials can withstand aggressive ArF chemicals and operate efficiently under ultra-high vacuum conditions of up to 10-9 Torr.

According to the SEMI roadmap, global wafer production is expected to reach 50 exawafers annually by 2030, further driving demand for high-purity sealing solutions. In addition, major investments such as TSMC’s Arizona facility, which includes a 20,000 m² cleanroom, highlight the scale of expansion in semiconductor manufacturing. Innovations like Parker’s Spectrum series have demonstrated the ability to reduce plasma etching downtime by up to 40%, improving operational efficiency. As a result, the high-purity semiconductor sealing market is projected to reach approximately US$ 500 million.

Expansion of Offshore Wind and Hydrogen Energy Sectors Drives Demand for Durable, Long-Lasting Elastomer Sealing Solutions In Harsh Environments

The growing renewable energy sector presents significant opportunities for high-performance elastomers, particularly in demanding environments such as offshore wind and hydrogen production. Floating offshore wind turbines are exposed to harsh conditions, including saltwater corrosion and wind speeds of up to 100 m/s, requiring durable FKM-based sealing solutions that can last over 20 years. According to the Global Wind Energy Council (GWEC), global offshore wind capacity is expected to reach 380 GW by 2030, driving substantial demand for advanced sealing materials.

Projects like Ørsted’s Hornsea wind farm already utilize Trelleborg Turcon components capable of withstanding up to 10 million operational cycles. Additionally, hydrogen electrolyzers operating at pressures of 80 bar and temperatures of 80°C require specialized AEM diaphragms for efficient performance. The International Renewable Energy Agency (IRENA) forecasts hydrogen capacity to reach 680 GW, further strengthening long-term growth opportunities in this segment.

Category-wise Analysis

Product Type Insights

Fluorocarbon elastomers (FKM) currently dominate the product type segment, accounting for approximately 42% of the global market share. Widely recognized grades such as Viton and Tecnoflon offer excellent resistance to harsh chemicals, jet fuels, and oils, while maintaining performance at temperatures up to 250°C, as defined by ASTM D1418 standards. The aerospace sector represents the largest consumer, contributing nearly 60% of total FKM demand due to the need for reliable sealing in critical applications.

Dow reports that FKM materials provide up to five times better compression set resistance compared to traditional nitrile rubber (NBR), enhancing durability and performance. Beyond aerospace, FKM seals are extensively used in oil and gas applications, where they must withstand extreme downhole conditions, including exposure to hydrogen sulfide (H2S). These performance advantages make FKM a preferred material across industries requiring high reliability, chemical resistance, and long operational life.

Processing Method Insights

Injection molding is the leading processing method in the high-performance elastomers market, accounting for nearly 55% of total production. This technique is particularly suitable for high-volume manufacturing of precision components such as O-rings used in electric vehicles and industrial systems. It enables tight dimensional tolerances of up to 0.05 mm, ensuring consistent product quality.

Materials like liquid silicone rubber (LSR), especially those with 55 durometer hardness, offer excellent flow characteristics and process up to ten times faster than FFKM materials. Automotive Tier 1 suppliers increasingly rely on injection molding to achieve large-scale production, with capabilities reaching up to one million parts per hour. The method also supports automation and reduces labor dependency, making it highly efficient and cost-effective. As demand for high-precision elastomer components continues to grow, injection molding remains a critical technology supporting scalability and quality across multiple industries.

Application Insights

Seals and gaskets represent the largest application segment in the high-performance elastomers market, contributing approximately 35% of total demand. These components play a crucial role in preventing fluid leakage and maintaining system integrity in critical applications. For instance, FKM static seals are widely used in turbopumps to prevent leakage of liquid oxygen (LOX), ensuring safety and efficiency in aerospace systems.

Organizations like NASA specify advanced materials such as Parker 4079 for missions like Artemis, highlighting the importance of high-performance sealing solutions. In addition, dynamic lip seals are increasingly used in electric vehicle motors, where they help reduce oil consumption by up to 30%, improving overall system efficiency. The growing adoption of advanced sealing technologies across aerospace, automotive, and industrial applications is driving continuous innovation, making seals and gaskets a key segment supporting performance, reliability, and operational safety.

End-user Insights

The automotive sector leads the end-use segment, accounting for approximately 28% of the high-performance elastomers market. The rapid transition toward electric vehicles is a major growth driver, as EV powertrains require advanced sealing materials capable of operating at temperatures up to 150°C. High-performance elastomers such as FFKM are increasingly used to ensure thermal stability and long-term reliability.

Industry standards set by SAE mandate durability requirements of up to 10 years, further increasing the need for high-quality sealing solutions. In addition, China’s strong growth in new energy vehicles (NEVs) is significantly boosting demand for elastomer components, with companies like BYD utilizing advanced gasket systems in their blade battery technology. These developments highlight the critical role of elastomers in enhancing vehicle performance, safety, and lifespan, positioning the automotive industry as a key contributor to overall market growth.

Regional Insights

North America High Performance Elastomers Market Trends

North America remains a key market for high-performance elastomers, driven primarily by strong demand from the aerospace and defense sectors. The United States, in particular, leads in advanced aircraft manufacturing, with companies like Boeing and GE requiring high-performance FFKM seals for applications such as F-35 actuators. Regulatory standards such as FAA Part 25 further ensure the adoption of certified sealing solutions from manufacturers like Parker.

The U.S. Department of Energy (DOE) supports research into advanced materials, including silicone-based solutions for solid oxide fuel cells. The region also benefits from a growing electric vehicle ecosystem, particularly in Silicon Valley, where startups are integrating liquid silicone rubber (LSR) into sensor technologies. Space exploration initiatives further boost demand, with SpaceX’s Raptor engines using specialized perfluoroelastomers, supported by NASA contracts worth approximately US$ 100 million, strengthening innovation and market growth.

Europe High Performance Elastomers Market Trends

Europe represents a mature yet innovation-driven market for high-performance elastomers, supported by strong automotive and aerospace industries. Germany’s leading automotive manufacturers are increasingly adopting FKM materials for electric axle (e-axle) systems to improve performance and durability. At the same time, regulatory frameworks such as REACH Annex XVII impose strict controls on chemical usage, encouraging the development of safer and more sustainable alternatives.

Aerospace companies in the UK and France, including Safran and BAE Systems, specify high-performance materials like Viton for advanced aircraft engines such as Rafale. In addition, renewable energy projects across Spain are utilizing durable components like Trelleborg Orkot bearings in wind farms. The European Green Deal further promotes sustainability by mandating up to 50% recycled content in materials, driving research and development efforts in bio-based silicone and eco-friendly elastomers across the region.

Asia Pacific High Performance Elastomers Market Trends

Asia Pacific dominates the global high-performance elastomers market, supported by rapid industrialization and strong manufacturing capabilities. China plays a key role in semiconductor production through companies like SMIC, while Japan’s Shin-Etsu supplies ultra-high purity silicone rubber (99.99%) for advanced lithography equipment used by global leaders. India’s “Make in India” initiative is further boosting domestic manufacturing, with companies like Tata Motors expanding electric vehicle production and increasing demand for advanced sealing solutions.

In Southeast Asia, oil and gas operations continue to rely heavily on FKM materials for durability in harsh environments. Additionally, global electronics manufacturing is driving demand, with companies like Foxconn using fluorosilicone materials in iPhone cabling. Semiconductor giant TSMC alone accounts for nearly 20% of global FFKM consumption, highlighting the region’s critical role in driving demand and innovation in high-performance elastomers.

Competitive Landscape

The high-performance elastomers market is oligopolistic in nature, with major players such as Dow, Chemours, and Daikin collectively holding around 60% of the global market share through strong patent portfolios, including well-known products like Viton, Kalrez, and Dynel. These companies are expanding their production capabilities through toll manufacturing, particularly in China, to meet growing global demand. Continuous investment in research and development is focused on emerging applications such as hydrogen-based systems and advanced AEM technologies.

Market players are also differentiating themselves through certifications such as ISO 9001 and AS9100, ensuring compliance with strict quality standards required in aerospace and automotive industries. In addition, the adoption of digital technologies, including digital twins for molding simulation, is improving efficiency and product design. A growing trend toward servitization is also emerging, with companies offering predictive maintenance solutions using IoT-enabled smart sealing systems.

Key Developments:

- In January, 2026: Chemours launched Viton Bio, a bio-based FKM with 30% renewable content, aligning with EV sustainability mandates. The product supports OEM decarbonization goals while maintaining high heat and chemical resistance required for advanced automotive and industrial sealing applications.

- In September, 2025: Wacker Chemie expanded its production capacity in China by adding 50 kilotons of liquid silicone rubber (LSR). This expansion targets rising demand from semiconductor manufacturing, particularly for high-precision gasket applications requiring purity, durability, and high thermal stability.

- In April, 2025: Dow and Evonik formed a strategic partnership to develop advanced silicone-acrylate hybrid materials. These materials are designed for extreme environments, including space reentry applications, offering enhanced thermal resistance, flexibility, and durability for next-generation aerospace sealing technologies.

Companies Covered in High Performance Elastomers Market

- Avient Corporation

- Chemours

- Dow

- Envalior

- Evonik AG

- ExxonMobil

- First Graphene

- Mitsubishi Chemical Group Corporation

- Mitsui Plastics, Inc.

- Radici Group

- Wacker Chemie AG

- Momentive

- Shin-Etsu Chemical

- Solvay

- Daikin Industries

- Parker Hannifin

- Trelleborg

Frequently Asked Questions

The high elastomers market is projected to hit US$ 37.6 Billion by 2033 at 5.6% CAGR, powered by EV/aerospace sealing.

Turbofan FFKM o-rings and EV thermal gaskets amid FAA/SAE durability mandates.

FKM at 42% share for unmatched fuel/heat resistance in aerospace/auto.

Asia Pacific leads via TSMC/SMIC semicon vacuum seals and BYD EV production.

EUV 2nm fab ultra-low outgassing perfluoro gaskets for 50 exawafers scale.

Dow, Chemours, Daikin, Wacker, Shin-Etsu excel in fluorinated formulations.