- Semiconductor Materials & Components

- GPON Technology Market

GPON Technology Market Size, Share, and Growth Forecast, 2026 - 2033

GPON Technology Market by Technology Type (2.5G PON, XG-PON, XGS-PON, NG-PON2), Component (Optical Network Terminal (ONT), Optical Line Terminal (OLT)), Application (FTTH, Other FTTx, Mobile Backhaul), and Regional Analysis for 2026 - 2033

GPON Technology Market Size and Trends Analysis

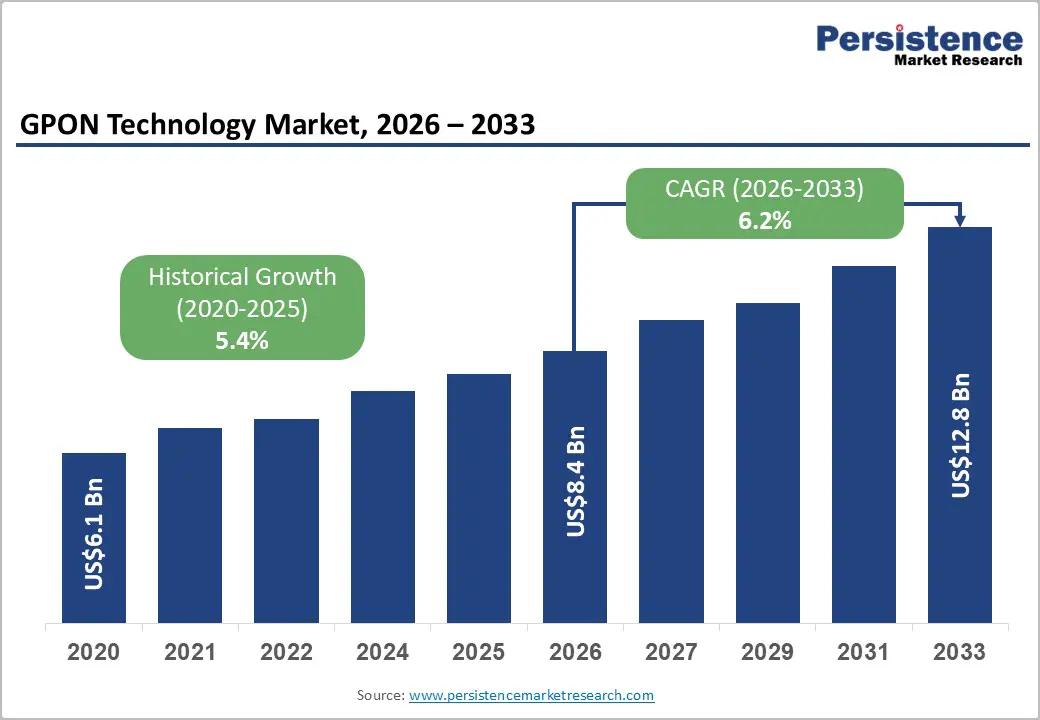

The global GPON technology market size is likely to be valued at US$8.4 billion in 2026 and is expected to reach US$12.8 billion by 2033, growing at a CAGR of 6.2% during the forecast period from 2026 to 2033, driven by telecom operators worldwide accelerate fiber broadband deployments to support rising data consumption, cloud applications, remote work, smart homes, IoT, and 5G backhaul networks.

GPON remains a foundational technology for Fiber-to-the-Home (FTTH) and Fiber-to-the-Building (FTTB) infrastructure due to its cost efficiency, scalability, and ability to deliver high-speed connectivity. According to the latest FTTH Council Europe Market Panorama 2026, full-fiber networks passed approximately 295 million homes across Europe by September 2025, representing 79% household coverage, while fiber adoption continued to grow significantly. The International Telecommunication Union (ITU) reported that global internet usage reached 74% of the world’s population in 2025, reflecting increasing demand for robust broadband infrastructure.

Key Industry Highlights:

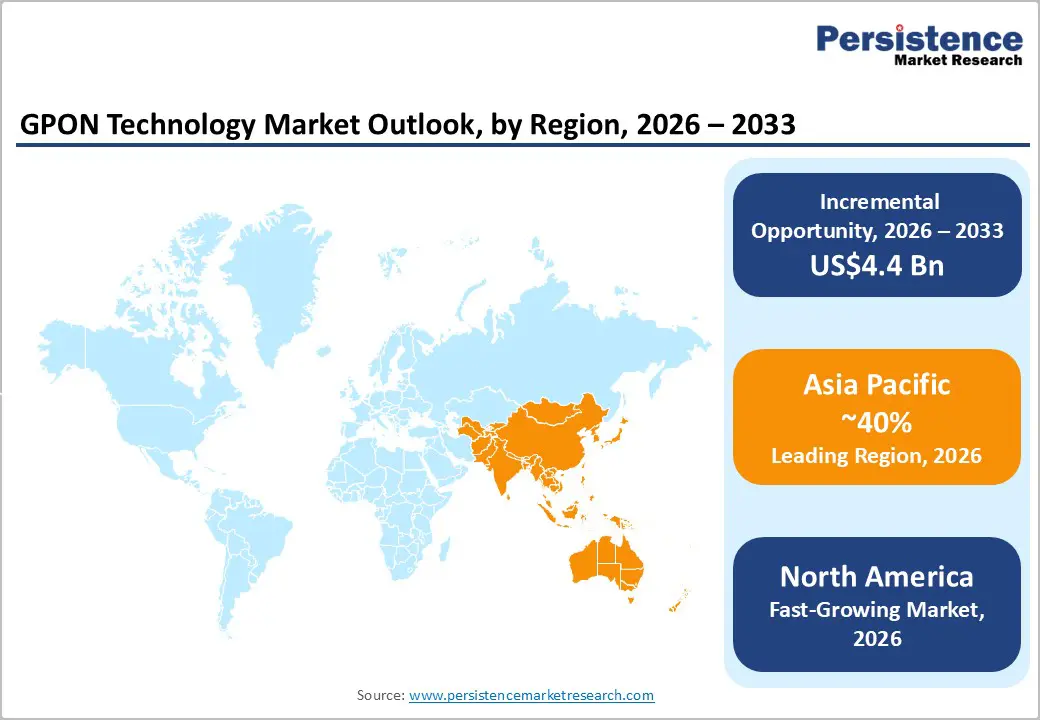

- Leading Region: Asia Pacific is anticipated to be the leading region, accounting for a market share of 40% in 2026, driven by large-scale fiber deployments, government-backed broadband initiatives, and rapid digital infrastructure development across major economies.

- Fastest-growing Region: North America is likely to be the fastest-growing region, supported by extensive fiber broadband deployment, 5G network expansion, and strong investment in next-generation access infrastructure.

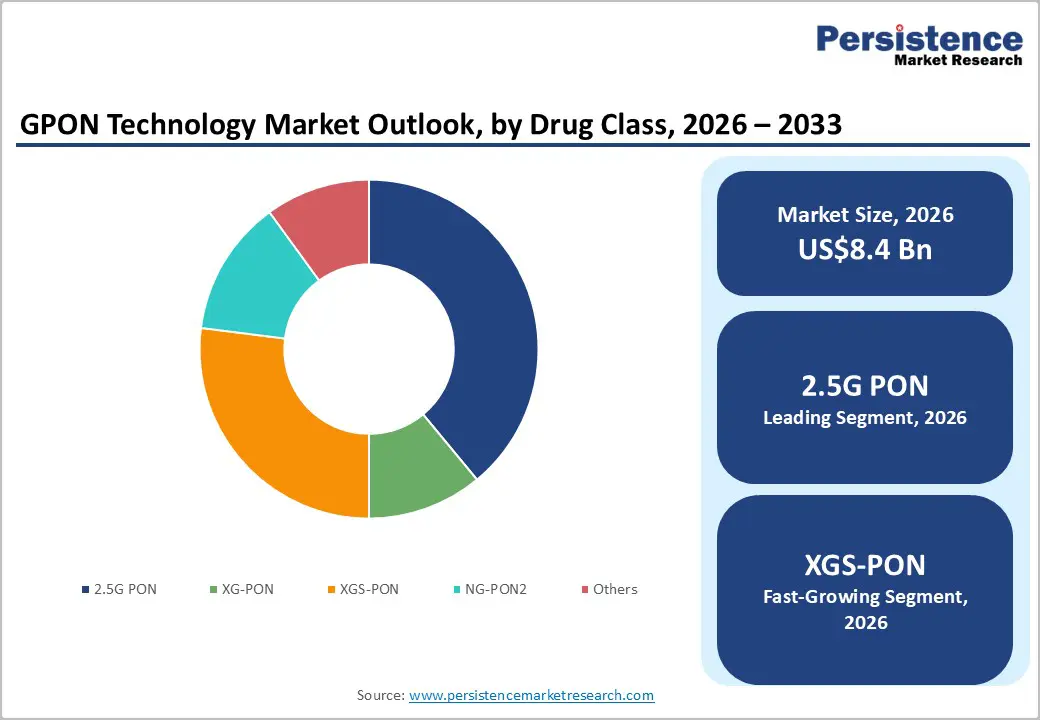

- Leading Technology Type: 2.5G PON is projected to represent the leading technology type in 2026, accounting for 55% of the revenue share, due to its extensive installed base and broad deployment across fiber access networks.

- Leading Component: Optical line terminal (OLT) is anticipated to be the leading component, accounting for over 60% of the revenue share in 2026, supported by its central role in network architecture and higher system value.

- Key Opportunity: The accelerating expansion of fiber-optic broadband networks and the transition toward next-generation multi-gigabit PON technologies create substantial growth opportunities across residential, enterprise, and 5G connectivity applications.

DRO Analysis

Driver - Rising Demand for High-Speed Broadband and Digital Transformation

Consumers and enterprises increasingly rely on bandwidth-intensive applications such as ultra-high-definition video streaming, cloud computing, online gaming, virtual collaboration platforms, and digital learning environments. GPON technology provides a scalable and cost-efficient solution for delivering reliable fiber-based internet services to residential and commercial users.

As internet traffic continues to increase, telecom operators are expanding fiber networks to meet customer expectations for faster and more stable connections. This trend is accelerating investments in GPON infrastructure across both developed and emerging economies worldwide. Digital transformation initiatives across industries are strengthening demand for GPON deployments.

Governments, businesses, healthcare providers, educational institutions, and smart city projects require robust communication networks capable of supporting connected devices and data-intensive services. GPON enables efficient delivery of high-capacity broadband while reducing operational costs through passive network architecture. The rapid adoption of IoT solutions, artificial intelligence applications, edge computing, and cloud-based platforms is increasing the need for dependable fiber infrastructure.

Restraint - Technological Obsolescence and Migration Risks

Emerging technologies such as XGS-PON and NG-PON2 offer enhanced performance, creating concerns among operators regarding the long-term viability of existing GPON infrastructure. Telecom providers often face challenges in balancing current investments with future upgrade requirements. As customer demand for multi-gigabit services grows, some operators delay deployment decisions while evaluating next-generation alternatives.

Migration from legacy GPON systems to advanced passive optical network technologies can involve substantial operational and financial challenges. Network upgrades require equipment replacement, compatibility assessments, workforce training, and service continuity planning. Operators must carefully manage coexistence between older and newer technologies while minimizing disruption to subscribers.

Opportunity - Technological Convergence and Customization

Telecom operators are increasingly adopting upgrade strategies that enable a seamless transition toward XGS-PON and NG-PON2 architectures while leveraging existing fiber assets. These advanced technologies support substantially higher bandwidth capabilities, improved service flexibility, and enhanced network efficiency.

Demand for multi-gigabit broadband services is expanding among residential users, enterprises, and public institutions, creating favorable conditions for network modernization. Vendors that provide interoperable and scalable solutions can benefit from rising investments aimed at supporting future digital infrastructure requirements across markets. Growing adoption of smart homes, cloud applications, industrial automation, and 5G mobile networks is creating new opportunities for multi-gig service deployment.

Advanced passive optical network technologies enable operators to deliver premium broadband packages, low-latency connectivity, and higher-value digital services. The ability to support increasing numbers of connected devices while maintaining network performance enhances the attractiveness of next-generation fiber solutions.

Category-wise Analysis

Technology Type Insights

2.5G PON is expected to account for 55% of revenue in 2026, due to its extensive deployment across fiber broadband networks worldwide. Telecom operators continue to rely on this technology because it offers a proven combination of performance, reliability, and cost-efficiency for residential and small business connectivity. A notable example includes Huawei’s GPON deployments across multiple broadband projects globally, where operators continue using 2.5G PON solutions to expand fiber access and improve connectivity coverage.

XGS-PON is likely to represent the fastest-growing segment, supported by increasingly upgraded networks to support higher bandwidth requirements and future digital services. Demand for symmetrical multi-gigabit speeds is rising due to cloud computing, ultra-high-definition streaming, enterprise connectivity, smart homes, and data-intensive applications. For example, Nokia’s XGS-PON deployments with broadband operators enable the delivery of next-generation fiber services and support growing demand for high-capacity network connectivity.

Component Insights

Optical line terminal (OLT) is projected to lead the market, capturing around 60% of the revenue share in 2026. OLT systems serve as the central control point within passive optical networks, managing communication between service provider networks and multiple subscriber endpoints. OLT platforms also facilitate integration with evolving technologies, making them essential for long-term network modernization strategies. For instance, ZTE’s OLT product portfolio is widely deployed by telecom operators to support large-scale fiber broadband networks and growing connectivity requirements.

Optical network terminal (ONT) is likely to be the fastest-growing component due to rising demand for high-speed broadband services. ONTs act as the customer-side endpoint that converts optical signals into usable internet, voice, and data services. A notable example includes Calix, which offers advanced subscriber-premises solutions that help broadband providers deliver enhanced user experiences and support growing demand for high-performance fiber connectivity.

Application Insights

FTTH is expected to account for 58% of revenue in 2026, due to strong demand for residential broadband connectivity. FTTH enables the delivery of high-speed, reliable broadband services directly to households, making it ideal for streaming, online education, remote work, gaming, and cloud-based applications. For example, FiberHome’s participation in large-scale FTTH projects supports broadband expansion initiatives and increases fiber connectivity.

Mobile backhaul is likely to represent the fastest-growing segment, supported by telecom operators accelerating 5G deployment and network densification strategies. Modern mobile networks require high-capacity, low-latency transport infrastructure capable of handling increasing data traffic generated by smartphones, connected devices, and advanced digital services. For instance, Nokia’s fiber-based mobile transport solutions, which support telecom operators in enhancing 5G network performance and capacity.

Regional Insights

North America GPON Technology Market Trends

North America is likely to be the fastest-growing region, supported by rising demand for gigabit internet services, cloud applications, remote work environments, and connected devices, which are driving investments in fiber-based access networks. A notable example includes Calix, which continues expanding its broadband platform portfolio to help service providers deliver advanced fiber services and improve subscriber experiences.

U.S. GPON Technology Market Trends

The U.S. is expected to dominate the regional market, accounting for approximately 87% of the market share in 2026, driven by extensive fiber infrastructure investments and high broadband demand. Telecom operators are accelerating FTTH deployment to support growing data consumption. Federal broadband funding initiatives continue encouraging fiber expansion in rural and underserved regions. The rapid rollout of 5G networks is increasing demand for fiber-based backhaul infrastructure.

Canada GPON Technology Market Trends

Canada is likely to be a significant market for GPON technology, holding approximately 13% of the market share in 2026, supported by increasing GPON adoption as operators expand fiber coverage across urban and remote communities. Growing demand for high-speed internet, remote work capabilities, and digital services is encouraging network expansion. Canadian telecom providers are accelerating FTTH projects to improve service quality and coverage.

Europe GPON Technology Market Trends

Europe is likely to be a significant market for GPON technology, due to extensive fiber rollout programs, digital transformation initiatives, and regulatory support for high-speed broadband infrastructure. Countries across the region continue replacing legacy networks with fiber-based systems to improve connectivity and support growing digital economies. For example, Nokia which continues supporting European telecom operators with advanced GPON and XGS-PON solutions for next-generation broadband network deployments.

U.K. GPON Technology Market Trends

The U.K. is likely to be a significant market for GPON technology, estimates for 15% of Europe market share in 2026. Telecom providers are expanding full-fiber networks to improve nationwide connectivity. Increasing demand for streaming, cloud applications, and remote working services is driving fiber adoption. Network operators are upgrading access infrastructure to support higher-speed broadband offerings.

Germany GPON Technology Market Trends

Germany is anticipated to dominate the regional market, accounting for around 37% of the Europe market share in 2026. The country is accelerating fiber expansion to improve national digital infrastructure. Government initiatives continue encouraging broadband deployment across residential and business sectors. Telecom operators are expanding FTTH coverage to strengthen broadband availability.

Asia Pacific GPON Technology Market Trends

The Asia Pacific region is anticipated to be the leading region, accounting for a market share of 40% in 2026. Its large-scale fiber deployments, expanding broadband penetration, rapid urbanization, and strong government support for digital infrastructure. For instance, Huawei Technologies which continues supplying GPON and XGS-PON solutions for large-scale broadband projects.

China GPON Technology Market Trends

China is projected to dominate the regional market, holding around a 30% share in 2026, due to its extensive fiber broadband infrastructure. The country continues investing heavily in nationwide digital connectivity projects. Telecom operators are expanding advanced fiber networks to support growing data traffic. Strong government support for digital transformation and smart city initiatives is accelerating deployment.

India GPON Technology Market Trends

India is expected to emerge as a significant market, accounting for approximately a 22% share in 2026, due to increasing internet penetration and rising consumption of digital services, which are supporting network expansion. Telecom operators are investing heavily in FTTH infrastructure to meet growing bandwidth demand. The rapid growth of cloud services, online education, and digital commerce is driving fiber deployment.

Competitive Landscape

The global GPON technology market exhibits a moderately fragmented structure, driven by increasing investments in fiber broadband infrastructure, growing demand for high-speed internet connectivity, and the ongoing transition toward next-generation passive optical network technologies.

With key leaders including Huawei Technologies, Nokia, ZTE Corporation, Cisco Systems, Calix, ADTRAN, FiberHome, and Mitsubishi Electric, the market remains highly innovation-focused. These players compete through product innovation, network performance enhancements, strategic partnerships with telecom operators, portfolio expansion into XGS-PON and NG-PON2 technologies, pricing strategies, and service capabilities.

Key Industry Developments:

- In April 2026, Broadcom launched its optimized 10G PON and Wi-Fi 8 solutions for mass-market broadband deployments, introducing the BCM68565 gateway SoC with integrated XGS-PON and GPON support to help service providers deliver reliable multi-gigabit fiber connectivity, lower latency, and improved network performance while accelerating the transition from legacy broadband infrastructure.

- In October 2025, ZTE unveiled a comprehensive optical access portfolio at Network X 2025, introducing new compact PON OLT solutions, Wi-Fi 7 access points with XGS-PON uplinks, an AI-powered Wi-Fi 7 router, and its Smart Cloud Platform (SCP) to accelerate FTTx deployments, support smart home evolution, and advance all-optical 10G network infrastructure worldwide.

Companies Covered in GPON Technology Market

- Huawei

- Nokia

- ZTE

- Cisco

- Calix

- ADTRAN

- FiberHome

- Mitsubishi Electric

Frequently Asked Questions

The global GPON technology market is projected to reach US$8.4 billion in 2026.

Rising demand for high-speed broadband connectivity, FTTH deployments, digital transformation initiatives, and expanding 5G infrastructure are driving the GPON technology market.

The GPON technology market is expected to grow at a CAGR of 6.2% from 2026 to 2033.

Growing adoption of XGS-PON and NG-PON2 technologies, along with expanding fiber broadband and multi-gigabit service deployments, presents significant market opportunities.

Huawei, Nokia, ZTE, Cisco, Calix, ADTRAN, and FiberHome are the leading players.