- Construction & Engineering

- Fly Ash Market

Fly Ash Market Size, Share, and Growth Forecast 2026 - 2033

Fly Ash Market by Ash Type (Class F, Class C), Application (Portland Cement & Concrete, Bricks and Blocks, Road Construction, Agriculture, Water Treatment, Other), and Regional Analysis for 2026 - 2033

Fly Ash Market Size and Trend Analysis

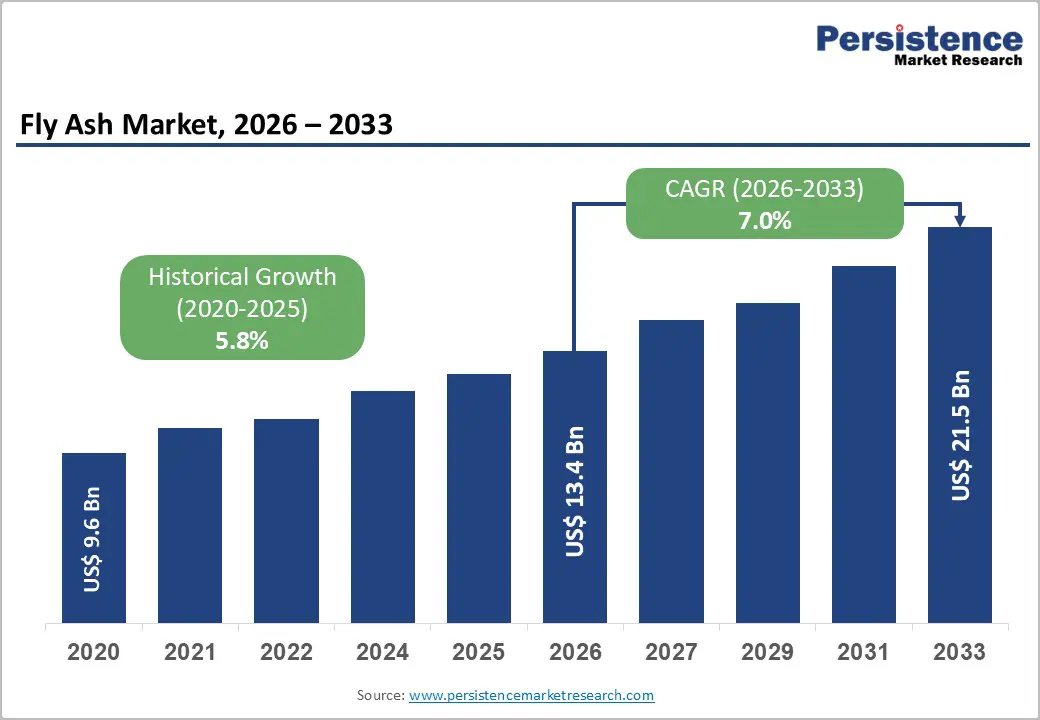

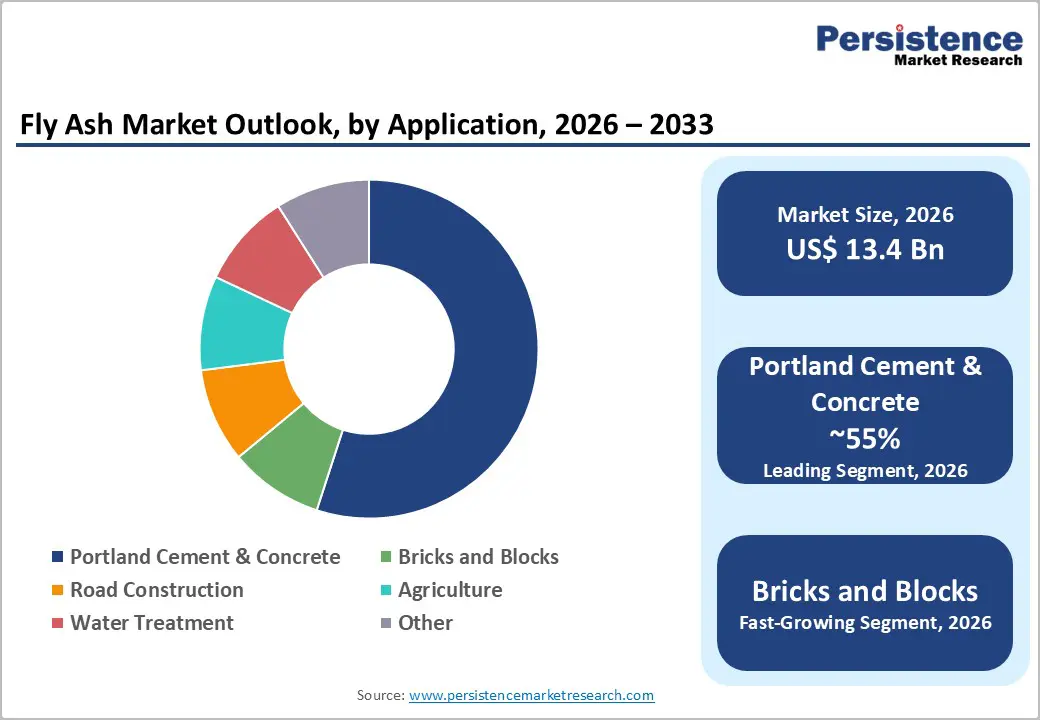

The global fly ash market size is valued at US$ 13.4 billion in 2026 and is projected to reach US$ 21.5 billion by 2033, growing at a CAGR of 7.0% between 2026 and 2033.

Robust growth is primarily driven by the global construction industry's accelerating pivot toward supplementary cementitious materials, mounting regulatory mandates on carbon intensity reduction in cement production, and large-scale urbanization across Asia-Pacific, South Asia, and sub-Saharan Africa. Fly ash offers a cost-effective and technically superior substitute for clinker, reducing CO2 emissions by approximately 0.9 tons per ton of cement clinker displaced. Historical momentum, with a CAGR of 5.8% between 2020 and 2025, underscores the market's structural demand resilience.

Key Industry Highlights:

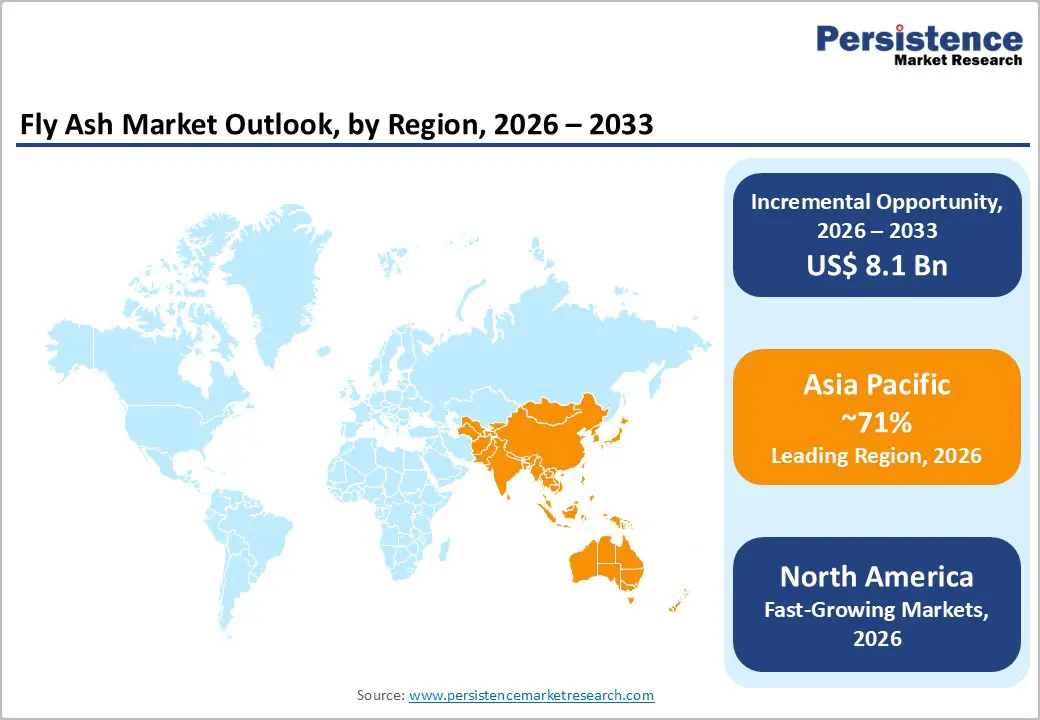

- Regional Leader: Asia Pacific dominates the global fly ash market with approximately 71% revenue share in 2025, propelled by India's 98% fly ash utilization rate in FY 2024–25 and China's sustained infrastructure investment across housing, highways, and industrial construction.

- Fastest Growing Region: North America is projected to record the highest regional CAGR of approximately 7.2% (2025–2030), driven by EPA's Legacy CCR Rule, Buy Clean Concrete mandates, and a robust pipeline of ash harvesting projects from legacy utility impoundments.

- Leading Segment: Class F fly ash commands approximately 62% of global market share due to its superior pozzolanic properties, including enhanced compressive strength, reduced permeability, and alkali-silica reaction resistance, making it the preferred grade for infrastructure-grade and ready-mix concrete applications.

- Fastest Growing Segment: The Portland Cement & Concrete segment is the fastest growing segment, growing at a CAGR of approximately 7.46% through 2030 as green building regulations and clinker-replacement economics drive adoption of fly ash blended cements in all major markets.

- Key Market Opportunity: The multi-billion-dollar opportunity in legacy coal ash pond remediation, catalyzed by the U.S. EPA's 2024 regulatory framework, is unlocking high-volume feedstocks for beneficiation, with companies like Eco Material Technologies and Heidelberg Materials already processing millions of tons annually from impoundments.

| Key Insights | Details |

|---|---|

|

Fly Ash Market Size (2026E) |

US$ 13.4 Bn |

|

Market Value Forecast (2033F) |

US$ 21.5 Bn |

|

Projected Growth CAGR (2026–2033) |

7.0% |

|

Historical Market Growth (2020–2025) |

5.8% |

DRO Analysis

Drivers - Infrastructure-Led Demand Surge in Emerging Economies

The single most impactful growth driver for the fly ash market is the unprecedented scale of infrastructure investment in emerging economies, particularly India and China. India alone generated 340.11 million tons of fly ash in FY 2024–25, of which 332.63 million tons (approximately 97.8%) were successfully utilized across construction, cement, and agricultural applications, according to data from the Ministry of Railways and NTPC.

The U.S. Census Bureau reported that U.S. construction spending reached US$ 1.8 trillion, creating substantial demand for fly ash across road, residential, and commercial projects. According to Invest India, India's construction industry is anticipated to reach US$ 1.4 trillion by 2025. These multi-decade capital expenditure cycles ensure a structurally embedded demand stream that reinforces the market's long-term trajectory.

Regulatory Mandates on Carbon Reduction in Cement Production

Tightening environmental regulations across major economies are systematically compelling cement producers to increase fly ash substitution rates. The U.S. Environmental Protection Agency (EPA) finalized the Legacy Coal Combustion Residuals (CCR) Surface Impoundments Rule in May 2024, which incentivizes beneficial reuse of fly ash over landfilling. In France, the RE2020 energy and climate code progressively ratchets down embodied-carbon ceilings for residential construction, incentivizing fly ash blends.

Ireland mandates a 30% clinker substitute in all state-funded projects. India's Ministry of Environment, Forest, and Climate Change (MoEFCC) mandates 100% utilization of fly ash by thermal power plants. These regulatory frameworks collectively convert speculative fly ash adoption into a structural market requirement, creating predictable, policy-backed demand for market participants.

Restraints - Declining Coal-Fired Power Generation and Supply Uncertainty

A critical restraint for the fly ash market is the progressive phasedown of coal-fired power generation across Europe and North America as governments advance net-zero commitments. As coal plants retire, the domestic supply of fresh fly ash diminishes, compelling concrete producers to source ash from greater distances or develop alternative supplementary cementitious materials.

In Germany, the planned coal exit by 2038 will significantly reduce indigenous fly ash supply, impacting the regional construction materials chain. This supply-demand mismatch elevates raw material risk and can increase procurement costs, tempering market growth in coal-transitioning regions.

Quality Variability and Lack of Standardization

Fly ash quality varies considerably based on coal type, combustion temperature, and power plant operational parameters, creating inconsistency that limits its use in high-performance concrete applications. The American Coal Ash Association (ACAA) has noted that unprocessed pond ash, in particular, often fails to meet ASTM C618 performance thresholds due to elevated carbon content and variable calcium levels. This inconsistency forces concrete producers to invest in costly quality testing protocols or resort to beneficiation, adding to material costs and limiting adoption in specifications-sensitive projects. Without harmonized international quality standards, market expansion remains constrained in regions with emerging regulatory frameworks.

Opportunities - Ash Harvesting from Legacy Impoundments: A New Feedstock Frontier

The U.S. Environmental Protection Agency’s Legacy Coal Combustion Residuals (CCR) Surface Impoundments Rule, enacted in May 2024, has created a significant commercial opportunity in the recovery of fly ash from legacy storage ponds. This regulation has accelerated large-scale ash harvesting initiatives, exemplified by Georgia Power’s 15-year agreement with Eco Material Technologies to dredge approximately 8 million tons of stored ash, as well as Consumers Energy’s plan to beneficiate 6 million tons from the J.H. Campbell site.

Further underscoring the strategic and financial importance of this segment, CRH completed the acquisition of Eco Material Technologies for US$ 2.1 billion in July 2025. Moreover, investments in advanced beneficiation solutions, such as Heidelberg Materials’ Staged Turbulent Air Reactor (STAR) technology, enable producers to convert previously landfilled ash into high-quality supplementary cementitious materials, thereby strengthening supply security and competitive positioning amid declining availability of freshly generated fly ash.

Green Cement and Low-Carbon Concrete: Structural Demand Catalyst

The global shift toward low-carbon construction represents a substantial and long-term growth opportunity for the fly ash market. The substitution of cement clinker with fly ash delivers measurable environmental benefits, as each ton of clinker displaced avoids approximately 0.9 ton of carbon dioxide emissions. Policy initiatives are reinforcing this transition: in 2025, the New York State Office of General Services implemented Buy Clean Concrete Guidelines, requiring Environmental Product Declarations for state-funded projects exceeding US$ 1 million in value.

Parallel industry actions further support market expansion. In India, JSW Cement commenced the development of zero-clinker cement formulations in 2024 using fly ash and ground-granulated blast-furnace slag. Additionally, in March 2025, Boral Limited secured a US$ 24.5 million federal grant to increase alternative raw material usage in kiln feed from 9% to 23%. Collectively, these regulatory and technological developments are elevating fly ash from a low-value by-product to a strategically important sustainable construction material.

Category-wise Analysis

Ash Type Insights

Class F fly ash is the dominant segment by ash type, accounting for approximately 62% of global market share in 2025. Produced from the combustion of anthracite and bituminous coals, Class F ash is composed predominantly of alumino-silicate glass along with quartz, mullite, and magnetite, and contains less than 10% calcium oxide (CaO). Its market dominance is attributable to superior pozzolanic properties, including enhanced late compressive strength, improved resistance to alkali-silica reaction (ASR), reduced permeability, and lower heat of hydration.

In Portland cement production, Class F ash is used as a substitution at 20–30% of cementitious materials, making it the preferred grade for infrastructure-grade ready-mix concrete and high-durability precast applications. The adoption of Class F ash is institutionally supported by standards such as ASTM C618 in the United States and IS 3812 in India, providing a well-defined technical framework that encourages specification-driven procurement.

Application Analysis

Portland Cement & Concrete is the leading application segment, accounting for approximately 55% of global fly ash consumption. Current estimates indicate that nearly 54% of total fly ash output is consumed in cement and blended materials, according to industry analyses. In India, 27% of FY 2024–25's total fly ash generation went directly to the cement industry, as documented by NTPC. The dominance of this segment stems from fly ash's technical role in producing Portland Pozzolana Cement (PPC), which accounts for the majority of cement consumed in Asia-Pacific markets.

PPC leverages fly ash to reduce clinker content, improve workability, and cut carbon emissions. The segment is expected to grow at a CAGR of approximately 7.46% through 2030, driven by green building mandates, public infrastructure outlays, and the economics of clinker-replacement in high-growth construction markets.

Regional Insights

North America Fly Ash Market Trends

North America represents a high-value and increasingly innovation-driven market for fly ash, led predominantly by the United States. Federal regulatory frameworks play a central role in shaping market dynamics, particularly the U.S. Environmental Protection Agency’s Legacy Coal Combustion Residuals Surface Impoundments Rule introduced in May 2024, which has fundamentally reoriented supply by encouraging the beneficial reuse of fly ash over landfilling.

Complementary procurement policies, such as New York State’s Buy Clean Concrete Guidelines implemented in 2025, along with similar initiatives in California and Massachusetts, are embedding fly ash into public infrastructure projects and generating sustained demand. Investments in rail-linked distribution terminals are improving the logistics of transporting harvested ash to urban centers. Regionally, North America is projected to record the highest growth rate, supported by infrastructure spending and ongoing technological advances in high-performance ash beneficiation.

Europe Fly Ash Market Trends

Europe occupies a strategically significant yet transitional role in the global fly ash market. Germany, historically a major producer of lignite-based Class C fly ash, is progressing toward a planned coal phase-out by 2038, resulting in a steady contraction of domestic supply. Despite declining ash generation, construction-sector demand remains structurally supported by the European Green Deal and revisions to the Construction Products Regulation, which harmonize standards for supplementary cementitious materials across EU member states.

France’s RE2020 framework and Ireland’s mandate for 30% clinker substitution collectively reinforce regulatory demand across the region. The United Kingdom is advancing embodied-carbon requirements in public procurement, expected to formalize fly ash usage by 2027. Spain and Poland continue to represent localized demand centers, although accelerated coal retirements under EU ETS cost pressures constrain long-term supply.

Asia Pacific Fly Ash Market Trends

Asia Pacific remains the dominant region in the global fly ash market, accounting for approximately 71% of total revenue in 2025. China and India constitute the principal demand centers, supported by sustained urbanization, large-scale affordable housing initiatives, and extensive national infrastructure programs. In FY 2024–25, India utilized over 332 million tons of fly ash, nearly 98% of total generation, reflecting the effectiveness of policy-driven utilization mandates and robust construction demand.

India’s urban population is projected to reach 600 million by 2036, underpinning a long-term pipeline for housing and infrastructure development. Across Southeast Asia, continued reliance on coal-fired power generation ensures abundant fly ash availability amid rapid construction growth. Japan represents a mature, high-specification market, particularly in precast and seismic-resistant applications. Regional geopolitical and logistics pressures further strengthen the preference for locally sourced fly ash solutions.

Competitive Landscape

The global fly ash market is characterized by a moderately consolidated competitive structure, dominated by several multinational corporations such as Heidelberg Materials AG, Holcim, and Eco Material Technologies. These companies command significant market share through vertically integrated supply chains, long-term utility agreements, and comprehensive ash management services. Market leaders differentiate themselves through advanced beneficiation technologies, assured supply arrangements, and certified Environmental Product Declarations that facilitate specification-driven public procurement. Strategic acquisitions remain the primary growth mechanism, reflecting efforts by major cement producers to internalize fly ash supply.

Key Market Developments

- July 2025: CRH (Dublin) announced the acquisition of Eco Material Technologies for US$ 2.1 billion, consolidating a leading position in North American near-zero-carbon cement and supplementary cementitious materials supply.

- March 2025: Boral Limited secured a US$ 24.5 million Federal grant to advance its kiln feed optimization project, increasing fly ash content in kiln feed from 9% to 23% and reducing CO2 emissions intensity.

- May 2023: Heidelberg Materials AG completed the acquisition of The SEFA Group (Lexington, South Carolina), the largest U.S. recycler of harvested fly ash, supplying over 800 concrete plants across 13 states, strengthening its supplementary cementitious material footprint in North America.

Top Companies in the Fly Ash Market

Heidelberg Materials AG (Heidelberg, Germany) is arguably the most strategically positioned player in the global fly ash market, following the acquisition of The SEFA Group in 2023 and ACE Group in 2024. With its evoBuild platform targeting 50% sustainable product revenue by 2030 and proprietary STAR beneficiation technology processing over 1 million tons per annum of pond ash, the company leads on both supply security and low-carbon product innovation.

Holcim (Jona, Switzerland) operates one of the most comprehensive fly ash product portfolios globally, underpinned by its ECOPlanet and ECOPact concrete suites that deliver a minimum 30% CO2 intensity reduction. The March 2024 launch of ECOAsh, a high-quality Class F fly ash reclaimed from landfills under its Lafarge operations in western Canada, demonstrates supply chain innovation. Holcim's forthcoming Amrize North American spin-off brand, confirmed in February 2025, will focus explicitly on low-carbon building solutions, including fly ash-integrated products.

Eco Material Technologies (Salt Lake City, U.S.) is the leading independent fly ash supplier in the United States, originally acquiring Boral's North American fly ash business for US$ 755 million in 2022. The company's expertise spans pond ash remediation, beneficiation, and commercial distribution, with active contracts involving millions of tons of legacy ash. Its acquisition by CRH for US$ 2.1 billion in 2025 underscores its market leadership and strategic value in North America's low-carbon construction materials ecosystem.

Companies Covered in Fly Ash Market

- Boral

- Charah Solutions Inc.

- Eco Material Technologies

- Heidelberg Materials AG

- Holcim

- Cement Australia Pty Limited

- Cemex SAB de CV

- Salt River Materials Group

- Separation Technologies LLC

- The SEFA Group LLC

- Ashtech Pvt Ltd.

- Titan America LLC

Frequently Asked Questions

The global fly ash market is valued at US$ 13.4 Bn in 2026 and is projected to reach US$ 21.5 Bn by 2033, growing at a CAGR of 7.0% during the forecast period.

Primary growth drivers include large-scale infrastructure investment in emerging economies such as India and China, tightening regulatory mandates on carbon intensity in cement production, cost advantages of fly ash as a clinker substitute (reducing CO₂ by approximately 0.9 tons per ton of clinker displaced), and advancing beneficiation technologies that unlock legacy ash pond feedstocks for commercial use.

Class F fly ash is the leading segment, holding approximately 62% of the global market share in 2025. Its dominance is driven by superior pozzolanic properties, including high resistance to alkali-silica reaction, enhanced compressive strength, and reduced permeability, making it the preferred grade for infrastructure-grade concrete and Portland cement applications.

Asia Pacific is the leading region, accounting for approximately 71% of global revenue share in 2025. The region's dominance is underpinned by massive construction activity in India and China, government-mandated fly ash utilization policies, and abundant supply from coal-fired thermal power plants. India alone generated 340.11 million tons of fly ash in FY 2024–25, achieving a 97.8% utilization rate.

The most significant near-term opportunity lies in ash harvesting from legacy coal combustion residual (CCR) impoundments. Catalyzed by the EPA's Legacy CCR Rule (May 2024), this opportunity is driving multi-billion-dollar contracts for pond remediation and beneficiation, converting landfilled ash into high-grade supplementary cementitious materials, while simultaneously addressing environmental liabilities of utilities, creating a win-win supply dynamic for fly ash market participants.

Leading market participants include Heidelberg Materials AG, Holcim, Eco Material Technologies (now a CRH company), Boral Limited, Cemex SAB de CV, Charah Solutions Inc., Titan America LLC, Salt River Materials Group, and Ashtech Pvt Ltd., among others. These companies compete through supply chain integration, technology innovation in beneficiation, and strategic partnerships with utilities.