- Biotechnology

- Fetal Bovine Serum Market

Fetal Bovine Serum Market Size, Share, and Growth Forecast 2026 - 2033

Fetal Bovine Serum Market by Product Type (Standard / Regular FBS, Charcoal Stripped FBS, Dialyzed FBS, Stem Cell Qualified FBS, Exosome Depleted FBS), by Application (Cell Culture & Research, Drug Discovery & Preclinical Studies, Biopharmaceutical, Vaccine Production, IVF & Diagnostics), End-user (Pharmaceutical & Biotech Companies, Contract Research Organizations (CROs), Academic & Research Institutes, Diagnostic Labs), and Regional Analysis, 2026 - 2033

Fetal Bovine Serum Market Share and Trends Analysis

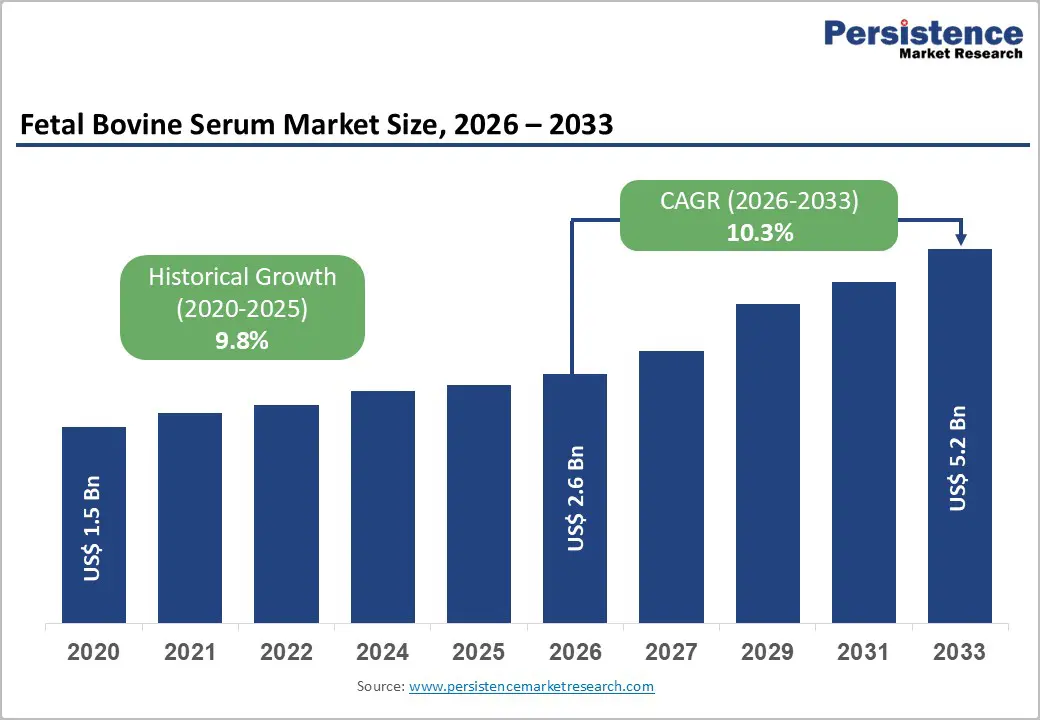

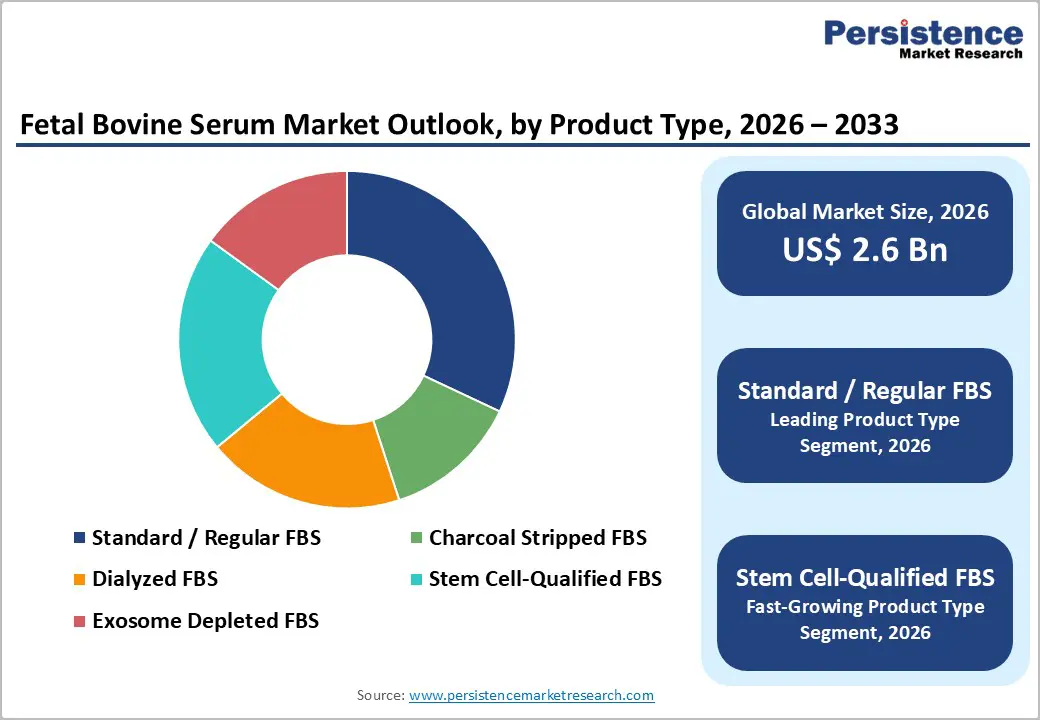

The global fetal bovine serum market size is expected to be valued at US$ 2.6 billion in 2026 and projected to reach US$ 5.2 billion by 2033, growing at a CAGR of 10.3% between 2026 and 2033. The market expansion is primarily driven by accelerating demand for biologics and cell-based therapies across global pharmaceutical pipelines.

The biopharmaceutical industry's pivot toward personalized medicine and advanced therapeutic modalities, including CAR-T cell therapies and regenerative medicine, has intensified the requirement for high-quality cell culture supplements. According to industry developments, the global cell and gene therapy contract research organizations market reached US$ 4.82 billion in 2024 and is projected to grow at a CAGR of 9.84%, underscoring the escalating demand for specialized cell culture reagents like FBS. Additionally, vaccine production capacity expansions driven by pandemic preparedness initiatives and growing adoption of stem cell research across academic and research institutes worldwide create sustained demand for specialized FBS grades, including stem cell-qualified and exosome-depleted formulations.

Key Industry Highlights:

- Leading Region: North America dominates the fetal bovine serum market with approximately 37% share in 2025, driven by advanced biopharmaceutical research infrastructure, stringent regulatory frameworks ensuring product quality, and concentrated presence of leading pharmaceutical companies, including Thermo Fisher Scientific and Merck KGaA.

- Fast-growing Region: Asia Pacific represents the fastest-growing regional market during 2025 - 2032, propelled by rapid biopharmaceutical manufacturing expansion, particularly in China, India, Japan, and Southeast Asia, with the region's innovative pipeline share expanding to 43% globally.

- Leading Product: Standard / Regular FBS maintains market dominance with approximately 32% share in 2025, reflecting its universal adoption as the preferred supplement for eukaryotic cell culture across diverse research and industrial applications.

- Fast-growing Product: Stem Cell-Qualified FBS emerges as the fastest-growing product segment during 2025 - 2032, driven by explosive expansion in stem cell research and regenerative medicine applications.

| Key Insights | Details |

|---|---|

| Fetal Bovine Serum Market Size (2026E) | US$ 2.6 billion |

| Market Value Forecast (2033F) | US$ 5.2 billion |

| Projected Growth CAGR (2026 - 2033) | 10.3% |

| Historical Market Growth (2020 - 2025) | 9.8% |

Market Dynamics

Drivers - Surge in Cell and Gene Therapy Development Accelerating FBS Demand

The exponential growth of cell and gene therapy pipelines represents a transformative driver for the fetal bovine serum market, as these advanced therapeutic modalities require extensive cell culture processes during development and manufacturing. Asia's innovative pipeline share has expanded from 28% to 43% in just five years, with the region contributing more than 85% of global growth in innovative drug pipelines during 2024. China now represents 29% of the global innovative pipeline, while India's biopharma innovation pipeline expanded from approximately 270 assets in 2015 to roughly 450 in 2024, marking a 1.5 times increase. The emergence of CAR-T cell therapies, chimeric antigen receptor natural killer (NK) cells, and receptor-modified T-cells necessitates specialized cell culture media supplemented with FBS to support T cell expansion and maintain early memory T cell phenotype during manufacturing. The U.S. FDA's Center for Biologics Evaluation and Research (CBER) has introduced flexible regulatory frameworks for cell and gene therapies, expediting product development timelines and consequently increasing the throughput of FBS-dependent manufacturing processes.

Expanding Biopharmaceutical Manufacturing Infrastructure and Investment

Substantial capital investments in biopharmaceutical manufacturing infrastructure globally significantly propel fetal bovine serum market growth, as expanded production facilities require corresponding increases in cell culture reagent consumption. Thermo Fisher Scientific Inc. announced a US$ 76 million investment for expanding their cell culture media manufacturing site in Grand Island, New York, constituting part of a broader US$ 650 million multi-year expansion to ensure reliable bioprocessing production capacity. Merck KGaA invested over €130 million in strengthening manufacturing capabilities in Molsheim, France, creating more than 800 jobs by 2028, alongside a €70 million expansion of antibody-drug conjugate (ADC) manufacturing capabilities in St. Louis, Missouri, tripling existing capacity. The global contract research organization (CRO) services market reached US$ 77.0 billion in 2024 and is expected to reach US$ 162.1 billion by 2033, growing at a CAGR of 8.6%, reflecting intensified outsourcing of clinical trials requiring extensive cell culture operations.

Restraints - Ethical Concerns and Growing Preference for Serum-Free Alternatives

The fetal bovine serum market faces significant headwinds from mounting ethical concerns regarding animal-derived products and accelerating development of serum-free media formulations. Ethical considerations surrounding FBS sourcing, particularly related to animal welfare and collection process involving bovine fetuses, have prompted regulatory scrutiny and corporate sustainability initiatives seeking alternatives. The global serum-free media market reached US$ 1.9 billion in 2025 and is projected to grow at a CAGR of 7.8% through 2032, demonstrating strong commercial momentum toward animal-origin-free solutions. Thermo Fisher Scientific launched the Gibco CTS OpTmizer One Serum-Free Medium, an animal origin-free (AOF) formulation specifically designed for clinical and commercial cell therapy manufacturing.

Supply Chain Volatility and Price Fluctuations

The fetal bovine serum market experiences persistent challenges from supply chain volatility and significant price fluctuations stemming from the biological nature of the product and dependence on livestock populations. FBS is a by-product of the meat industry, with collection dependent on cattle slaughter operations, making supply inherently susceptible to agricultural dynamics, disease outbreaks affecting cattle populations, and seasonal variations in livestock processing. The cost of FBS can fluctuate considerably due to supply-demand imbalances, production costs, transportation logistics, and stringent quality testing requirements necessary to ensure product safety and efficacy.

Opportunity - Stem Cell Research Expansion and Specialized FBS Grade Development

The burgeoning stem cell research sector presents substantial growth opportunities for specialized fetal bovine serum formulations, particularly stem cell-qualified FBS designed to support pluripotent stem cell culture applications. The International Society for Stem Cell Research (ISSCR) updated its guidelines in August 2025, refining recommendations for stem cell-based embryo models and providing clearer frameworks for research activities. Human pluripotent stem cells including human embryonic stem cells (hESCs) and human induced pluripotent stem cells (hiPSCs) have enabled production of therapeutically important cell types including insulin-producing beta cells, retinal pigment epithelial cells, cardiomyocytes, and neurons in practically unlimited quantities, all requiring optimized culture conditions supported by specialized FBS grades.

Category-wise Analysis

Product Type Insights

Standard / Regular FBS dominates the fetal bovine serum market with approximately 32% market share in 2025, reflecting its widespread adoption as the universal supplement for eukaryotic cell culture across diverse research and industrial applications. This segment's leadership position stems from its versatility in supporting both primary cells and established cell lines across multiple mammalian cell types, combined with relatively lower cost compared to specialized FBS grades. Standard FBS contains exceptionally high concentrations of growth and attachment factors, lower levels of antibodies, reduced complement protein activity, and fewer growth-inhibiting components compared to adult bovine serum, making it the preferred choice for routine cell culture operations in academic and research institutes, pharmaceutical companies, and contract research organizations.

Application Insights

Biopharmaceutical manufacturing applications capture the leading market share in 2025, accounting for approximately 35% of total fetal bovine serum consumption, reflecting the industry's intensive reliance on cell culture processes for producing biologics including monoclonal antibodies, recombinant proteins, and viral vectors. The biopharmaceutical sector's sustained expansion, with global biologics manufacturing capacity increasing substantially to meet demand for novel therapeutic modalities, directly translates to elevated FBS consumption across production operations. Major pharmaceutical manufacturers including Merck KGaA, Thermo Fisher Scientific Inc., and Lonza Group Ltd. have announced significant capacity expansion investments exceeding several hundred million dollars, necessitating proportional increases in cell culture media components including FBS.

End-user Insights

Pharmaceutical & Biotech Companies constitute the dominant end-user segment with approximately 38% market share in 2025, driven by their extensive cell culture operations spanning research, development, and commercial manufacturing of biological therapeutics. This segment's leadership reflects the pharmaceutical industry's transformation toward biologics and biosimilars, with India alone having more than 138 biosimilars approved across global markets as pharmaceutical firms expand beyond traditional small molecule drugs into complex biological products requiring intensive cell culture processes.

Regional Insights

North America Fetal Bovine Serum Market Trends and Insights

The North America Fetal Bovine Serum (FBS) market leads globally, supported by a highly developed biotechnology and biopharmaceutical ecosystem. The region benefits from strong demand across cell culture research, biologics manufacturing, and advanced therapies, including cell and gene therapies. A high concentration of pharmaceutical companies, academic research institutes, and contract research organizations ensures consistent FBS consumption. Continuous innovation in drug discovery, vaccine development, and regenerative medicine further reinforces market leadership. In addition, strict quality standards and regulatory compliance drive demand for premium and traceable FBS products. North America also shows early adoption of specialty FBS types, such as stem cell-qualified and exosome-depleted variants, reflecting the region’s focus on high-end research applications. Strong research funding, robust infrastructure, and established supply chains collectively position North America as the most mature and dominant regional market for Fetal Bovine Serum.

Asia Pacific Fetal Bovine Serum Market Trends and Insights

The Asia Pacific Fetal Bovine Serum (FBS) market is emerging rapidly due to the region’s expanding life sciences ecosystem and increasing investments in biomedical research. Countries such as China, India, South Korea, and Japan are witnessing strong growth in cell culture-based research, vaccine development, and biopharmaceutical manufacturing, which directly drives FBS demand. Rising government funding for biotechnology, the establishment of new research institutes, and growth in contract research and manufacturing activities are strengthening regional consumption. In addition, Asia Pacific benefits from a large pool of academic and clinical research organizations adopting advanced cell-based assays and regenerative medicine approaches. Cost advantages, improving regulatory frameworks, and increasing local production of research reagents are further enhancing market accessibility. While standard FBS currently dominates usage due to affordability, demand for specialty FBS types is increasing as research complexity grows. Overall, the Asia Pacific is transitioning from a volume-driven market to a quality-focused one, positioning it as a key growth engine for the global FBS industry over the forecast period.

Competitive Landscape

The global fetal bovine serum market features a moderately consolidated competitive landscape characterized by strong emphasis on quality, traceability, and regulatory compliance. Market participants compete primarily on serum consistency, origin certification, and rigorous testing standards to ensure suitability for sensitive cell culture applications. Product differentiation is increasingly driven by the availability of specialty FBS types tailored for advanced research, including stem cell and gene therapy applications. Companies are also focusing on strengthening global distribution networks and long-term sourcing agreements to manage supply volatility. Technological improvements in filtration, viral inactivation, and quality control processes enhance competitive positioning.

Key Developments:

- In February 2026, US cultivated meat startup Omeat rebranded to Evergreen Connect and secured $6 million in new funding to advance its blended lab-grown beef products for the US and Singapore markets. The company had raised a total of $46 million with the new round and planned to collaborate with meat distributors to commercialise blended beef mince. It was reported to be well advanced in regulatory processes in both regions and intended to use part of the funding for regulatory approval efforts, positioning its approach as a way to strengthen supply chain stability and bring cultivated meat closer to consumers.

Companies Covered in Fetal Bovine Serum Market

- Thermo Fisher Scientific Inc

- Merck KGaA (Sigma-Aldrich)

- Cytiva (Danaher)

- Lonza Group Ltd

- HiMedia Laboratories Pvt. Ltd

- Biowest S.A.S

- Atlanta Biologicals, Inc

- PAN-Biotech GmbH

- Rocky Mountain Biologicals (Inotiv)

- Moregate BioTech

- Gemini Bio-Products

- TCS Biosciences Ltd

- Corning Incorporated

- Biological Industries

- Capricorn Scientific

- Bovogen Biologicals Pty Ltd

- RMBIO

- Tissue Culture Biologicals

- Sera Laboratories International Ltd

- Serana Europe GmbH

Frequently Asked Questions

The global fetal bovine serum market size is expected to be valued at US$ 2.6 billion in 2026 and projected to reach US$ 5.2 billion by 2033, growing at a CAGR of 10.3% between 2026 and 2033.

The market is primarily driven by the surge in cell and gene therapy development, with Asia's innovative pipeline share expanding to 43% globally and substantial capital investments in biopharmaceutical manufacturing infrastructure.

North America maintains market leadership with approximately 37% market share in 2025, underpinned by advanced biopharmaceutical research infrastructure and robust regulatory frameworks under U.S. FDA CBER oversight.

The expanding in vitro fertilization (IVF) market valued at approximately US$ 28.55 billion in 2024 and expected to reach US$ 66.30 billion by 2034 represents a significant opportunity.

Leading market players include Thermo Fisher Scientific Inc., Merck KGaA (Sigma-Aldrich), Cytiva (Danaher), Lonza Group Ltd., HiMedia Laboratories Pvt. Ltd., Biowest S.A.S., competing through product quality differentiation and regulatory compliance.