- Renewable Energy

- Fault Current Limiter Market

Fault Current Limiter Market Size, Share, and Growth Forecast, 2026 - 2033

Fault Current Limiter Market by Product Type (Superconducting FCL, Non-Superconducting FCL, Others), Voltage Range (High Voltage (>40 kV), Medium Voltage (1-40 kV), Others), End-user, and Regional Analysis for 2026 - 2033

Fault Current Limiter Market Size and Trends Analysis

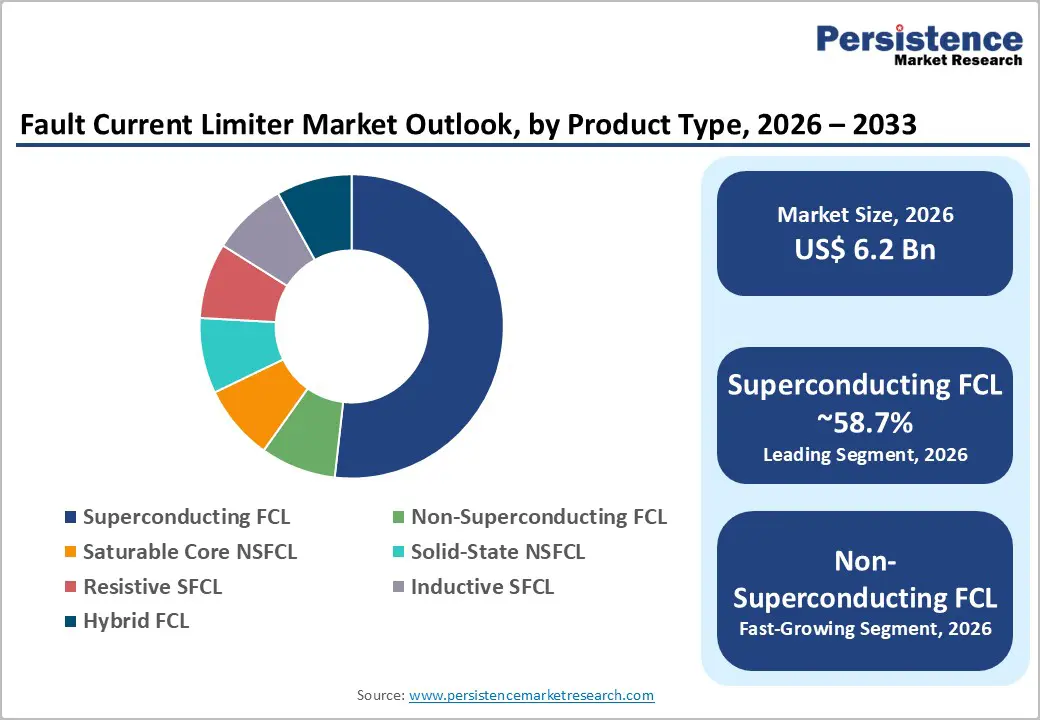

The global fault current limiter market size is likely to be valued at US$6.2 billion in 2026 and is expected to reach US$9.7 billion by 2033, growing at a CAGR of 6.6% between 2026 and 2033.

Growth reflects increasing grid modernization investments, rising short-circuit current levels driven by distributed energy resources, and the adoption of advanced superconducting and solid-state fault-current limiting technologies. Utilities and industrial operators are increasingly deploying fault current limiters to prevent costly substation upgrades and protect critical electrical equipment. Continuous improvements in superconducting materials, cryogenic systems, and power electronics are reducing lifecycle costs, making the technology more commercially viable. The market’s historical CAGR of 6.9% demonstrates steady, technology-driven growth supported by long-term infrastructure investment cycles.

Key Industry Highlights:

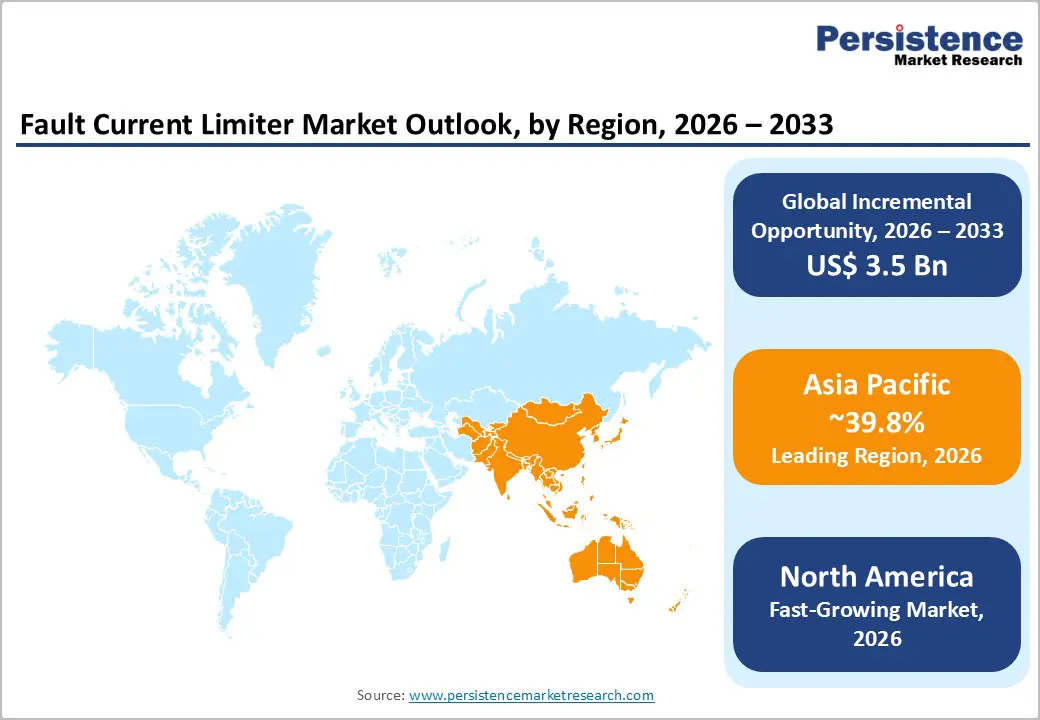

- Leading Region: Asia Pacific is projected to lead the market with approximately 39.8% market share, supported by large-scale grid expansion projects, strong power infrastructure investments in China, India, and Japan, and rapid renewable energy integration across regional transmission networks.

- Fastest-growing Region: North America is the fastest-growing regional market, driven by accelerated grid modernization programs, rising investments in smart grid technologies, and increasing deployment of advanced grid protection solutions across the U.S. and Canada.

- Investment Plans: Governments and utilities worldwide are increasing investments in grid resilience, renewable integration infrastructure, and transmission modernization, which is expected to significantly boost the deployment of advanced protection technologies such as fault current limiters over the forecast period.

- Dominant Product Type: Superconducting fault current limiters (SFCLs) are anticipated to be the dominant product segment, accounting for approximately 58.7% of market share, primarily due to their rapid response, minimal energy loss, and strong suitability for high-capacity transmission networks.

- Leading Voltage Range: High-voltage fault current limiters (>40 kV) are estimated to hold the largest share of 55.6%, as transmission networks require advanced protection systems to manage rising short-circuit currents caused by grid interconnections and large-scale renewable power integration.

| Key Insights | Details |

|---|---|

| Fault Current Limiter Market Size (2026E) | US$6.2 Bn |

| Market Value Forecast (2033F) | US$9.7 Bn |

| Projected Growth (CAGR 2026 to 2033) | 6.6% |

| Historical Market Growth (CAGR 2020 to 2025) | 6.9% |

Market Factors - Growth, Barriers, and Opportunity Analysis

Growth Analysis - Rapid Growth of Distributed Energy Resources and Renewable Integration

The accelerating integration of distributed energy resources, such as solar photovoltaic systems, wind power installations, and battery energy storage, is significantly increasing fault current levels in transmission and distribution networks. As grid interconnections expand, fault currents can exceed the interrupting capacity of existing circuit breakers and transformers. Utilities are therefore deploying fault current limiters (FCLs) as a cost-effective solution to maintain system protection without replacing major infrastructure components. Electrical power systems with high renewable penetration require precise fault current management to ensure protection coordination and system reliability. The ability of FCLs to limit instantaneous fault currents without interrupting normal operation makes them particularly valuable in renewable-rich grids. Consequently, utility investment in fault current limiting technologies continues to increase as part of grid modernization strategies.

Advancements in Superconducting and Solid-State Technologies

Technological improvements in high-temperature superconducting (HTS) materials and solid-state power electronics have significantly improved the performance and commercial viability of modern FCL systems. Early superconducting designs required complex cooling systems and carried high installation costs. Recent engineering advances have reduced cryogenic system complexity while improving operational reliability and fault response speed. Solid-state FCLs now use advanced semiconductor switching technologies capable of extremely rapid response to fault conditions while minimizing insertion losses. These innovations have improved system efficiency and reduced maintenance requirements. As a result, utilities and industrial operators are transitioning from pilot projects toward commercial deployment. Continued research and development in power electronics and superconducting materials is expected to further enhance system performance and reduce total ownership costs.

Regulatory Focus on Grid Resilience and Safety

Government regulators and grid operators are increasingly prioritizing power system resilience and infrastructure reliability. Aging electrical networks, increasing power demand, and the expansion of distributed generation have intensified the need for improved fault management. Regulatory frameworks in several major power markets encourage the adoption of technologies that enhance system stability and reduce the risk of blackouts. Fault current limiters allow utilities to increase network capacity without undertaking expensive infrastructure replacements such as transformer upgrades or circuit breaker replacements. Public funding programs and research initiatives have also supported demonstration projects for advanced FCL technologies. These initiatives are accelerating technology validation and encouraging utilities to incorporate FCL deployment into long-term grid planning.

Barrier Analysis - High Initial Capital Investment

One of the most significant barriers to widespread adoption of fault current limiter systems is the high upfront installation cost, particularly for superconducting technologies. Superconducting FCLs require specialized materials and cooling systems, which increase equipment and installation expenses compared with traditional protection equipment. Although lifecycle cost savings can offset these investments through deferred infrastructure upgrades and reduced equipment damage, utilities often require extensive financial justification before committing to new technologies. Budget constraints and conservative capital expenditure policies can therefore slow deployment in certain markets.

Technical Integration and Protection Coordination Challenges

Integrating FCL systems into existing power networks requires detailed engineering analysis to ensure proper coordination with protective relays, circuit breakers, and other protection devices. As fault current limiters alter the electrical characteristics of fault conditions, utilities must conduct extensive modeling, testing, and commissioning procedures before installation. In networks with aging or complex protection architectures, integration timelines may become lengthy and expensive. The absence of universally standardized performance criteria for some advanced FCL technologies can further increase technical uncertainty for utilities evaluating new deployments.

Opportunity Analysis - Retrofit Opportunities in Aging Power Infrastructure

A significant opportunity for the fault current limiter market lies in modernizing aging electrical infrastructure. Many transmission and distribution systems were designed decades ago and now operate close to their maximum fault current capacity. Replacing transformers, breakers, and substations can require substantial capital investment and long construction timelines. Installing FCLs provides a cost-effective alternative by limiting short-circuit currents without requiring major equipment replacements. Utilities can strategically deploy FCLs at critical grid nodes to defer large capital upgrades while maintaining system safety.

Growing Demand from Industrial Power Systems

Industrial facilities such as steel mills, petrochemical plants, chemical processing units, and heavy manufacturing complexes operate large motors and high-power electrical systems that generate substantial fault currents. Uncontrolled fault currents can cause severe equipment damage and costly production downtime. As industrial operations increasingly depend on uninterrupted power supply and automated production systems, the demand for advanced protection technologies continues to grow. Fault current limiters provide a reliable solution for protecting critical equipment and ensuring operational continuity, making them increasingly attractive for industrial power systems.

Expansion Opportunities in Emerging Electricity Markets

Rapid industrialization and urbanization in emerging economies are driving large-scale expansion of power generation and transmission infrastructure. Countries across the Asia Pacific are investing heavily in renewable energy, high-capacity transmission networks, and urban electrification programs. These developments increase fault current levels within rapidly expanding electrical grids, creating strong demand for advanced protection technologies. Local manufacturing capabilities and regional supply chains also support cost reductions and faster technology deployment, making emerging markets an important growth opportunity for global FCL suppliers.

Category-wise Analysis

Product Type Insights

Superconducting fault current limiters (SFCLs) are anticipated to represent the leading product segment, accounting for approximately 58.7% of the market share in 2026. These systems utilize high-temperature superconducting materials that exhibit near-zero electrical resistance under normal operating conditions. When a short-circuit fault occurs, the superconducting material instantly transitions into a resistive state, limiting the fault current within milliseconds. This capability enables SFCLs to protect transmission networks while maintaining normal grid efficiency.

Transmission utilities favor superconducting solutions as they minimize energy losses, require limited operational intervention, and maintain grid stability during fault events. According to grid modernization initiatives reported by the International Energy Agency (IEA) and U.S. Department of Energy (DOE), increasing grid interconnections and renewable energy integration are pushing fault current levels beyond the rating of conventional switchgear. As a result, utilities are deploying SFCLs in high-capacity transmission networks, metropolitan substations, and renewable integration hubs to avoid expensive infrastructure upgrades while ensuring protection coordination across complex grid architectures.

The non-superconducting fault current limiter (NSFCL) segment is projected to experience the fastest growth during the forecast period, driven by technological diversification and cost advantages. This category includes saturable core FCLs, solid-state FCLs, resistive designs, inductive designs, and hybrid configurations. Among these, solid-state FCLs are attracting significant industry attention because they rely on power semiconductor switching devices rather than superconducting materials, simplifying system architecture and reducing cryogenic cooling requirements. This design flexibility makes them suitable for medium-voltage distribution systems, industrial facilities, and decentralized power networks.

Saturable core designs are also widely used in industrial installations due to their mechanical robustness and passive operation. Hybrid FCL configurations, which combine passive magnetic components with semiconductor switching elements, are emerging as practical solutions for microgrids and distributed generation environments. As reported by industry analyses from Deloitte and MarketsandMarkets, utilities are increasingly prioritizing cost-efficient, modular, and easily deployable protection solutions, particularly for distribution-level networks. Consequently, demand for non-superconducting FCL technologies is expected to accelerate as grid operators expand distributed power systems, renewable integration infrastructure, and smart grid networks worldwide.

Voltage Range Insights

The high-voltage segment (>40 kV) is estimated to account for the largest share of the market, with approximately 55.6% in 2026. High-voltage transmission networks experience the highest fault current magnitudes due to large-scale power generation units, long-distance transmission lines, and interconnected regional grids. When short-circuit currents exceed equipment ratings, conventional circuit breakers and transformers are at increased risk of damage or premature failure. Installing FCL systems at high-voltage substations and transmission nodes helps utilities manage rising fault levels without replacing existing switchgear.

According to the International Energy Agency (IEA) and the World Bank's energy infrastructure reports, many countries are expanding cross-border grid interconnections and integrating large renewable energy sources, such as offshore wind and utility-scale solar plants. These developments significantly increase network fault levels. Utilities therefore deploy high-voltage FCL systems as strategic grid protection investments, allowing operators to defer expensive substation upgrades and extend the service life of installed assets. This economic advantage, combined with reliability improvements, continues to drive strong demand for high-voltage FCL installations across major transmission networks.

The medium-voltage segment (1-40 kV) is expected to register the fastest growth throughout the forecast period, supported by the rapid expansion of distributed energy systems and electrified industrial infrastructure. Medium-voltage networks form the backbone of power distribution systems supplying industrial facilities, commercial campuses, and urban residential districts. In recent years, the proliferation of distributed energy resources (DERs), including rooftop solar, battery energy storage, and localized generation, has increased short-circuit current levels within distribution networks.

Maintaining protection coordination in such environments often requires replacing expensive switchgear equipment, which can significantly increase infrastructure costs. Medium-voltage fault current limiters provide a cost-effective alternative by reducing fault current levels without modifying the existing protection architecture. Their compact footprint and relatively straightforward installation make them particularly suitable for urban substations, microgrid installations, renewable integration points, and large industrial complexes. Energy transition policies promoted by organizations such as the International Renewable Energy Agency (IRENA) are accelerating the deployment of distributed generation systems worldwide. As a result, utilities and industrial operators are increasingly adopting medium-voltage FCL solutions to ensure grid reliability, safety compliance, and efficient integration of decentralized power resources, positioning this segment for sustained growth in the coming decade.

Regional Insights

North America Fault Current Limiter Market Trends - Grid Modernization and Renewable Integration Driving Rapid Adoption

North America represents one of the most technologically advanced markets for fault current limiter systems and is projected to be the fastest-growing regional market during the forecast period. The U.S. dominates regional demand due to extensive investment in grid modernization, renewable energy integration, and infrastructure resilience programs. Electric utilities across the country are upgrading transmission networks to accommodate increasing electricity demand and expanding renewable generation capacity.

As renewable energy penetration increases, short-circuit current levels in transmission systems also rise, creating a strong need for advanced protection technologies. Government initiatives supporting infrastructure modernization and grid resilience have encouraged utilities to evaluate emerging technologies such as superconducting and solid-state FCL systems. Demonstration projects conducted by research institutions and utility partnerships have helped validate the performance and reliability of these systems in real-world operating environments. The availability of advanced engineering expertise and strong collaboration between utilities, equipment manufacturers, and research institutions further strengthens the region’s leadership in technology development.

Industrial demand also contributes to market growth in North America. Energy-intensive industries such as petrochemicals, mining, and heavy manufacturing require reliable electrical protection to maintain operational continuity. The adoption of automated production systems and digitally controlled industrial facilities has increased the importance of a stable power supply and fault management. Investment trends indicate increasing collaboration between technology developers and engineering procurement contractors to accelerate commercial deployment. Service-based business models that combine equipment installation with maintenance and monitoring services are becoming more common. As utilities continue to modernize aging infrastructure and integrate distributed energy resources, North America is expected to remain a key growth market for advanced fault current limiting technologies.

Europe Fault Current Limiter Market Trends - Energy Transition and Distributed Generation Supporting Steady Market Expansion

Europe represents a mature but steadily expanding market for fault current limiter systems. The region’s electricity sector is undergoing a significant transformation as countries transition to renewable energy sources and reduce reliance on conventional fossil-fuel generation. This energy transition has increased the complexity of grid operations and raised fault-current levels in interconnected power networks. Germany, the U.K., France, and Spain are among the leading European markets adopting advanced electrical protection technologies. Germany’s strong engineering sector and focus on integrating renewable energy have spurred research and pilot projects on superconducting fault current limiter systems. France and the U.K. are investing heavily in grid modernization to support offshore wind development and electrification initiatives.

European utilities face the challenge of integrating increasing volumes of distributed generation into densely interconnected networks. In many cases, installing FCL systems offers a practical solution for maintaining protection coordination without replacing large numbers of circuit breakers and transformers. Regional regulatory bodies emphasize grid stability and reliability, creating a favorable policy environment for the deployment of advanced protection technologies.

Research institutions and engineering firms across Europe continue to collaborate on improving superconducting materials, cryogenic systems, and advanced power electronics used in FCL designs. Cross-border research initiatives and industry partnerships have accelerated technology validation and commercialization. As electrification initiatives expand across transportation, industry, and residential sectors, the need for reliable grid infrastructure is expected to sustain demand for fault-current-limiting technologies across the European power sector.

Asia Pacific Fault Current Limiter Market Trends - Large-Scale Grid Expansion and Rising Electricity Demand Fueling Market Leadership

Asia Pacific is anticipated to represent the largest regional market, accounting for approximately 39.8% of the market share in 2026. Rapid economic development, expanding electricity demand, and large-scale infrastructure investments have significantly increased the complexity and capacity of regional power systems. Countries including China, Japan, India, and several Southeast Asian economies are investing heavily in high-capacity transmission networks and in integrating renewable energy. China represents the largest national market within the region due to its extensive power infrastructure expansion and strong domestic manufacturing capabilities. The country’s power sector continues to build large transmission networks and integrate renewable generation projects on a massive scale. These developments increase short-circuit current levels across interconnected grids, creating strong demand for advanced protection technologies such as fault current limiters.

Japan is recognized for its advanced electrical engineering capabilities and early adoption of superconducting technologies. Japanese utilities have implemented several pilot projects using superconducting fault current limiters to improve grid reliability in densely populated urban areas. These projects have demonstrated the technical feasibility and operational benefits of FCL technology. India and Southeast Asian countries are also experiencing rapid growth in electricity demand due to industrial expansion and urbanization. Governments across the region are investing in grid modernization, rural electrification, and renewable energy development.

These initiatives require robust electrical protection systems capable of managing increasing fault current levels. The presence of large electrical equipment manufacturers and expanding domestic supply chains in Asia Pacific supports the development and commercialization of advanced FCL technologies. Local production capabilities reduce manufacturing costs and enable faster deployment across regional power networks. As electricity demand continues to rise and grid infrastructure expands, Asia Pacific is expected to remain the dominant regional market for fault current limiter systems.

Competitive Landscape

The global fault current limiter market exhibits a moderately consolidated competitive structure dominated by large multinational electrical equipment manufacturers and specialized technology developers. Leading companies provide high-voltage grid equipment and advanced protection solutions, allowing them to secure major utility contracts for transmission and distribution infrastructure projects. These established firms benefit from strong engineering expertise, extensive service networks, and long-standing relationships with utility operators.

The market also includes smaller technology specialists focused on superconducting materials, cryogenic systems, and solid-state switching technologies. These niche companies often collaborate with larger equipment manufacturers to commercialize new solutions. While high-voltage transmission applications remain relatively concentrated among major OEMs, medium-voltage and industrial segments show greater competitive diversity with multiple technology providers offering modular and customized solutions. Leading companies in the fault current limiter market focus on technological innovation, strategic partnerships with utilities, and geographic market expansion. Many suppliers are investing heavily in research and development to improve superconducting materials and solid-state switching technologies. Service-based models that combine equipment installation with long-term maintenance support are also emerging as important competitive differentiators.

Key Industry Developments

- In January 2025, SuperGrid Institute announced the successful validation of a resistive superconducting fault current limiter (RSFCL) integrated with a mechanical DC circuit breaker during high-voltage tests reaching 50 kV. The technology demonstrated the ability to limit fault currents by approximately 87%, creating a new protection approach for high-voltage direct current (HVDC) networks and offshore renewable power systems.

Companies Covered in Fault Current Limiter Market

- ABB Ltd.

- Siemens AG

- Schneider Electric SE

- General Electric (GE) Grid Solutions

- Mitsubishi Electric Corporation

- Toshiba Corporation

- American Superconductor Corporation (AMSC)

- Nexans S.A.

- Eaton Corporation plc

- Rongxin Power Electronic Co., Ltd. (RXPE)

- Zenergy Power plc

- Superconductor Technologies Inc.

- Sumitomo Electric Industries, Ltd.

- Furukawa Electric Co., Ltd.

- Applied Materials, Inc.

- GridON Ltd.

- Shanghai Electric Group Company Limited

- ASG Superconductors S.p.A.

Frequently Asked Questions

The global fault current limiter market is estimated to be valued at approximately US$6.2 billion in 2026.

By 2033, the global market is projected to reach around US$9.7 billion.

Several industry trends are shaping the market, including the expansion of smart grid infrastructure, rising renewable energy integration, increasing deployment of distributed energy resources, and the growing adoption of superconducting and solid-state protection technologies.

Superconducting fault current limiters (SFCLs) currently represent the leading product segment, accounting for nearly 58.7% of the market share, due to their rapid response capability, minimal energy losses, and strong suitability for high-voltage transmission networks.

The fault current limiter market is expected to grow at a CAGR of approximately 6.6% between 2026 and 2033.

Major companies include ABB Ltd., Siemens AG, Schneider Electric, General Electric, and Toshiba Corporation.