- Travel and Tourism

- Europe Golden Generation Travel Market

Europe Golden Generation Travel Market Size, Share, and Growth Forecast 2026 - 2033

Europe Golden Generation Travel Market by Travel Type (Leisure Travel, Cultural Travel, Medical Travel, Adventure Travel), Tourist Type (Domestic, International), Accommodation Type (Luxury Hotels, Budget / Mid-Scale Hotels, Vacation Rentals), Transportation Mode (Air Travel, Cruise Travel, Rail Travel) and Regional Analysis, 2026 - 2033

Europe Golden Generation Travel Market Size and Trend Analysis

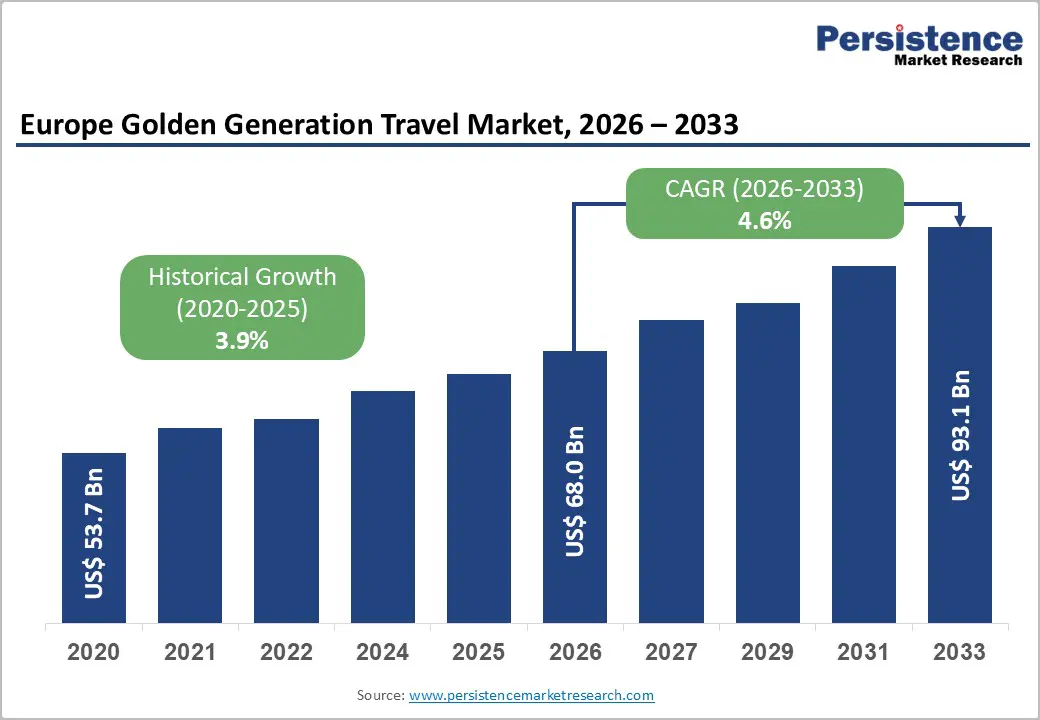

The Europe golden generation travel market size is likely to be valued at US$68.0 billion in 2026 and is projected to reach US$93.1 billion by 2033, growing at a CAGR of 4.6% between 2026 and 2033. The market recorded a historical value of US$53.7 billion in 2020, reflecting a historical CAGR of 3.9%, underscoring the structural resilience of senior travel demand across Europe even through periods of macroeconomic disruption.

Europe's rapidly aging population demographic, strong post-pandemic restoration of travel confidence among senior travelers, the maturation of experiential and wellness-oriented travel products specifically engineered for the 55-plus age cohort, and the structural expansion of Europe's aviation and rail connectivity infrastructure are making multi-destination itineraries more accessible and affordable.

Key Industry Highlights:

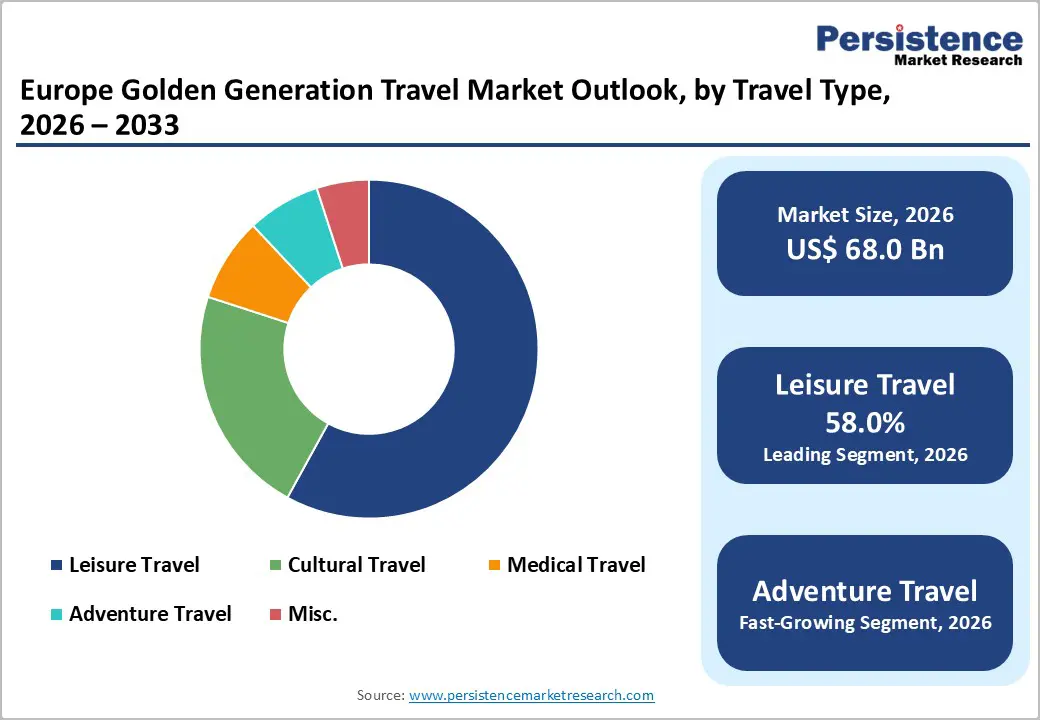

- Leading Travel Type Segment: Leisure Travel dominates with 58% share (2025), driven by strong demand for cultural tourism, wellness retreats, beach holidays, and multi-country European touring among retired and semi-retired travelers.

- Fastest-Growing Travel Type Segment: Adventure Travel is the fastest-growing segment, driven by increasing participation of the active 55-70 age cohort seeking immersive, physically engaging, and experience-led travel formats.

- Leading Transportation Mode Segment: Air Travel leads with 44% share (2025), supported by strong intra-European and international connectivity, record passenger volumes (2.6 billion in 2025), and expanding low-cost airline networks enabling senior mobility.

- Fastest-Growing Transportation Mode Segment: Cruise Travel is the fastest-growing segment, supported by post-pandemic recovery above pre-COVID levels (107%), strong European river cruise expansion, and high repeat-travel rates among senior travelers.

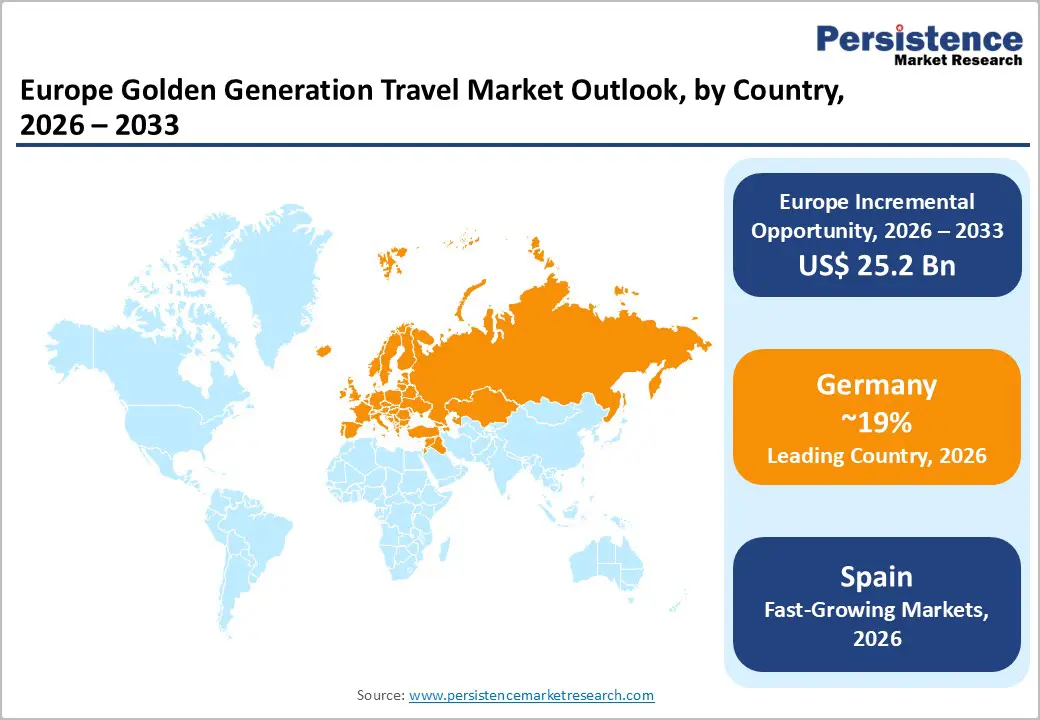

- Leading Country: Germany dominates the European golden generation travel market with 19% share in 2025, driven by its large aging population base, high senior disposable income, strong outbound travel culture, and extensive air and rail connectivity enabling frequent domestic and international senior travel.

- Fastest-Growing Markets: Spain and Türkiye are the fastest-growing markets, supported by strong Mediterranean leisure tourism appeal, expanding cruise and cultural travel infrastructure, competitive cost advantages, and rising demand from senior travelers for wellness, heritage, and long-stay vacation experiences.

DRO Analysis

Europe's Aging Population Creating Structural Demand in the Golden Generation Travel Market

The fundamental demographic driver of the golden generation travel market is Europe's accelerating ageing transition, the largest and most sustained structural demand catalyst in the region's travel and tourism economy. According to Eurostat, the proportion of Europeans aged 65 and above is projected to reach 29.5% of the total EU population by 2050, up from approximately 21.1% in 2023, adding nearly 40 million individuals to the primary golden generation travel cohort over the next three decades.

In real economic terms, this cohort controls a disproportionate share of household wealth: European seniors aged 60 and above account for an estimated 50% of total consumer spending in the EU, supported by pension entitlements, accumulated real estate equity, and lower household expenditure obligations compared to working-age groups. This demographic and wealth concentration positions senior travelers as structurally higher-spending, longer-staying, and off-peak-willing than other traveler segments, enabling the golden generation travel market to achieve both volume growth and yield improvement characteristics that are essentially independent of short-term economic cycles.

Strong Recovery in European Air and Rail Connectivity Enabling Senior Travel Access

The recovery and structural expansion of Europe's multi-modal transport infrastructure is directly enabling the golden generation travel market by reducing the logistical and physical barriers that historically constrained senior long-haul and multi-destination travel.

European air travel reached a record 2.6 billion passengers in 2025, reflecting a 4.4% year-on-year advance and adding approximately 100 million travelers. ACI Europe projects continued growth of approximately 3.3% in 2026, supported by stronger financial performance and a structural shift toward intra-European leisure travel. Between January and September 2025, approximately 840 million passengers were transported across the EU, a 3.7% increase compared to the same period in 2024, with extra-EU travel accounting for 50.1% of traffic, up 4.8% from the same period in 2024, reflecting senior travelers' increasing preference for international and cruise-linked itineraries.

Rail transport simultaneously reached a record 443 billion passenger-kilometers in 2024, a 5.8% increase from 2023, the highest level since Eurostat data collection commenced in 2004, with countries such as Hungary recording 60% growth, further enriching the multi-modal connectivity options available to senior travelers.

Post-Pandemic Restoration of Senior Travel Confidence and Premiumization of Experiential Products

The sustained recovery of European tourism following the COVID-19 pandemic has disproportionately benefited the Golden Generation Travel Market, as senior travelers who were among the most severely constrained during the pandemic period have demonstrated an accelerated propensity to travel driven by accumulated deferred demand, heightened awareness of temporal opportunity, and a structural shift toward experience-prioritizing consumption.

The global cruise industry surpassed pre-pandemic levels in 2023 at 31.7 million passengers, representing 107% of 2019 volumes, with Europe recording a 6.5% increase relative to pre-pandemic baselines, a recovery rate closely correlated with senior travel demand, given the cruise segment's disproportionately senior passenger demographic. A notable 12% of cruise travelers take two cruises annually, and 10% take three to five trips per year, demonstrating the high loyalty and frequency characteristics of the golden generation traveler profile that underpin repeat revenue for operators.

This structural shift toward premium, experience-driven, multi-modal travel spanning cultural immersion, active adventures, and wellness retreats has enabled leading tour operators to successfully premiumize their product portfolios.

Restraint - Health Risks, Travel Insurance Complexity, and Operational Disruptions

Senior travelers face disproportionate health-related travel risks and insurance access barriers compared to younger demographics, creating a structural friction layer that moderates demand conversion and trip completion rates in the golden generation travel market. Pre-existing conditions, mobility limitations, and age-related premium surcharges in travel insurance products can substantially elevate the all-in cost of international travel for the 70-plus cohort, while the EU's Entry-Exit System is expected to introduce passport scanning requirements at external borders, which may create processing delays and operational complexity at major European hub airports that particularly impact older travelers with limited digital literacy or mobility constraints. These structural friction factors represent ongoing challenges in product design and service delivery for operators.

Opportunities - Underpenetrated Eastern and Southern European Destinations as New High-Growth Corridors

Eastern and Southern Europe represent a compelling geographic expansion opportunity for operators in the golden generation travel market, with several markets recording double-digit passenger traffic growth in 2025, including Slovakia, Poland, Cyprus, and Hungary, indicating a shift in European travel patterns toward previously secondary destinations. These markets offer a combination of cultural richness, lower cost bases, strong heritage and culinary tourism appeal, and improving accessibility infrastructure that aligns directly with senior travelers' preference for authentic, unhurried, and value-conscious experiences.

Hungary's 60% rail passenger growth in 2024, Poland's strong aviation expansion, and the broader connectivity improvements across Eastern Europe, supported by EU cohesion fund infrastructure investments are progressively lowering the logistical barriers to senior-friendly multi-destination rail and road itineraries across the region. For tour operators, developing dedicated golden generation products centered on Eastern and Southern European cultural routes combining UNESCO heritage sites, thermal spa destinations, and gastronomic experiences represents an actionable portfolio diversification strategy with both demand pull and supply-side cost advantages relative to saturated Western European itineraries.

Cruise Travel Expansion as a Premium Senior Travel Vehicle in the Golden Generation Travel Market

The cruise segment's exceptional recovery to 107% of pre-pandemic passenger volumes by 2023, with Europe contributing a 6.5% incremental increase, establishes river and ocean cruising as one of the highest-growth and highest-yield product formats, given the segment's disproportionately senior demographic composition and premium spend characteristics. Global cruise volumes are projected to approach 40 million passengers by 2027, with Europe positioned as the second-largest source market, creating a structural tailwind for European senior travel operators with cruise-integrated product portfolios.

River cruising, particularly along European itineraries traversing the Rhine, Danube, and Douro, offers an especially senior-friendly travel format combining comfortable, mobility-accessible accommodation, destination-rich daily port calls, curated cultural excursions, and inclusive on-board service architectures that minimize logistical complexity for the 65-plus traveler. Viking Cruises, Tauck, and Grand Circle Travel have each invested heavily in European river cruise product development, and expanding dedicated senior-configured river cruise fleets represents a quantifiable market penetration strategy aligned with both demographic demand and product preference data.

Digital Personalization and Age-Inclusive Technology as a Competitive Differentiator

Digital transformation of the senior travel booking and experience delivery process represents a strategically underinvested opportunity in the golden generation travel market, with significant potential to reduce booking friction, increase trip conversion rates, and strengthen loyalty among an increasingly digitally confident cohort of 55- to 70-year-old travelers. ACI Europe's observation of operational challenges from new digital border systems underscores the importance of proactive digital enablement and accessibility design across the travel journey.

Tour operators and accommodation providers that invest in age-inclusive digital interfaces, AI-powered itinerary personalization, simplified mobile booking platforms, and integrated health and wellness pre-screening capabilities are positioned to capture disproportionate share among the technically confident segment of European senior travelers, a cohort that has demonstrated higher digital adoption rates post-pandemic than pre-pandemic studies projected. Partnerships between tour operators and telemedicine or travel health platforms further enable operators to address the insurance and health risk barriers identified as a market restraint, transforming a friction point into a service differentiator.

Category-wise Analysis

Travel Type Insights

Leisure Travel commands 58% of the European golden generation travel market, establishing it as the dominant travel type by a substantial margin and reflecting the fundamental character of retired and semi-retired senior travelers for whom leisure is the primary motivation for discretionary travel expenditure. This segment encompasses beach and coastal holidays, cultural city breaks, countryside touring, spa and wellness retreats, and touring that align with senior travelers' preference for comfortable, low-stress, and socially enriching experiences.

Europe's established tourism infrastructure, including Mediterranean resort destinations in Spain and Italy, which recorded the highest aggregate passenger volumes in 2025, provides a deep and geographically diverse supply base for leisure product development that sustains demand breadth across age cohorts, income levels, and physical mobility profiles within the golden generation traveler spectrum.

Adventure travel is the fastest-growing travel type in the golden generation travel market, driven by a structural generational shift in senior travelers' self-perception and aspirational travel preferences, with the active 55 to 70 age cohort increasingly rejecting passive touring models in favor of physically engaging, authentically immersive, and achievement-oriented travel experiences.

Accommodation Type Insights

Budget and mid-scale hotels command approximately 46% of the European golden generation travel market by accommodation type, reflecting the value-conscious spending behavior of the majority of European senior travelers who prioritize comfort, accessibility, and reliable service standards over luxury amenity provision. This segment encompasses well-established European hotel brands operating across the three to four-star tier, including Accor's Novotel and Mercure chains, IHG's Holiday Inn network, and Marriott's Courtyard portfolio, which deliver the predictable service standards, accessible room configurations, and convenient hub locations that senior travelers consistently prioritise in accommodation selection.

Countries such as Hungary and Poland, recording strong passenger traffic growth in 2025, are seeing investment in mid-scale hotel capacity specifically configured for touring coach and rail-linked senior itineraries, reinforcing the segment's infrastructure depth across new Eastern European corridors.

Vacation rentals are the fastest-growing accommodation type in the golden generation travel market, propelled by senior travelers' preference for longer-stay, home-like living environments that offer kitchen facilities, laundry access, private outdoor spaces, and family-group configurations all attributes particularly valued by the 60-plus traveller for extended European stays of two weeks or more.

Transportation Mode Insights

Air Travel commands approximately 44% of the European golden generation travel market by transportation mode, sustained by the segment's unmatched connectivity reach, time efficiency for long-haul international itineraries, and the progressive improvement of airport accessibility infrastructure across major European hubs. European air travel reached a record 2.6 billion passengers in 2025, with 4.4% year-on-year growth. London Heathrow and Istanbul Airport ranked as the continent's two busiest hubs, both critical gateways for senior travelers accessing cruise embarkation ports, international heritage destinations, and long-haul leisure routes.

Extra-EU travel accounted for 50.1% of all EU air passenger traffic at a 4.8% growth rate, reflecting senior travelers' strong appetite for international itineraries beyond Europe's borders, including North Africa, the Middle East, and North America. ACI Europe projects continued aviation growth of approximately 3.3% in 2026, further consolidating air travel's modal leadership within the golden generation travel purchasing basket.

Competitive Landscape

Europe golden generation travel market exhibits a fragmented competitive structure, with no single operator commanding dominant market concentration, and hundreds of specialist senior travel providers competing alongside large diversified tour operators. The top five to six players Colette Tours, Globus, Trafalgar, Viking Cruises, Grand Circle Travel, and Saga Holidays, hold the highest brand recognition and distribution scale, but collectively account for a modest share of total market revenue, with regional specialists, cruise operators, and online travel agencies competing vigorously across price tiers.

Competition is primarily differentiated on itinerary depth, accessibility, accommodation, safety reputation, and traveller community loyalty programs rather than pricing alone.

Leading players in the Europe Golden Generation Travel Market primarily pursue experience differentiation and loyalty programme investment as their dominant strategic themes, combining curated cultural access, accessible travel design, and community-building between repeat travelers as key differentiators. Subscription-based membership models providing early access booking, exclusive itinerary options, and dedicated senior travel concierge services are emerging as the dominant business model evolution, supported by AI-driven personalisation platforms that enhance trip customisation at scale.

Key Developments:

- In March 2026, Geographic Expeditions & Golden Eagle Luxury Trains expanded their European offerings with the launch of two new luxury rail voyages from Paris and Venice to the Balkans, targeting premium, long-duration experiential travel demand, which is highly aligned with the spending patterns and preferences of Golden Generation travelers seeking comfort, curated itineraries, and slow travel experiences.

- In February 2026, Thrillophilia launched a new portfolio of Europe travel packages for 2026 focused on slower, comfort-driven and immersive journeys, with a 38% increase in demand for relaxed pacing and a 19% rise in comfort-first travel preferences, aligning strongly with Golden Generation travelers seeking longer stays, fewer destinations, and culturally rich experiences.

Companies Covered in Europe Golden Generation Travel Market

- Colette Tours

- Globus

- Trafalgar

- Road Scholar

- Grand Circle Travel

- Intrepid Travel

- Overseas Adventure Travel

- ElderTreks

- Smithsonian Journeys

- Backroads

- Saga Holidays

- Viking Cruises

- Tauck

- Odysseys Unlimited

- Grand European Tours

Frequently Asked Questions

Europe Golden Generation Travel Market is projected to be valued at US$ 68.0 Bn in 2026.

Leisure Travel leads the market with approximately 68% share, driven by rising disposable incomes, growing preference for experiential and wellness-focused vacations, expansion of affordable travel options, increased connectivity, and strong post-pandemic recovery in tourism demand.

The Air Travel segment dominates the market with approximately 44.0% share, driven by increasing global connectivity, time-efficient long-distance travel demand, expansion of low-cost carriers, rising international tourism, and continuous growth in airline route networks and airport infrastructure.

Europe golden generation travel market is expected to witness a CAGR of 4.8% from 2026 to 2033.

Europe’s Golden Generation Travel Market growth is driven by rapid population ageing and high senior wealth concentration, alongside strong recovery and expansion of air and rail connectivity, and post-pandemic resurgence in senior travel demand with a shift toward premium, experiential, and cruise-based tourism.

Key market opportunities in Europe’s Golden Generation Travel Market include expansion into underpenetrated Eastern and Southern European destinations with rising tourism and cultural appeal, strong growth in cruise and river cruise travel as a premium senior-friendly segment, and digital personalisation through age-inclusive booking platforms and AI-driven travel services that enhance accessibility, convenience, and customer experience.

Key players in the Golden Generation Travel Market include Colette Tours, Globus, Trafalgar, Viking Cruises, Grand Circle Travel, and Saga Holidays.