- Automotive Components & Materials

- Europe Automotive Wiring Harness Market

Europe Automotive Wiring Harness Market Size, Share, and Growth Forecast, 2026 - 2033

Europe Automotive Wiring Harness Market By Harness Type (General Wiring Harness, High-Voltage Wiring Harness, Speciality / Data Harness), Application (Chassis Harness, Engine Harness, Sensors / ADAS Harness, EV Underfloor Harness, Body Harness, HVAC Harness) Vehicle Type (Passenger Vehicle, Light Commercial Vehicle, Heavy Commercial Vehicle, Electric Vehicle) and Regional Analysis for 2026 - 2033

Europe Automotive Wiring Harness Market Size and Trends Analysis

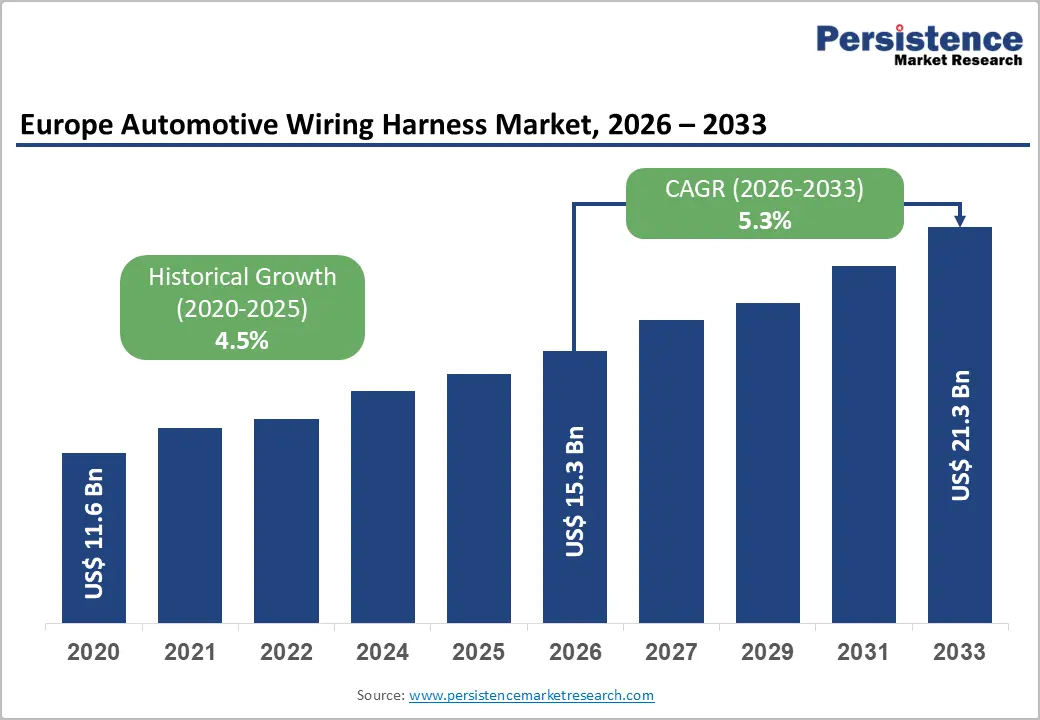

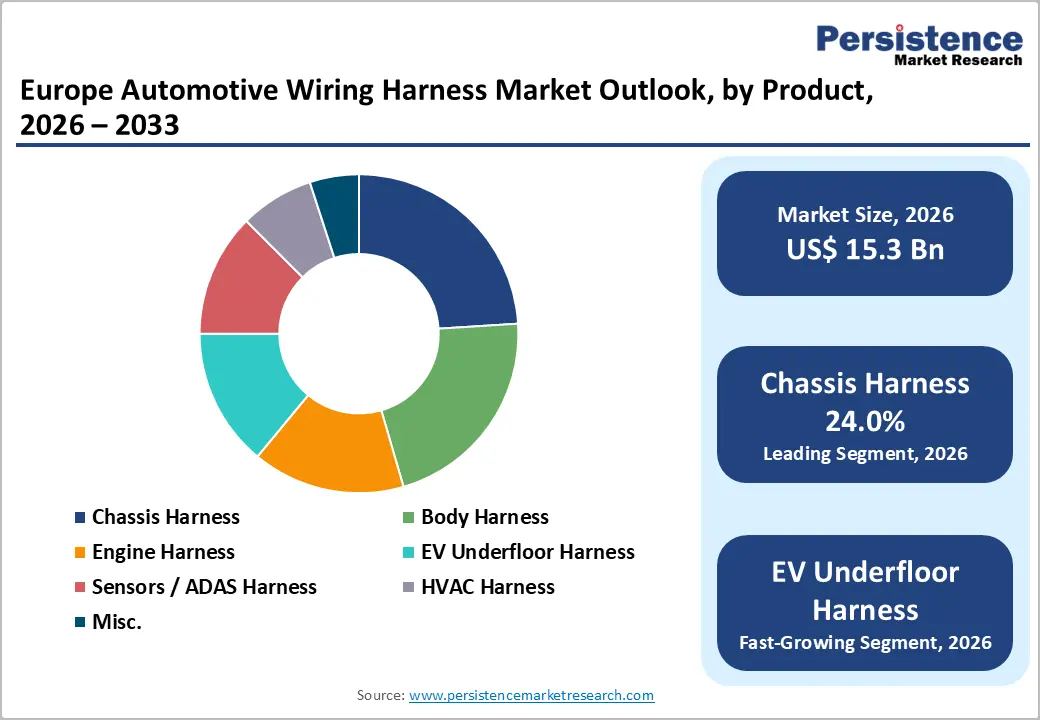

Europe Automotive Wiring Harness Market size is likely to be valued at US$15.3 billion in 2026 and is projected to reach US$21.9 billion by 2033, growing at a CAGR of 5.3% between 2026 and 2033. The EU's legally binding zero-emission vehicle mandate requiring 100% zero-emission new cars by 2035, the phased implementation of the EU General Safety Regulation mandating ADAS features across all vehicle categories, and the deepening electronics content per vehicle as average engine power has increased by 56% since 2001 have amplified the demand for automotive wiring harness in Europe.

Europe's automotive sector contributes over 7% of EU GDP and employs 13.8 million people, providing a durable industrial base that sustains demand for increasingly complex wiring harness systems across passenger cars, commercial vehicles, and electrified platforms through the forecast horizon.

Key Industry Highlights:

- Leading Regional Market: Germany dominates the europe automotive wiring harness market with 29% share, driven by strong OEM presence, premium vehicle production, and high ADAS integration.

- High-Value Leading Component: Electric Wires hold the largest share, 52%, reflecting their fundamental role in power and signal distribution across all vehicle architectures.

- Fastest-Growing Component: Connectors are the fastest-growing segment, supported by rising ECU density, ADAS integration, and high-speed data transmission requirements.

- Leading Application Segment: Chassis Harness leads with 24% share, driven by its critical role in safety systems and widespread integration across all vehicle types.

- Fastest-Growing Application Segment: EV Underfloor and Sensors/ADAS harnesses are the fastest-growing, fueled by electrification and mandatory safety regulations.

- Leading Harness Type: General (low-voltage) wiring harness dominates with a 61% share, supported by the large installed base of ICE and hybrid vehicles.

- Fastest-Growing Harness Type: High-voltage wiring harness is the fastest-growing segment, driven by rapid BEV/PHEV adoption and the expansion of 400V–800V architecture.

- Key Growth Drivers: EU CO2 mandates, GSR2 safety regulations, and strong automotive production scale are structurally increasing wiring complexity and per-vehicle harness value.

| Key Insights | Details |

|---|---|

|

Automotive Wiring Harness Size (2026E) |

US$ 15.3 Bn |

|

Market Value Forecast (2033F) |

US$ 21.9 Bn |

|

Projected Growth (CAGR 2026 to 2033) |

5.3% |

|

Historical Market Growth (CAGR 2020 to 2025) |

4.5% |

Market Dynamics

Drivers - EU Zero-Emission Vehicle Mandate Reshapes Harness Architecture Demand

The EU's phased CO2 reduction framework is the most consequential structural demand driver for the Europe Automotive Wiring Harness Market, compelling a fundamental transition in vehicle powertrain architecture and the wiring systems that serve it. The European Commission's enforceable standards require a 15% reduction in CO2 emissions by 2025, a 55% reduction in passenger-car emissions by 2030, and 100% of new vehicle sales to be zero-emission by 2035, all measured against the 2021 baseline.

In 2024, battery electric vehicles accounted for nearly 14% of EU new passenger car registrations, while plug-in hybrid electric vehicles represented approximately 7%, collectively demonstrating accelerating OEM electrification investment aligned with regulatory compliance timelines. BEV lifecycle emissions are approximately 73% lower than conventional ICE vehicles, reinforcing the policy rationale. Battery electric vehicles require entirely new high-voltage harness architectures to manage 400V to 800V power flows between battery packs, inverters, and electric motors, with per-vehicle wiring content substantially exceeding that of ICE equivalents.

Countries including Denmark at 51%, Sweden at 36%, the Netherlands at 35%, and Belgium at 29% have achieved particularly high BEV penetration, directly translating into volume demand for specialized high-voltage harness systems and EV-specific wiring assemblies in Europe automotive wiring harness market.

EU General Safety Regulation Mandates Accelerate Sensor and Data Harness Integration

The EU General Safety Regulation, Regulation EU 2019 to 2144, represents a binding technology mandate that directly amplifies wiring harness content per vehicle across the European Automotive Wiring Harness Market by requiring the mandatory integration of Advanced Driver Assistance Systems across all newly sold vehicles in Europe.

Implemented in phases, Phase 1 took effect in July 2022 for new vehicle models, Phase 2 in July 2024 applied mandatory ADAS features, including Intelligent Speed Assistance and Emergency Lane Keeping, to all existing models, and Phase 3 in July 2026 extends requirements to include Advanced driver distraction warning and additional pedestrian and cyclist Autonomous Emergency Braking systems. Each mandated ADAS function requires dedicated sensor modules, radar units, cameras, and electronic control units, all of which demand precision-engineered wiring harnesses, shielded data cables, and high-reliability connectors.

Modern vehicles equipped with full ADAS suites can contain 5 kilometers or more of electrical wiring and dozens of ECUs, substantially amplifying harness routing complexity. Germany, which contributes 21% of all cars sold in the EU and hosts key harness OEM engineering and design centers, anchors premium-segment ADAS deployment. The mandatory nature of GSR2 ensures a non-discretionary harness content floor across all European vehicle categories, providing structural demand visibility for harness manufacturers operating within the European Automotive Wiring Harness Market.

Europe's Embedded Automotive Production Scale Sustains Tier-1 Harness Demand

Europe's sustained automotive manufacturing scale provides a durable structural foundation that is reinforced by deep upstream and downstream supply chain integration. The European Union accounted for 14.6% of global vehicle production in 2025, with EU-based manufacturers supplying 73% of the domestic market and exporting over one-third of their output to international buyers. Global car production reached 78.7 million units in 2025, with worldwide registrations rising 3.5% to 77.6 million units, reflecting the continued robustness of the global vehicle market that drives European Tier-1 harness supplier volumes.

The EU automotive sector employs 13.8 million people, representing 6.1% of total EU employment, with 2.6 million in direct manufacturing accounting for 8.5% of EU manufacturing employment. The sector is the largest private R&D investor in the EU, with investment flowing into electrification, connectivity, and lightweight materials that collectively increase the harness content value per vehicle. EU GDP rose 1.5% in 2025, with a similar pace anticipated in 2026 and 2027, providing macroeconomic stability that supports automotive OEM capital investment programs and the multi-year harness development cycles.

Restraint - Copper Price Volatility and Elevated European Energy Costs Compress Harness Margins

Copper is the primary material in automotive wiring harnesses and accounts for the largest share of the bill of materials cost across low-voltage, high-voltage, and specialty harness configurations. Global copper price volatility, driven by supply constraints from primary mining and competing demand from renewable energy infrastructure build-out, directly pressures manufacturer margins and disrupts OEM procurement cost planning.

Aluminum-based wiring alternatives are under active development as lightweighting solutions, but technical challenges in achieving precision crimping, corrosion resistance, and current-carrying capacity relative to copper limit near-term substitution rates. EU automotive trade performance deteriorated materially in 2025, with imports falling 3.2% and exports declining 6.2%, compressing OEM capital expenditure available for harness technology investment and lengthening supplier qualification timelines, further amplifying raw material cost sensitivity for the market.

Geopolitical Supply Chain Fragility and Eastern Europe Labor Cost Pressures

Automotive wiring harness assembly is among the most labor-intensive manufacturing processes in the tier-1 automotive supply chain, historically dependent on cost-competitive production facilities in Eastern Europe and North Africa to serve European OEM programs. Escalating labor costs across traditional lower-cost manufacturing locations, combined with geopolitical uncertainties affecting cross-border logistics corridors, represent structural risks to harness supply continuity.

EU exports to China fell 43% in 2025 amid intensifying local competition, while EU exports to the United States declined 21.4% as a direct consequence of trade tariffs, reflecting broader trade fragility that constrains harnessing supplier revenue visibility. These dynamics elevate per-unit operational cost for European-oriented supply chains, creating compression pressure on harness delivery timelines and increasing the risk of inventory shortfalls for OEM platform launches.

Opportunities - Commercial Vehicle Electrification Creating High-Value Harness Content Demand

The progressive electrification of Europe's commercial vehicle fleet represents a significant addressable opportunity for suppliers in the European Automotive Wiring Harness Market, particularly for high-voltage and EV-specific harness architectures. Bus registrations in Europe recorded a 7.5% rebound in 2025, and specific truck configurations, including 4 into 2 and 6 into 2 rigid trucks, deployed in urban and regional delivery operations, are electrifying at an accelerating pace due to their smaller battery requirements, shorter operational ranges, and frequent stop-and-go energy recuperation cycles. The EU's phased commercial vehicle CO2 standards create a regulatory-backed upgrade cycle through 2030 that is structurally distinct from the passenger car electrification wave.

High-voltage harnesses for commercial EVs are architecturally more demanding than their passenger vehicle counterparts, requiring higher-ampacity conductors, advanced thermal management and insulation, robust electromagnetic shielding, and IP-rated sealing for underfloor and chassis routing. This elevated technical specification commands a substantial per-unit revenue premium relative to conventional commercial vehicle harness assemblies.

The EU's Green Deal, targeting carbon neutrality by 2050, is directing capital toward electrified commercial vehicle platforms at OEMs, including Volvo, Mercedes-Benz Trucks, Iveco, and Scania, all of which require qualified harness supply partnerships. Manufacturers positioned in Europe automotive wiring harness market with validated high-voltage commercial harness capabilities are therefore well-placed to capture above-average revenue per vehicle as fleet electrification accelerates through the forecast period.

ADAS Phase 3 Implementation: Catalyzing Sensors to ADAS Harness Investment

The scheduled July 2026 implementation of GSR2 Phase 3 creates a precisely timed and policy-guaranteed demand catalyst for Sensors to ADAS Harness systems within the European Automotive Wiring Harness Market, affecting all vehicle models across the EU's annual registration base of approximately 10.6 million new passenger cars.

Phase 3 mandates Advanced Driver Distraction Warning and expanded pedestrian and cyclist Autonomous Emergency Braking across all vehicle models, requiring additional sensor integration, dedicated ECU wiring circuits, and high-speed data communication cabling that were absent from pre-2026 vehicle architectures. Many vehicles sold across the UK will additionally conform to EU-specification software configurations due to the complexity of developing UK-specific variants, further broadening the addressable harness demand base.

Modern ADAS-intensive vehicles can contain several hundred individual connector interfaces; per-vehicle ECU count in vehicles complying with full GSR2 Phase 3 requirements is materially higher than pre-mandate baselines. The Specialty and Data Harness segment benefits most directly, as high-speed ADAS sensor data transmission requires shielded twisted-pair and coaxial cabling with controlled impedance.

Germany, as both the EU's largest production hub and the home base of Tier-1 ADAS harness suppliers, will serve as the primary geographic center for Phase 3 compliance investment, with harness co-development programs between OEMs and suppliers already underway. This regulatory timeline provides harness suppliers in the European Automotive Wiring Harness Market with a predictable and non-discretionary demand pipeline through 2027 and beyond.

Category-wise Analysis

Component Insights

Electric wires are the dominant component, accounting for approximately 52% of total component revenue in 2026. Their dominance reflects the foundational role of copper-conductor wiring as the primary medium for power and signal distribution across all vehicle platforms, from conventional internal combustion engines to full battery-electric architectures.

As vehicle electrical content per unit advances through electrification, mandatory ADAS integration, and infotainment proliferation, the aggregate conductor length per vehicle and total copper content per harness assembly have both risen substantially across European vehicle segments. The progressive adoption of aluminum-conductor alternatives for weight reduction, while technically constrained, is beginning to create a parallel subcategory within electric wire procurement strategies at major European OEMs.

Connectors represent the fastest-growing component segment in the European automotive wiring harness market, driven by the high density of electronic control units per vehicle and the proliferation of high-speed data interconnections required for ADAS sensor arrays, battery management systems, and infotainment networks.

Application Insights

The chassis harness segment leads the European automotive wiring harness market by application, holding approximately 24% of market revenue in 2026. Chassis harnesses integrate wiring for anti-lock braking systems, electronic stability control, suspension management sensors, transmission controls, and increasingly, chassis-level ADAS sensor clusters. Their leadership position reflects both the high base volume of conventional and hybrid vehicle platforms, which continue to represent the majority of European registrations, and the progressive addition of chassis-mounted ADAS content under the GSR2 compliance calendar. The complexity of chassis harness routing in modern vehicles, combined with vibration and thermal durability requirements, makes this a technically differentiated and relatively stable revenue segment for established harness suppliers.

The EV Underfloor Harness and Sensors to ADAS Harness categories represent the two fastest-growing application segments, reflecting the dual structural forces of fleet electrification and regulatory ADAS content mandates simultaneously reshaping European vehicle architectures. EV Underfloor Harnesses connect the high-voltage battery pack to the drivetrain, inverter, and thermal management systems and constitute the highest-value and most technically demanding harness assembly in a full BEV architecture, requiring orange-coded high-voltage cabling, robust mechanical protection, and IP67-rated sealing for underfloor exposure.

Harness Insights

The general wiring harness low voltage segment maintains the commanding majority share of the European automotive wiring harness market at approximately 61% of total harness type revenue in 2026, reflecting the still-predominant volume of conventional ICE, mild-hybrid, and full-hybrid vehicles in the European annual registration base. These vehicles operate on 12V or 48V electrical architectures governing body electronics, lighting networks, HVAC controls, instrument cluster systems, and chassis management, all of which require extensive low-voltage harness assemblies.

In 2024, gasoline and diesel vehicles continued to represent the majority of new European registrations, ensuring the General Wiring Harness Low Voltage segment sustains a substantial production volume base, even as the structural trend toward electrification progressively shifts the harness type mix across the forecast period to 2033.

The high-voltage wiring harness segment is the fastest-growing harness type in the Europe automotive wiring harness market, directly driven by the mandatory acceleration of BEV and PHEV fleet penetration across the EU. High-voltage harnesses operate at 400V to 800V architectures in modern battery-electric platforms, requiring specialized cross-linked polyethylene insulation, electromagnetic interference shielding, thermally resistant jacketing and mechanically robust routing protection, which command a significant unit revenue premium over General Wiring Harness assemblies.

Competitive Landscape

Europe automotive wiring harness market exhibits an oligopolistic competitive structure, with a small number of globally scaled Tier-1 suppliers commanding dominant shares of OEM long-term platform supply agreements. Leading players include Yazaki Corporation, Sumitomo Electric Industries, Aptiv PLC, Leoni AG, Lear Corporation, and Kromberg and Schubert. These firms operate vertically integrated networks spanning harness design, component sourcing, assembly, and logistics across Germany, Eastern Europe, and North Africa.

Market entry barriers are structurally high, driven by OEM multi-year platform qualification requirements, capital intensity of harness design tooling, and the technical certification demands associated with high-voltage EV and ADAS-compliant harness systems. The market is not fragmented; competitive positioning centers on OEM co-development depth, engineering proximity to German automotive clusters, and certified capability in high-voltage harness production.

Leading harness manufacturers are prioritizing technology differentiation through certified EV-specific high-voltage harness platforms, lightweight material innovation incorporating aluminum conductor integration, and modular harness architecture design to reduce OEM platform complexity and assembly labor cost. Strategic investment themes include geographic proximity to German and Central European OEM assembly hubs, multi-decade OEM co-development agreements, vertical integration of connector and terminal component supply, and accelerated R&D in data transmission harnesses for software-defined vehicle architectures.

Key Developments:

- In 2024, DRÄXLMAIER Group showcased advanced low-voltage, high-voltage, and battery-integrated wiring harness innovations at the International Suppliers Fair (IZB) 2024 in Germany, including intelligent harness architectures for semi-autonomous driving and the “dFUSE smart HV” system for enhanced safety and efficiency in 400V–800V EV platforms, reinforcing its position in next-generation vehicle electrification and connectivity solutions.

- In 2023, Yazaki Corporation & NEC Corporation conducted a successful demonstration of an AI-driven robotic planning system for automotive wiring harness manufacturing, reducing robot programming time from 40 days to 1 day and improving production efficiency by ~10%, with commercialization targeted by July 2025 to enable scalable, flexible, and energy-efficient harness production.

- In 2025, Aptiv PLC: Aptiv announced the strategic spin-off of its Electrical Distribution Systems (EDS) business into a separate independent entity, aimed at strengthening focus on low- and high-voltage wiring harness systems and positioning the new EDS company to capitalize on growing demand for power and data distribution solutions in automotive and commercial vehicles.

Companies Covered in Europe Automotive Wiring Harness Market

- Sumitomo Electric Industries

- YAZAKI Corporation

- Fuzikura

- Aptiv PLC

- Lear Corporation

- Motherson Group

- LEONI Group

- Luxshare Precision

- Cloom Tech

- Tianhai Auto Electronics Group Co., Ltd. (THB Group)

- Kromberg & Schubert GmbH Cable & Wire

Frequently Asked Questions

Europe Automotive Wiring Harness is projected to be valued at US$ 15.3 Bn in 2026.

The Radiators segment is expected to account for approximately 61% of the Europe Automotive Wiring Harness by Harness Type in 2026.

The market is expected to witness a CAGR of 5.3% from 2026 to 2033.

Europe Automotive Wiring Harness market growth is driven by EU zero-emission mandates accelerating EV adoption (boosting high-voltage harness demand), mandatory ADAS regulations increasing sensor/data wiring complexity, and strong automotive production scale sustaining Tier-1 supplier volumes.

Key opportunities in the Europe Automotive Wiring Harness market stem from commercial vehicle electrification driving high-value high-voltage harness demand and upcoming ADAS Phase 3 regulations accelerating investment in sensor and data harness systems.

Key players in Automotive Wiring Harness include Yazaki Corporation, Sumitomo Electric Industries, Aptiv PLC, Leoni AG, Lear Corporation, and Kromberg and Schubert.