- Automotive Components & Materials

- Europe Automotive Heat Exchanger Market

Europe Automotive Heat Exchanger Market Size, Share, and Growth Forecast, 2026 - 2033

Europe Automotive Heat Exchanger Market by Product Type (Radiators, Intercoolers, Air Conditioning Systems, Oil Coolers, EGR Coolers, Others), Design (Plate-fin, Tube-fin), Vehicle Type (Passenger Vehicles (Compact Cars, Mid-size Cars, SUVs, Luxury Vehicles), Light Commercial Vehicle, Heavy Commercial Vehicle, Electric Vehicle), and Regional Analysis for 2026 - 2033

Europe Automotive Heat Exchanger Market Size and Trends Analysis

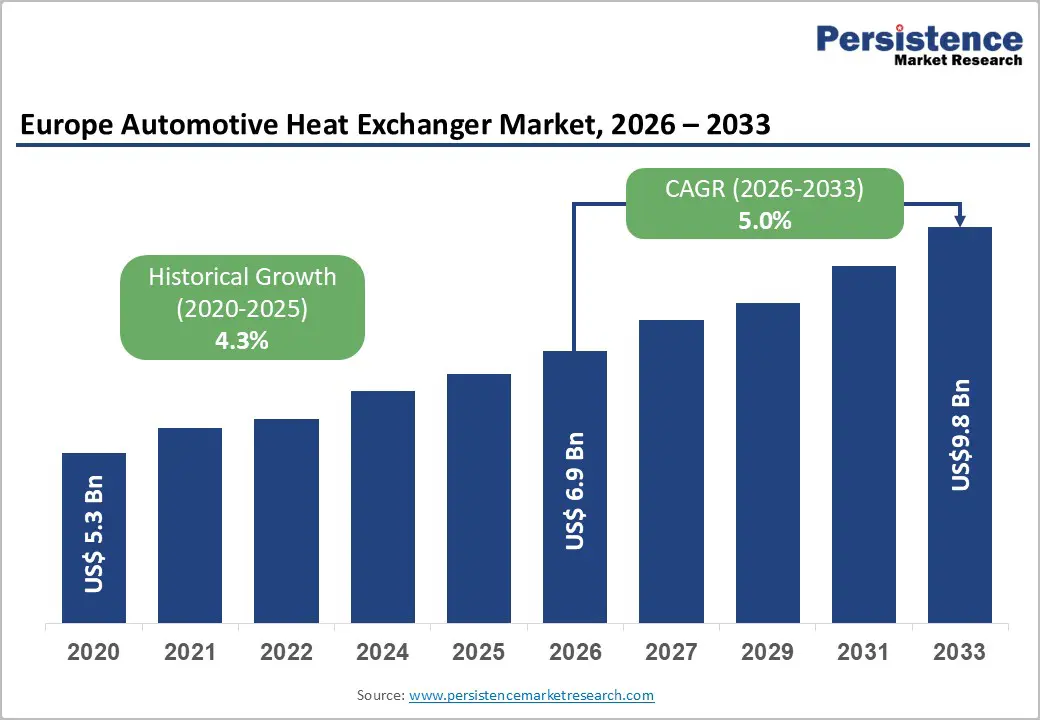

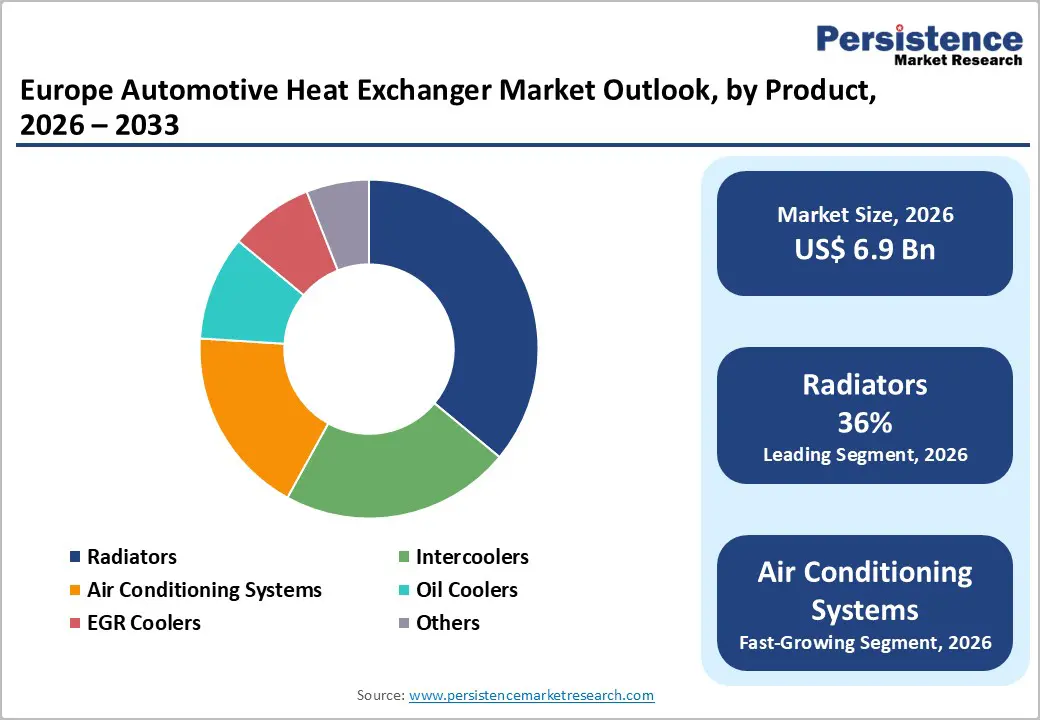

Europe Automotive Heat Exchanger Market size is likely to be valued at US$ 6.9 billion in 2026 and is projected to reach US$ 9.8 billion by 2033, growing at a CAGR of 5.0% between 2026 and 2033.

The market's forward trajectory is anchored by the accelerating electrification of Europe's automotive fleet, tightening EU emission mandates, and substantial OEM investment in next-generation thermal management architectures. The European Union registered approximately 10.6 million new passenger cars in 2024, with battery electric vehicles accounting for nearly 14% of all new passenger car registrations, a structural shift demanding more sophisticated heat exchanger configurations across vehicle platforms. Building from a 2020 base value of US$5.3 billion at a historical CAGR of 4.3%, the market is transitioning from incremental product improvement toward systemic redesign of thermal systems to serve both zero-emission and compliant combustion-engine vehicles simultaneously.

Key Industry Highlights:

- Leading Regional Market: Germany dominates the European Automotive Heat Exchanger Market, accounting for approximately 26% of all new EU passenger car registrations, supported by dense automotive engineering and OEM activity.

- High-Value Leading Segment: Radiators hold the largest share at 36% of the market, reflecting continued demand from internal combustion engine vehicles and high-capacity thermal management requirements.

- Fastest-Growing Segment: Air conditioning systems are the fastest-growing product type, driven by integration with EV heat pump circuits and rising demand for year-round cabin thermal comfort.

- Leading Vehicle Type: Passenger vehicles remain the largest segment with 54% market share, reflecting Europe’s personal mobility culture and broad OEM production volumes.

- Fastest-Growing Vehicle Type: Electric vehicles are the fastest-growing segment, supported by EU zero-emission mandates, expanding charging infrastructure, and specialised thermal management needs per unit.

- Key Growth Drivers: EU CO2 emission regulations, fleet electrification, and cross-continental OEM supply chain integration are compelling demand for advanced EGR coolers, intercoolers, and battery-specific heat exchangers.

| Key Insights | Details |

|---|---|

|

Automotive Heat Exchanger Size (2026E) |

US$ 6.9 Bn |

|

Market Value Forecast (2033F) |

US$ 9.8 Bn |

|

Projected Growth (CAGR 2026 to 2033) |

5.0% |

|

Historical Market Growth (CAGR 2020 to 2025) |

4.3% |

Market Dynamics

Drivers - EU Emission Regulatory Framework Compelling Systemic Thermal Management Redesign

Stringent EU CO2 regulations represent the most decisive policy force shaping demand trajectories in the Europe Automotive Heat Exchanger Market. These standards compel automakers and thermal component suppliers to fundamentally re-engineer vehicle heat management to achieve statutory compliance across all newly registered fleets.

The European Union introduced updated CO2 standards in 2025, mandating a 15% emission reduction by 2025, a 55% reduction for passenger cars by 2030, and a 100% zero-emission requirement for all new passenger cars by 2035 relative to the 2021 baseline.

In 2024, the average CO2 emissions of newly registered EU passenger cars stood at approximately 108 g/km under the Worldwide Harmonised Light Vehicles Test Procedure, with Germany recording 117 g/km in 2024 compared with 106 g/km in 2022 a deterioration that intensifies pressure on OEMs in the region's largest automotive market. All manufacturers successfully complied with 2024 fleet targets, but the accelerating thresholds toward 2030 require heat exchanger solutions that can simultaneously manage battery thermal loads, cabin climate control, and residual drivetrain heat. This regulatory pressure directly drives procurement of advanced EGR coolers, intercoolers, and battery-specific thermal exchange systems across all vehicle segments.

Electrification of Europe's Vehicle Fleet: Transforming Heat Exchanger Product Architecture

The structural transition of Europe's automotive market toward battery electric and plug-in hybrid vehicles is fundamentally altering the thermal management requirements that drive demand in the European Automotive Heat Exchanger Market. Unlike conventional internal combustion engine vehicles, electrified platforms require integrated and multi-function heat exchanger systems covering battery cooling, power electronics thermal management, and cabin heat pump functionality.

In 2024, battery electric vehicles accounted for nearly 14% of all new EU passenger car registrations and plug-in hybrid electric vehicles represented approximately 7%, with Denmark at 51%, Sweden at 36%, and the Netherlands at 35% leading national adoption rates. Battery electric vehicles reduce life-cycle emissions by approximately 73% compared with petrol vehicles, making them the centrepiece of the EU's transport decarbonisation strategy.

MAHLE's production-ready compact thermal management module, showcased at IAA Mobility in September 2025, demonstrated a heat pump system capable of extending electric vehicle range by up to 20%, while the MAHLE HeatX Range+ system introduced in February 2026 reduces cabin heating energy demand by up to 20% and extends winter driving range by nearly 10 km. These innovations confirm the depth of R&D investment, redirecting the European heat exchanger industry toward electrification-compatible product lines.

North American and Cross-Continental Trade Dynamics Reinforcing Supply Chain Integration

The deepening integration of global automotive supply chains, particularly within the North American trade corridor that influences European supplier networks and component sourcing, creates secondary demand reinforcement for the Europe Automotive Heat Exchanger Market. As European automotive OEMs supply vehicles and powertrains across continental boundaries, thermal management components must comply with multi-regional regulatory environments

According to the Bureau of Transportation Statistics, total transborder freight between the United States and North American partners reached $124.8 billion in November 2025, with computer-related machinery and automotive components together representing approximately $44.8 billion in cross-border commodity value. Motor vehicles and automotive components specifically totalled approximately $18.0 billion in cross-border trade value, underscoring the depth of integrated supply chain dependency between European OEM design centres and North American assembly operations. For European heat exchange manufacturers such as MAHLE, Valeo, and DENSO, whose production footprints span both continents, this level of cross-border integration reinforces consistent demand for thermally compliant components across international vehicle programmes.

Restraint - Raw Material Price Volatility Compressing Component Manufacturer Margins

Automotive heat exchangers rely heavily on aluminium, copper, and speciality alloys as primary production materials. European heat exchanger manufacturers face sustained exposure to commodity price fluctuations driven by global energy costs, mining output variability, and geopolitical supply disruptions. As vehicle architecture evolves toward lighter multi-material assemblies, the per-unit material cost of advanced thermal systems escalates.

Valeo's March 2026 initiative to adopt recycled and bio-based materials in front cooling modules and heat exchanger water tanks, enabling up to a 35% reduction in carbon footprint, signals industry acknowledgement that raw material cost and sustainability pressures are structural constraints requiring redesign-led rather than procurement-led solutions.

Technological Complexity and High Development Costs of EV-Compatible Systems

The transition from single-function heat exchangers to integrated multi-circuit thermal systems significantly raises development expenditure and unit cost for both OEMs and Tier 1 suppliers in the Europe Automotive Heat Exchanger Market. Battery thermal management systems, heat pump integration, and electronics cooling modules require new manufacturing processes, tooling investments, and validation cycles that extend product development timelines.

Modine Manufacturing's decision to begin manufacturing battery thermal management and electronics cooling systems for electric commercial vehicles at its Pontevico facility in 2024 illustrates the capital intensity of repositioning conventional production assets toward EV-compatible thermal platforms. These high entry barriers disproportionately challenge smaller regional component manufacturers competing against well-capitalised global Tier 1 suppliers.

Opportunity - Lightweight and Sustainable Material Innovation Opening Premium Product Differentiation

The adoption of advanced lightweight and sustainable materials in automotive heat exchanger manufacturing represents a high-value commercial opportunity within the Europe Automotive Heat Exchanger Market. As EU emission targets and vehicle weight regulations simultaneously tighten, OEMs place a premium on thermally efficient components that also reduce overall vehicle mass and embodied carbon.

Valeo's announcement at JEC World 2026 in March 2026 highlighted the use of recycled and bio-based materials in front cooling modules and heat exchanger water tanks, achieving up to a 35% reduction in carbon footprint relative to conventional designs. This innovation directly responds to OEM procurement mandates that now include lifecycle carbon criteria alongside unit performance benchmarks.

Suppliers capable of commercializing lightweight heat exchanger solutions at production scale stand to capture premium contracts across passenger vehicle, light commercial vehicle, and electric vehicle programmes, particularly in Germany, which accounts for approximately 26% of all EU new passenger car registrations and hosts the region's densest concentration of automotive engineering investment.

Rapid Expansion of EV Charging Infrastructure Accelerating Thermal System Demand

The accelerating deployment of public electric vehicle charging infrastructure across Europe creates a parallel structural opportunity for heat exchanger manufacturers to serve the Europe Automotive Heat Exchanger Market. As charging becomes more accessible, consumer confidence in electric vehicle adoption strengthens, which directly translates to higher procurement volumes for EV-specific thermal management components.

By mid-2025, Europe had approximately eight public charging points per 1,000 passenger cars and vans, compared with just one charger per 1,000 vehicles in early 2021, an eightfold in infrastructure density within four years. This charging availability underpins accelerated battery electric vehicle uptake, and each electric vehicle platform requires dedicated battery cooling circuits, heat pump assemblies, and power electronics thermal management systems that conventional combustion vehicles do not require. DENSO's February 2025 European product portfolio expansion, which added 32 new thermal components covering over 1,000 vehicle applications, including the Nissan Leaf and Volkswagen ID.3, demonstrates how suppliers are proactively scaling aftermarket and OEM coverage to serve the broadening EV parc across the continent.

Commercial Vehicle Electrification: Creating an Underpenetrated Thermal Management Segment

The electrification of light and heavy commercial vehicles represents an emerging and structurally underpenetrated opportunity for suppliers active in the European Automotive Heat Exchanger Market. Commercial vehicle thermal demands differ substantially from passenger vehicle requirements, with heavier duty cycles, more demanding thermal loads, and longer service life expectations creating a distinct premium product category.

In 2024, new heavy-duty truck and bus registrations in the EU declined by approximately 5% to 363,500 vehicles, but electrification within this segment is beginning at the level of urban delivery and regional freight vehicles. Rigid trucks configured for urban and regional use, such as 4x2 and 6x2 variants, are electrifying ahead of long-haul tractor-trailers due to shorter routes, smaller battery requirements, and greater energy recuperation potential from frequent stops. Modine Manufacturing's October 2023 announcement confirmed that its Pontevico, Italy, facility would begin manufacturing EVantage thermal management and electronics cooling systems for electric commercial vehicles from 2024, marking a strategic first-mover position in a segment where dedicated thermal solution supply remains limited, and pricing power is structurally favourable for early entrants.

Category-wise Analysis

Product Type Insights

Radiators hold the largest share of Europe Automotive Heat Exchanger Market by product type, commanding approximately 36% of the total market value in 2026. This dominance reflects the continued prevalence of internal combustion engine vehicles across the European fleet, where coolant-based radiators serve as the primary heat rejection mechanism for engine thermal management. The EU's approximately 10.6 million new passenger car registrations in 2024, the majority of which were still gasoline and diesel powered, sustain consistent OEM and aftermarket demand for radiator assemblies at scale.

DENSO's February 2025 European portfolio expansion included 9 new radiator variants covering over 1,000 vehicle applications across both conventional and electric models, illustrating the segment's continued commercial relevance alongside the electrification transition. As vehicle weight reached an average of 1,554 kg in 2024, 22% higher than in 2001, and average engine power increased by 56% over the same period, thermal loads managed by radiators have intensified, supporting demand for higher-capacity and thermally efficient radiator designs rather than volume contraction.

Air Conditioning Systems represent the fastest-growing product type within the Europe Automotive Heat Exchanger Market, driven by the convergence of EV-specific thermal comfort requirements, regulatory pressure on thermal efficiency, and climate-driven demand for year-round cabin conditioning across all vehicle segments. In electrified vehicles, the air conditioning system is structurally integrated with the heat pump circuit, creating a combined thermal management architecture that replaces the separate systems found in conventional vehicles.

Vehicle Type Insights

Passenger vehicles account for approximately 54% in 2026, reflecting Europe's dominant personal mobility culture, established OEM production volumes, and the broad diversity of heat exchanger requirements across compact, mid-size, SUV, and luxury vehicle segments. The EU registered approximately 10.6 million new passenger cars in 2024, maintaining the recovery trajectory established in 2022 and 2023 following the pandemic slowdown. SUVs and off-road vehicles captured 48% of all new EU registrations in 2024, representing the single largest vehicle format and commanding the most thermally complex combustion-era platforms.

Germany's position as the EU's largest automotive market, accounting for approximately 26% of all new passenger car registrations, concentrates passenger vehicle heat exchanger demand in a single high-value geography served by all major European Tier 1 thermal suppliers. Valeo's record order intakes exceeding €4 billion in 2022 for thermal systems supporting vehicle electrification, including contracts with Stellantis and other major passenger vehicle OEMs for heat pump technologies and front-end cooling modules, confirms the segment's commercial primacy within Europe Automotive Heat Exchanger Market.

Electric vehicles represent the fastest-growing segment within the Europe Automotive Heat Exchanger Market's vehicle type classification, driven by regulatory mandates, fleet emission targets, expanding charging infrastructure, and manufacturer electrification commitments across all vehicle categories. Battery electric vehicles require fundamentally different and more complex thermal management systems than conventional combustion vehicles, creating incremental demand for specialised heat exchanger components per unit that exceeds conventional vehicle content values.

In 2024, battery electric vehicles accounted for nearly 14% of all new EU passenger car registrations, with adoption rates exceeding 50% in Denmark and 35% in Sweden. The EU's legislated requirement for 100% zero-emission new passenger cars by 2035 ensures a structurally expanding electric vehicle fleet throughout the forecast horizon. MAHLE's compact thermal management module with integrated heat pump, presented in production-ready form at IAA Mobility in September 2025, extends EV driving range by up to 20%, while Modine's EVantage systems for electric commercial vehicles reinforce supplier readiness across both passenger and commercial electric vehicle segments.

Competitive Landscape

Europe automotive heat exchanger market is moderately fragmented, with several global Tier-1 automotive suppliers and specialized thermal system manufacturers competing across OEM and aftermarket channels. A few established companies dominate technological development and maintain strong partnerships with major European automakers, while smaller suppliers focus on niche applications and regional supply chains.

Key players shaping the competitive landscape include MAHLE GmbH, Valeo SA, DENSO Corporation, Modine Manufacturing Company, AKG Group, and Marelli. These companies compete through innovation in lightweight aluminum heat exchangers, EV battery cooling systems, and integrated thermal management technologies. The rapid electrification of vehicles and strict European emission regulations are further intensifying competition, encouraging suppliers to develop advanced cooling solutions tailored for hybrid and electric vehicle platforms.

Key Industry Developments:

- In February 2026 – MAHLE GmbH introduced the HeatX Range+ heat recovery system for electric vehicles, which reduces cabin heating energy demand by up to 20% and can extend EV driving range by nearly 10 km, strengthening innovation in automotive thermal management and heat exchanger technologies in Europe.

- In February 2025 – DENSO expanded its thermal management product portfolio in Europe by adding 32 new components, including AC condensers, radiators, a cooling fan, and heater core, covering more than 1,000 vehicle applications and supporting the growing demand for advanced automotive heat exchanger and engine cooling solutions.

Europe Automotive Heat Exchanger Segmentation

By Equipment Type

- Radiators

- Oil Coolers

- Air Conditioning Systems

- Intercoolers

- EGR Coolers

- Others

By Installation Type

- Plate-fin

- Tube-fin

- Others

By Industry

- Passenger Vehicles

- Compact Cars

- Mid-size Cars

- SUVs

- Luxury Vehicles

- Light Commercial Vehicle

- Heavy Commercial Vehicle

- Electric Vehicle

By Country

- Germany

- France

- U.K.

- Italy

- Spain

- Türkiye

- Russia

- Rest of Europe

Companies Covered in Europe Automotive Heat Exchanger Market

- MAHLE GmbH

- Valeo SA

- Denso Thermal Systems S.p.A.

- Modine Manufacturing Company

- TitanX Engine Cooling

- AKG Group

- Dana Incorporated

- NRF B.V.

- Grayson Thermal Systems

- Marelli

- Sanden Holdings Corporation

Frequently Asked Questions

Europe Automotive Heat Exchanger is projected to be valued at US$ 6.9 Bn in 2026.

The Radiators segment is expected to account for approximately 36% of the Europe Automotive Heat Exchanger by Product type in 2026.

The market is expected to witness a CAGR of 5.0% from 2026 to 2033.

The Europe Automotive Heat Exchanger Market growth is primarily driven by stringent EU CO₂ emission regulations, accelerating electrification of passenger and commercial vehicles, and cross-continental OEM supply chain integration requiring advanced thermal management solutions.

Key market opportunities in the Europe Automotive Heat Exchanger Market lie in the adoption of lightweight and sustainable materials, expansion of EV charging infrastructure driving demand for advanced thermal systems, and the electrification of commercial vehicles, creating a structurally underpenetrated high-value segment.