- Executive Summary

- Global DNA Synthesis Market Snapshot 2026 and 2033

- Market Opportunity Assessment, 2026 - 2033, US$ Bn

- Key Market Trends

- Industry Developments and Key Market Events

- Demand Side and Supply Side Analysis

- PMR Analysis and Recommendations

- Market Overview

- Market Scope and Definitions

- Market Dynamics

- Driver

- Restraint

- Opportunities

- Trends

- Macro-Economic Factors

- Global GDP Outlook

- Global Healthcare Expenditure

- Forecast Factors - Relevance and Impact

- COVID-19 Impact Assessment

- Value Added Insights

- Value Chain analysis

- Key Market Players

- Product Adoption Analysis

- Key Promotional Strategies by key players

- PESTLE Analysis

- Porter's Five Forces Analysis

- Regulatory and Technology Landscape

- Price Trend Analysis, 2025

- Region-wise Price Analysis

- Price by Segments

- Price Impact Factors

- Global DNA Synthesis Market Outlook: Historical (2020 - 2025) and Forecast (2026 - 2033)

- Key Highlights

- Global DNA Synthesis Market Outlook: Product

- Introduction/Key Findings

- Historical Market Size (US$ Bn) Analysis by Product, 2020-2025

- Current Market Size (US$ Bn) Forecast, by Product, 2026-2033

- Oligonucleotides (short DNA sequences)

- Gene synthesis (custom genes)

- DNA libraries

- Reagents & kits

- Instruments & synthesizers

- Market Attractiveness Analysis: Product

- Global DNA Synthesis Market Outlook: Application

- Introduction/Key Findings

- Historical Market Size (US$ Bn) Analysis by Application, 2020-2025

- Current Market Size (US$ Bn) Forecast, by Application, 2026-2033

- Research & Development (R&D)

- Diagnostics

- Therapeutics

- Academic use

- Industrial use

- Market Attractiveness Analysis: Application

- Global DNA Synthesis Market Outlook: End User

- Introduction/Key Findings

- Historical Market Size (US$ Bn) Analysis by End User, 2020-2025

- Current Market Size (US$ Bn) Forecast, by End User, 2026-2033

- Biotech & pharma companies

- Academic & research institutes

- Contract research organizations (CROs)

- Clinical laboratories

- Market Attractiveness Analysis: End User

- Global DNA Synthesis Market Outlook: Region

- Key Highlights

- Historical Market Size (US$ Bn) Analysis by Region, 2020-2025

- Current Market Size (US$ Bn) Forecast, by Region, 2026-2033

- North America

- Europe

- East Asia

- South Asia & Oceania

- Latin America

- Middle East & Africa

- Market Attractiveness Analysis: Region

- North America DNA Synthesis Market Outlook: Historical (2020 - 2025) and Forecast (2026 - 2033)

- Key Highlights

- North America Market Size (US$ Bn) Forecast, by Country, 2026-2033

- U.S.

- Canada

- North America Market Size (US$ Bn) Forecast, by Product, 2026-2033

- Oligonucleotides (short DNA sequences)

- Gene synthesis (custom genes)

- DNA libraries

- Reagents & kits

- Instruments & synthesizers

- North America Market Size (US$ Bn) Forecast, by Application, 2026-2033

- Research & Development (R&D)

- Diagnostics

- Therapeutics

- Academic use

- Industrial use

- North America Market Size (US$ Bn) Forecast, by End User, 2026-2033

- Biotech & pharma companies

- Academic & research institutes

- Contract research organizations (CROs)

- Clinical laboratories

- Europe DNA Synthesis Market Outlook: Historical (2020 - 2025) and Forecast (2026 - 2033)

- Key Highlights

- Europe Market Size (US$ Bn) Forecast, by Country, 2026-2033

- Germany

- Italy

- France

- U.K.

- Spain

- Russia

- Rest of Europe

- Europe Market Size (US$ Bn) Forecast, by Product, 2026-2033

- Oligonucleotides (short DNA sequences)

- Gene synthesis (custom genes)

- DNA libraries

- Reagents & kits

- Instruments & synthesizers

- Europe Market Size (US$ Bn) Forecast, by Application, 2026-2033

- Research & Development (R&D)

- Diagnostics

- Therapeutics

- Academic use

- Industrial use

- Europe Market Size (US$ Bn) Forecast, by End User, 2026-2033

- Biotech & pharma companies

- Academic & research institutes

- Contract research organizations (CROs)

- Clinical laboratories

- East Asia DNA Synthesis Market Outlook: Historical (2020 - 2025) and Forecast (2026 - 2033)

- Key Highlights

- East Asia Market Size (US$ Bn) Forecast, by Country, 2026-2033

- China

- Japan

- South Korea

- East Asia Market Size (US$ Bn) Forecast, by Product, 2026-2033

- Oligonucleotides (short DNA sequences)

- Gene synthesis (custom genes)

- DNA libraries

- Reagents & kits

- Instruments & synthesizers

- East Asia Market Size (US$ Bn) Forecast, by Application, 2026-2033

- Research & Development (R&D)

- Diagnostics

- Therapeutics

- Academic use

- Industrial use

- East Asia Market Size (US$ Bn) Forecast, by End User, 2026-2033

- Biotech & pharma companies

- Academic & research institutes

- Contract research organizations (CROs)

- Clinical laboratories

- South Asia & Oceania DNA Synthesis Market Outlook: Historical (2020 - 2025) and Forecast (2026 - 2033)

- Key Highlights

- South Asia & Oceania Market Size (US$ Bn) Forecast, by Country, 2026-2033

- India

- Southeast Asia

- ANZ

- Rest of SAO

- South Asia & Oceania Market Size (US$ Bn) Forecast, by Product, 2026-2033

- Oligonucleotides (short DNA sequences)

- Gene synthesis (custom genes)

- DNA libraries

- Reagents & kits

- Instruments & synthesizers

- South Asia & Oceania Market Size (US$ Bn) Forecast, by Application, 2026-2033

- Research & Development (R&D)

- Diagnostics

- Therapeutics

- Academic use

- Industrial use

- South Asia & Oceania Market Size (US$ Bn) Forecast, by End User, 2026-2033

- Biotech & pharma companies

- Academic & research institutes

- Contract research organizations (CROs)

- Clinical laboratories

- Latin America DNA Synthesis Market Outlook: Historical (2020 - 2025) and Forecast (2026 - 2033)

- Key Highlights

- Latin America Market Size (US$ Bn) Forecast, by Country, 2026-2033

- Brazil

- Mexico

- Rest of LATAM

- Latin America Market Size (US$ Bn) Forecast, by Product, 2026-2033

- Oligonucleotides (short DNA sequences)

- Gene synthesis (custom genes)

- DNA libraries

- Reagents & kits

- Instruments & synthesizers

- Latin America Market Size (US$ Bn) Forecast, by Application, 2026-2033

- Research & Development (R&D)

- Diagnostics

- Therapeutics

- Academic use

- Industrial use

- Latin America Market Size (US$ Bn) Forecast, by End User, 2026-2033

- Biotech & pharma companies

- Academic & research institutes

- Contract research organizations (CROs)

- Clinical laboratories

- Middle East & Africa DNA Synthesis Market Outlook: Historical (2020 - 2025) and Forecast (2026 - 2033)

- Key Highlights

- Middle East & Africa Market Size (US$ Bn) Forecast, by Country, 2026-2033

- GCC Countries

- South Africa

- Northern Africa

- Rest of MEA

- Middle East & Africa Market Size (US$ Bn) Forecast, by Product, 2026-2033

- Oligonucleotides (short DNA sequences)

- Gene synthesis (custom genes)

- DNA libraries

- Reagents & kits

- Instruments & synthesizers

- Middle East & Africa Market Size (US$ Bn) Forecast, by Application, 2026-2033

- Research & Development (R&D)

- Diagnostics

- Therapeutics

- Academic use

- Industrial use

- Middle East & Africa Market Size (US$ Bn) Forecast, by End User, 2026-2033

- Biotech & pharma companies

- Academic & research institutes

- Contract research organizations (CROs)

- Clinical laboratories

- Competition Landscape

- Market Share Analysis, 2025

- Market Structure

- Competition Intensity Mapping

- Competition Dashboard

- Company Profiles

- Brooks Automation, Inc. (GENEWIZ)

- Company Overview

- Product Portfolio/Offerings

- Key Financials

- SWOT Analysis

- Company Strategy and Key Developments

- Boster Biological Technology

- ProteoGenix

- Biomatik

- ProMab Biotechnologies, Inc

- Thermo Fisher Scientific, Inc

- Integrated DNA Technologies, Inc

- OriGene Technologies, Inc

- Brooks Automation, Inc. (GENEWIZ)

- Appendix

- Research Methodology

- Research Assumptions

- Acronyms and Abbreviations

- Biotechnology

- DNA Synthesis Market

DNA Synthesis Market Size, Share, and Growth Forecast 2026 - 2033

DNA Synthesis Market by Product (Oligonucleotides, Gene synthesis, DNA libraries, Reagents & kits, Instruments & synthesizers), Application (Research & Development, Diagnostics, Therapeutics, Academic use, Industrial use), End-user (Biotech & pharma companies, Academic & research institutes, Contract research organizations, Clinical laboratories), Regional Analysis for 2026 - 2033

DNA Synthesis Market Size and Trend Analysis

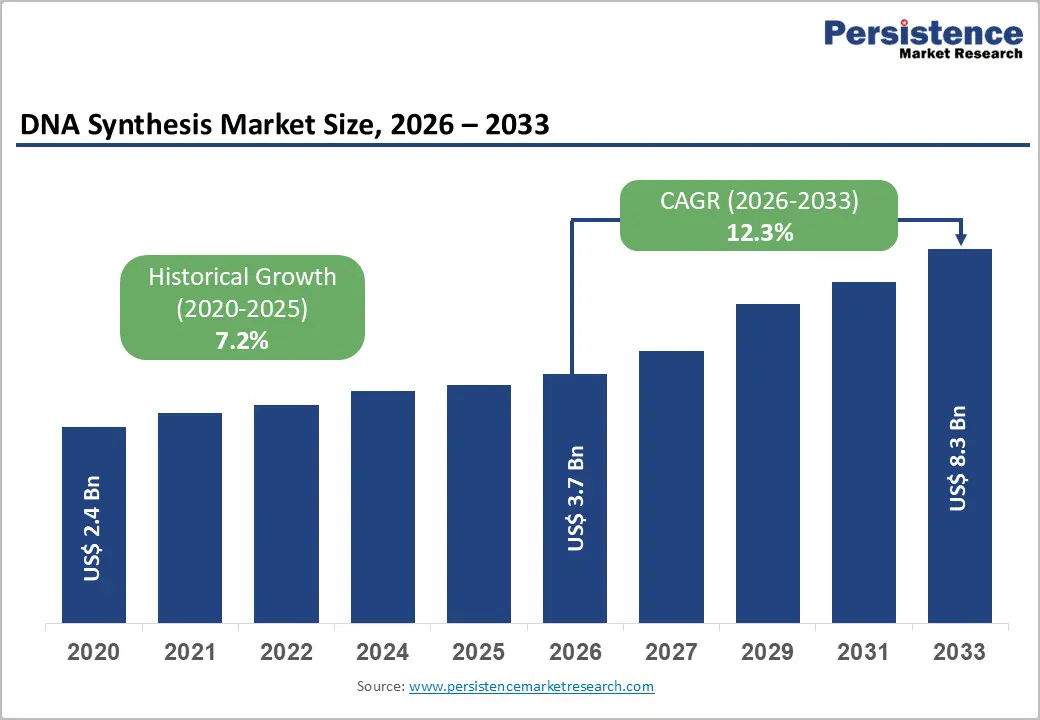

The global DNA synthesis market size is expected to be valued at US$ 3.7 billion in 2026 and projected to reach US$ 8.3 billion by 2033, growing at a CAGR of 12.3% between 2026 and 2033.

Market expansion is fundamentally driven by three distinct structural mechanisms rather than by incremental growth in research demand. First, CRISPR therapeutics achieving clinical approval and demonstrating durable efficacy (Casgevy achieving first-ever CRISPR medicine approval for sickle cell disease in late 2023, with 50+ active treatment sites operating across North America, the European Union, and Middle East) establishes structural therapeutic demand requiring specialized DNA synthesis for guide RNA, donor DNA, and therapeutic manufacturing, translating to permanent production capacity expansion.

Key Highlights:

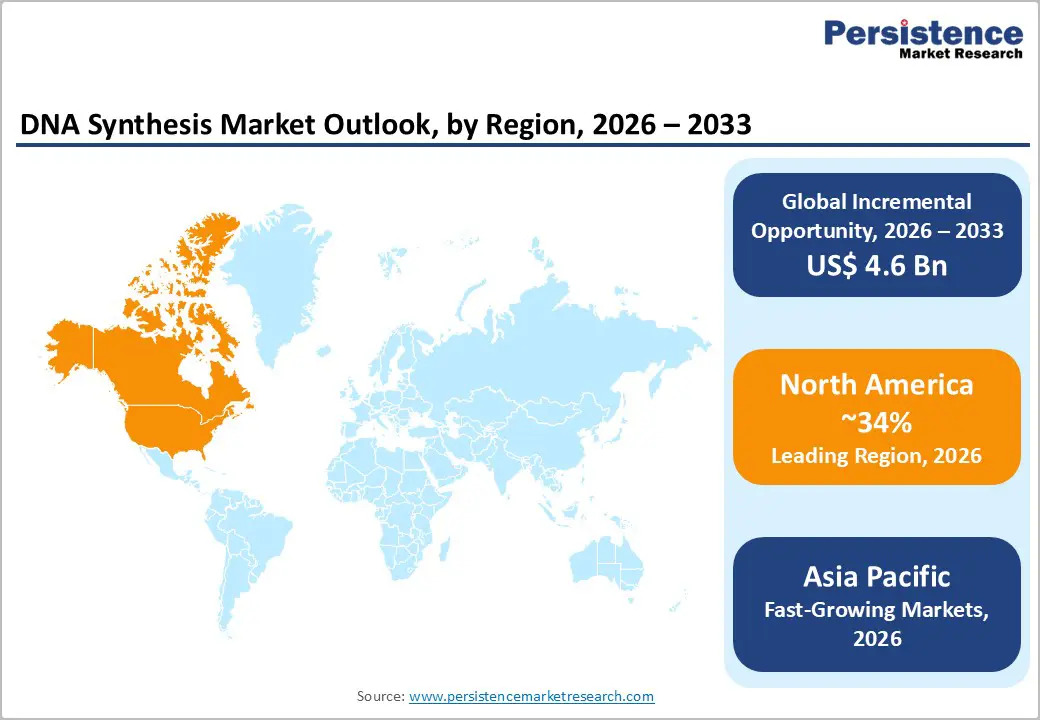

- Leading Region: North America led the DNA synthesis market with 34% share in 2025, supported by advanced biotech infrastructure, strong NIH funding, and CRISPR therapeutic commercialization following Casgevy approval.

- Fastest-Growing Region: Asia-Pacific is projected to register a 19.7% CAGR through 2033, driven by cost-efficient manufacturing, government-backed CRISPR initiatives, and supply chain diversification.

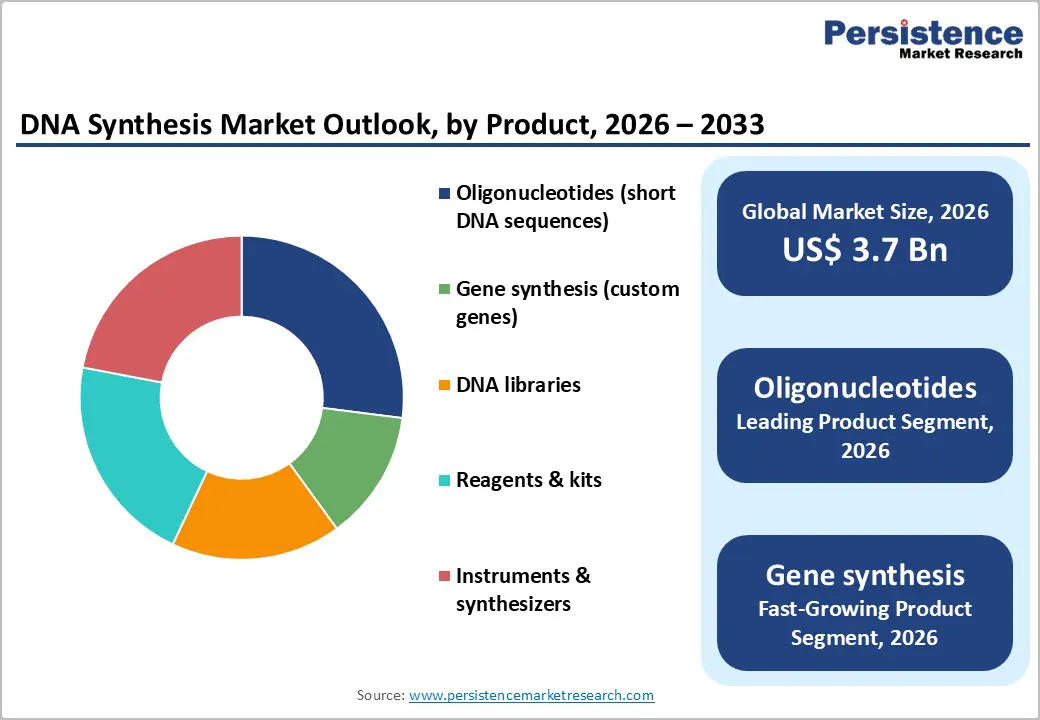

- Dominant Product: Oligonucleotides accounted for 27% of the market in 2025, driven by widespread use in PCR, diagnostics, and therapeutic development.

- Fastest-Growing Product: Gene synthesis is the fastest-growing segment, driven by advances in CRISPR, gene therapy, and synthetic biology.

- Key Opportunity: Personalized and variant-specific DNA synthesis offers high-margin growth potential through customized therapeutic applications.

| Key Insights | Details |

|---|---|

| DNA Synthesis Market Size (2026E) | US$ 3.7 billion |

| Market Value Forecast (2033F) | US$ 8.3 billion |

| Projected Growth CAGR (2026 - 2033) | 12.3% |

| Historical Market Growth (2020 - 2025) | 7.2% |

Market Dynamics

CRISPR Therapeutic Translation: Establishing Structural Demand Through Clinical Approvals and Expanding Treatment Pipeline

CRISPR therapeutic translation is emerging as a powerful structural driver for the DNA synthesis market as genome-editing technologies move from experimental research into regulated clinical use. Recent clinical approvals and late-stage pipeline candidates have validated CRISPR as a viable therapeutic modality, thereby accelerating investment across the biopharmaceutical and academic ecosystems. Each stage of CRISPR development, from guide RNA design and donor template construction to validation and scale-up, relies heavily on high-precision synthetic DNA and oligonucleotides. As pipelines expand to address genetic disorders, oncology, and rare diseases, demand is shifting toward longer, more complex, and highly customized DNA constructs. Additionally, the need for rapid iteration, quality control, and regulatory-grade synthesis is reinforcing reliance on specialized DNA synthesis providers. This transition from research-only use to commercial therapeutics is creating sustained, long-term demand growth for the DNA synthesis market.

Restraints - Manufacturing Complexity and Quality Control Requirements Constraining Scale-Up Velocity in Therapeutic-Grade Applications

The DNA Synthesis Market faces significant manufacturing scale-up barriers that constrain therapeutic-grade production expansion despite strong demand signals. Phosphoramidite chemistry's coupling efficiency declines with increasing sequence length, creating cost and yield penalties for longer custom sequences required by emerging therapeutic applications, with synthesis cost scaling nonlinearly with target sequence complexity. GMP (Good Manufacturing Practice) certification requirements for therapeutic applications mandate pharmaceutical-grade manufacturing infrastructure, HPLC/UPLC quality control automation, and LC-MS analytical capabilities, imposing capex requirements exceeding $10-50 million, constraining smaller competitors and creating industry consolidation pressure. Quality consistency challenges, including off-target synthesis, sequence-fidelity variability, and batch-to-batch inconsistency, require sophisticated analytical validation and statistical process control, thereby increasing operational complexity and cost relative to research-grade applications. Intellectual property fragmentation across phosphoramidite chemistry patents, proprietary enzymatic-synthesis platforms, and delivery-system innovations creates licensing and royalty complexity, constraining the adoption of novel technologies by risk-averse manufacturers who prioritize established chemistry platforms despite their cost disadvantages.

Supply Chain Concentration and Geopolitical Trade Tensions Constraining Global Manufacturing Diversification

The DNA Synthesis Market faces persistent supply chain vulnerabilities due to the geographic concentration of specialized reagent suppliers, synthesizer manufacturers, and contract manufacturing organizations, with critical dependencies on China-based phosphoramidite suppliers and U.S.-based synthesizer manufacturers. Trade tensions, including U.S. export restrictions on advanced synthesizer technologies and Chinese intellectual property concerns, create regulatory uncertainty, constraining manufacturing facility expansion and technology transfer between regions. Dependence on rare-earth materials and specialized chemical supply-chain bottlenecks limit the scaling of production velocity, with reagent availability constraints periodically restricting manufacturing throughput. Regulatory harmonization gaps across jurisdictional frameworks (FDA, EMA, CFDA quality standards) create operational complexity and duplicate testing requirements for manufacturers seeking multi-regional certifications, thereby increasing operational costs and constraining smaller competitors unable to finance parallel regulatory approvals.

Opportunities - Personalized Medicine and Variant-Specific DNA Synthesis Enabling Premium Service Models and Direct-to-Patient Therapeutic Customization

Personalized medicine represents the highest-growth opportunity within the DNA Synthesis Market, with custom DNA synthesis enabling genetic variant-specific therapeutic development tailored to individual patient genomic architecture. Clinical-grade NGS (Next-Generation Sequencing) integration with synthetic biology platforms enabling precision medicine workflows where patient genomic data directly drives customized therapeutic design establishes premium service category supporting 50-100% pricing premiums relative to commodity DNA synthesis offerings.

CRISPR therapeutic personalization, in which patient-specific guide RNA design addresses individual genetic variants, enables scalable personalized therapy manufacturing and clinical trial expansion across rare genetic diseases (Intellia Therapeutics' CRISPR-based hATTR amyloidosis therapy Phase I trial demonstrated therapeutic efficacy), establishing a sustained demand stream. Tissue engineering and regenerative medicine applications that require custom DNA circuit design for programmable cell behavior constitute an emerging therapeutic modality with high profit-margin potential. Companion diagnostic integration, where DNA synthesis enables rapid development of genetic testing platforms for treatment selection and patient stratification, creates bundled service opportunities that capture value across the diagnosis, therapeutics, and monitoring continuum. Manufacturers capable of establishing end-to-end personalized medicine workflows combining genomic analysis, custom DNA synthesis, therapeutic manufacturing, and clinical validation can achieve ecosystem lock-in, creating sustainable competitive differentiation through data network effects and customer switching costs.

Category-wise Analysis

Product Insights

Oligonucleotides command a dominant position, with a 27% market share in 2025, driven by widespread applications across molecular biology, diagnostics, and therapeutics. PCR primer dominance (established molecular biology standard) captures the largest oligonucleotide sub-segment, with routine use in research laboratories globally and institutional procurement cycles establishing stable revenue foundation. Phosphoramidite chemistry, remaining the industry standard for 35 years reflects proven efficiency, reliability, and scalability, with coupling efficiency exceeding 99% per nucleotide and HPLC/UPLC purification standards enabling therapeutic-grade applications. Synthetic oligonucleotides for molecular diagnostics (infectious disease testing, cancer biomarker detection) and therapeutic applications (siRNA, antisense oligonucleotides, mRNA adapters) are driving diversification across the oligonucleotide segment, with therapeutic-grade GMP manufacturing commanding premium pricing. However, the gene synthesis segment is emerging as the fastest-growing category, with a projected CAGR of 15%+ through 2032, driven by CRISPR guide RNA requirements, gene therapy manufacturing, and synthetic biology circuit design.

Gene synthesis cost trajectory advancing toward <$0.05 per base-pair target (versus current 0.10-0.30 per base-pair commercial pricing) through enzymatic platforms and array-based synthesis enables expansion into personalized medicine and large-scale therapeutic manufacturing applications where cost economics previously prohibited adoption. Ansa Biotechnologies capability milestone, achieving 50-kilobase custom genes (May 2025) demonstrates the emerging technological superiority of enzymatic platforms over traditional phosphoramidite chemistry for complex, long-sequence applications.

End-User Insights

Biopharmaceutical companies maintain dominant end-user positioning, commanding the largest aggregate spending through R&D pipeline requirements for drug discovery, target validation, and gene therapy manufacturing. Integrated pharmaceutical manufacturers (Thermo Fisher integrated model; Roche in-house synthesis) are implementing vertical integration strategies to secure supply chain resilience while expanding internal margins. Academic and research institutes maintain a significant share by expanding genomics research investment, with government funding agencies (NIH, NSF, CEPI) supporting large-scale research programs that require specialized DNA synthesis services. Clinical laboratories are becoming a nascent end-user segment through companion diagnostic development and the integration of personalized medicine into clinical workflows, creating a growing revenue opportunity as genetic testing adoption expands across healthcare systems.

Regional Insights

North America DNA Synthesis Market Trends

North America continues to lead the DNA synthesis market, driven by strong biopharmaceutical innovation, advanced research infrastructure, and high funding intensity across genomics and synthetic biology. The region benefits from early adoption of next-generation sequencing, gene editing, and cell and gene therapy technologies, which rely heavily on high-quality synthetic DNA. Robust academic industry collaboration and the presence of contract research and manufacturing ecosystems support rapid translation from discovery to commercialization. Additionally, favorable regulatory clarity for advanced therapies and sustained public and private investment in life sciences research reinforce market leadership. Rising demand for custom gene synthesis, DNA libraries, and precision oligonucleotides across therapeutic development, diagnostics, and vaccine research continues to strengthen North America’s dominant position in the global DNA synthesis market.

Asia Pacific DNA Synthesis Market Trends

Asia Pacific is emerging as a high-growth region in the DNA synthesis market, supported by expanding biotechnology capabilities, increasing R&D investment, and rapid adoption of synthetic biology applications. Countries across the region are strengthening genomics research, precision medicine programs, and vaccine development efforts, driving rising demand for custom DNA constructs and oligonucleotides. Cost-efficient manufacturing, the growing availability of skilled scientific talent, and improved laboratory infrastructure are enabling regional players to scale their synthesis capacity competitively. In parallel, government-led initiatives that promote biotechnology innovation, academic research funding, and domestic biopharmaceutical production are accelerating market expansion. The increasing presence of contract research organizations and startup ecosystems focused on gene editing, diagnostics, and agricultural biotechnology further supports demand. As clinical research activity and therapeutic pipelines expand, the Asia Pacific is positioned to transition from a cost-advantaged supplier base into a strategically important growth market for DNA synthesis.

Competitive Landscape

The DNA synthesis market is highly competitive, characterized by rapid technological innovation and specialization. Companies compete on accuracy, throughput, turnaround times, and the ability to deliver complex, high-fidelity constructs. Strategic initiatives such as partnerships, licensing agreements, and capacity expansions are common to enhance service portfolios and geographic reach. Competitive differentiation increasingly hinges on automation, error-reduction technologies, and regulatory compliance for therapeutic applications.

Key Developments:

- In October 2025, Ribbon Bio and Scala Biodesign, two emerging biotechnology companies, collaborated to focus on improving the delivery of enzymes that enable more advanced DNA synthesis. The companies combined their expertise in DNA synthesis and enzyme design to demonstrate how enhanced molecular tools could accelerate progress across the life sciences and extend the reach of their industry-leading technologies to a broader global customer base.

Companies Covered in DNA Synthesis Market

- Brooks Automation, Inc. (GENEWIZ)

- Boster Biological Technology

- ProteoGenix

- Biomatik

- ProMab Biotechnologies, Inc

- Thermo Fisher Scientific, Inc

- Integrated DNA Technologies, Inc

- OriGene Technologies, Inc

Frequently Asked Questions

The global DNA Synthesis Market is projected to achieve valuation of US$ 3.7 billion in 2026.

Rapid advances in genomics, synthetic biology, and systems biology are increasing demand for custom oligonucleotides, genes, and DNA libraries for research and commercial applications.

North America maintains global market leadership with 34% regional share in 2025.

The most significant growth opportunity in the DNA Synthesis Market lies in personalized medicine and advanced therapeutic DNA synthesis, driven by the shift toward patient-specific and precision treatments.

The DNA Synthesis Market is dominated by Thermo Fisher Scientific, Integrated DNA Technologies (GENEWIZ via Brooks Automation), and specialized service providers including Aragen, ProteoGenix, and Biomatik, collectively controlling majority market share.