- Inks, Coatings, Adhesives & Sealants (ICAS)

- Dispersant Polymer Market

Dispersant Polymer Market Size, Share, and Growth Forecast 2026 - 2033

Dispersant Polymer Market by Product Type (Acrylic-based, Polyurethane-based, Polycarboxylates, Epoxy-based, Polyester-based, Others), Application (Paints & Coatings, Oil & Gas, Adhesives & Sealants, Cement Construction, Agricultural Products, Detergents, Others), Form (Liquid, Powder, Granules), End-use Industry (Automotive, Construction, Oil & Gas, Agriculture, Household & Personal Care, Other), and Regional Analysis for 2026 - 2033

Dispersant Polymer Market Size and Trend Analysis

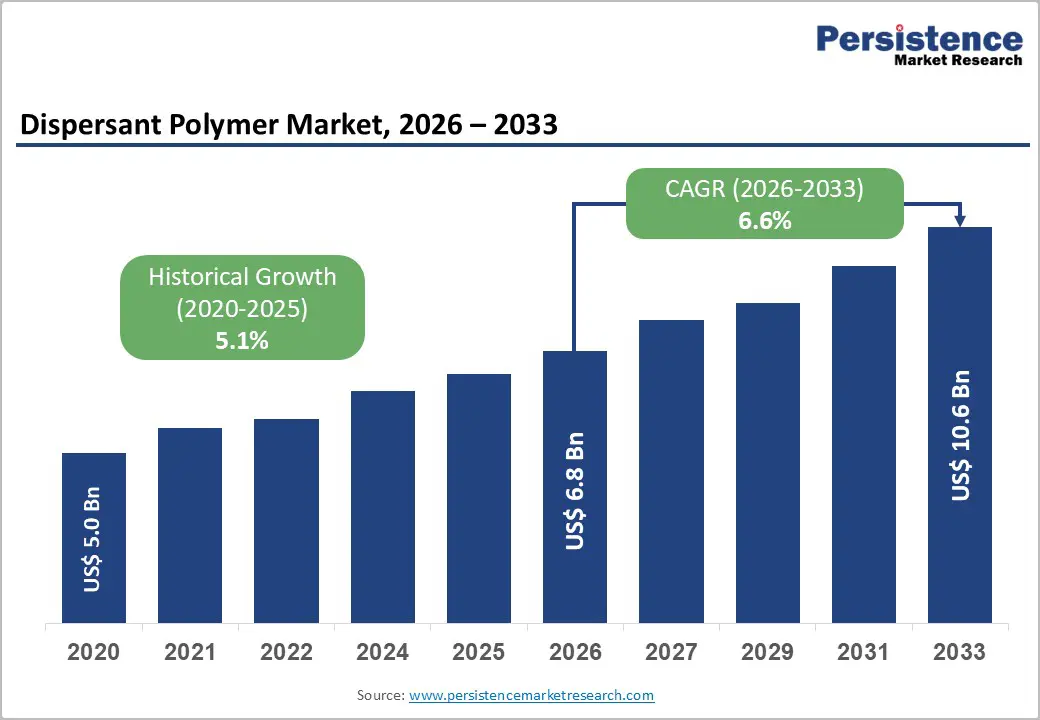

The global dispersant polymer market is supposed to be valued at US$ 6.8 billion in 2026 and is projected to reach US$ 10.6 billion by 2033, growing at a CAGR of 6.6% between 2026 and 2033.

The growth is principally driven by surging demand across paints & coatings, construction, and oil & gas sectors, where dispersant polymers serve as indispensable additives for pigment stabilization, viscosity management, and formulation performance optimization. Environmental mandates, particularly VOC emission regulations enforced by the U.S. Environmental Protection Agency (EPA) and the European Union's Industrial Emissions Directive, are compelling coatings manufacturers to reformulate products using high-performance polymeric dispersants. Simultaneously, rapid urbanization in the Asia Pacific and the rise in upstream oil and gas investment are reinforcing multi-sector demand throughout the forecast period.

Key Industry Highlights:

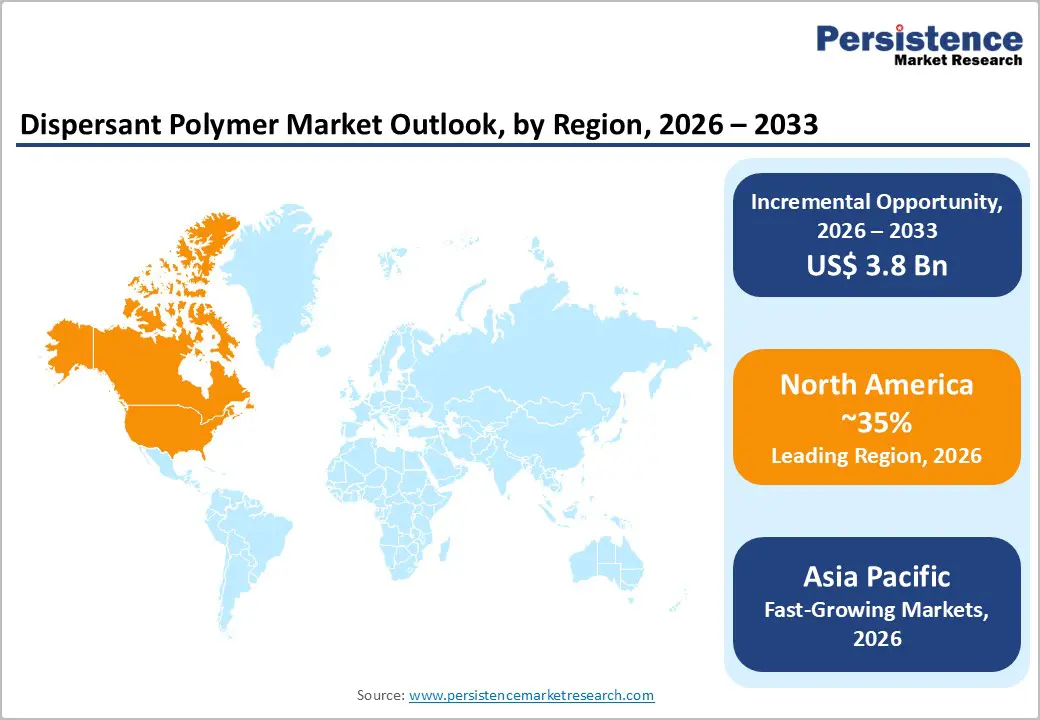

- Leading Region: North America leads the global dispersant polymer market, with 35% market share, supported by the extensive U.S. paints & coatings and oil & gas industries, a robust EPA-driven regulatory environment, and a mature innovation ecosystem supporting advanced waterborne formulation development.

- Fastest Growing Region: Asia Pacific is the fastest-growing regional market, propelled by rapid urbanization, large-scale infrastructure construction in China and India, expanding manufacturing capacity, and growing agricultural and personal care sectors, driving dispersant polymer demand.

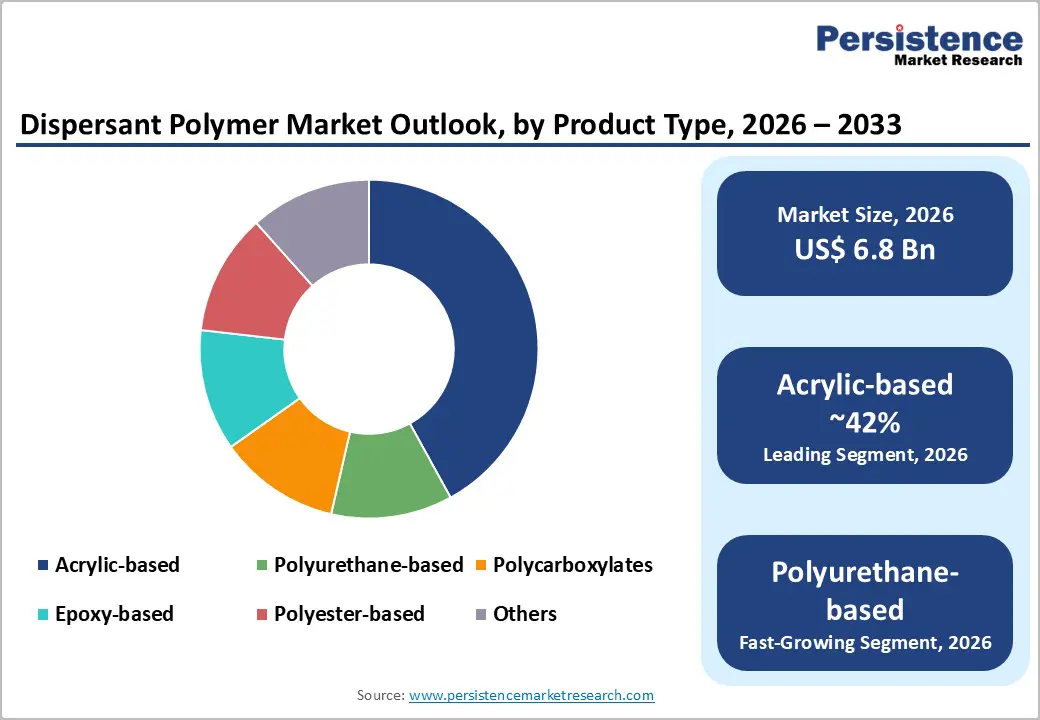

- Dominant Segment: Acrylic-based dispersant polymers dominate the product type category with approximately 42% revenue share, favored for superior UV stability, chemical resistance, and broad compatibility with pigment systems used in paints, coatings, and construction formulations.

- Fastest Growing Segment: Polyurethane-based dispersant polymers represent the fastest-growing product type, with a projected CAGR of approximately 5.8%, driven by demand for high-performance, eco-friendly waterborne coatings in automotive, aerospace, and industrial protection applications.

- Key Opportunity: The expanding adoption of bio-based and renewable dispersant polymers, driven by the European Green Deal, the U.S. BioPreferred Program, and circular-economy mandates, presents significant growth opportunities for companies investing in sustainable dispersant chemistry platforms.

| Key Insights | Details |

|---|---|

|

Dispersant Polymer Market Size (2026E) |

US$ 6.8 Bn |

|

Market Value Forecast (2033F) |

US$ 10.6 Bn |

|

Projected Growth CAGR (2026–2033) |

6.6% |

|

Historical Market Growth (2020–2025) |

5.1% |

Market Dynamics

Drivers - Surge in Waterborne Paints & Coatings Demand

The transition from solvent-based to waterborne paints and coatings has emerged as one of the most powerful structural catalysts for dispersant polymer consumption. Regulatory agencies worldwide, including the U.S. EPA and the European Chemicals Agency (ECHA), have imposed stringent VOC emission limits on solvent-based coatings, compelling manufacturers to reformulate products with high-performance polymeric dispersants. According to the American Coatings Association (ACA), the U.S. coatings industry generates approximately US$ 33 billion in annual shipments, with waterborne formulations now accounting for over 60% of the total architectural coatings segment.

Dispersant polymers, especially acrylic- and polycarboxylate-based variants, are critical in preventing pigment agglomeration, improving color development, and ensuring long-term coating stability. The ongoing residential and commercial construction boom, particularly across the Asia Pacific and North America, is expected to further reinforce demand for advanced dispersant polymers in waterborne surface treatment applications.

Expanding Global Oil & Gas Exploration and Production Activities

Growing global energy demand continues to drive upstream oil and gas exploration, creating robust demand for dispersant polymers used in drilling fluids, cementing slurries, and enhanced oil recovery (EOR) operations. Polycarboxylate and sulfonated copolymer dispersants play an indispensable role in stabilizing clay particles in drilling muds, improving fluid rheology, and preventing formation damage at elevated temperatures and pressures.

According to the International Energy Agency (IEA), global upstream oil and gas capital expenditure is expected to exceed US$ 600 billion in 2025, reflecting intensified drilling activity, particularly in the Middle East, North America, and offshore deepwater basins. The increasing complexity of well completions and the shift toward unconventional reserves, including tight oil and shale gas, further amplify the technical performance requirements placed on dispersant polymer additives used in well stimulation fluids, underpinning sustained market demand.

Restraints - Volatility in Raw Material Prices

Dispersant polymers are predominantly synthesized from acrylic acid, methacrylic acid, and other petrochemical derivatives, making production costs highly sensitive to crude oil price fluctuations. According to the U.S. Energy Information Administration (EIA), crude oil prices fluctuated by approximately 40% during 2023–2024, directly affecting feedstock costs for polymer manufacturers. Such price instability compresses profit margins across the value chain, creates budgetary uncertainty for formulators, and incentivizes substitution with lower-cost alternatives. Small and medium-sized dispersant polymer producers are disproportionately affected, as limited hedging capacity and reduced purchasing power relative to large chemical conglomerates further erode competitive positioning and financial resilience.

Environmental and Regulatory Compliance Complexity

While environmental regulations stimulate demand for low-VOC formulations, they simultaneously impose substantial compliance burdens on dispersant polymer producers. The European Union's REACH (Registration, Evaluation, Authorization, and Restriction of Chemicals) regulation requires extensive toxicological and ecotoxicological data submissions for chemical substances, increasing time-to-market and R&D costs for new polymer grades.

According to the European Chemicals Agency (ECHA), over 22,000 substances are currently registered under REACH, and manufacturers introducing novel dispersant chemistries must navigate lengthy authorization procedures. These regulatory barriers disproportionately constrain innovation from smaller producers and may slow the market's broader transition toward bio-based and sustainably sourced dispersant polymer formulations.

Opportunities - Bio-based and Sustainable Dispersant Polymers

Accelerating the global transition toward sustainable chemistry presents a transformative growth opportunity for dispersant polymer manufacturers. Bio-based dispersants, derived from renewable feedstocks such as succinic acid, citric acid, and plant-based polyols, are gaining significant market traction as manufacturers seek to reduce lifecycle carbon footprints and align with circular economy mandates. The European Green Deal, which targets a 55% reduction in net greenhouse gas emissions by 2030, and the U.S. Department of Energy's BioPreferred Program, which mandates bio-based product procurement across federal agencies, are creating structured policy pull for renewable polymer dispersants.

Leading industry players, including Clariant AG and Croda International, have already introduced commercially viable bio-based dispersant grades for construction and personal care applications. According to the European Bioplastics Association, the global bio-based chemicals market is projected to grow at approximately 10% annually through 2030, providing a substantial addressable opportunity for dispersant polymer innovators with sustainable product portfolios.

Growth in Advanced Construction Materials and Green Building Applications

The global push toward high-performance, sustainable construction materials, including ultra-high-performance concrete (UHPC), self-compacting concrete (SCC), and low-carbon cement formulations, is generating substantial incremental demand for polycarboxylate-ether (PCE) dispersant polymers used as superplasticizer admixtures. According to the Global Cement and Concrete Association (GCCA), the global construction industry is targeted to halve its CO2 emissions by 2050, driving significant investment in advanced cement chemistry and concrete admixtures.

The U.S. Infrastructure Investment and Jobs Act (2021), which allocated US$ 1.2 trillion toward infrastructure development, and China's 14th Five-Year Plan for urban development are among the landmark policy frameworks supporting construction-grade dispersant polymer demand. These macro drivers position the construction segment as one of the most strategically attractive growth avenues for dispersant polymer manufacturers through 2033.

Category-wise Analysis

Product Type Insights

The acrylic-based segment holds the dominant position in the global dispersant polymer market, accounting for approximately 42% of total revenue. Acrylic-based dispersants, including homo- and co-polymers of acrylic acid and methacrylic acid, are widely preferred across paints, coatings, and construction applications due to their exceptional chemical stability, weather resistance, UV durability, and broad compatibility with inorganic pigment systems. According to the American Chemistry Council, acrylic polymers rank among the most versatile performance additives in waterborne formulation chemistry. Their ability to provide both steric and electrostatic stabilization mechanisms simultaneously makes them particularly effective in high-shear manufacturing environments.

Moreover, acrylic-based dispersants are compatible with a wide spectrum of substrates and offer excellent shelf-life stability, a critical requirement for industrial coating formulations that undergo extended storage. These multi-functional attributes consistently differentiate acrylic-based products from competing polyurethane and epoxy alternatives in the marketplace.

Application Insights

Within the application landscape, the paints & coatings segment leads, accounting for approximately 48% of total dispersant polymer demand. This dominance reflects the segment's sheer industrial scale and the critical functional role dispersants play in modern coating formulations, preventing pigment flocculation, achieving optimal particle size distribution, and maintaining viscosity stability across the manufacturing and application lifecycle.

According to the European Council of the Paint, Printing Ink and Artists' Colours Industry (CEPE), the European coatings industry alone produces over 7 million tonnes of paint and coatings annually, representing a consistently high-volume sink for dispersant additives. The ongoing transition to waterborne architectural and industrial coatings, driven by VOC regulations in the U.S., EU, and China, is further expanding per-tonne dispersant loading rates in formulated products, effectively multiplying demand growth beyond volumetric production increases alone.

Form Insights

The liquid form segment leads the dispersant polymer market, accounting for approximately 58% of global revenue. Liquid dispersants offer decisive formulation advantages: they integrate readily into aqueous or solvent-based systems without the pre-dispersion steps required for powder or granule grades, enabling simpler manufacturing workflows and more precise dosing. For applications in paints, coatings, and cement construction, where rapid incorporation and uniform distribution are critical quality parameters, liquid dispersant polymers represent the preferred commercial form.

According to industry practice standards published by the Society for Coatings Technology (SCT), liquid additives consistently outperform solid-form alternatives in processing efficiency benchmarks. Furthermore, the growing adoption of inline-dosing automated production systems in large-scale coatings and detergent manufacturing further favors liquid forms due to their pumpability and compatibility with continuous-flow industrial processes.

Industry Insights

The construction industry represents the leading end-use segment for dispersant polymers, accounting for an estimated 32% of total market demand. This is driven primarily by the extensive use of polycarboxylate-ether (PCE) superplasticizers and dispersant admixtures in ready-mix concrete, precast concrete elements, and self-compacting concrete applications. According to the United Nations Environment Programme (UNEP), the construction sector accounts for approximately 37% of global CO2 emissions, creating strong regulatory and economic imperatives to optimize material efficiency, directly stimulating the adoption of high-performance concrete dispersants that reduce water-to-cement ratios and improve structural durability.

Rapid urbanization in the Asia Pacific, major infrastructure investment in the United States under the Infrastructure Investment and Jobs Act, and ongoing large-scale housing programs in India and Southeast Asia collectively sustain high baseline demand for construction-grade dispersant polymers across the forecast period.

Regional Insights

North America Dispersant Polymer Market Trends

North America remains one of the most established and influential regional markets for dispersant polymers, supported by a substantial industrial base spanning paints and coatings, oil and gas, and adhesives and sealants. The United States represents the core of regional consumption, guided by a comprehensive regulatory framework administered by the U.S. Environmental Protection Agency, including NESHAP and the Architectural Coatings Rule, which has accelerated the adoption of waterborne, low-VOC formulations and, in turn, increased demand for advanced dispersant polymers.

Furthermore, the region benefits from a mature innovation ecosystem led by major global chemical manufacturers. Although geopolitical tensions in the Middle East have disrupted crude oil supply chains, the expansion of domestic shale gas production and refining capacity has helped stabilize feedstock availability and maintain market resilience.

Europe Dispersant Polymer Market Trends

Europe represents a highly strategic market for dispersant polymers, distinguished by stringent regulatory governance, advanced sustainability requirements, and a mature industrial customer base. Key economies, including Germany, France, the United Kingdom, and Spain, form the core of regional demand, supported by steady consumption from the European coatings sector. Regulatory frameworks such as the EU’s REACH legislation and the European Green Deal continue to influence formulation practices, encouraging the development of low-toxicity and bio-based dispersant grades to maintain compliance and competitiveness.

Although geopolitical tensions have contributed to elevated energy costs and increased production pressures, manufacturers are accelerating investments in renewable-energy-based facilities and circular chemistry R&D. Additionally, the UK’s post-Brexit regulatory divergence under UK REACH introduces new compliance obligations while enabling differentiated market positioning.

Asia Pacific Dispersant Polymer Market Trends

Asia Pacific is the fastest-growing market for dispersant polymers, driven by rapid industrialization, extensive infrastructure development, and a continuously expanding manufacturing ecosystem. China remains the dominant contributor, driven by significant construction activity, rising automotive production, and a robust domestic paints and coatings sector. Under the 14th Five-Year Plan, the NDRC’s emphasis on advanced material self-sufficiency, including specialty polymer additives, continues to strengthen domestic capabilities.

India and ASEAN economies are emerging as major high-growth markets, enabled by government-led construction initiatives, expanding agricultural chemical formulation, and increasing demand for personal care products. Japan retains an important position as a technology-driven producer, particularly in polycarboxylate chemistry and high-purity dispersants. Regional geopolitical tensions, which intermittently influence energy prices and shipping routes, intermittently elevate feedstock cost pressures across South and Southeast Asia.

Competitive Landscape

The global dispersant polymer market exhibits a moderately consolidated competitive structure, with the top six to eight players, including BASF SE, Dow Inc., Evonik Industries AG, Lubrizol Corporation, Ashland Inc., and Clariant AG, collectively accounting for an estimated 55–65% of total global revenues. These market leaders pursue aggressive portfolio expansion and innovation strategies, investing in bio-based polymer R&D, sustainable production technologies, and application-specific dispersant formulations. Strategic acquisitions, licensing agreements, and geographic capacity expansions are central to sustaining competitive differentiation. Simultaneously, the market features a fragmented tail of regional specialty chemical producers in Asia Pacific offering niche dispersant grades at competitive price points, intensifying competition in commodity formulation segments.

Key Developments:

- March 2026: BASF SE has expanded production capacity for dispersions at its site in Durban, South Africa, strengthening the company’s ability to supply customers with high-quality dispersions used in architectural coatings, construction materials, and the paper industry.

- May 2025: Evonik Coating Additives introduced a range of four new AERODISP® dispersions based on SiO2 or Al2O3 particles, designed to improve waterborne inkjet ink receptive coatings. With the new range of waterborne AERODISP® dispersions, Evonik Coating Additives has developed products to ensure high dot sharpness and fixation of ink droplets on ink-receptive coatings, also known as inkjet primers.

- November 2025: BASF officially commissioned its high-performance dispersant production line at the Jiangbei New Material Technology Park, Nanjing, China. This investment enables local production of the most advanced dispersants using Controlled Free Radical Polymerization (CFRP) technology.

Top Companies in the Dispersant Polymer Market

BASF SE (Ludwigshafen, Germany) is the world's largest chemical company by revenue and a leading global supplier of dispersant polymers under its Dispex and Sokalan product families. The company's extensive R&D infrastructure and global manufacturing footprint across Europe, the Americas, and the Asia Pacific enable it to serve diverse end-use markets spanning coatings, construction, personal care, and detergents with highly tailored dispersant solutions, supported by deep application engineering capabilities and robust technical service networks.

Dow Inc. (Midland, Michigan, U.S.) holds a prominent position in the dispersant polymer landscape through its acrylic polymer technologies and Acusol dispersant brand. With growing investments in biodegradable polymer platforms and sustainable formulation chemistry, Dow is strategically aligned with regulatory trends promoting bio-based and environmentally responsible dispersant solutions, particularly in home care, water treatment, and industrial coatings applications, where performance and sustainability must be simultaneously optimized.

Evonik Industries AG (Essen, Germany) is a global specialty chemicals leader whose TEGO Dispers product range enjoys strong market acceptance across inkjet inks, waterborne industrial coatings, and plastics applications. The company's focus on high-performance specialty dispersants, backed by deep application engineering expertise and a robust global distribution network, enables it to command premium pricing and build strong customer retention in technically demanding formulation segments across the Americas, Europe, and Asia Pacific.

Companies Covered in Dispersant Polymer Market

- BASF SE

- Dow Inc.

- Evonik Industries AG

- Lubrizol Corporation

- Ashland Inc.

- Clariant AG

- Arkema Group

- Solvay S.A.

- Nouryon

- Covestro AG

- Nippon Shokubai Co. Ltd.

- Elementis PLC

Frequently Asked Questions

The global dispersant polymer market is valued at approximately US$ 6.8 Bn in 2026 and is projected to reach US$ 10.6 Bn by 2033, registering a CAGR of 6.6% during the forecast period of 2026–2033. The market was valued at US$ 5.0 Bn in 2020, reflecting a historical CAGR of 5.1% between 2020 and 2025.

Primary growth drivers include the rapid expansion of waterborne paints & coatings compelled by VOC emission regulations from the U.S. EPA and the EU's Industrial Emissions Directive, escalating global upstream oil and gas capital expenditure projected to exceed US$ 600 billion in 2025 per the IEA, and surging construction activity across the Asia Pacific and North America driving demand for polycarboxylate-ether (PCE) superplasticizer admixtures.

Acrylic-based dispersant polymers hold the leading position, accounting for approximately 42% of global market revenue. Their dominance is attributed to superior weather resistance, chemical stability, UV durability, and broad compatibility with inorganic pigment systems across coatings and construction applications, as well as high processability in waterborne formulation manufacturing environments.

North America currently represents one of the largest and most established regional markets, driven by the extensive U.S. paints & coatings and oil & gas industries, supported by robust EPA regulatory frameworks. However, Asia Pacific is the fastest-growing region, led by China, India, and ASEAN nations, underpinned by rapid urbanization, infrastructure investment, and expanding manufacturing sectors.

The transition toward bio-based and sustainably sourced dispersant polymers, supported by the European Green Deal's 2030 emission targets and the U.S. BioPreferred Program, represents a high-growth opportunity, alongside surging demand for PCE admixtures in advanced concrete formulations under global infrastructure investment programs such as the U.S. Infrastructure Investment and Jobs Act and China's 14th Five-Year Plan.

Key participants include BASF SE, Dow Inc., Evonik Industries AG, Lubrizol Corporation, Ashland Inc., Clariant AG, Arkema Group, Solvay S.A., Nouryon, Covestro AG, Nippon Shokubai Co. Ltd., and Elementis PLC. These companies compete on product innovation, application engineering expertise, sustainability credentials, and geographic manufacturing reach to serve diverse global end-user industries.