- Non-food Packaging

- Direct Thermal Labels Market

Direct Thermal Labels Market Size, Share, and Growth Forecast, 2026 - 2033

Direct Thermal Labels Market By Facestock Material (Paper, Linerless, Others), Form Factor (Rolls, Linerless Reels, Others), End-use Industry, and Regional Analysis for 2026 - 2033

Direct Thermal Labels Market Size and Trends Analysis

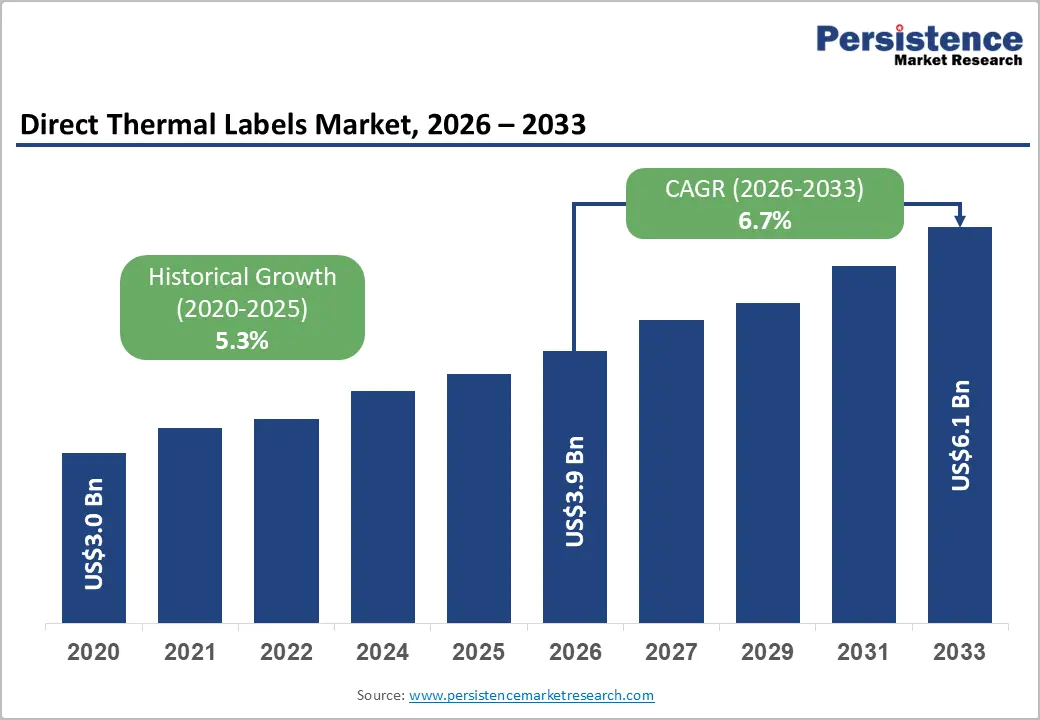

The global direct thermal labels market size is likely to be valued at US$ 3.9 billion in 2026 and is expected to reach US$ 6.1 billion by 2033, growing at a CAGR of 6.7% between 2026 and 2033, driven by rising parcel volumes, faster retail fulfillment cycles, stricter traceability requirements, and increasing adoption of phenol-free and linerless label formats.

Paper facestock and roll-based formats continue to dominate due to cost efficiency and compatibility with existing printing infrastructure, while North America leads in market share and Asia Pacific emerges as the fastest-growing region. Growth is supported by the inherent cost advantage of direct thermal printing over ribbon-based alternatives, particularly in high-throughput environments such as logistics, retail checkout, and short-life labeling applications. Expanding e-commerce activity, regulatory compliance requirements in food and pharmaceuticals, and sustainability-driven material innovation are collectively reinforcing long-term demand.

Key Industry Highlights:

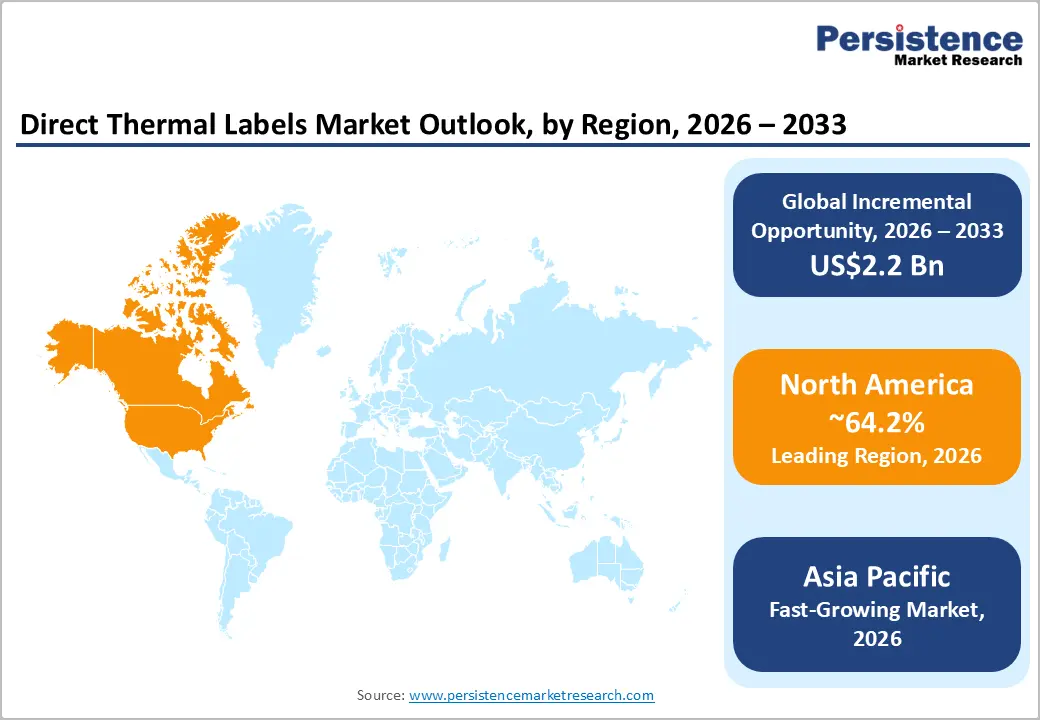

- Leading Region: North America is projected to account for 34.3% of the market share, supported by strong e-commerce penetration, advanced logistics infrastructure, and early adoption of sustainable labeling solutions.

- Fastest-growing Region: Asia Pacific is the fastest-growing region, driven by rapid expansion in e-commerce, manufacturing, and retail sectors across China, India, Japan, and Southeast Asia, with strong momentum in logistics and supply chain modernization.

- Investment Plans: Industry investments are increasingly focused on linerless labeling technologies, phenol-free materials, and healthcare-grade labeling solutions, with companies expanding production capacity and forming technology partnerships to support sustainable and compliant product development.

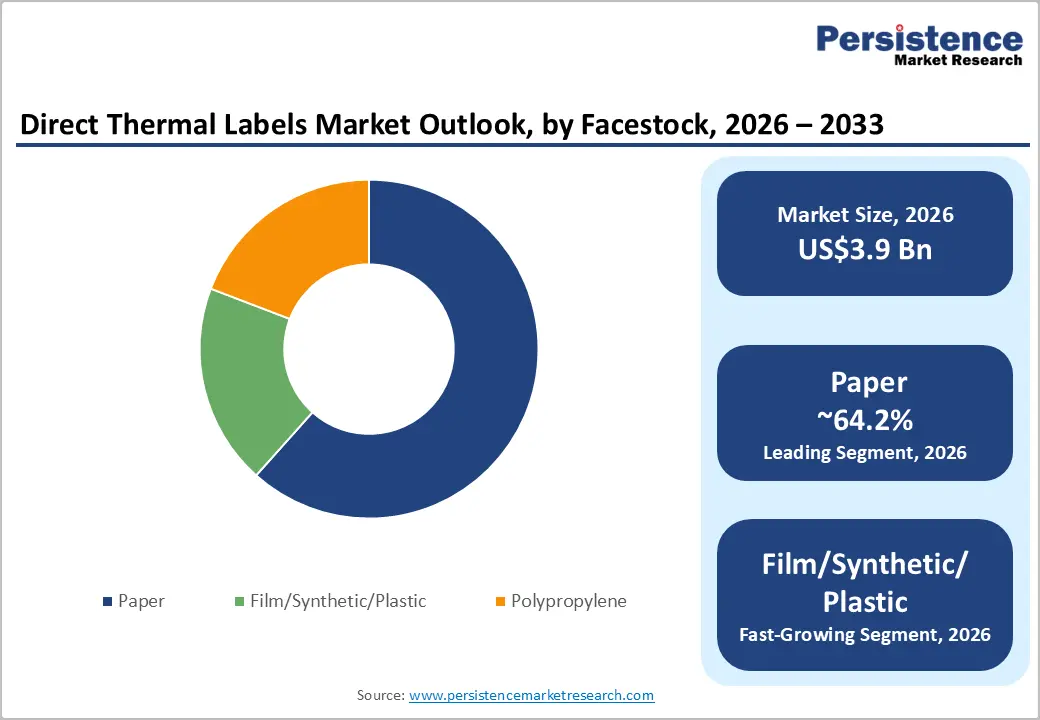

- Dominant Facestock Material: Paper facestock is anticipated to hold 64.2% of market share, due to its cost-efficiency, ease of printing, and widespread use in high-volume, short-life applications such as retail and logistics.

- Leading Form Factor: Roll-based labels are estimated to lead the form factor segment with a 73.3% market share, driven by their compatibility with most printing systems and suitability for high-speed, large-scale operations.

| Key Insights | Details |

|---|---|

| Direct Thermal Labels Market Size (2026E) | US$3.9 Bn |

| Market Value Forecast (2033F) | US$6.1 Bn |

| Projected Growth (CAGR 2026 to 2033) | 6.7% |

| Historical Market Growth (CAGR 2020 to 2025) | 5.3% |

Market Factors - Growth, Barriers, and Opportunity Analysis

Growth Analysis - Rapid Expansion of E-Commerce and Omnichannel Logistics

The continued growth of global e-commerce is a primary driver for direct thermal labels. These large-scale transaction volumes directly increase demand for shipping labels, warehouse identification tags, and return labels. Direct thermal technology is preferred in these applications due to its speed, simplicity, and lower consumable requirements, as it eliminates the need for ribbons and reduces maintenance complexity. As order volumes increase, logistics providers and retailers require fast, reliable labeling solutions that can support real-time tracking and high scanning accuracy across automated systems.

Direct thermal labels meet these requirements by enabling clear barcode printing and consistent performance in high-throughput environments. For manufacturers and converters, this translates into sustained high-volume demand across logistics networks, fulfillment centers, and last-mile delivery systems, with additional growth coming from reverse logistics and same-day delivery models that further increase label consumption.

Increasing Regulatory Requirements for Traceability and Labeling Compliance

Regulatory frameworks across food, pharmaceuticals, and logistics are driving the adoption of standardized, machine-readable labeling solutions. Global supply chains increasingly rely on barcode-based identification systems to ensure traceability, product authentication, and recall readiness. Food safety regulations require full traceability across the supply chain, while pharmaceutical regulations mandate clear labeling, serialization, and packaging integrity. These requirements are shifting demand from basic labeling solutions toward high-quality, compliant direct thermal labels capable of maintaining readability and accuracy throughout the product lifecycle.

Sustainability and Regulatory Push toward Phenol-Free and Linerless Materials

Environmental regulations and corporate sustainability initiatives are accelerating the transition toward phenol-free direct thermal labels and linerless formats. Regulatory restrictions on bisphenol-based chemicals in thermal paper, including bans implemented in certain jurisdictions from 2026, are forcing manufacturers to reformulate products. Linerless labels are gaining traction due to their ability to reduce waste, improve operational efficiency, and increase labels per roll. These trends are creating a premium segment within the market, where compliance and sustainability credentials drive purchasing decisions.

Barrier Analysis - Limited Durability and Environmental Sensitivity of Direct Thermal Prints

A key limitation of direct thermal labels is their susceptibility to environmental conditions such as heat, ultraviolet exposure, moisture, and abrasion. Over time, printed images may fade or degrade, making them unsuitable for long-term applications or harsh environments. This restricts their use in industries requiring durable labeling, such as manufacturing and outdoor asset tracking. As a result, some end users continue to prefer thermal transfer or synthetic labeling solutions, limiting the addressable market for direct thermal technologies.

Rising Material Costs and Compliance-Related Complexities

The shift toward BPA/BPS-free formulations and environmentally compliant materials introduces additional cost and complexity for manufacturers. Reformulation, certification, and testing processes can increase production costs and extend product development timelines. Linerless label formats, while beneficial, require specialized adhesives and compatible printing equipment, which can slow adoption among users with legacy systems. These factors collectively create margin pressure for label converters and may delay large-scale transitions in cost-sensitive markets.

Opportunity Analysis - Expansion of Linerless Labeling Solutions

Linerless labels represent one of the most significant growth opportunities in the market, with a projected CAGR of 6.23%. By eliminating the release liner, these labels reduce material waste, increase operational efficiency, and allow more labels per roll. This results in fewer roll changes, reduced storage requirements, and lower transportation costs. For manufacturers, linerless solutions offer a compelling value proposition that combines sustainability with cost savings. As printer compatibility improves, adoption is expected to accelerate across retail, logistics, and foodservice sectors.

Beyond operational efficiency, linerless labeling also aligns with corporate sustainability goals and regulatory pressures to reduce packaging waste. Companies are increasingly quantifying environmental benefits, such as reduced landfill contribution and lower carbon footprint per label. The integration of linerless technology with automated labeling systems and IoT-enabled printers further enhances workflow optimization, making it an attractive investment for high-volume users.

Growth in Healthcare and Pharmaceutical Labeling Applications

Healthcare and pharmaceutical sectors present strong growth opportunities due to increasing regulatory requirements and the need for precise labeling. Applications such as patient identification, specimen tracking, and pharmaceutical packaging require reliable and compliant labeling solutions. Direct thermal labels are increasingly being adapted for these use cases, particularly where short-to-medium term durability is sufficient. The higher value per label and strict qualification requirements in these sectors also provide opportunities for premium product offerings.

Moreover, the rise in global healthcare spending, expansion of diagnostic services, and growth in clinical trials are increasing the volume of labeled items across hospitals and laboratories. The need for error-free identification and real-time data capture is driving demand for high-resolution, scannable labels. This is encouraging manufacturers to develop specialized direct thermal solutions with enhanced image stability, chemical resistance, and compatibility with healthcare-grade adhesives.

Technological Advancements in High-Performance Facestock Materials

Advancements in synthetic and coated facestock materials are expanding the applicability of direct thermal labels. New materials offer improved resistance to moisture, chemicals, and temperature variations, enabling their use in more demanding environments such as cold-chain logistics and industrial applications. These innovations allow manufacturers to address traditional limitations of direct thermal technology while capturing higher-margin opportunities in specialized applications.

Ongoing research in coating chemistries and surface treatments is also improving print clarity, image longevity, and environmental resistance without compromising print speed. The development of phenol-free coatings and recyclable synthetic materials further supports sustainability objectives while maintaining performance standards. As these advanced materials become more cost-competitive, their adoption is expected to increase across sectors that previously relied on thermal transfer labeling solutions.

Segmentation Analysis

Facestock Material Insights

Paper facestock is anticipated to dominate the market, accounting for 64.2% of market share in 2026. Its widespread adoption is primarily driven by its cost-effectiveness, ease of printing, and compatibility with a broad range of direct thermal printers. Paper-based labels are particularly well-suited for high-volume, short-life applications such as shipping labels, retail price tags, and food packaging, where durability requirements are limited, and speed is critical. The extensive installed base of direct thermal printing equipment further reinforces paper’s dominance, as businesses can continue using existing infrastructure without incurring additional capital expenditure.

Paper facestock offers good print clarity for barcodes and text, making it reliable for scanning and data capture in fast-paced environments. Despite increasing sustainability scrutiny, advancements in recyclable and phenol-free paper coatings are helping maintain its strong position in the market.

Synthetic materials, including film and polypropylene, represent the fastest-growing segment within the facestock category due to their superior durability and resistance to environmental conditions. These materials are increasingly adopted in applications that require longer label life, such as cold-chain logistics, healthcare labeling, and industrial asset tracking. Growth is supported by rising demand for labels that can withstand moisture, temperature fluctuations, chemicals, and physical abrasion without compromising print quality.

In sectors such as pharmaceuticals and food distribution, where labeling accuracy and longevity are critical, synthetic facestock provides a more reliable solution compared to traditional paper. Continuous innovation in phenol-free coatings, advanced adhesives, and surface treatments is further enhancing the performance and cost-efficiency of these materials, accelerating their adoption across high-value applications.

Form Factor Insights

Roll-based labels are estimated to dominate the market with a 73.3% share in 2026, supported by their compatibility with the majority of direct thermal printing systems. Rolls enable continuous, high-speed printing, making them ideal for large-scale operations such as logistics, retail checkout, warehousing, and healthcare environments. Their design allows for seamless integration with both desktop and industrial printers, ensuring consistent performance in high-throughput settings.

Operational advantages such as ease of handling, compact storage, and reduced downtime during printing processes further strengthen their market position. Rolls also support automated labeling systems, including print-and-apply solutions used in fulfillment centers and manufacturing lines. The widespread adoption of roll formats is closely linked to the large installed base of compatible printers, which continues to drive steady demand.

Linerless reels are expected to be the fastest-growing form factor. By eliminating the release liner, these labels significantly reduce material waste and improve overall efficiency. The ability to accommodate more labels per roll results in fewer roll changes, reduced downtime, and lower storage and transportation costs, making linerless solutions highly attractive for high-volume operations. Adoption is increasing rapidly across industries such as quick-service restaurants, retail, and logistics, where operational efficiency and sustainability are the key priorities.

Linerless labels also align with corporate environmental goals by minimizing waste generation and improving resource utilization. As printer technology evolves to support linerless formats and compatibility challenges are addressed, this segment is expected to witness accelerated growth, particularly in applications requiring continuous labeling and flexible label lengths.

Regional Insights

North America Direct Thermal Labels Market Trends - E-commerce Logistics Scale & Shift to Phenol-Free Materials

North America is projected to hold the largest share of the market at 34.3% in 2026, driven by a mature e-commerce ecosystem, advanced logistics infrastructure, and well-established regulatory frameworks. The U.S. leads the region, supported by high online retail penetration and extensive fulfillment networks operated by major players such as Amazon, Walmart, and FedEx. The scale and sophistication of these logistics systems require high volumes of reliable, cost-efficient labeling solutions, reinforcing the dominance of direct thermal labels in shipping, warehousing, and last-mile delivery operations.

Regulatory developments are playing a critical role in shaping market dynamics. Restrictions on bisphenol-based thermal paper, particularly at the state level, are accelerating the transition toward phenol-free and environmentally compliant label materials. This shift is influencing procurement decisions across retail and foodservice chains, pushing suppliers to innovate in sustainable formulations. Companies such as Avery Dennison and Zebra Technologies have also expanded their portfolios of linerless and eco-friendly direct thermal solutions, supporting adoption across quick-service restaurants and retail chains. Investment opportunities are concentrated in linerless labeling, healthcare identification systems, and foodservice applications, where efficiency, compliance, and sustainability intersect to drive long-term growth.

Europe Direct Thermal Labels Market Trends - Sustainability Mandates & Traceability-Driven Label Innovation

Europe represents a significant market, characterized by strong regulatory oversight and a consistent focus on sustainability and product traceability. Countries, including Germany, the U.K., France, and Spain, are the key contributors due to their advanced retail infrastructure, cross-border logistics networks, and high levels of industrial automation. Strict regulatory frameworks governing food safety, pharmaceutical labeling, and environmental compliance are key drivers of demand for high-quality, standardized labeling solutions.

The region is also at the forefront of sustainable labeling innovation. Increasing adoption of linerless labels and recyclable materials is supported by broader European Union initiatives aimed at reducing packaging waste and improving circular economy practices. Companies such as HERMA and UPM have introduced advanced adhesive materials and linerless label technologies tailored to meet these requirements, while retailers and food producers are actively transitioning toward lower-waste labeling formats.

In addition, supermarket chains across Europe are implementing digital price labeling and integrated barcode systems, which further increase the demand for high-performance direct thermal labels. These developments are creating opportunities for manufacturers that can deliver both regulatory compliance and environmental performance.

Asia Pacific Direct Thermal Labels Market Trends - E-commerce Expansion & High-Volume Manufacturing Growth

Asia Pacific is the fastest-growing region, driven by rapid urbanization, expanding e-commerce markets, and increasing industrialization. Key markets such as China, India, Japan, and Southeast Asia are experiencing strong growth in online retail, supported by platforms like Alibaba, JD.com, and Flipkart. These platforms rely heavily on efficient logistics and high-volume label usage, particularly for shipping, sorting, and inventory management. As a result, demand for direct thermal labels is increasing significantly across fulfillment centers and distribution hubs.

The region also benefits from strong manufacturing capabilities and cost advantages, enabling large-scale production of label materials and printing solutions. Companies such as SATO Holdings, Ricoh, and Fuji Seal are actively expanding their presence in Asia Pacific by investing in advanced labeling technologies and localized production facilities. In India, the rapid growth of organized retail and food delivery platforms has increased demand for labeling in packaging and logistics, while in China, the expansion of cold-chain logistics for food and pharmaceuticals is driving adoption of more durable direct thermal solutions.

At the same time, governments across the region are gradually strengthening regulatory frameworks related to food safety and product traceability. This is encouraging the adoption of higher-quality labeling solutions and standardized barcode systems. While price sensitivity remains a challenge in certain markets, the overall trend toward modernization of supply chains and increased regulatory compliance is expected to sustain strong growth in the region.

Competitive Landscape

The global direct thermal labels market is moderately fragmented, with a mix of global and regional players competing across various segments. Leading companies maintain strong positions through product innovation, extensive distribution networks, and established customer relationships. While a few large players dominate high-volume segments, smaller companies play a critical role in niche and regional markets. Key players are focusing on sustainability, product innovation, and ecosystem integration. Strategies include developing phenol-free materials, expanding linerless solutions, and ensuring compatibility with printing hardware. Companies are increasingly offering integrated solutions that combine labels, printers, and software to enhance customer retention and operational efficiency.

Key Industry Developments:

- In April 2025, UPM Raflatac introduced product footprint data (product passport prototypes) into customer quotes, enabling converters to assess environmental impact and reduce Scope 3 emissions, thereby enhancing transparency and sustainability decision-making in label procurement.

- In September 2025, Avery Dennison Corporation announced a strategic partnership with Wiliot to expand ambient IoT-based supply chain intelligence, enhancing real-time tracking and visibility across logistics and retail environments.

Companies Covered in Direct Thermal Labels Market

- Avery Dennison Corporation

- Zebra Technologies Corporation

- CCL Industries Inc.

- UPM Raflatac

- Ricoh Company, Ltd.

- SATO Holdings Corporation

- Appvion Operations, Inc.

- HERMA GmbH

- LINTEC Corporation

- Oji Holdings Corporation

- Fuji Seal International, Inc.

- Bizerba SE & Co. KG

- Mitsubishi Paper Mills Limited

- Lecta Group

- Nippon Paper Industries Co., Ltd.

- Toshiba Tec Corporation

Frequently Asked Questions

The direct thermal labels market size is estimated to be US$3.9 billion in 2026.

The direct thermal labels market is projected to reach US$ 6.1 billion by 2033.

Key trends include the growing adoption of linerless labeling solutions, increasing demand for phenol-free and sustainable materials, expansion of e-commerce-driven logistics labeling, and rising use in healthcare and pharmaceutical traceability applications.

Paper facestock is the leading segment, accounting for 64.2% of the market share, driven by its cost efficiency and suitability for high-volume applications.

The direct thermal labels market is expected to grow at a CAGR of 6.7% from 2026 to 2033.

Major players include Avery Dennison Corporation, Zebra Technologies Corporation, CCL Industries Inc., UPM Adhesive Materials, and SATO Holdings Corporation.