- Non-food Packaging

- Die Cut Carton Market

Die Cut Carton Market Size, Share, and Growth Forecast, 2026 - 2033

Die Cut Carton Market by Wall Type (Single Wall, Double Wall, Others), Box Design (Regular Slotted Container, Window Die-Cut, Others), End-use Industry, and Regional Analysis for 2026 - 2033

Die Cut Carton Market Size and Trends Analysis

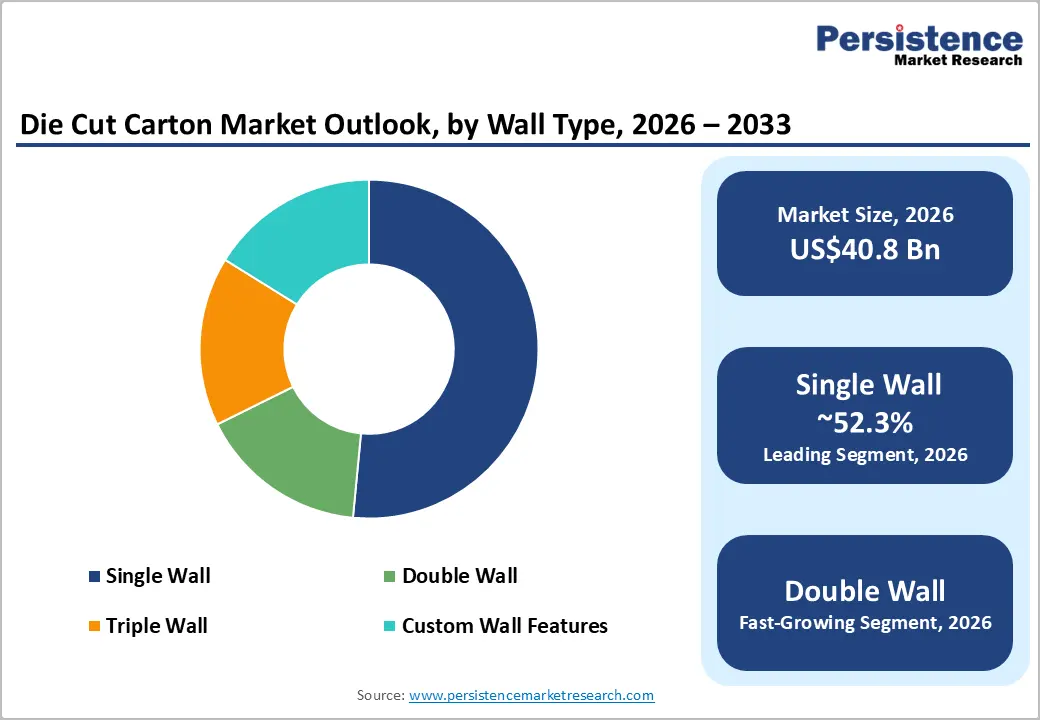

The global die cut carton market size is likely to be valued at US$40.8 billion in 2026 and is expected to reach US$56.6 billion by 2033, growing at a CAGR of 4.8% between 2026 and 2033, driven by increasing e-commerce shipments, tightening sustainability regulations, and rising demand for compliant packaging across food, beverage, and pharmaceutical sectors.

Brand owners are transitioning toward fiber-based packaging formats to improve recyclability, enhance shelf visibility, and meet evolving regulatory requirements. The market is also benefiting from the broader transition toward circular packaging systems. High recycling rates for paper-based materials and stricter sustainability mandates across major economies are reinforcing the adoption of die-cut cartons in retail-ready packaging, shipping applications, and premium secondary packaging formats.

Key Industry Highlights:

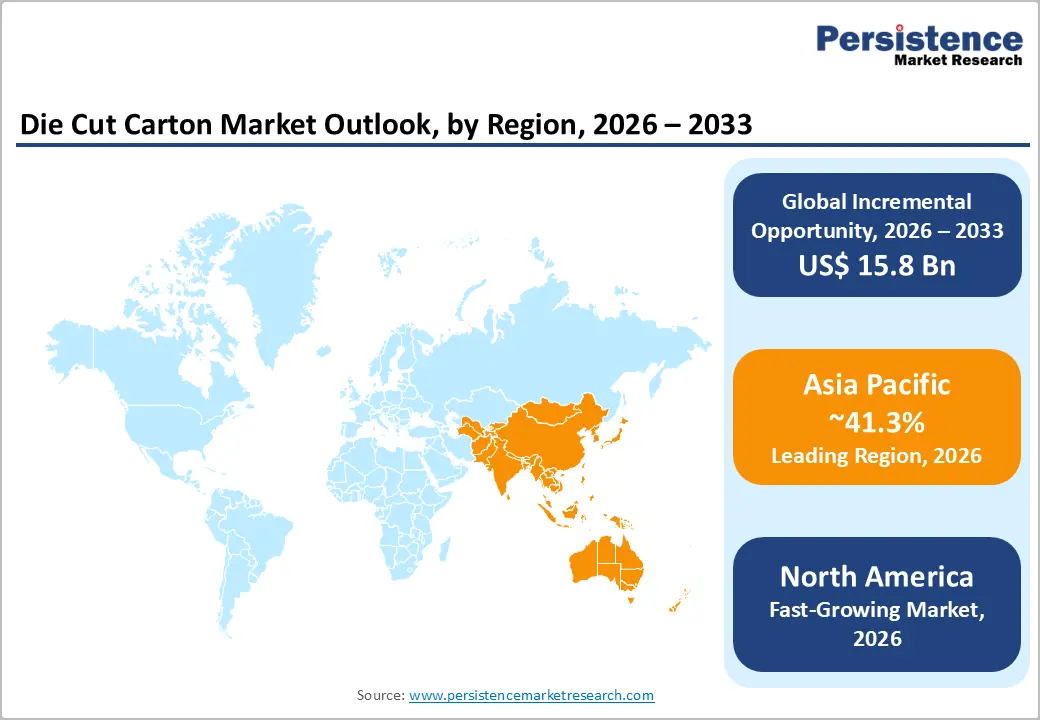

- Leading Region: Asia Pacific is projected to lead the market with an anticipated 41.3% market share, supported by large-scale manufacturing, strong e-commerce growth, and cost-efficient production ecosystems across China, India, and Southeast Asia.

- Fastest-growing Region: North America is the fastest-growing region, driven by rapid e-commerce expansion, rising demand for sustainable packaging, and advanced automation in logistics and distribution networks.

- Investment Plans: Industry investments are focused on sustainable fiber-based materials, recycling infrastructure, and automation technologies, along with capacity expansion to meet rising e-commerce demand and regulatory compliance requirements.

- Dominant Wall Type: Single-wall cartons are expected to account for 52.3% of the market, owing to their cost-effectiveness, lightweight structure, and suitability for high-volume e-commerce shipments.

- Leading Box Design: Regular slotted containers (RSC) lead with an anticipated 42% market share, supported by their standardized design, ease of manufacturing, and widespread use across multiple industries.

| Key Insights | Details |

|---|---|

| Die Cut Carton Market Size (2026E) | US$40.8 Bn |

| Market Value Forecast (2033F) | US$56.6 Bn |

| Projected Growth (CAGR 2026 to 2033) | 4.8% |

| Historical Market Growth (CAGR 2020 to 2025) | 4.4% |

DRO Analysis

Driver Analysis - Expansion of E-commerce Driving Carton Demand

The rapid growth of global e-commerce continues to significantly increase demand for die-cut cartons. Rising online retail penetration has led to higher shipment volumes, requiring packaging solutions that are lightweight, durable, and customizable. Die-cut cartons meet these requirements by offering flexibility in size, structural design, and branding capabilities. Companies are optimizing packaging to reduce void space, minimize shipping costs, and improve the customer unboxing experience. This shift is particularly evident in sectors such as electronics, apparel, and personal care, where packaging serves both protective and marketing functions. As e-commerce logistics become more sophisticated, demand for precision-engineered carton designs is expected to accelerate further.

Sustainability Regulations Favoring Fiber-Based Packaging

Environmental regulations are increasingly promoting the use of recyclable and biodegradable packaging materials. Paper-based cartons benefit from well-established recycling infrastructure and higher recovery rates than plastic alternatives. Governments across North America and Europe are implementing stricter packaging waste regulations, including mandates for recyclability, reduced material usage, and improved labeling transparency. These policies are encouraging manufacturers to shift toward die-cut cartons made from recycled or sustainably sourced paperboard. This transition is not only regulatory-driven but also supported by consumer preference for environmentally responsible packaging, strengthening long-term demand for die-cut carton solutions.

Growth in Food, Beverage, and Pharmaceutical Packaging

The food, beverage, and pharmaceutical industries are key drivers of demand for die-cut cartons, driven by stringent packaging requirements. These sectors require packaging solutions that ensure product safety, maintain quality, and comply with regulatory standards. Die-cut cartons offer advantages such as tamper-evident structures, high-quality labeling, and compatibility with automated packaging systems. In the pharmaceutical industry, serialization and anti-counterfeiting measures are increasing the need for precision packaging. In food and beverages, the shift toward sustainable and convenient packaging formats further supports carton adoption. As these industries continue to expand globally, demand for specialized die-cut carton designs is expected to grow steadily.

Restraint Analysis - Volatility in Raw Material and Energy Costs

Fluctuations in paperboard prices, energy costs, and transportation expenses present a significant challenge for manufacturers. Since paper-based materials are the primary input for die-cut cartons, any instability in supply or pricing directly impacts production costs and profit margins. Energy-intensive manufacturing processes further amplify cost sensitivity. In highly competitive markets, passing these costs on to customers can be difficult, putting pressure on suppliers' margins. This volatility creates uncertainty in pricing strategies and long-term planning for both manufacturers and end users.

Substitution from Alternative Packaging Formats

Die-cut cartons face competition from alternative packaging solutions such as flexible packaging, rigid plastics, and reusable containers. In applications requiring moisture resistance, barrier protection, or enhanced durability, alternative materials may be preferred. Regulatory compliance requirements, especially in the food and pharmaceutical sectors, can increase production complexity and costs. These factors may limit adoption in certain applications and create barriers for smaller manufacturers attempting to enter highly regulated markets.

Opportunity Analysis - Premium and Customized Packaging Solutions

There is a growing demand for visually appealing and functionally advanced packaging, particularly in retail and e-commerce. Die-cut cartons offer significant design flexibility, enabling features such as windows, custom shapes, embossing, and innovative locking mechanisms. These capabilities not only enhance product visibility but also strengthen shelf differentiation and brand recall. As consumer purchasing decisions are increasingly influenced by packaging aesthetics and sustainability claims, brands are leveraging die-cut cartons as a strategic marketing tool. This shift is encouraging manufacturers to invest in advanced converting technologies, digital printing, and rapid prototyping to deliver highly customized, short-run packaging solutions for premium segments such as cosmetics, confectionery, and specialty foods.

Expansion in Emerging Markets

Emerging economies in the Asia Pacific, Latin America, and parts of Africa are experiencing rapid growth in organized retail and e-commerce ecosystems. Urbanization, rising disposable incomes, and a growing middle-class population are accelerating the consumption of packaged goods across categories. Governments and private players are also investing in logistics infrastructure, warehousing, and domestic manufacturing capabilities, which increases demand for efficient packaging solutions. Localized production of die-cut cartons reduces lead times and transportation costs, making it an attractive option for regional brands. This environment creates strong opportunities for both multinational and local manufacturers to expand capacity, form strategic partnerships, and tailor product offerings to regional preferences and regulatory requirements.

Rising Demand in Pharmaceutical Packaging

The pharmaceutical sector offers a high-value growth opportunity, driven by its strict regulatory framework and the increasing emphasis on patient safety and product integrity. Die-cut cartons are widely used for secondary packaging of medicines, as they provide sufficient space for detailed labeling, dosage instructions, and regulatory information. The growing adoption of serialization, track-and-trace systems, and anti-counterfeiting technologies is further increasing the need for precision-engineered carton designs with tamper-evident features. In addition, the expansion of global pharmaceutical supply chains and the rise of biologics and specialty drugs are driving demand for packaging that ensures protection during storage and transit. Manufacturers that can deliver compliance-ready, high-quality, and scalable solutions are well-positioned to secure long-term contracts in this segment.

Category-wise Analysis

Wall Type Insights

Single-wall dominates the market with an anticipated 52.3% share in 2026, due to its optimal balance between cost, strength, and material efficiency. These cartons consist of one layer of fluting sandwiched between two linerboards, providing sufficient durability for most consumer goods while maintaining a lightweight structure. Their widespread adoption is strongly linked to the growth of e-commerce and organized retail, where high-volume, low-cost packaging solutions are essential.

For example, major e-commerce players such as Amazon and Flipkart extensively use single-wall cartons for shipping electronics, apparel, and household goods. Their compatibility with automated packing lines and reduced material consumption further enhances operational efficiency. Advancements in corrugation technology and recyclable materials are also improving the strength-to-weight ratio of single-wall cartons, reinforcing their dominance across multiple industries.

Double wall is the fastest-growing segment and is experiencing the fastest growth due to increasing demand for enhanced durability, stacking strength, and protection during long-distance transportation. These cartons feature two layers of fluting, making them suitable for heavier or more fragile items such as industrial equipment, automotive components, and bulk consumer goods.

The expansion of global supply chains and the rise of warehouse-based distribution models are key factors driving demand for stronger packaging solutions. For instance, logistics providers and manufacturers handling exports often prefer double-wall cartons to ensure product integrity during extended transit. Triple-wall cartons remain limited to heavy-duty applications such as machinery and large industrial shipments, while customized single-wall variants, such as coated or reinforced designs, are gaining traction in premium packaging segments where branding and presentation are equally important.

Box Design Insights

Regular slotted containers (RSC) lead the market with an anticipated 42% share due to their standardized design, cost efficiency, and versatility across industries. These boxes feature equal-length flaps that meet at the center when closed, providing structural integrity and ease of sealing. Their simple construction allows for mass production, efficient storage, and compatibility with automated packaging systems, making them the preferred choice for bulk shipping.

Industries such as food and beverage, electronics, and consumer goods rely heavily on RSC designs for consistent and reliable packaging. For example, companies such as Nestlé and Samsung Electronics utilize RSC cartons for large-scale distribution of packaged goods and devices. Their ability to accommodate a wide range of product sizes further strengthens their market position.

Window die-cut designs represent the fastest-growing segment and are gaining rapid traction as brands increasingly prioritize product visibility, differentiation, and consumer engagement. These cartons feature transparent or open windows that let customers view the product directly, enhancing shelf appeal and influencing purchasing decisions. They are widely used in retail segments such as cosmetics, confectionery, toys, and premium food packaging.

For instance, brands in the confectionery sector often use window die-cut cartons to showcase chocolates and baked goods, creating a more attractive presentation. The growth of organized retail and premiumization trends is further accelerating demand for these designs. Other formats, including tuck-end and auto-lock bottom cartons, cater to specialized requirements such as secure closures, ease of assembly, and tamper resistance, particularly in pharmaceuticals and high-value consumer goods.

Regional Insights

North America Die Cut Carton Market Trends - E-commerce Surge and Sustainability-Driven Automation

North America is the fastest-growing region, driven by strong e-commerce penetration, advanced packaging infrastructure, and increasing demand for sustainable solutions. The U.S. leads the market, supported by high consumer spending, a mature retail ecosystem, and highly efficient logistics networks. The rapid expansion of online retail, led by companies such as Amazon and Walmart, has significantly increased demand for corrugated packaging, particularly single-wall cartons for last-mile delivery. Sustainability initiatives and well-established recycling systems, including widespread curbside recycling programs, further support the adoption of paper-based packaging across industries.

Regulatory requirements in sectors such as food and pharmaceuticals are stringent, encouraging the use of high-quality, compliant packaging materials. Companies in the region are investing heavily in automation and sustainable innovation to remain competitive. For instance, International Paper has expanded its corrugated packaging capabilities and focused on recyclable material solutions, while WestRock continues to invest in automated packaging systems and fiber-based alternatives to plastic. Strategic acquisitions and product innovation initiatives are enabling companies to enhance production efficiency, reduce environmental impact, and strengthen their market positions.

Europe Die Cut Carton Market Trends - Circular Economy Policies and Eco-Packaging Leadership

Europe remains a key market characterized by strict environmental regulations and a strong emphasis on sustainable packaging solutions. Countries such as Germany, the U.K., France, and Spain are leading contributors due to their robust industrial bases, high environmental awareness, and well-established recycling infrastructure. The region’s regulatory framework, including policies that promote circular-economy principles, is driving the adoption of recyclable and reusable packaging materials at scale.

Major companies such as Smurfit Kappa Group and DS Smith are actively investing in sustainable packaging innovations, including fiber-based alternatives and closed-loop recycling systems. For example, DS Smith has implemented circular packaging solutions that integrate design, production, and recycling to minimize waste. Regulatory harmonization across the European Union further supports consistent adoption of eco-friendly materials and packaging standards.

Investments in the region are focused on improving material efficiency, reducing carbon emissions, and enhancing recyclability. Companies are increasingly adopting integrated business models that combine manufacturing, recycling, and design innovation. This approach not only ensures compliance with environmental regulations but also aligns with growing consumer demand for sustainable products, reinforcing Europe’s position as a leader in environmentally responsible packaging.

Asia Pacific Die Cut Carton Market Trends - Manufacturing Scale and E-commerce-Led Demand Dominance

Asia Pacific is the leading region, with an anticipated 41.3% market share in 2026, driven by large-scale manufacturing capabilities, expanding consumer markets, and rapid e-commerce growth. China, India, Japan, and Southeast Asian countries are key contributors, supported by rising disposable incomes and increasing demand for packaged goods. The dominance of e-commerce platforms such as Alibaba Group and JD.com has significantly boosted demand for corrugated packaging, particularly in China, the region's largest manufacturing hub.

The region benefits from cost-effective production, abundant raw material availability, and well-developed supply chain networks. In India, companies like ITC Limited are expanding their packaging divisions to cater to growing domestic demand while focusing on sustainable and recyclable materials. Similarly, Japanese firms such as Oji Holdings Corporation are investing in advanced packaging technologies and environmentally friendly solutions. Increasing investments in packaging infrastructure, automation, and sustainability initiatives are further accelerating growth.

Governments across the region are promoting eco-friendly packaging practices and strengthening waste management systems. As demand continues to rise, local manufacturers are expanding production capacity and adopting advanced technologies such as digital printing and smart packaging to enhance efficiency and product quality. This combination of scale, cost advantage, and innovation positions the Asia Pacific as the dominant and most dynamic region in the global packaging market.

Competitive Landscape

The global die cut carton market is moderately fragmented, with a mix of global leaders and regional players. Large companies dominate through integrated operations, economies of scale, and strong distribution networks. Smaller players also compete by offering customized solutions and specialized products. This combination creates a competitive environment where innovation and operational efficiency are key differentiators.

Market leaders focus on innovation, sustainability, and geographic expansion. Key strategies include investment in advanced manufacturing technologies, development of eco-friendly materials, and expansion into emerging markets. Companies are also strengthening supply chain integration to improve cost efficiency and responsiveness.

Key Industry Developments

- In January 2025, International Paper announced the completion of its acquisition of DS Smith, creating a global leader in sustainable packaging solutions with expanded capabilities across North America and EMEA regions. This strategic move strengthens its product portfolio in fiber-based packaging and enhances geographic reach and operational scale.

- In November 2025, Mondi launched an expanded corrugated and solid board packaging portfolio for the food industry, incorporating advanced digital printing capabilities and enhanced sustainable material solutions. This development aims to address increasing demand for retail-ready, compliant, and visually differentiated packaging formats.

Companies Covered in Die Cut Carton Market

- Smurfit Westrock plc

- Graphic Packaging Holding Company

- International Paper Company

- Mondi plc

- Mayr-Melnhof Karton AG

- Stora Enso Oyj

- Oji Holdings Corporation

- Rengo Co., Ltd.

- Huhtamäki Oyj

- Sonoco Products Company

- DS Smith plc

- Georgia-Pacific LLC

- Amcor plc

- Metsä Board Oyj

- American Carton Company

- Seaboard Folding Box Company, Inc.

Frequently Asked Questions

The global die cut carton market is estimated to be valued at US$40.8 billion in 2026.

The die cut carton market is projected to reach US$56.6 billion by 2033.

Key trends include the growing adoption of sustainable and recyclable packaging, rising demand for customized and premium carton designs, increased use of window die-cut formats for retail visibility, and strong growth in e-commerce-driven packaging solutions. Automation in packaging production and advancements in digital printing are also shaping the market.

The single wall segment is expected to be the leading category, accounting for 52.3% of the market share in 2026, due to its cost-effectiveness, lightweight nature, and suitability for high-volume applications such as e-commerce and retail distribution.

The die cut carton market is expected to grow at a CAGR of 4.8% from 2026 to 2033.

Some of the major players include Smurfit Westrock plc, Graphic Packaging Holding Company, International Paper Company, Mondi plc, and Stora Enso Oyj.