- Medical Devices

- Dental Laboratories Market

Dental Laboratories Market Size, Share, and Growth Forecast 2026 - 2033

Dental Laboratories Market by Laboratory Type (Independent Dental Laboratories, Corporate/Chain Dental Laboratories, Inhouse Dental Clinic Laboratories, Full service Dental Laboratories, Others), Service Type (Crown & Bridge Services, Denture Fabrication Services, Orthodontic Appliance Services, Implant Restoration Services, Others), Technology, and Regional Analysis, 2026 - 2033

Dental Laboratories Market Size and Trend Analysis

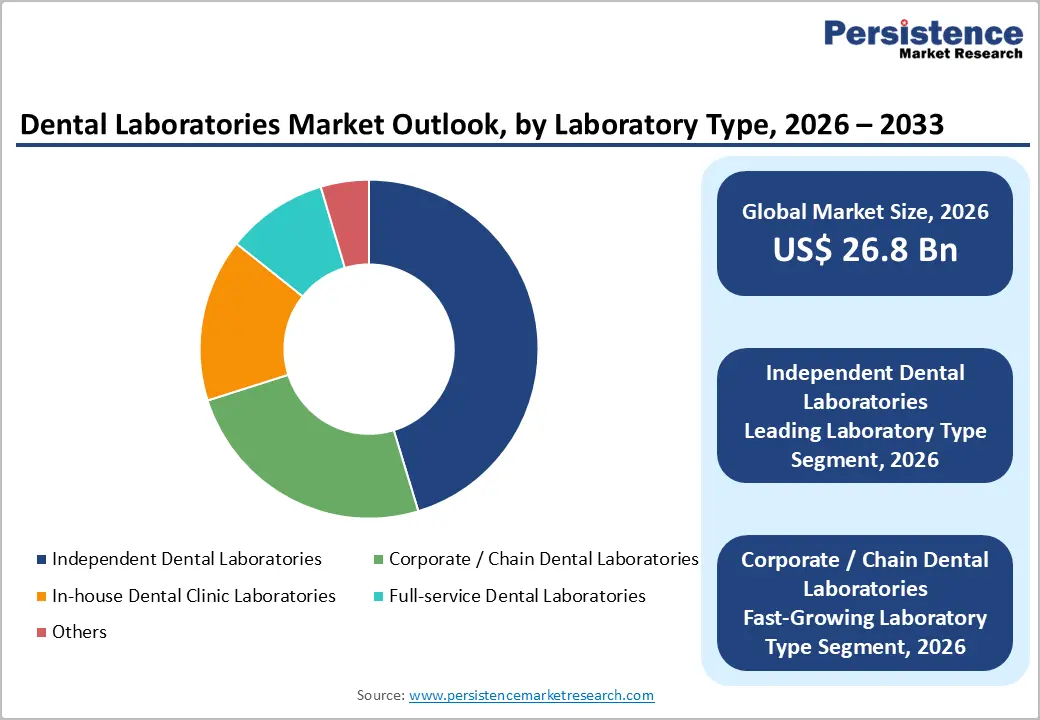

The global dental laboratories market size is expected to be valued at US$ 26.8 billion in 2026 and projected to reach US$ 38.3 billion by 2033, reaching a CAGR of 5.2% between 2026 and 2033.

This growth is driven by the convergence of demographic aging, digital dentistry transformation, and rapidly expanding dental implant and cosmetic restoration demand globally.

The World Health Organization (WHO) estimates that oral diseases affect nearly 3.5 billion people worldwide, with untreated tooth decay representing the most prevalent health condition globally.

As the aging population in North America, Europe, and Asia Pacific drive demand for prosthetic and restorative dental work, the adoption of CAD/CAM technology, 3D printing, and digital impression scanning is reshaping dental laboratory workflows enabling faster turnaround, improved precision, and new commercial models including centralized corporate laboratory networks and inoffice milling solutions. These forces together are systematically expanding the dental laboratory services market through 2033.

Key Market Highlights

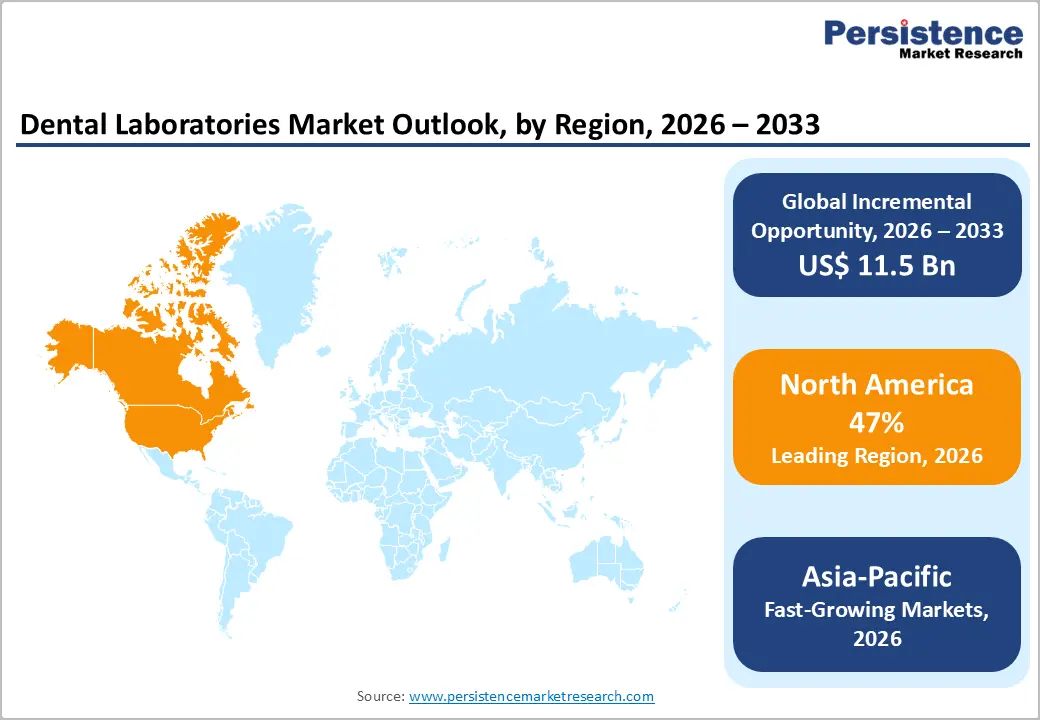

- Leading Region: North America leads the global Dental Laboratories market with approximately 47% revenue share in 2025, driven by high per-capita dental expenditure, an extensive NADL laboratory network of 46,000+ technologists, and DSO-driven corporate laboratory consolidation.

- Fast-Growing Market: Asia Pacific is the fast-growing dental laboratories region during 2026 - 2033, anchored by China's massive unmet dental care need (97% adult dental disease prevalence), India's expanding clinic network, Japan's aging population, and growing dental tourism in Southeast Asia.

- Dominant Segment: Independent Dental Laboratories lead with approximately 45% of market share in 2025, sustained by over 85% of U.S. dental labs being independently owned (NADL), though corporate chain models are growing fastest, driven by digital technology scale advantages.

- Fast-Growing Laboratory Type: Corporate/Chain Dental Laboratories are the fastest growing laboratory type during the forecast period, owing to digital CAD/CAM production, DSO integration, and centralized procurement drive market consolidation by groups including Glidewell Dental and National Dentex Labs.

- Key Opportunity: Implant Restoration Services represent the high-value growth opportunity with over 5 million implants placed annually in the U.S. (ICOI) as dental implant adoption grows globally and laboratory fabrication of implant crowns, abutments, and fullarch restorations generates substantially premium per unit revenue.

Market Dynamics

Is the Growing Demand for Prosthetic and Restorative Dental Services Driven by the Aging Population?

The global aging population is a prominent driver of the dental laboratories market. As individuals age, the prevalence of tooth loss, periodontal disease, and the need for restorative prosthetics, including crowns, bridges, dentures, and dental implants, increases dramatically. The United Nations Department of Economic and Social Affairs projects that the global population aged 65 and over will reach 1.5 billion by 2050, doubling from 761 million in 2021.

The American College of Prosthodontists estimates that approximately 178 million Americans are missing at least one tooth, with 40 million completely edentulous. Each tooth replacement whether via crown, bridge, implant crown, or complete denture, requires dental laboratory fabrication, creating durable, recurring revenue for both independent and corporate laboratory operators globally.

Digital Dentistry Transformation: Prominence of CAD/CAM, 3D Printing, and Workflow Automation?

The digital transformation of dental laboratory workflows is accelerating market growth by expanding production capacity, improving restoration accuracy, and enabling new competitive business models. CAD/CAM technology has become the production standard for ceramic crowns, bridges, and implant abutments, with leading systems including Dentsply Sirona's CEREC, Straumann's CARES, and 3Shape's Dental System driving adoption.

The American Dental Association (ADA) reported in its Health Policy Institute survey that digital impression adoption among U.S. dentists exceeded 40% in 2022. Intraoral scanner adoption rates are growing at over 20% annually globally, according to Straumann Group's investor disclosures, generating digital case files that feed directly into laboratory CAD/CAM and 3D printing workflows, reducing turnaround times from weeks to days and expanding laboratory throughput capacity.

How Does the Shortage of Skilled Dental Technicians and Laboratory Workforce Restrict Growth?

The global shortage of qualified dental technicians restricts the scaling of the laboratory workforce. The National Association of Dental Laboratories (NADL) in the U.S. has reported a persistent decline in the dental technician workforce, with laboratory employment contracting as experienced technicians retire without sufficient replacement from younger cohorts entering the profession.

The Bureau of Labor Statistics (BLS) projects a continued shortage of dental laboratory technologists through 2030. This workforce gap limits production capacity at independent laboratories and increases labor costs, constraining margin expansion and scalability across the sector.

Is There a Need for High Capital Investment for Digital Technology Adoption?

Transitioning from conventional analog laboratory workflows to fully digital CAD/CAM and 3D printing environments requires substantial capital investment. A professional-grade 5-axis milling machine costs US$ 50,000-US$ 300,000, while industrial dental 3D printers range from US$ 10,000 to US$ 150,000 per unit.

For the majority of the 150,000+ independent dental laboratories operating globally, these capital requirements are prohibitive without external financing or consolidation into corporate networks, creating a bifurcation between well-capitalized operators and smaller traditional labs unable to compete on technology, speed, or cost.

Emergence of Corporate/Chain Dental Laboratory Consolidation Encourages Novel Opportunities?

Corporate and chain dental laboratory models represent the fastest growing laboratory type segment, driven by the economic advantages of centralized digital production infrastructure, volume based procurement of materials, and standardized quality management systems. Groups including Glidewell Dental, National Dentex Labs (NDX), and Affordable Care (AC Group) in the U.S. have built multifacility networks processing millions of cases annually, achieving per unit economics unavailable to independent operators.

The NADL estimates that corporate networks now account for a growing share of U.S. laboratory case volume, a trend expected to accelerate globally as dental service organizations (DSOs) vertically integrate laboratory services. Investors are actively backing laboratory consolidation platforms in Europe and Asia Pacific, creating a high-growth commercial model that will capture increasing market share in the forecast period.

Implant Restoration Services: High Value Aligned with Global Implant Adoption Surge

Implant restoration laboratory services represent one of the high-value and fastest-growing service categories. As the dental implant placement volumes are globally growing, the FDA and CE-approved next-generation implant systems, and expanding dental insurance coverage, laboratory demand for implant crowns, abutments, and prosthetic superstructures grows in parallel.

The International Congress of Oral Implantologists (ICOI) estimates that over 5 million implants are placed annually in the U.S. alone, each requiring laboratory-fabricated restoration components with average per-unit revenues substantially exceeding conventional crown and bridge work. Dental laboratories that invest in titanium milling, zirconia implant crown fabrication, and certified digital implant workflows compatible with Straumann, Nobel Biocare, and Zimmer Biomet implant systems are positioned to capture premium, high-margin revenue growth through the forecast period.

Category-wise Analysis

Laboratory Type Insights

The independent dental laboratories segment leads the dental laboratories market by laboratory type, accounting for approximately 45% of total market revenue in 2026. Despite the growing corporate laboratory consolidation trend, independent laboratories continue to dominate by sheer number and established relationships with local dental practices built over decades of personalized service.

The National Association of Dental Laboratories (NADL) estimates that over 85% of U.S. dental laboratories are independently owned and operated. Independent laboratories differentiate through custom artistry, direct technician dentist communication, and flexibility in complex case management that large volume corporate networks may not offer. However, their share is gradually declining relative to corporate chains as digital technology scale advantages become more pronounced, confirming the sector's structural evolution.

Service Type Insights

The crown & bridge services segment leads the dental laboratories market by service type, representing approximately 40% of service revenue in 2026. Crown and bridge restorations are the highest volume single tooth and multiunit fixed prosthetic service in dentistry, representing the core revenue stream for the majority of dental laboratories globally.

The American Dental Association (ADA) consistently reports crown fabrication as among the top five most performed dental procedures in the U.S., with millions of crowns fabricated annually. The segment has been transformed by CAD/CAM technology, enabling same-day crown fabrication through in-office milling or rapid laboratory turnaround via digital workflows, sustaining high-volume demand while improving quality and reducing remakes that previously constrained laboratory profitability.

Technology Insights

The CAD/CAM Technology segment leads the dental laboratories market by technology, accounting for approximately 46% of technology-based revenue in 2026. CAD/CAM has displaced conventional casting and manual ceramic build-up as the production standard for ceramic and zirconia dental restorations, driven by its superior dimensional accuracy (±20 microns vs. ±100+ microns for conventional techniques), reduced marginal error rates, and compatibility with digital impression workflows.

DENTSPLY Sirona's CEREC system, with over 60,000 units installed globally and Roland's DWX milling series are among the most widely deployed CAD/CAM platforms in laboratories worldwide. As zirconia disc and polymer material costs decline, CAD/CAM-based laboratory workflows continue to expand their addressable case types and dominate technology adoption metrics through 2033.

Regional Insights

North America Dental Laboratories Market Trends and Insights

North America is likely to account for approximately 46.8% of the global dental laboratories market revenue in 2026, supported by the adoption of advanced restorative dentistry, a highly consolidated dental service organization (DSO) ecosystem, and strong penetration of CAD/CAM and 3D printing technologies. The region benefits from high per-capita dental expenditure, broad insurance coverage, and increasing demand for implant-supported and cosmetic restorations. The United States dominates the regional market with nearly 86% share, while Canada is emerging as a faster-growing market due to expanded federal dental reimbursement programs.

United States Dental Laboratories Market Trends

The United States is likely to represent about 85.7% of North American dental laboratory revenue in 2026. The country has more than 200,000 practicing dentists and a large network of independent and corporate laboratories. Rapid adoption of digital workflows, zirconia restorations, and implant prosthetics, along with continued consolidation by dental service organizations, is sustaining robust laboratory outsourcing volumes.

Canada Dental Laboratories Market Trends

Canada accounted for roughly 10.9% of the regional market in 2026 and is projected to reach a positive CAGR in the coming years. Its growth is driven by the Canadian Dental Care Plan (CDCP), which is expanding access to restorative and prosthetic procedures among previously uninsured populations, increasing crown, bridge, and denture case volumes across domestic laboratory networks.

Europe Dental Laboratories Market Trends and Insights

Europe captured around 29.4% of the global dental laboratories market revenue in 2026, making it the second-largest regional market. Demand is supported by favorable reimbursement frameworks for dental prosthetics, a large aging population, and strong adoption of digital manufacturing technologies. Regulatory harmonization under the EU Medical Device Regulation (MDR) is improving quality standards across laboratories. Germany leads the region, while the United Kingdom and France continue to expand through public reimbursement and growing private cosmetic dentistry demand.

Germany Dental Laboratories Market Trends

Germany held an estimated 24.6% share of the European market in 2025. The country maintains one of the world’s most advanced dental laboratory sectors, supported by extensive statutory reimbursement for prosthetics, a dense laboratory network, and widespread use of zirconia, ceramic restorations, and CAD/CAM-based digital production technologies.

United Kingdom Dental Laboratories Market Trends

The United Kingdom accounted for approximately 14.8% of the regional market in 2025 and is expected to expand at a CAGR of about 6.6% through 2033. Growth is supported by stable NHS prosthetic demand and increasing uptake of premium private treatments, including implants, veneers, and clear aligner-related restorative services.

Asia Pacific Dental Laboratories Market Trends and Insights

Asia Pacific represented approximately 18.9% of global dental laboratories market revenue in 2025 and is projected to register the fastest growth, with an estimated CAGR of 8.8% from 2026 to 2033. Growth is fueled by expanding dental clinic networks, rising disposable incomes, increasing demand for aesthetic restorations, and the rapid digitalization of laboratories. China dominates the region as both a domestic growth market and an international outsourcing hub, while Japan and India contribute significantly through aging demographics and expanding access to oral healthcare.

China Dental Laboratories Market Trends

China accounted for nearly 41.5% of Asia Pacific dental laboratory revenue in 2025. The country combines strong domestic demand for restorative dentistry with a large export-oriented manufacturing base producing ceramic crowns, dentures, and aligner models for laboratories and clinics worldwide.

Japan Dental Laboratories Market Trends

Japan held around 22.8% of the regional market in 2025. A rapidly aging population, broad reimbursement for dentures and prosthetics, and high utilization of premium ceramic and implant-supported restorations continue to drive consistent laboratory demand across the country.

Competitive Landscape

The global dental laboratories market is highly fragmented at the operator level, with over 150,000 laboratories operating globally (predominantly independent), yet increasingly consolidated at the network level through corporate dental laboratory groups. Market leaders, including Glidewell Dental, National Dentex Labs (NDX), and ClearChoice in North America, and Straumann Group's laboratory service subsidiaries in Europe, differentiate through digital production scale, material science R&D, and DSO partnership programs.

Key competitive trends include dental tourism, laboratory outsourcing to China, India, and Thailand; the rise of in-house chairside milling eroding traditional laboratory case volumes in select prosthetic categories; and AI-assisted design tools accelerating case throughput.

Key Developments:

- March 2025: Straumann Group expanded its ClearCorrect aligner laboratory network into 12 new Asia Pacific markets, integrating digital scanning, AI-powered treatment planning, and centralized laboratory production for orthodontic appliance fabrication.

- November 2024: Glidewell Dental launched its BruxZir NOW same-day zirconia crown service across its U.S. laboratory network, enabling a 4-hour turnaround for single-unit zirconia crowns via intraoral scantomill digital workflows.

- June 2024: Dentsply Sirona announced integration of AI-assisted crown design into its inLab CAD software platform, reducing crown design time from 20 to under 5 minutes per unit, targeting laboratory productivity improvements across its global installed base.

Companies Covered in Dental Laboratories Market

- Cameron Station Dental Care

- FULLER SMILES Inc.

- Venice Family Clinic Dental Center

- Kids Dental Avenue

- Kreativ Dental Clinic

- Kalmar Implant Dentistry

- Dental Clinic Antalya

- Dentineo Dental Clinic

- ForteDent Dental Clinic

- FMS Dental Hospitals

- Beverly Wilshire Dental Centre

- Goodness Dental

- ClearChoice Dental Implant Center

- Picasso Dental Clinic

- Clove Dental

- Others

Frequently Asked Questions

The dental laboratories market size is projected to reach US$ 38.3 billion by 2033, growing at an accelerated forecast CAGR of 5.2% between 2026 and 2033, driven by digital technology adoption and aging population prosthetics demand.

The rising prevalence of tooth loss, dental caries, and cosmetic dentistry procedures is increasing demand for crowns, bridges, dentures, implants, and orthodontic restorations outsourced to dental laboratories.

North America leads with approximately 46.8% of global dental laboratories' revenue in 2026. The U.S. dominates through the world's highest per capita dental expenditure, a network of over 200,000 practicing dentists (ADA), approximately 46,000 dental laboratory technologists (BLS), and active DSO-led corporate laboratory consolidation. Canada's Canadian Dental Care Plan (CDCP) is additionally expanding case volumes.

Rapid adoption of digital dentistry technologies, including CAD/CAM, 3D printing, and intraoral scanning, is enabling dental laboratories to expand high-margin, precision-based restorative and aesthetic services.

The market includes specialized dental clinic and laboratory operators across regions: ClearChoice Dental Implant Center, FMS Dental Hospitals, Clove Dental, Glidewell Dental, and National Dentex Labs (NDX) are among the most commercially significant operators.