- Hardware & Software IT Services

- Managed Data Center Services Market

Managed Data Center Services Market Size, Share, and Growth Forecast, 2026 - 2033

Managed Data Center Services Market by Service Type (Managed IT Infrastructure, Managed Security Services, Others), Deployment Model (Cloud, On-Premise, Others), Enterprise Size, and Regional Analysis for 2026 - 2033

Managed Data Center Services Market Size and Trends Analysis

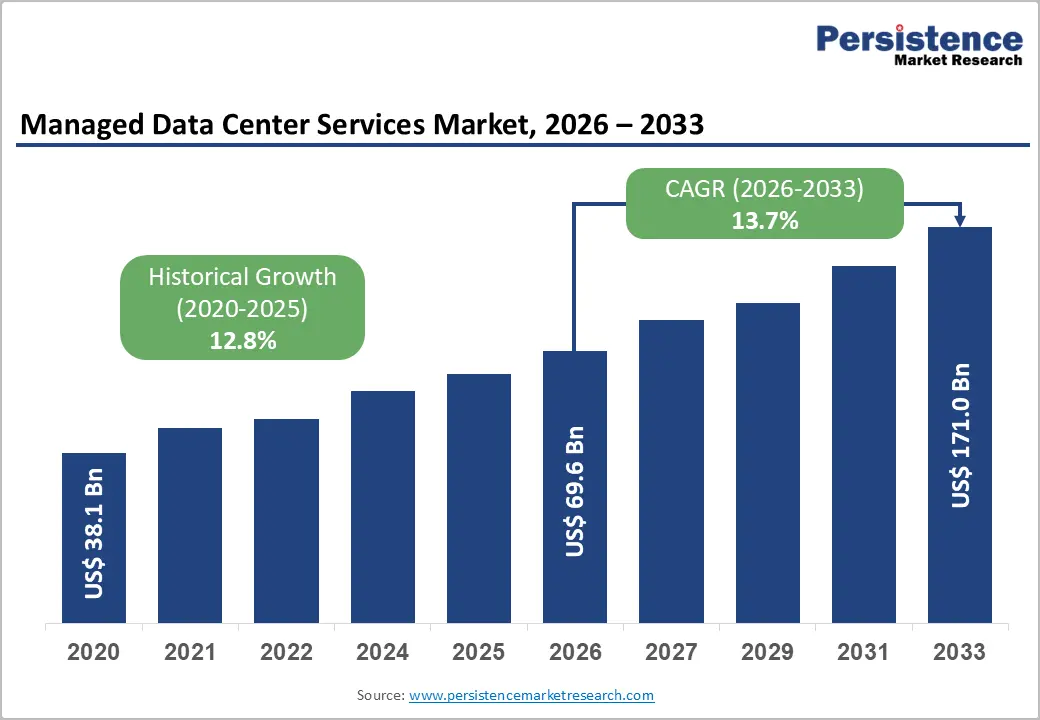

The global managed data center services market size is likely to be valued at US$69.6 billion in 2026 and is expected to reach US$171.0 billion by 2033, driven by a structural transition from in-house infrastructure management to outsourced service models. Increasing security demands, stricter regulatory compliance requirements, and the need for scalable, cloud-integrated solutions are key contributing factors.

In addition, the rapid adoption of public cloud, hybrid IT environments, and AI-enabled infrastructure is further boosting demand for managed services that enhance uptime, reduce operational costs, and ensure effective governance across increasingly complex IT ecosystems.

Key Industry Highlights:

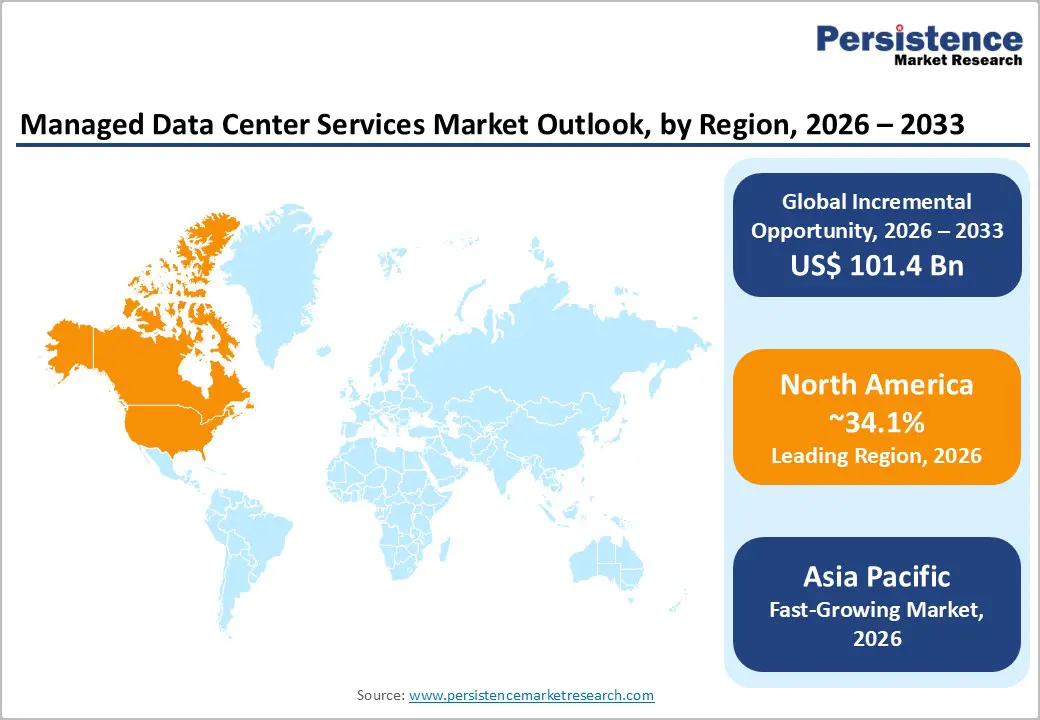

- Leading Region: North America is projected to account for 34.1% of the market share, driven by strong cloud adoption, advanced digital infrastructure, and significant investments in AI-ready data center operations.

- Fastest-growing Region: Asia Pacific is likely to be the fastest-growing region, supported by rapid digitalization, increasing cloud penetration, and large-scale data center investments across China, India, Japan, and Southeast Asia.

- Investment Plans: Industry investments are heavily focused on AI-driven data center expansion, energy-efficient infrastructure, and hybrid cloud ecosystems, with hyperscalers and service providers allocating substantial capital toward high-density computing, cooling technologies, and regional data center expansion.

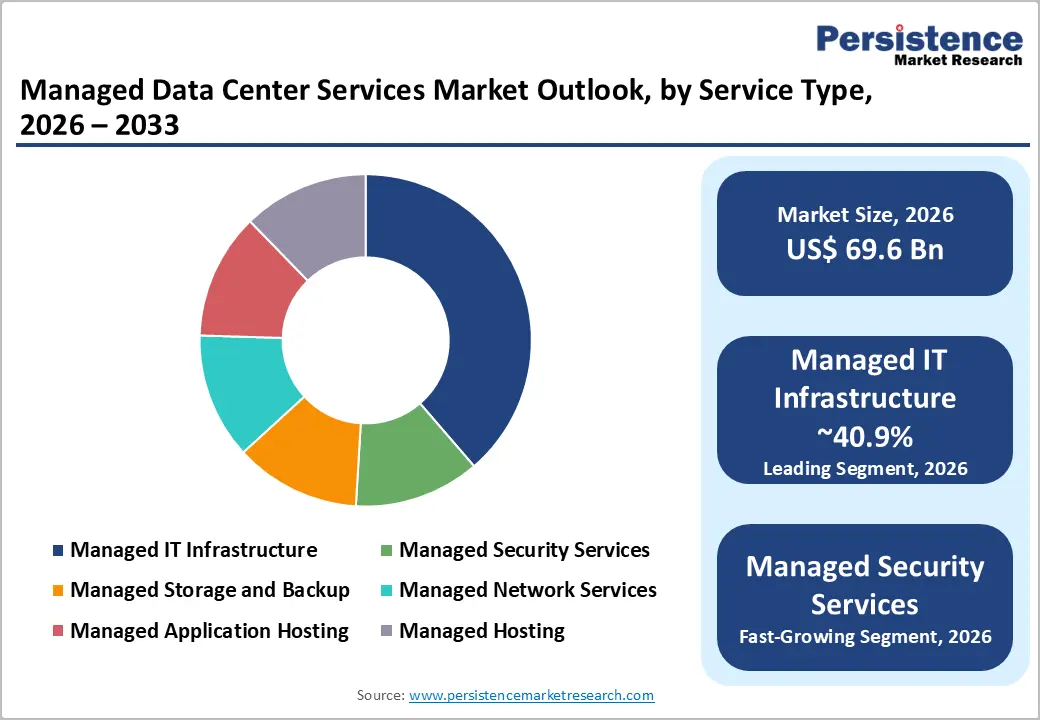

- Dominant Service Type: Managed IT Infrastructure is expected to dominate, holding an anticipated 40.9% market share, as enterprises prioritize outsourcing core infrastructure operations to ensure scalability, efficiency, and business continuity.

- Leading Deployment Model: Cloud deployment is expected to lead the market with an estimated 61.4% market share in 2026, driven by demand for scalable, on-demand, and cost-efficient infrastructure solutions.

DRO Analysis

Driver - Rising Cloud Adoption and Workload Modernization are expanding the Addressable Market

Enterprise cloud adoption has reached a critical inflection point, with a majority of organizations now utilizing cloud-based services across core business functions. Large enterprises show the highest adoption rates, followed by medium-sized firms, while small businesses are steadily increasing their usage. These trends are accompanied by growing reliance on advanced workloads such as enterprise resource planning, database management, application development, and security platforms.

This shift is significant as managed data center services increasingly underpin cloud operations, including migration, integration, monitoring, and lifecycle management. Organizations are moving away from standalone hosting models toward continuous optimization frameworks that require real-time visibility, automated management, and cross-platform interoperability. As digital transformation initiatives deepen, enterprises seek unified operating models spanning legacy infrastructure, private cloud, and public cloud environments, thereby reinforcing demand for managed services.

AI Adoption and Rising Energy Intensity are Driving Demand for Operational Expertise

The rapid expansion of artificial intelligence workloads is significantly increasing data center complexity and energy consumption. Global data center electricity demand has grown at a double-digit rate, with AI-focused data centers expanding even faster. Projections indicate that overall data center energy consumption will nearly double within the next decade.

This trend introduces new operational challenges, including power efficiency, cooling optimization, workload balancing, and sustainability reporting. Data centers already account for a measurable share of global electricity usage, prompting regulatory bodies to introduce stricter transparency requirements and performance standards. Managed service providers are well-positioned to address these challenges by delivering energy-efficient operations, predictive maintenance, and compliance-ready reporting frameworks. As AI adoption scales, the role of managed services is evolving from infrastructure support to strategic operational enablement.

Restraint - Cost Pressures, Vendor Lock-In, and Infrastructure Complexity Limit Adoption

Despite strong growth prospects, the market faces structural constraints related to cost and complexity. Managed data center services require significant upfront investment in infrastructure, including servers, networking equipment, and cooling systems. These capital requirements are further amplified by the need for continuous upgrades and energy management capabilities.

Vendor lock-in remains a critical concern for enterprises, as long-term contracts, proprietary technologies, and limited interoperability can restrict flexibility. Switching providers often involves high transition costs, operational disruption, and data migration challenges. These factors can slow adoption, particularly among cost-sensitive organizations and those operating in highly regulated environments. While managed services reduce internal complexity, they also require careful vendor selection and contract management to mitigate long-term risks.

Opportunity - Security-Led Managed Services Present a High-Growth Opportunity

The increasing frequency and sophistication of cyber threats are driving demand for managed security services. Modern threat landscapes include AI-enabled attacks, ransomware, identity breaches, and hybrid environment vulnerabilities. A significant proportion of security incidents originates from phishing and social engineering, while hybrid infrastructures introduce additional exposure points.

Enterprises are responding by outsourcing security operations to managed service providers that offer continuous monitoring, threat intelligence, incident response, and compliance management. This shift is particularly evident in organizations seeking to enhance security posture without significantly expanding internal teams. The most promising opportunity lies in integrated security offerings that combine data center, cloud, and identity protection into a unified managed framework.

Regulatory Compliance and Sustainability Requirements are Creating New Service Lines

Governments and regulatory bodies are introducing stricter requirements for data center energy efficiency, reporting, and environmental impact. These include mandatory disclosure frameworks, performance rating systems, and minimum efficiency standards. Organizations are increasingly required to demonstrate compliance with these regulations while maintaining operational efficiency.

This environment creates a strong opportunity for managed service providers to offer compliance-driven solutions, including energy monitoring, carbon tracking, workload optimization, and regulatory reporting. Enterprises are prioritizing providers that can deliver both operational excellence and measurable sustainability outcomes. As environmental accountability becomes a core business requirement, managed services are evolving into a critical enabler of compliance and corporate responsibility.

Category-wise Analysis

Service Type Insights

Managed IT infrastructure is expected to dominate, holding approximately 40.9% market share in 2026, due to its foundational role in supporting enterprise operations. This segment encompasses compute, storage, networking, virtualization, patch management, and capacity planning. Organizations often prioritize outsourcing infrastructure management because it is resource-intensive and requires specialized expertise. For example, global enterprises in banking and telecommunications increasingly rely on managed infrastructure providers to maintain high-availability environments across multiple data centers while ensuring real-time transaction processing and minimal downtime.

The segment benefits from its direct link to business continuity, making it a recurring and essential service. It also serves as the entry point for broader managed service engagements, allowing providers to expand into adjacent offerings such as security, application management, and performance optimization. For instance, a multinational retail company outsourcing its infrastructure management often extends the contract to include application hosting and disaster recovery services to support seasonal demand fluctuations and ensure uninterrupted operations.

Managed security services are likely to be the fastest-growing segment, experiencing rapid growth due to increasing cyber risks and regulatory requirements. Enterprises are investing in advanced security capabilities, including threat detection, identity management, and incident response, to address evolving threats. For example, financial institutions are adopting managed security operations centers (SOCs) to monitor transactions and detect fraud in real time, while healthcare organizations are outsourcing security to protect sensitive patient data and comply with data protection regulations.

The shift toward cloud and hybrid environments further amplifies security challenges, driving demand for specialized expertise. Organizations are increasingly outsourcing security operations to ensure continuous monitoring and compliance, making this segment one of the most attractive growth areas within the market. For instance, technology companies deploying hybrid cloud environments often integrate managed security services to secure both on-premise systems and cloud workloads under a unified framework.

Deployment Model Insights

Cloud deployment is expected to be both the leading and fastest-growing model, with an anticipated share of 61.4% over the forecast period. Cloud-based managed services dominate the market due to their scalability, flexibility, and cost efficiency. Enterprises benefit from on-demand resource allocation, rapid deployment, and consumption-based pricing models. These advantages make cloud deployment particularly attractive for dynamic workloads and digital transformation initiatives.

For example, global e-commerce companies leverage managed cloud services to automatically scale infrastructure during peak shopping periods, ensuring seamless user experiences without overinvesting in permanent capacity. Managed service providers play a crucial role in enabling cloud adoption by offering migration, integration, monitoring, and optimization services. As organizations continue to expand their cloud footprints, demand for managed cloud services is expected to grow significantly. For instance, enterprises migrating legacy ERP systems to cloud environments often rely on managed service providers to handle data migration, performance tuning, and ongoing system management.

On-premise deployment remains relevant for organizations with strict data sovereignty, regulatory, or latency requirements. For example, government agencies and defense organizations often maintain on-premise data centers to retain full control over sensitive information. Hybrid models are increasingly common, allowing enterprises to balance control and flexibility by combining on-premise infrastructure with cloud resources. A typical example includes financial services firms that store critical customer data on-premises while using cloud environments for analytics and customer-facing applications.

Managed service providers are essential in orchestrating these complex environments, ensuring seamless integration, security, and performance across platforms.

Regional Insights

North America Managed Data Center Services Market Trends - AI-Ready Infrastructure Expansion and Hybrid Cloud Automation Leadership

North America is expected to lead, accounting for 34.1% of market share in 2026 and maintaining a strong growth trajectory with a CAGR of 13.3%. The region’s leadership is supported by a mature IT ecosystem, high cloud adoption rates, and a concentration of leading technology providers such as IBM, Amazon Web Services, Microsoft Azure, and Google Cloud. A notable development is IBM’s acquisition of HashiCorp in 2025, which strengthens hybrid cloud automation and enhances managed infrastructure capabilities. This directly supports the market shift toward integrated, automated service delivery models.

The U.S. plays a central role, driven by large-scale enterprise demand, advanced digital infrastructure, and significant investment in AI and cloud technologies. Hyperscalers such as Amazon, Microsoft, and Google continue to expand AI-ready data centers across key states, increasing demand for managed services related to workload optimization, cooling, and energy efficiency. For example, Digital Realty has expanded high-density colocation capacity to support AI workloads, while Equinix continues to scale interconnection services to enable hybrid cloud environments. These investments are reshaping the region’s infrastructure toward high-performance, low-latency ecosystems.

Regulatory considerations, including data privacy and energy efficiency, are shaping market dynamics, encouraging the adoption of managed services that ensure compliance and operational resilience. Increasing scrutiny on energy consumption has led companies such as Schneider Electric to introduce advanced energy management and cooling solutions tailored for data centers. Investment trends indicate continued expansion in AI-ready infrastructure, edge data centers, and hybrid cloud solutions, reinforcing North America’s leadership in both innovation and service delivery.

Europe Managed Data Center Services Market Trends - Sovereign Cloud Growth and Compliance-Driven Managed Services Adoption

Europe represents a significant market characterized by strong cloud adoption and a robust regulatory framework. Over half of enterprises in the region use cloud services, with higher adoption rates in advanced economies. Leading providers, such as OVHcloud, Atos, and Capgemini, are actively expanding managed service portfolios to address growing enterprise demand. For example, OVHcloud has continued to invest in sovereign cloud infrastructure, which aligns with Europe’s focus on data sovereignty and local data control.

Regulatory initiatives focusing on data protection, energy efficiency, and sustainability are key drivers of demand. Frameworks such as the General Data Protection Regulation (GDPR) and emerging energy-efficiency mandates are pushing enterprises to adopt managed services that ensure compliance and transparency in reporting. Companies such as Schneider Electric and Siemens are introducing smart energy and automation solutions for European data centers, helping operators meet strict environmental standards while optimizing performance.

Major markets such as Germany, the U.K., France, and Spain are leading adoption, supported by digital transformation initiatives and enterprise modernization efforts. For instance, Equinix has expanded its presence in Frankfurt and Paris to support interconnection demand, while Orange Business continues to strengthen managed cloud and data center offerings. The emphasis on data sovereignty and cross-border operations further drives demand for hybrid and managed service models across the region.

Asia Pacific Managed Data Center Services Market Trends - Rapid Digitalization and Hyperscaler-Led Multi-Cloud Expansion

Asia Pacific is likely to be the fastest-growing region, with a projected CAGR of 15.1%. Growth is driven by rapid digitalization, expanding cloud adoption, and increasing investment in data center infrastructure. Major players such as NTT DATA, Alibaba Cloud, and Tencent Cloud are expanding their managed service capabilities across the region. A key development is NTT DATA’s 2025 partnership with Google Cloud to accelerate AI-driven cloud transformation, highlighting the region’s focus on next-generation infrastructure.

Key markets include China, Japan, India, and Southeast Asia, each contributing to regional growth through large-scale infrastructure development and enterprise demand. In Southeast Asia, Equinix’s acquisition of data centers in the Philippines has strengthened its regional footprint, supporting the growth of the digital economy. Similarly, Digital Realty has expanded its presence in Japan to support high-performance computing and AI workloads.

Rising AI adoption and the growth of the digital economy are creating new opportunities for managed service providers. In India, hyperscalers such as Amazon Web Services and Microsoft Azure are investing in new data center regions, driving demand for managed infrastructure and security services. The focus on local data residency, energy efficiency, and scalable infrastructure solutions is shaping market development. As enterprises continue to modernize their IT environments, demand for managed services is expected to accelerate, particularly in hybrid and multi-cloud deployments across the Asia Pacific.

Competitive Landscape

The global managed data center services market is moderately fragmented, with a mix of global technology providers, infrastructure specialists, and regional service providers. While the underlying cloud infrastructure layer is relatively concentrated, the managed services segment remains competitive, with providers differentiating through service quality, integration capabilities, and geographic presence.

Recent industry developments highlight a shift toward integrated platforms and AI-driven services. Major providers have focused on acquisitions to strengthen hybrid cloud capabilities, partnerships to expand cloud ecosystems, and geographic expansions to enhance global reach.

Leading players are focusing on platform integration, cloud partnerships, geographic expansion, and security-driven differentiation. The market is moving toward outcome-based service models that emphasize performance, scalability, and compliance, supported by automation and AI-driven operations.

Key Industry Developments:

- In February 2025, IBM announced the completion of its acquisition of HashiCorp to strengthen hybrid cloud and infrastructure automation capabilities, enabling enterprises to better manage and secure multi-cloud and AI-driven data center environments.

- In June 2025, Equinix completed the acquisition of three data centers in Manila from Total Information Management, expanding its footprint in Southeast Asia and enabling enterprises to scale digital infrastructure and interconnect with global cloud and network ecosystems.

Companies Covered in Managed Data Center Services Market

- IBM

- Kyndryl

- DXC Technology

- NTT DATA

- Accenture

- Capgemini

- Hewlett Packard Enterprise

- Dell Technologies

- Cisco

- Rackspace Technology

- Equinix

- Digital Realty

- Oracle

- Schneider Electric

- Fujitsu

- Tata Consultancy Services

Frequently Asked Questions

The managed data center services market is valued at US$69.6 billion in 2026.

The global managed data center services market is projected to reach US$171.0 billion by 2033.

Key trends include the rapid expansion of cloud and hybrid deployment models, growing adoption of AI-ready data center infrastructure, increasing demand for managed security services, and a stronger focus on energy efficiency and regulatory compliance.

Managed IT Infrastructure is the leading segment, accounting for an anticipated 40.9% market share, due to its critical role in supporting enterprise operations and business continuity.

The managed data center services market is expected to grow at a CAGR of 13.7% between 2026 and 2033.

Major players with strong portfolios include IBM, NTT DATA, Equinix, Digital Realty, and Cisco.