- Oil & Gas

- Enhanced Oil Recovery Market

Enhanced Oil Recovery Market Size, Share, and Growth Forecast 2026 - 2033

Enhanced Oil Recovery Market by Technology Type (Thermal EOR (Steam, In-Situ Combustion, Others (Hot Water and Solar)), Chemical (Polymer, Surfactant, Alkaline Surfactant Polymer), Gas EOR (CO2 Gas, Other Gases), Others), Application (Onshore, Offshore), and Regional Analysis for 2026 - 2033

Enhanced Oil Recovery Market Size and Trend Analysis

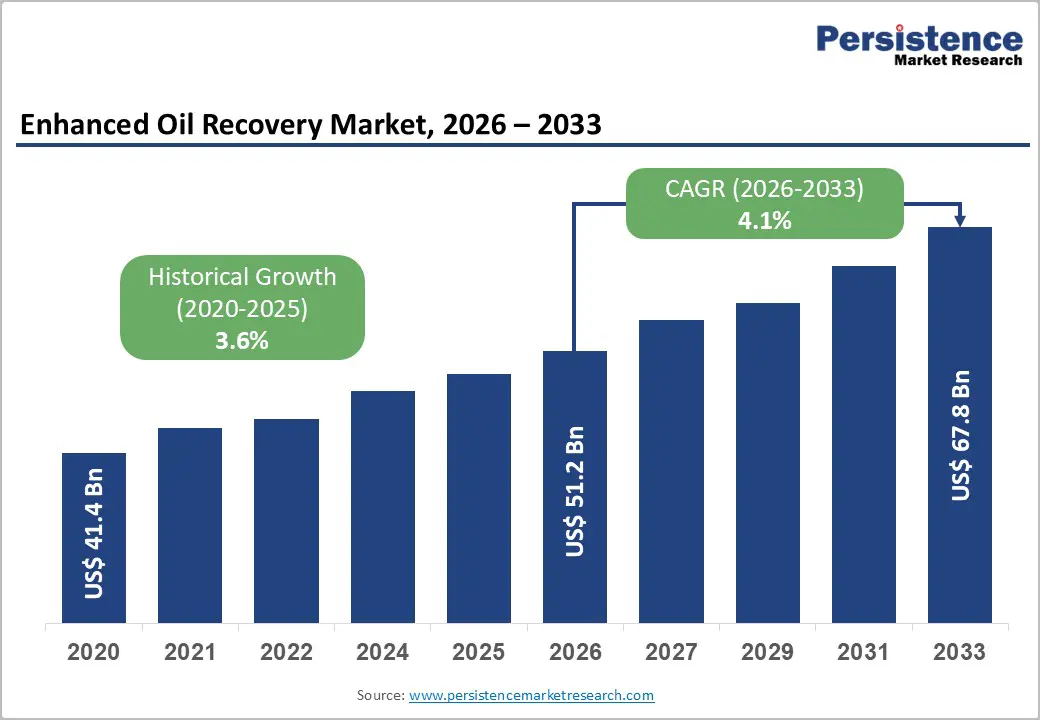

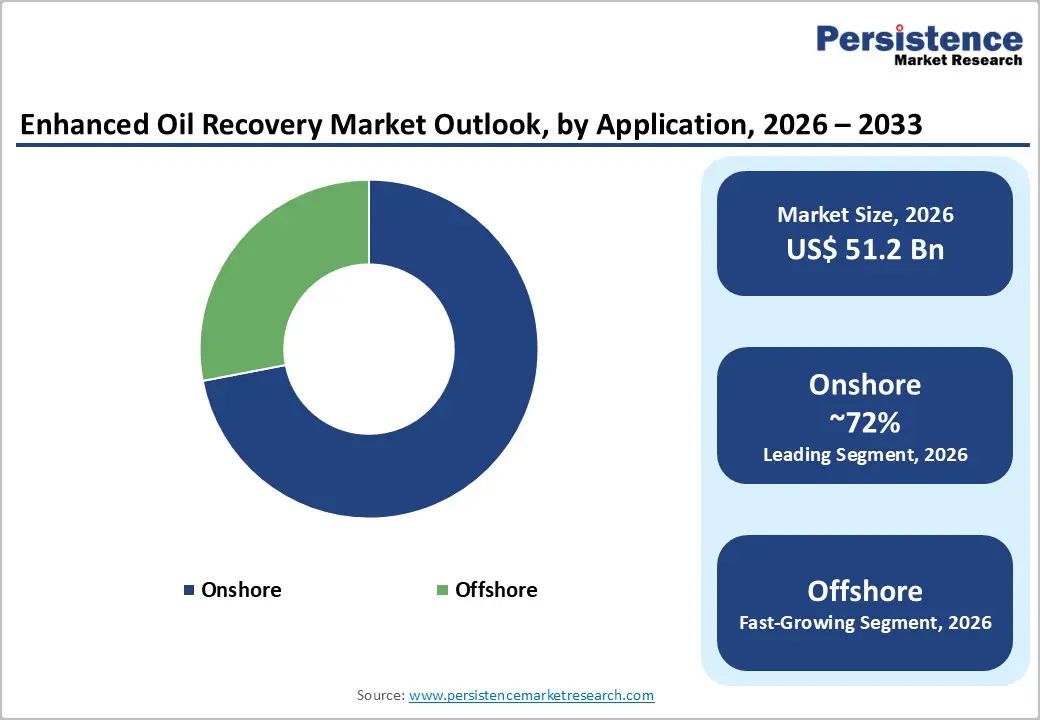

The global enhanced oil recovery market size is valued at US$ 51.2 Bn in 2026 and is projected to reach US$ 67.8 Bn by 2033, growing at a CAGR of 4.1% between 2026 and 2033.

This sustained growth is driven by the accelerating depletion of conventional oil fields worldwide, where primary and secondary recovery methods typically extract only 30-40% of original oil in place, compelling operators to deploy advanced EOR techniques to maximize production from existing reservoirs.

The convergence of CO2-Enhanced Oil Recovery with Carbon Capture, Utilization, and Storage (CCUS) frameworks, supported by fiscal incentives such as the U.S. 45Q tax credit, and the rising economic viability of thermal EOR in heavy oil reserves across Canada, China, and the Middle East, is amplifying investment commitments from both national oil companies and international supermajors.

Key Market Highlights

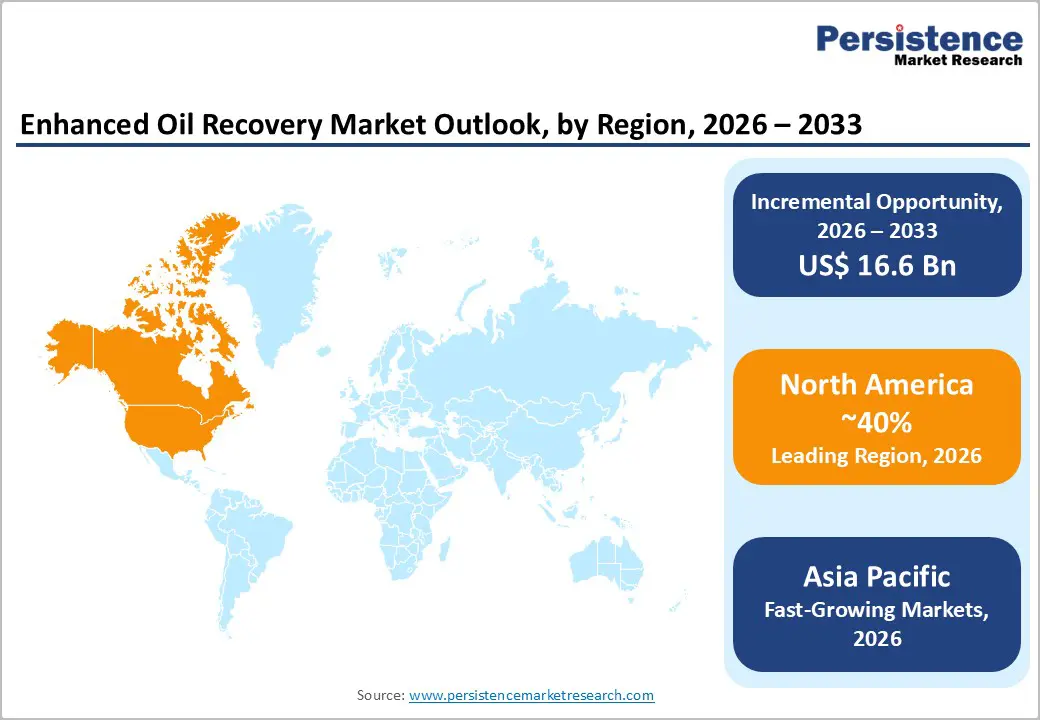

- Leading Region: North America leads the global enhanced oil recovery market, accounting for approximately 35-40% of total revenue, underpinned by over 100 commercial CO2-EOR projects in the Permian Basin, U.S. 45Q tax credit incentives, and Canada's large-scale thermal SAGD operations in the Alberta oil sands.

- Fastest Growing Region: Asia Pacific is the fastest-growing EOR region, driven by China's PetroChina and Sinopec large-scale thermal programs in the Liaohe and Shengli fields, India's ONGC chemical EOR expansion, and ASEAN mature offshore field revitalization initiatives, collectively registering among the highest regional CAGRs globally.

- Dominant Segment: The Thermal EOR technology type segment leads the market with approximately 35% of global revenue, driven by its critical role in extracting heavy and extra-heavy crude oil from over 1 trillion barrels of technically recoverable USGS-estimated global heavy oil and bitumen resources.

- Fastest-Growing Segment: Gas EOR, CO2 Gas injection is the fastest-growing technology segment, propelled by the U.S. 45Q tax credit providing up to US$ 85 per tonne for sequestered CO2, Occidental Petroleum's Permian Basin CO2-EOR scale-up, and the global CCUS regulatory framework creating dual-revenue project economics for CO2 injection operators.

- Key Market Opportunity: Solar-assisted thermal EOR, exemplified by the ADNOC/GlassPoint Miraah Solar Plant generating 1,021 MW of solar thermal energy, offers oil producers in the Middle East and sun-rich producing regions the opportunity to dramatically reduce steam generation costs and carbon intensity, unlocking new EOR project economics aligned with net-zero operational targets through 2033.

| Key Insights | Details |

|---|---|

| Enhanced Oil Recovery Market Size (2026E) | US$ 51.2 Bn |

| Market Value Forecast (2033F) | US$ 67.8 Bn |

| Projected Growth CAGR (2026 - 2033) | 4.1% |

| Historical Market Growth (2020 - 2025) | 3.6% |

DRO Analysis

Market Growth Drivers

Maturing Global Oil Field Base Compelling Widespread EOR Deployment

The progressive maturation of conventional oil reservoirs across every major producing region is the most fundamental structural driver of the global enhanced oil recovery market. According to the International Energy Agency (IEA), natural decline rates in existing producing fields average 6-8% annually without sustained capital intervention, creating a persistent gap between production supply and global energy demand that EOR techniques are uniquely positioned to bridge. Primary recovery methods capture only 20-30% of the original oil in place in most reservoirs, leaving substantial hydrocarbon volumes accessible exclusively through advanced recovery methods.

Thermal, chemical, and gas injection EOR technologies extend productive field life by an additional 5-25 percentage points of recovery factor, depending on reservoir type and method employed. There are over 100 commercial CO2-EOR projects concentrated in formations such as the West Texas Permian Basin, where the proven technology stack and favorable geology have delivered sustained incremental production. This irreversible transition from primary to enhanced recovery, particularly in the United States, Canada, China, the Middle East, and Latin America, is generating compulsory, multi-decade EOR investment commitments from both independent and national oil companies.

CO2-EOR and CCUS Convergence Creating Dual-Revenue Project Economics

The integration of CO2-based Enhanced Oil Recovery with Carbon Capture, Utilization, and Storage infrastructure is reshaping EOR project economics globally, creating a powerful growth catalyst that simultaneously serves hydrocarbon production and climate regulatory objectives. Under the U.S. Inflation Reduction Act (IRA) and the associated Section 45Q tax credit, which provides up to US$ 85 per tonne for permanently sequestered CO2 used in EOR, operators receive a dual revenue stream comprising both incremental oil production value and carbon management credits.

Occidental Petroleum has been the most visible pioneer of this model: in February 2024, the company announced plans to bring online approximately 60 wells in the Permian Basin using CO2 sourced from its Stratos Direct Air Capture (DAC) hub, targeting production additions of approximately 4,000 barrels per day initially, scaling to approximately 12,000 barrels per day by 2026. The U.S. Department of Energy (DOE) has additionally committed a US$ 650 million grant toward Occidental's second DAC facility in South Texas, signaling durable federal support for CO2-EOR-CCUS integration as a commercially bankable energy and climate strategy.

Market Restraints

High Capital and Operational Expenditure Requirements Limiting Market Accessibility

Enhanced Oil Recovery projects, particularly thermal methods involving steam injection infrastructure and CO2 supply chain development, require substantial upfront capital investment, which constrains deployment, especially in price-volatile oil market conditions. Steam injection EOR requires extensive wellbore installation, procurement of high-pressure steam generators, and surface facility development.

According to the U.S. Energy Information Administration (EIA), EOR break-even oil prices typically range from US$ 35 to US$ 70 per barrel, depending on the method and geography. Sustained oil price downturns, as witnessed during 2015-2016 and the 2020 COVID-19 pandemic price collapse, can render EOR project economics unviable, leading to project deferrals and capital reallocation, meaningfully suppressing near-term market growth during periods of energy price volatility.

Environmental Regulations and Water Management Challenges Constraining Chemical EOR

Chemical EOR, including polymer, surfactant, and alkaline-surfactant-polymer (ASP) flooding, faces growing regulatory scrutiny over the environmental fate of injected chemical additives in subsurface aquifers and produced water streams. Regulations enforced by the U.S. Environmental Protection Agency (EPA) under the Safe Drinking Water Act (SDWA) and Underground Injection Control (UIC) program, as well as analogous environmental frameworks in the European Union and Canada, impose stringent requirements on subsurface chemical injection activities.

Compliance obligations for chemical disposal, produced water treatment, and secondary containment impose high operational costs that erode project net present value, dampening the adoption pace of chemical EOR methods in regulatory-sensitive geographies.

Market Opportunities

Solar-Assisted Thermal EOR: Decarbonizing Heavy Oil Production at Scale

Solar-assisted Enhanced Oil Recovery represents one of the most strategically differentiated growth opportunities for technology providers and oil producers seeking to reduce the carbon intensity and fuel cost of steam-driven thermal EOR operations. Conventional steam injection is predominantly powered by natural gas combustion, a process that generates significant greenhouse gas emissions and is subject to volatile energy costs. Solar EOR replaces or supplements natural gas-fired steam generation with concentrating solar thermal (CST) systems, dramatically reducing fuel consumption and direct CO2 emissions from EOR operations.

The Abu Dhabi National Oil Company (ADNOC) deployed the world's largest solar-powered EOR project at the Miraah Solar Plant in Oman through its GlassPoint Solar partnership, a facility that generates 1,021 MW of solar thermal energy and is designed to produce 6,000 tonnes of steam per day for Petroleum Development Oman's oilfield operations. With oil-producing nations across the Gulf Cooperation Council (GCC) committed to net-zero operational emissions targets and abundant solar irradiation, solar-assisted thermal EOR is positioned for rapid commercial-scale-up. Companies that integrate solar EOR solutions into their technology portfolios will benefit from both differentiated project economics and regulatory alignment across climate-conscious producing regions through 2033 and beyond.

AI-Driven Smart EOR and Digital Reservoir Management Unlocking Efficiency Gains

The integration of Artificial Intelligence (AI), real-time sensor networks, and advanced digital reservoir modeling into EOR operations represents a transformational opportunity for service companies and operators to optimize project performance, reduce operational costs, and improve incremental recovery rates. Traditional EOR design relies on static reservoir characterization and infrequent laboratory analysis, limiting adaptive responses to reservoir heterogeneity during injection operations.

AI-powered smart EOR platforms enable continuous dynamic modeling of fluid mobility fronts, injection pressure optimization, and real-time chemical dosing adjustments, improving recovery efficiency. Industry data indicates that advanced polymer flooding techniques, combined with AI optimization, can increase recovery rates by up to 15% compared to conventional injection methods.

Halliburton and Chevron deployed an intelligent fracturing system in the Colorado shale in June 2025, integrating Chevron's hydraulic stimulation with Halliburton's ZEUS IQ platform for enhanced reservoir contact, exemplifying the industry's accelerating investment in technology-driven recovery optimization. The U.S. DOE's Office of Fossil Energy and Carbon Management has directed funding toward AI-assisted subsurface monitoring programs, creating a policy-backed innovation environment that will substantially expand smart EOR's commercial adoption over the forecast period.

Category-wise Analysis

Technology Type Insights

Thermal EOR is the dominant technology segment, accounting for approximately 35% of the global enhanced oil recovery market revenue. Thermal methods, primarily steam injection, cyclic steam stimulation (CSS), and in-situ combustion, are the most widely deployed EOR technologies globally, uniquely suited for the large volumes of heavy and extra-heavy crude oil reserves concentrated in Canada's Alberta oil sands, China's Liaohe and Shengli fields, Venezuela, and California.

By introducing heat into the reservoir, steam injection reduces crude oil viscosity by several orders of magnitude, enabling heavy oils with viscosities exceeding 1,000 centipoise to flow freely to production wells, delivering recovery factor improvements of up to 30% above primary production, as demonstrated in PetroChina's large-scale cyclic steam and steam flooding programs. The global stock of heavy oil and bitumen, estimated by the United States Geological Survey (USGS) at over 1 trillion barrels of technically recoverable resources, ensures the long-term feedstock base that sustains thermal EOR's market leadership across the forecast period.

Application Insights

Onshore is the dominant application segment, accounting for approximately 72% of the global enhanced oil recovery market revenue. The overwhelming majority of commercially operating EOR projects are located in onshore fields, which benefit from significantly lower infrastructure costs, more accessible drilling environments, simpler deployment of injection well networks, and established regulatory and operational frameworks relative to offshore equivalents. North America's Permian Basin, San Joaquin Valley, and Midcontinent fields; the Middle East's supergiant carbonate reservoirs; China's mature onshore basins; and Canada's Alberta heavy oil belt collectively constitute the primary demand base for onshore EOR investment.

The high prevalence of mature onshore fields with low primary recovery factors, many of which extract less than 30% of the original oil in place, sustains a persistent economic incentive for onshore EOR deployment. Furthermore, the operational versatility of onshore fields in trialing multiple sequential EOR methods across different reservoir zones makes them the preferred laboratory and commercial proving ground for developing new EOR technologies.

Regional Analysis

North America Enhanced Oil Recovery Trends & Insights

North America is the dominant regional market for enhanced oil recovery, accounting for approximately 40% of global market revenue, anchored by the world's most extensive base of operating EOR projects in the United States and Canada. The U.S. Permian Basin hosts over 100 commercial CO2-EOR operations, the highest concentration globally, benefiting from naturally occurring CO2 deposits in the Bravo Dome and McElmo Dome formations that historically provided low-cost CO2 supply. The U.S. 45Q tax credit under the Inflation Reduction Act (IRA), which provides up to US$ 85 per tonne for CO2 used in EOR and permanently sequestered, is fundamentally improving CO2-EOR project returns and attracting new capital commitments across the region.

Canada contributes substantially through its thermal EOR operations targeting the Alberta oil sands, where Steam-Assisted Gravity Drainage (SAGD) is the dominant recovery method for bitumen production. The Alberta Energy Regulator (AER) oversees one of the most comprehensive regulatory frameworks for in-situ oil sands thermal production. Canada's federal government is additionally supporting carbon capture investment through the Investment Tax Credit (ITC) for Carbon Capture, Utilization and Storage announced in Budget 2022, directly enhancing the economic case for CO2-EOR alongside existing thermal operations. The presence of globally leading EOR service providers, including Halliburton, SLB (Schlumberger), and Baker Hughes, all headquartered or substantially operating in North America, gives the region a decisive technological and commercial leadership advantage.

Europe Enhanced Oil Recovery Trends & Insights

Europe represents a mature yet innovation-focused regional market for Enhanced Oil Recovery, characterized by aging offshore and onshore field infrastructure, robust environmental regulatory frameworks, and strong national energy security imperatives that drive mature field optimization. The North Sea, shared between the United Kingdom, Norway, Denmark, and the Netherlands, hosts Europe's most significant EOR activity, with mature platforms deploying water injection, polymer flooding, and low-salinity water injection techniques to arrest production decline. According to the Oil and Gas Authority (now NSTA, North Sea Transition Authority) in the U.K., enhanced recovery from existing fields is a strategic national priority within the North Sea Transition Deal, which commits to maximizing economic recovery while progressing toward net-zero operations by 2050.

Norway's Equinor has operated the Sleipner CO2 injection project, the world's first industrial-scale offshore CO2 storage project, since 1996, establishing a proven template for offshore CO2-EOR and sequestration integration. Germany's onshore oil industry is deploying chemical EOR methods in the Molasse and North German Basins, in mature fields. The European Commission's Innovation Fund and Horizon Europe research program are directing investment toward low-carbon EOR methods, including solar-assisted steam generation, bio-surfactant flooding, and AI-driven reservoir management, reinforcing Europe's position as a center for sustainable EOR technology development.

Asia Pacific Enhanced Oil Recovery Trends & Insights

Asia Pacific is the fastest-growing regional market for Enhanced Oil Recovery, propelled by China's massive heavy oil reservoir base, India's mature onshore field revitalization programs, and escalating energy security imperatives across the broader region. China is the single largest national market for thermal EOR in the world, with PetroChina and Sinopec operating large-scale steam flooding and in-situ combustion programs across the Liaohe, Shengli, and Daqing oilfields, fields where conventional recovery has declined significantly from peak production periods.

China National Petroleum Corporation (CNPC) has demonstrated recovery factor improvements of up to 30% through integrated thermal EOR in heavy oil formations, establishing a domestic model for large-scale government-backed mature field optimization.

India's ONGC (Oil and Natural Gas Corporation) has been actively expanding polymer and surfactant-based chemical EOR pilot programs in Cambay Basin and Rajasthan mature fields, supported by the Ministry of Petroleum and Natural Gas's Production Enhancement programs targeting increased oil recovery from aging domestic reserves. Japan contributes through advanced engineering and process technology development, with institutions including the Japan Oil, Gas and Metals National Corporation (JOGMEC) funding EOR research programs for offshore and unconventional reservoirs. Indonesia, Malaysia, and Vietnam, ASEAN nations with extensively mature offshore oil fields, are accelerating EOR deployment with technical support from international service companies and national oil company partnerships, making Southeast Asia a strategically significant growth sub-region through 2033.

Competitive Landscape

The global Enhanced Oil Recovery market exhibits a moderately consolidated competitive structure, with a tier of dominant supermajor oil and gas operators and internationally leading oilfield services companies commanding the majority of market activity, complemented by a broader tier of regional operators, national oil companies, and specialist chemical EOR service providers. Market leadership is determined by reservoir access, proprietary EOR technology portfolios, project execution capability, and CCUS integration expertise.

Leading oilfield service firms, SLB (Schlumberger), Halliburton, and Baker Hughes, compete through technology differentiation in AI-assisted reservoir management, chemical formulation innovation, and CO2 injection infrastructure. Integrated supermajors including ExxonMobil, Chevron, Shell, and Occidental pursue in-house EOR deployment combined with strategic CCUS co-investments. Emerging competitive models include outcome-based EOR service contracts and technology licensing partnerships aligned with national oil company decarbonization mandates.

Key Market Developments

- In February 2024, Occidental Petroleum announced plans to bring online approximately 60 CO2-EOR wells in the Permian Basin using carbon captured via its Stratos DAC hub, targeting incremental production of 4,000 barrels per day, projected to triple to 12,000 barrels per day by 2026.

- In June 2025, Chevron and Halliburton deployed an intelligent fracturing system in the Colorado shale, integrating Chevron's hydraulic fracturing program with Halliburton's ZEUS IQ platform to enhance reservoir contact and optimize recovery efficiency in mature tight-oil formations.

- In May 2025, ExxonMobil committed US$ 1.5 billion to deep-water Nigeria projects incorporating advanced recovery systems, with investment execution planned between Q2 2025 and 2027, expanding its offshore EOR capability in West Africa.

Companies Covered in Enhanced Oil Recovery Market

- Schlumberger Limited

- Halliburton Company

- Baker Hughes Company

- Chevron Corporation

- Shell plc

- ExxonMobil Corporation

- BP plc

- TotalEnergies SE

- ConocoPhillips

- Occidental Petroleum Corporation

- Petrobras

- China National Petroleum Corporation (CNPC)

- Sinopec

- Linde plc

- TechnipFMC plc

Frequently Asked Questions

The global Enhanced Oil Recovery market is valued at US$ 51.2 Bn in 2026 and is projected to reach US$ 67.8 Bn by 2033, growing at a CAGR of 4.1% during the forecast period. Growth is driven by accelerating depletion of conventional reservoirs, CO2-EOR-CCUS integration incentives, and thermal EOR expansion across major heavy oil producing regions globally.

The primary demand drivers are the global maturation of conventional oil fields, where primary recovery methods extract only 20-30% of original oil in place, and the convergence of CO2-EOR with carbon capture and storage frameworks. The U.S. 45Q tax credit offering up to US$ 85 per tonne for sequestered CO2 in EOR creates dual-revenue project economics that structurally improve EOR investment returns.

Thermal EOR leads the technology type category with approximately 35% of global market revenue, driven by its indispensable role in extracting heavy crude oil from reservoirs in Canada, China, California, and Venezuela. Large-scale deployments by PetroChina using cyclic steam stimulation in the Liaohe and Shengli oilfields have demonstrated up to 30% recovery factor improvements, underpinning the segment's market leadership.

North America dominates the global Enhanced Oil Recovery market with approximately 35-40% of total revenue, anchored by over 100 commercial CO2-EOR projects in the U.S. Permian Basin, generous IRA 45Q tax credits, Canada's extensive Alberta oil sands SAGD operations, and the presence of globally leading EOR service companies including SLB, Halliburton, and Baker Hughes.

The most significant emerging opportunity is the commercialization of AI-driven smart EOR and solar-assisted thermal EOR. AI optimization delivers recovery rate improvements of up to 15%, while solar thermal EOR, as demonstrated by the 1,021 MW Miraah Solar Plant in Oman, dramatically reduces fuel costs and carbon intensity of steam injection operations, enabling oil producers in GCC countries to meet net-zero operational targets while sustaining EOR productivity.

The global Enhanced Oil Recovery market is led by Schlumberger Limited (SLB), Halliburton Company, Baker Hughes Company, Occidental Petroleum Corporation, ExxonMobil Corporation, Chevron Corporation, Shell plc, BP plc, TotalEnergies SE, ConocoPhillips, Petrobras, China National Petroleum Corporation (CNPC), Sinopec, Linde plc, and TechnipFMC plc, among others.