- Sporting Goods & Equipment

- Treadmill Ergometer Market

Treadmill Ergometer Market Size, Share, and Growth Forecast 2026 - 2033

Treadmill Ergometer Market by Product Type (Manual Treadmill Ergometer, Motorized Treadmill Ergometer), Application (Cardiac Rehabilitation, Sports Training, Fitness & Wellness, Medical Diagnostics), End User (Hospitals, Rehabilitation Centers, Gyms & Fitness Centers, Home Care), Distribution Channel (Direct Sales, Distributors, Online), and Regional Analysis, 2026 - 2033

Treadmill Ergometer Market Size and Trend Analysis

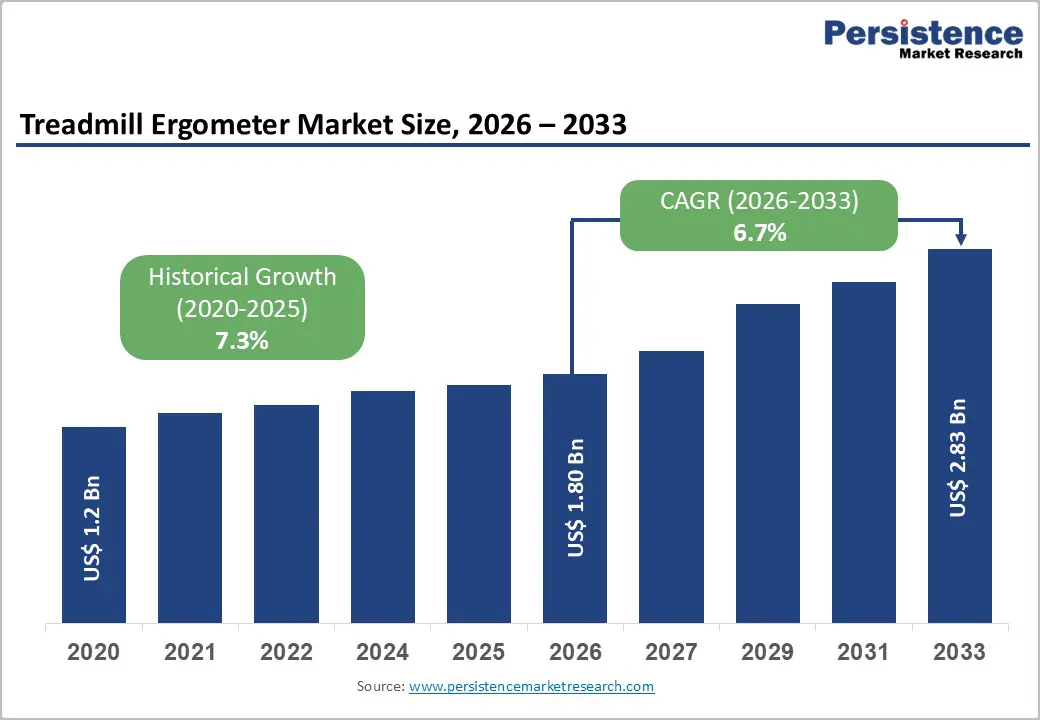

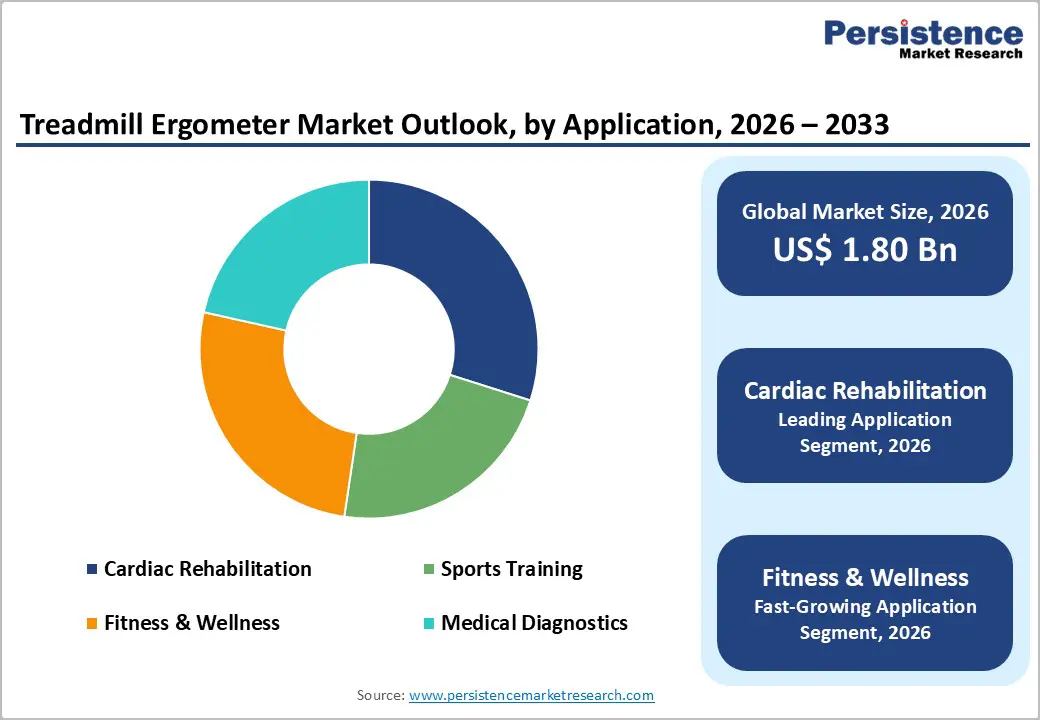

The global treadmill ergometer market is expected to be valued at US$ 1.80 billion in 2026 and projected to reach US$ 2.83 billion by 2033, registering a CAGR of 6.7% between 2026 and 2033.

The rising global cardiovascular diseases, expanding institutional investment in rehabilitation infrastructure, and deepening consumer adoption of structured fitness monitoring. Regulatory endorsement of stress-testing protocols by bodies such as the American Heart Association (AHA) and European Society of Cardiology (ESC) further reinforces procurement volumes across hospitals and specialist cardiology centres globally.

Key Industry Highlights:

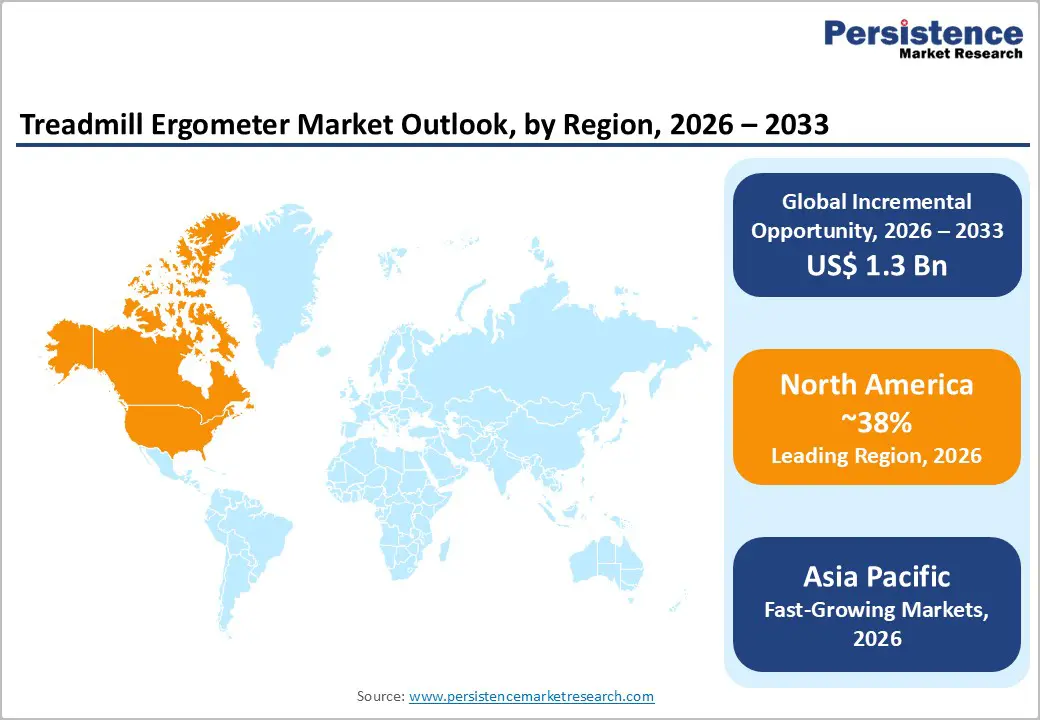

- Leading Region: North America commands approximately 38% of global revenue, anchored by high cardiovascular disease prevalence, mature cardiac rehabilitation reimbursement frameworks, and a concentrated base of leading clinical and sports performance equipment manufacturers.

- Fastest Growing Region: Asia Pacific is projected to expand at a CAGR above 8.5% through 2033, driven by accelerating public healthcare capital investment in China and India, rising chronic disease incidence, and rapid commercial fitness sector expansion.

- Leading Category: The Motorized Treadmill Ergometer segment dominates with a 72.0% share, secured by its mandatory role in clinically validated stress-test and cardiac rehabilitation protocols endorsed by leading cardiology guideline bodies.

- Fastest Growing Application Category: The Fitness & Wellness application segment leads growth, fuelled by the commercial gym sector's post-pandemic investment surge, mainstreaming of performance monitoring among recreational athletes, and rising consumer demand for quantified health data.

- Key Opportunity: Integration of AI-powered diagnostics and digital health connectivity represents the most actionable opportunity, as hospitals and fitness operators seek equipment interfacing with EHR systems and performance analytics platforms for recurring service revenue.

Market Dynamics

Drivers - Rising Global Burden of Cardiovascular Disease Fuelling Clinical Procurement

The rise in cardiovascular disease incidence worldwide, directly expands the addressable patient base for stress testing and cardiac rehabilitation equipment. According to the World Health Organization (WHO), cardiovascular conditions account for approximately 32% of all global deaths annually, creating a structurally non-discretionary demand pool for diagnostic-grade treadmill ergometers across hospitals.

Hospitals and rehabilitation centres respond to this epidemiological pressure by upgrading diagnostic infrastructure, with treadmill stress-test systems occupying a central position in standard cardiology departments. Policy frameworks in North America and Western Europe that mandate exercise electrocardiography as a frontline cardiac diagnostic tool further guarantee recurring institutional spend, insulating the Treadmill Ergometer market from macroeconomic volatility and reinforcing long-term procurement visibility.

Expansion of Professional Sports Science and Human Performance Monitoring

The professionalisation of athlete monitoring across elite and semi-elite sports programmes represents a high-value structural catalyst accelerating treadmill ergometer market growth beyond its traditional clinical base. Sports federations, national Olympic committees, and university athletic departments now deploy laboratory-grade treadmill ergometers as standard VO2 max and lactate threshold testing tools, with leading institutions reporting equipment replacement cycles as short as four to six years.

The increasing adoption of biomechanical gait analysis software which treadmill ergometers increasingly support as an embedded or peripherally connected feature broadens the unit value proposition and justifies premium procurement budgets. This dynamic is particularly pronounced across Germany, Japan, Australia, and the United States, where sports science infrastructure spending receives both public and private institutional backing through national performance agencies.

Restraints - High Capital Expenditure and Maintenance Costs Limiting Penetration in Price-Sensitive Markets

Medical-grade and research-grade treadmill ergometers carry acquisition costs that frequently range between US$ 8,000 and US$ 35,000 per unit, representing a significant capital commitment that effectively excludes under-resourced healthcare providers in emerging economies. Maintenance obligations including motor servicing, belt replacement, and electronic calibration add recurring costs that small clinics and community rehabilitation centres struggle to absorb within constrained equipment budgets.

This cost structure creates a two-tier market where premium products circulate predominantly among well-capitalised hospital systems and elite sports institutes, while lower-acuity providers default to basic alternatives or defer replacement cycles. The consequence is a ceiling on addressable volume in Latin America, Sub-Saharan Africa, and parts of South and Southeast Asia, where healthcare capital expenditure per capita remains materially below the required threshold.

Intensifying Competition from Alternative Cardiopulmonary Exercise Testing Modalities

Cycle ergometers and rowing ergometers increasingly compete with treadmill-based platforms in both clinical stress-testing and sports performance assessment environments, particularly for patient populations where treadmill safety concerns arise. As reported by clinical guideline committees including the European Society of Cardiology (ESC), cycle ergometers are preferred for approximately 30-40% of cardiac stress tests in European clinical settings due to lower fall-risk profiles and easier ECG electrode attachment.

This substitution pressure constrains the Treadmill Ergometer market's ability to capture incremental clinical volume, even as the overall cardiopulmonary exercise testing category expands. Vendors that fail to differentiate treadmill ergometers through superior data integration, safety engineering, or multi-modal compatibility risk ceding share to cycle-based platforms among procurement decision-makers who evaluate equipment on protocol versatility rather than category loyalty.

Opportunities - Integration of Digital Health Ecosystems and AI-Powered Diagnostic Analytics

The convergence of treadmill ergometer hardware with cloud-based electronic health record platforms and AI-driven diagnostic analytics constitutes the single most transformative commercial opportunity available to manufacturers between 2026 and 2033. Vendors that embed real-time data streaming, remote monitoring capability, and machine-learning-assisted interpretation into their ergometer platforms can reposition their products from one-time capital purchases to recurring software-and-service revenue streams, fundamentally improving margin profiles.

According to the World Health Organization (WHO), the global digital health ecosystem is expanding at a CAGR exceeding 15%, and treadmill ergometer suppliers integrating seamlessly with this stack stand to capture disproportionate institutional upgrade budgets. Manufacturers should prioritise open-API architectures and HL7 FHIR interoperability certifications to avoid lock-out from hospital IT procurement frameworks, where first-mover integration deals create durable multi-year switching costs.

Emerging Market Healthcare Infrastructure Investment Creating New Volume Pools

Government-led healthcare infrastructure expansion programmes across India, China, Brazil, and Southeast Asia are creating a rapidly widening addressable market that treadmill ergometer manufacturers have historically underserved due to price point and distribution constraints. Public healthcare capital expenditure across Asia Pacific economies, per World Bank data, grew at an average 8-10% annually through the early 2020s, with the trajectory expected to continue amid aging-population pressures.

Manufacturers developing tiered product architectures offering clinically validated but cost-optimised configurations priced below US$ 5,000 can unlock procurement from district hospitals, government rehabilitation centres, and public sports academies representing tens of thousands of placement opportunities. Partnering with established regional distributors who hold existing relationships with public-sector procurement agencies is critical, as tender framework inclusion delivers durable early-mover advantages within government specification standards.

Category-wise Analysis

Product Type Insights

The Motorized Treadmill Ergometer segment accounts for 72.0% of the global market in 2026, equivalent to US$ 1.30 billion, establishing it as the uncontested dominant product category across clinical and commercial channels. Motorized platforms lead because they deliver controlled, reproducible speed and gradient protocols required by ACC/AHA-endorsed stress tests, including the Bruce Protocol and Modified Bruce Protocol, anchoring institutional demand within this segment.

The Manual Treadmill Ergometer segment is the fastest growing product type, propelled by renewed interest in low-cost, power-independent rehabilitation applications and the expanding home-fitness consumer base seeking maintenance-free equipment. Manual platforms are gaining traction in home care and community fitness contexts where power consumption, footprint, and total cost of ownership become decision-relevant, signalling a clear entry-level whitespace warranting dedicated product line investment.

Application Insights

The Cardiac Rehabilitation segment holds 34.0% of the global Treadmill Ergometer market in 2026, equivalent to US$ 0.61 Billion, reflecting its foundational role in the clinical use case that originally defined this category. Exercise-based rehabilitation following myocardial infarction, heart failure, or cardiac surgery is clinically mandated and reimbursable across North America, Europe, and East Asia, with guideline-directed programmes reducing hospital readmissions by 25-30%.

The Fitness & Wellness segment is the fastest growing application, powered by the post-pandemic normalisation of preventive health monitoring, proliferation of commercial fitness facilities incorporating clinical-grade assessment tools, and rising consumer willingness to pay for quantified performance data. This momentum advises manufacturers to maintain dual-channel portfolios retaining clinical-grade configurations for healthcare procurement while developing wellness-positioned variants tailored to digitally integrated fitness-centre buyers.

End-user Insights

Hospitals account for 40.0% of the global Treadmill Ergometer market in 2026, equivalent to US$ 720 million, consolidating their position as the primary institutional demand engine across the industry. Hospitals concentrate the diagnostic, stress-testing, and cardiac rehabilitation functions that generate the highest-volume procurement decisions, with an estimated 80% of formal exercise stress tests globally conducted within hospital cardiology departments or affiliated outpatient cardiac diagnostic facilities.

Gyms & Fitness Centers represent the fastest growing end-user segment, fuelled by the commercial fitness industry's post-pandemic recovery, integration of fitness assessment services into gym membership offerings, and the trend toward data-driven personal training programmes requiring ergometer-grade measurement. Manufacturers should build sales capabilities tailored to commercial fitness buyers including flexible financing, digital connectivity, and premium-fitness brand positioning to capture share in this expanding demand channel.

Distribution Channel Analysis

The Distributors channel accounts for 36.0% of the global Treadmill Ergometer market in 2026, equivalent to US$ 650 million, reflecting the sector's reliance on specialist medical and fitness equipment networks to reach geographically dispersed institutional buyers. More than 60% of hospital capital equipment procurement across markets such as Germany, Japan, and Brazil flows through established distributors holding preferred vendor status within national procurement frameworks.

The online channel is the fast-growing distribution segment, driven by accelerating digital procurement habits of commercial gym operators, home-care buyers, and smaller rehabilitation facilities prioritising price transparency, product comparison, and direct manufacturer engagement. Manufacturers should pursue a hybrid strategy preserving distributor relationships for clinical and enterprise accounts while investing in direct digital commerce capabilities to capture small-institution and consumer-grade transactions migrating online.

Regional Insights

North America Treadmill Ergometer Market Trends and Insights

North America leads the global treadmill ergometer market with an estimated 38% share in 2025, supported by high cardiovascular disease prevalence, robust reimbursement frameworks, and strong adoption of advanced cardiac rehabilitation programs. Continuous investment by leading hospital chains, presence of major manufacturers, and integration of AI-enabled connected fitness solutions across gyms and home-care settings sustain regional leadership.

- U.S. Treadmill Ergometer Market Size

The United States accounts for nearly 84% of the North American market in 2025, underpinned by over 6,120 hospitals and widespread CMS-reimbursed cardiac rehabilitation. CDC data show about 805,000 Americans suffer a heart attack annually, sustaining demand for stress testing and rehab equipment. Strong presence of Life Fitness, True Fitness, and Woodway USA further reinforces market depth.

Europe Treadmill Ergometer Market Trends and Insights

Europe holds a strong position driven by aging demographics, established cardiac rehab networks, and EU MDR-compliant device adoption. Government-funded healthcare systems support institutional procurement, while rising obesity rates Eurostat notes over 50% of EU adults are overweight boost fitness-segment demand. Smart-gym proliferation and tele-rehabilitation programs across Western Europe are accelerating connected treadmill ergometer adoption.

- Germany Treadmill Ergometer Market Size

Germany holds nearly 22% of the European treadmill ergometer market in 2025, supported by over 1,900 hospitals and one of the world’s most developed cardiac-rehabilitation infrastructures funded under statutory health insurance. Robust presence of manufacturers such as h/p/cosmos and ergoline GmbH strengthens domestic supply, while strong DGSP-aligned sports-medicine practices drive consistent equipment upgrades.

- U.K. Treadmill Ergometer Market Size

The U.K. captures around 16% of European market share in 2025, driven by NHS-supported cardiac rehabilitation programs and rising private-sector fitness investments. The British Heart Foundation reports over 7.6 million people living with heart and circulatory diseases nationwide, sustaining hospital and outpatient demand for stress-testing treadmills, while expanding boutique-gym chains support commercial-grade purchases.

- France Treadmill Ergometer Market Size

France holds approximately 13% of Europe’s market in 2025, anchored by Assurance Maladie-reimbursed cardiac rehabilitation and a network of more than 220 accredited rehab centers. Santé publique France highlights cardiovascular diseases as a leading mortality cause, sustaining hospital procurement, while growing fitness-club penetration surpassing 6 million members drives commercial treadmill ergometer demand.

Asia Pacific Treadmill Ergometer Market Trends and Insights

Asia Pacific is the fast-growing region fueled by rising CVD burden, expanding hospital infrastructure, and surging fitness-club penetration. China, contributing nearly 34% of the regional market, leads adoption through its Healthy China 2030 initiative, growing private-hospital networks, and rising consumer spending on smart home-fitness equipment.

- India Treadmill Ergometer Market Size

India captures roughly 14% of Asia Pacific share in 2025, supported by ICMR estimates that CVDs cause about 28% of all deaths nationwide. Expansion of corporate hospital chains such as Apollo and Fortis, coupled with rising disposable incomes and fitness-club growth over 30,000 gyms operating is accelerating treadmill ergometer demand across both clinical and consumer segments.

- Japan Treadmill Ergometer Market Size

Japan holds nearly 18% of Asia Pacific market share in 2025, driven by its rapidly aging population over 29% aged 65+ per the Statistics Bureau of Japan and a deeply embedded preventive-health culture. Strong hospital infrastructure, MHLW-supported rehabilitation programs, and domestic manufacturers such as Fukuda Denshi sustain consistent equipment upgrades and replacement cycles.

- Southeast Asia Treadmill Ergometer Market Size

Southeast Asia accounts for about 11% of regional market share in 2025, led by Singapore, Thailand, Malaysia, and Indonesia. Rising medical-tourism inflows, expanding private hospital chains, and increasing fitness-club density support equipment demand. WHO notes NCDs cause roughly 74% of regional deaths, prompting governments to expand cardiac rehabilitation capacity and modernize stress-testing infrastructure.

Competitive Landscape

The Treadmill Ergometer market operates as a moderately fragmented competitive environment, where a cohort of established medtech and fitness equipment majors co-exists with a long tail of regional and application-specialist vendors. Scale advantages accrue primarily to diversified healthcare equipment companies that leverage cross-portfolio hospital relationships to drive treadmill ergometer placement alongside broader cardiology system investments and integrated diagnostic suites.

Differentiation-focused competitors compete on engineering precision, biomechanical performance, and integration depth with physiological measurement platforms rather than price. Dominant strategic themes shaping competitive posture in 2025-2026 include software and connectivity investment, clinical validation partnerships, geographic expansion into emerging healthcare channels, and the disruptive shift toward equipment-as-a-service and subscription-based software licensing models.

Key Developments:

- In January 2025, GE HealthCare announced the expansion of its cardiology diagnostics portfolio with an upgraded treadmill stress-testing platform featuring integrated AI-assisted ECG interpretation, targeting cardiac catheterisation laboratory upgrades across North American hospital systems with a planned Q2 2025 commercial rollout.

- In March 2025, TechnoGym unveiled a next-generation connected treadmill ergometer series at the FIBO international fitness trade show, incorporating real-time biometric data streaming and personalised training algorithm capabilities designed to serve both elite sports performance centres and premium commercial gym operators globally.

- In October 2024, Woodway USA formalised a distribution partnership with a major Asia-Pacific sports medicine equipment network to accelerate market entry across South Korea, Australia, and Singapore, addressing identified whitespace in high-performance sports science laboratory infrastructure in the region.

Treadmill Ergometer Market - Key Insights & Details

| Key Insights | Details |

|---|---|

| Historical Market Value (2020) | US$ 1.32 Billion |

| Current Market Value (2026) | US$ 1.80 Billion |

| Projected Market Value (2033) | US$ 2.83 Billion |

| CAGR (2026 - 2033) | 6.7% |

| Leading Region | North America (38%) |

| Dominant Product Type | Motorized Treadmill Ergometer (72.0%) |

| Top-ranking Application | Cardiac Rehabilitation (34.0%) |

| Top-ranking End User | Hospitals (40.0%) |

| Top-ranking Distribution Channel | Distributors (36.0%) |

| Incremental Opportunity (2026 - 2033) | US$ 1.03 Billion |

Companies Covered in Treadmill Ergometer Market

- GE HealthCare

- Philips Healthcare

- Schiller AG

- COSMED

- Woodway

- Trackmaster

- Noraxon

- Lode BV

- h/p/cosmos

- Mortara Instrument

- Cortex Biophysik

- TechnoGym

- Life Fitness

- BH Fitness

- ICON Health & Fitness

- Cardiocom

- Quinton Cardiology Systems

- Precor

- Star Trac

- Seca GmbH

Frequently Asked Questions

The global Treadmill Ergometer market is valued at US$ 1.80 Billion in 2026 and projected to reach US$ 2.83 Billion by 2033, expanding at a CAGR of 6.7%.

Rising global cardiovascular disease burden-accounting for 32% of global deaths-and accelerating professionalisation of sports science and performance monitoring are the principal demand drivers.

The Motorized Treadmill Ergometer segment holds 72.0% share in 2026, anchored by its mandatory role in clinically validated stress-test protocols like the Bruce Protocol.

North America dominates with approximately 38% of global revenue in 2026, supported by high cardiovascular disease prevalence and mature cardiac rehabilitation reimbursement frameworks.

Integration of AI-powered diagnostic analytics and HL7 FHIR-compliant cloud connectivity, enabling manufacturers to transition from one-time capital sales to recurring software-and-service revenue streams.

Leading players include GE HealthCare, Philips Healthcare, Schiller AG, TechnoGym, Woodway, COSMED, h/p/cosmos, Life Fitness, ICON Health & Fitness, and Lode BV.