- Advanced Materials

- Coal Bed Methane Market

Coal Bed Methane Market Size, Share, and Growth Forecast 2026 - 2033

Coal Bed Methane Market by Technology (Hydraulic Fracturing, Horizontal Drilling, CO2 Sequestration), End-User (Power Generation, Residential, Commercial, Industrial, Transportation), and Regional Analysis for 2026 - 2033

Coal Bed Methane Market Size and Trend Analysis

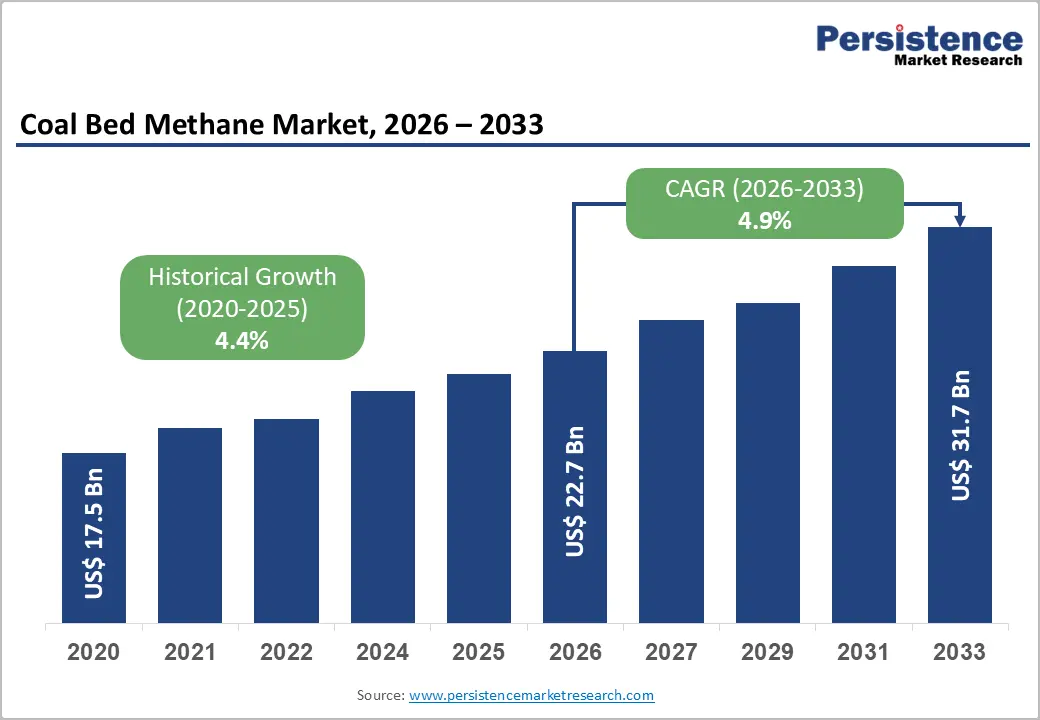

The global coal bed methane market size is valued at US$ 22.7 billion in 2026 and is projected to reach US$ 31.7 billion by 2033, growing at a CAGR of 4.9% between 2026 and 2033.

This sustained expansion is driven by rising global natural gas demand as nations seek lower-carbon alternatives to coal and oil, accelerating unconventional gas development programs in China, India, and Australia, and the growing deployment of advanced extraction technologies including multi-stage hydraulic fracturing and horizontal drilling, that have materially improved CBM well productivity and economic viability.

Key Industry Highlights:

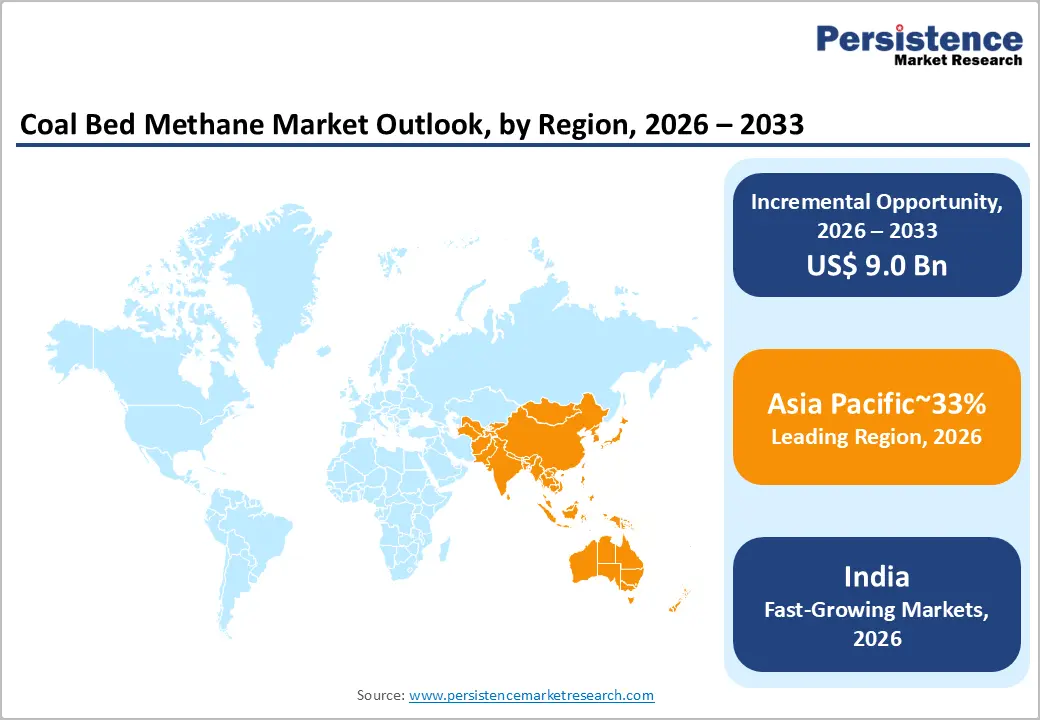

- Leading Region: Asia Pacific leads the global Coal Bed Methane market with 33% share driven by China's record Q1 2025 CBM output growth, Australia's world-class CBM-to-LNG infrastructure in the Surat and Bowen Basins, and India's commercial CBM launch at Jharia by ONGC targeting 0.4 million m³/day by 2027.

- Fastest Growing Region: Asia Pacific is simultaneously the fastest-growing region, with China growing at 6.6% CAGR, India at 6.5% CAGR, and Indonesia, holding an estimated 453 Tcf of in-place CBM gas, positioned to emerge as a major new production frontier once regulatory frameworks for commercial CBM development are finalized.

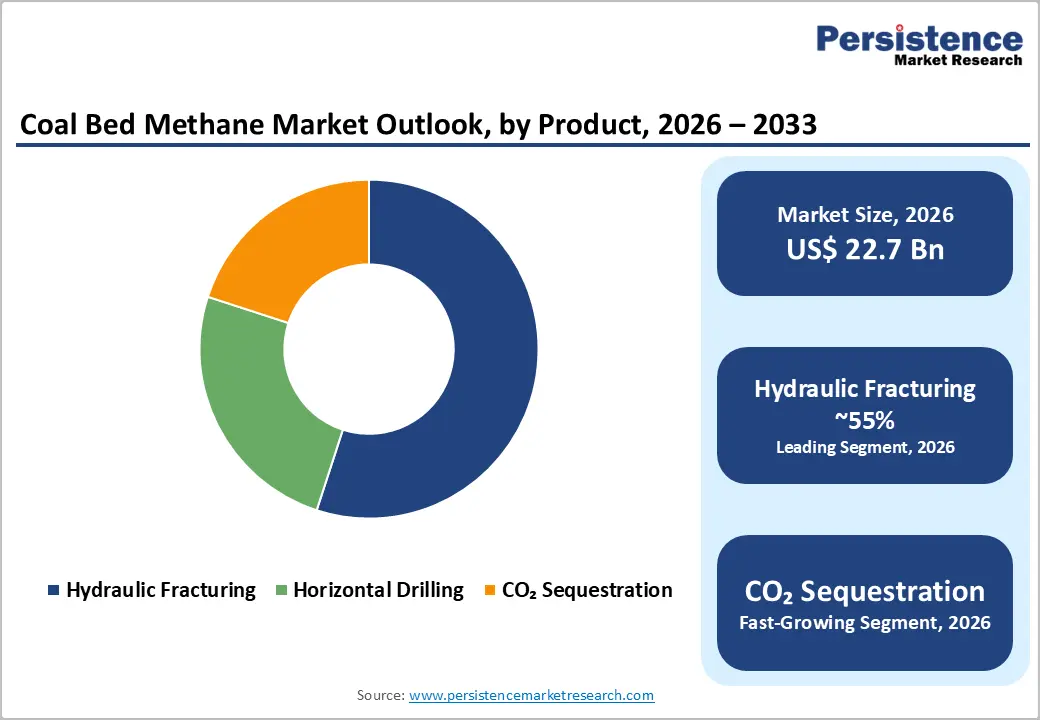

- Dominant Segment: Hydraulic fracturing is dominant and approximately accounts for 55% of global CBM market revenue, reflecting its non-optional role in stimulating low-permeability coal seams to achieve commercial gas flow rates, supported by research confirming horizontal well fracturing as the most effective technical approach for unconventional coalbed methane development.

- Fastest Growing Segment: CO2 Sequestration (ECBM) is the fastest-growing technology segment, driven by ONGC's MECBM microbial enhancement program (April 2025), IPCC recognition of ECBM as a viable carbon mitigation pathway, and growing interest from CBM operators in accessing carbon credit revenues alongside enhanced gas production through CO2 injection into coal seams.

- Key Opportunity: The CO2-Enhanced CBM (ECBM) sequestration technology opportunity, capable of improving methane recovery by up to 90% while permanently sequestering CO2 underground, positions CBM operators to simultaneously access carbon credit markets and enhance production economics, attracting ESG-aligned capital investment and qualifying for government CCS incentives under the U.S. Inflation Reduction Act's 45Q tax credit and equivalent EU programs.

DRO Analysis

Drivers

Rising Global Natural Gas Demand and Energy Security Imperatives Propelling CBM Utilization

The global energy transition, while accelerating the growth of renewables, has simultaneously reinforced the strategic importance of natural gas as a reliable baseload and transition fuel capable of displacing coal in power generation while complementing intermittent renewable energy sources. Coal bed methane, as a domestically extractable unconventional natural gas resource, is increasingly recognized by governments in Asia Pacific, Europe, and North America as a critical energy security lever. China's National Energy Administration (NEA) has actively promoted CBM development through successive Five-Year Plans for the coalbed methane industry, targeting domestic production of 10 billion cubic meters (Bcm) annually from surface CBM wells to reduce import dependency.

India's Ministry of Coal has been advancing CBM as a cleaner energy alternative by unlocking coal-bearing basin potential across the country's major coalfields including Jharia, Raniganj, and Sohagpur. In December 2024, Oil and Natural Gas Corporation (ONGC) launched commercial CBM output at Jharia, targeting 0.4 million m³/day of production by 2027, a development that underscores the growing governmental commitment to CBM as a domestic gas supply diversification strategy across the Asia Pacific.

Advanced Extraction Technologies Enhancing CBM Well Economics and Recovery Rates

The commercial viability of coal bed methane extraction has been fundamentally transformed by the widespread adoption of hydraulic fracturing and horizontal drilling technologies, both of which materially improve gas recovery rates, well productivity, and field economics. Hydraulic fracturing applied to CBM wells creates high-conductivity fracture networks within coal seams, dramatically increasing permeability and gas desorption rates from the coal matrix, while horizontal drilling allows a single wellbore to access significantly larger volumes of gas-bearing coal than vertical configurations. Research published in Coal Science and Technology (2025) confirms that horizontal well fracturing stimulation is the most effective technical approach for achieving efficient development of unconventional coalbed methane, particularly in low-permeability seams.

At India Energy Week in February 2024, Seros Energy showcased its CBM exploration leadership, highlighting directional drilling, hydraulic fracturing, and well services capabilities and achieving 10,000+ meters of CBM wells monthly, reflecting the rapid commercialization of advanced drilling technologies in emerging CBM markets. The global hydraulic fracturing market, a critical enabling service sector for CBM development, is projected to grow from US$ 43.3 Bn in 2026 to US$ 83.73 Bn by 2033, reflecting broad industry investment in fracturing services that directly benefit CBM extraction efficiency.

Restraints

Environmental Concerns and Regulatory Pressure on Hydraulic Fracturing Operations

Hydraulic fracturing, the dominant CBM extraction technology, faces significant and growing regulatory and public opposition in multiple jurisdictions due to concerns over groundwater contamination from fracturing fluids, induced seismicity, methane leakage during well completion and production, and surface land disturbance. The European Union's precautionary approach has resulted in hydraulic fracturing moratoriums or outright bans in France, Germany, and the United Kingdom, effectively preventing commercial CBM development in regions with significant coalfield potential.

Even in jurisdictions where fracturing is permitted, increasingly stringent U.S. Environmental Protection Agency (EPA) methane emission regulations, under the Inflation Reduction Act's methane fee provisions, are adding compliance costs and operational complexity for CBM operators, constraining production economics and deterring new project investments in regulated markets.

High Upfront Capital Costs and Long Dewatering Periods Delaying Project Returns

CBM wells require extensive dewatering operations, pumping groundwater out of coal seams to reduce hydrostatic pressure and enable methane desorption, before reaching commercial gas production rates. This dewatering phase can extend from several months to over two years, creating a prolonged period of capital expenditure without meaningful gas revenue that significantly increases project payback periods and financing costs.

The International Energy Agency (IEA) acknowledges that unconventional gas projects, including CBM, carry materially higher upfront development costs compared to conventional gas fields, a financial characteristic that discourages investment from smaller operators and in jurisdictions without supportive fiscal regimes or production-sharing arrangements. In price-volatile natural gas markets, extended dewatering timelines compound the financial risk of CBM project development.

Opportunities

CO2-Enhanced CBM (ECBM) Sequestration: Dual-Benefit Climate and Production Technology

The integration of CO2 sequestration with enhanced coal bed methane (ECBM) recovery represents one of the most technologically promising and strategically significant growth opportunities for the CBM industry over the forecast period. The ECBM process involves injecting captured CO2 into coal seams, where it preferentially adsorbs onto coal matrix surfaces, displacing methane and driving additional gas production, while permanently sequestering the CO2 underground. This dual-benefit mechanism simultaneously enhances methane recovery by up to 90% compared to primary depletion and provides a measurable carbon capture and storage (CCS) pathway that can help CBM operators meet net-zero emission commitments.

In April 2025, India's Oil and Natural Gas Corporation (ONGC), along with partners including Oil India and TERI, introduced MECBM technology that injects nutrient-rich solutions to activate microbial communities within coal seams, enhancing biogenic methane generation in a novel approach related to ECBM principles.

The Intergovernmental Panel on Climate Change (IPCC) has identified ECBM with CO2 sequestration as a technically viable carbon mitigation pathway, with ongoing research and pilot projects in China, Australia, and the United States advancing field-scale implementation. CBM companies that develop ECBM project capabilities will be positioned to access carbon credit revenues alongside gas production income, improving project economics and attracting ESG-aligned investment capital through the forecast period.

CNG Expansion Transportation Sector is a High-Growth End-Use for CBM-Derived Gas

The expanding adoption of Compressed Natural Gas (CNG) as a vehicle fuel in commercial transportation, driven by government fleet mandates, fuel cost advantages over diesel, and mounting pressure to reduce urban air pollution, creates a structurally growing end-use demand stream for CBM-derived gas that is distinct from the dominant power generation segment. China, the world's largest CNG vehicle market with over 7 million CNG vehicles operating on public roads per data from the China Natural Gas Vehicle Network, is progressively integrating CBM production from provinces including Shanxi, Guizhou, and Sichuan into regional CNG refueling supply chains, supporting both rural energy access and urban transportation decarbonization simultaneously.

In India, the Ministry of Petroleum and Natural Gas has aggressively expanded the City Gas Distribution (CGD) network under the Pradhan Mantri Urja Ganga program, with CBM blocks in Jharia and Bokaro positioned to supply gas to adjacent CGD networks for CNG and piped natural gas distribution. The International Gas Union (IGU) identifies CNG for transportation as a rapidly growing global natural gas demand category, particularly in South Asia, Southeast Asia, and Latin America, all regions with significant untapped CBM resources. CBM producers that develop direct offtake agreements with CGD operators and CNG station networks can secure long-term contracted revenue streams while serving the transportation sector's growing demand for clean fuels.

Category-wise Analysis

Technology Insights

Hydraulic fracturing is the dominant technology segment in the Coal Bed Methane market, accounting for approximately 55% of total global CBM market revenue by technology deployment. The dominance of hydraulic fracturing in CBM production reflects its fundamental operational role: coal seams typically exhibit very low natural permeability, often below 1 millidarcy, making hydraulic fracturing an essentially non-optional technology step for achieving commercial gas flow rates from CBM wells. Without fracturing, methane desorption and migration through the coal matrix to the wellbore occurs too slowly for economic production in the majority of global CBM basins.

Multi-stage hydraulic fracturing, combined with advanced proppant selection and fracture design optimization, has significantly improved CBM well initial production rates and estimated ultimate recovery (EUR) across major producing basins in the United States (San Juan, Black Warrior, Powder River), Australia (Bowen, Surat), China (Qinshui, Ordos), and India (Damodar Valley). Research published in Coal Science and Technology (2025) confirms that horizontal well fracturing stimulation represents the current frontier of CBM technology evolution, with integrated fracture modeling and real-time microseismic monitoring enabling operators to achieve materially superior stimulation outcomes compared to conventional vertical well fracturing approaches.

End-user Insights

Power generation is the leading end-use segment in the Coal Bed Methane market, commanding approximately 42% of total global CBM consumption by end-use. Power generation's dominance reflects CBM's superior suitability as a fuel for gas-fired power plants, both open-cycle and combined-cycle configurations, where its high methane content (95-98% CH4 typical specification) and consistent calorific value enable efficient, low-emission electricity generation compared to coal. According to data compiled from industry analyses, power plants accounted for 41.3% of CBM market consumption in 2024, supported by a pipeline of 18.7 GW of upcoming combined-cycle gas turbine (CCGT) capacity globally that specifically targets CBM and domestic natural gas as primary feedstocks.

China's state-owned power generators, including China Energy Investment Corporation (CEIC) and China Huaneng Group, are actively integrating CBM from Shanxi province into gas-fired power plant fuel supply portfolios, with CBM-fired power generation supported under China's national air quality improvement and coal-to-gas switching programs. The segment's structural dominance is sustained by the global energy transition's need for dispatchable gas-fired backup capacity to balance intermittent renewable generation, ensuring CBM's continued relevance in power-sector fuel mixes through 2033.

Regional Analysis

North America Coal Bed Methane Trends & Insights

The United States is the most mature CBM-producing nation globally, with over three decades of commercial production history anchored in prolific basins including the San Juan Basin (Colorado/New Mexico), Black Warrior Basin (Alabama), and Powder River Basin (Wyoming/Montana).

The U.S. Energy Information Administration (EIA) has documented the gradual maturation of legacy CBM production in the San Juan Basin, historically the world's largest single CBM-producing basin, with declining well productivity in older fields prompting operators to apply advanced restimulation and infill drilling techniques to maintain output. CONSOL Energy Inc. and Pioneer Natural Resources represent the U.S. market's leading integrated coal and gas operators, with CONSOL's Buchanan mine in Virginia operating one of the country's most productive coal mine methane drainage and utilization programs. Canada's CBM resources, particularly in Alberta's Horseshoe Canyon formation, continue to be developed by companies including Encana Corporation (Ovintiv Inc.), with CBM contributing to Canada's domestic natural gas supply portfolio.

The U.S. Environmental Protection Agency (EPA) regulates CBM operations under the Clean Air Act and Safe Drinking Water Act (SDWA) frameworks, with Underground Injection Control (UIC) permitting governing hydraulic fracturing operations in CBM wells. The EPA's methane fee under the Inflation Reduction Act, applicable to oil and gas operations including CBM is compelling operators to invest in methane leak detection and repair (LDAR) technologies, adding compliance costs but also incentivizing more efficient gas capture from coal seams.

North America remains the world's largest established CBM market, with sustained investment in technology-driven well performance improvement sustaining the region's production even as focus increasingly shifts to newer frontier basins in Asia Pacific.

Europe Coal Bed Methane Trends & Insights

Europe's CBM market operates in a distinctly challenging regulatory environment, defined by the tension between significant geological resource potential, particularly in Poland, Germany, Czech Republic, and Ukraine, and stringent environmental regulations that restrict hydraulic fracturing in most EU member states. Poland holds the most actively pursued CBM exploration program in Europe, with the Polish Geological Institute (PIG) estimating Poland's CBM resources at approximately 3 trillion cubic meters (Tcm) in-place across the Upper Silesian and Lublin coal basins.

Germany has explored CBM potential in the Ruhr Valley, one of Europe's most historically significant coal mining regions, though hydraulic fracturing restrictions under German water protection laws have constrained commercial development. The European Commission's methane emissions regulation, which entered into force in 2024, specifically targets coal mine methane (CMM) and CBM, mandating monitoring, reporting, and mitigation of methane venting and flaring from coal mines, creating a compliance-driven incentive for CBM capture and utilization.

Ukraine, which holds significant CBM resources in the Donets Basin, remains constrained by geopolitical disruption, while Spain and France have effectively closed their territories to CBM development through hydraulic fracturing prohibitions. Despite these constraints, the EU's REPowerEU Plan, targeting diversification away from Russian natural gas, has renewed policy interest in domestically producible unconventional gas resources including CBM as a medium-term indigenous supply option. The development of advanced non-hydraulic fracturing stimulation techniques, including nitrogen foam fracturing and CO2-based ECBM, may provide a regulatory pathway for CBM development in fracturing-restricted European jurisdictions, representing a long-term market development opportunity.

Asia Pacific Coal Bed Methane Trends & Insights

Asia Pacific is the world's fastest-growing CBM market and largest share accounting 33% of the market, driven by the region's vast coal reserves, estimated to contain some of the world's highest in-place CBM resources, and the growing urgency of energy security diversification, coal mine safety improvement, and domestic gas production augmentation across China, India, Australia, and Indonesia. China is by far the world's most dynamic CBM growth market, having recorded a record output performance in Q1 2025 per industry data, with CNOOC reporting massive reserve additions in the Qinshui and Ordos basins. China's National Energy Administration (NEA) has promoted CBM production as a strategic component of the country's natural gas supply expansion strategy, with Shanxi province alone having commercially recoverable CBM resources estimated at over 8 Tcm.

India is the region's fastest-growing individual CBM market, with the Ministry of Coal advancing CBM across major coalfields and the DGH administering an active CBM block licensing program. ONGC's December 2024 commercial production launch at Jharia, targeting 0.4 million m³/day by 2027, marks a pivotal milestone for India's CBM industry, supported by the April 2025 introduction of MECBM microbial enhancement technology developed with Oil India and TERI.

Australia contributes through a world-class CBM-to-LNG supply chain centered in Queensland's Surat and Bowen Basins, with Santos Limited, Arrow Energy, and Shell's QGC operating large-scale CBM gathering and processing infrastructure supplying the GLNG, APLNG, and QGC LNG export terminals at Gladstone. Indonesia holds an estimated 453 Tcf of in-place CBM gas, one of the world's largest resource endowments, but awaits regulatory certainty to unlock commercial development at scale.

Competitive Landscape

The global coal bed methane market exhibits a moderately consolidated competitive structure, with large integrated energy majors, including ExxonMobil, BP plc, Shell (QGC), Chevron, and ConocoPhillips, competing alongside state-owned enterprises such as PetroChina, China United Coalbed Methane Corporation (CUCBM), and ONGC, and regional specialists including Santos Limited, Arrow Energy, and Great Eastern Energy Corporation (GEECL).

Key competitive differentiators include basin-specific geological expertise, proprietary hydraulic fracturing design capabilities, CBM-to-LNG integration infrastructure, and government relationship advantages in licensing jurisdictions. Emerging competitive trends include joint ventures between international majors and national oil companies for technology transfer, increased focus on ECBM-CCS project development for carbon credit monetization, and digital oilfield technologies for CBM production optimization.

Key Developments:

- In April 2025, ONGC, alongside partners Oil India and TERI, introduced MECBM technology, injecting nutrient-rich solutions to stimulate microbial communities in coal seams, representing a breakthrough approach to biogenic methane enhancement in Indian CBM fields.

- In December 2024, Oil and Natural Gas Corporation (ONGC) launched commercial CBM production at the Jharia coalfield in India, targeting 0.4 million m³/day by 2027, marking a significant milestone in India's domestic unconventional gas development strategy.

Companies Covered in Coal Bed Methane Market

- ExxonMobil

- BP plc

- ConocoPhillips

- Royal Dutch Shell (QGC)

- Chevron Corporation

- PetroChina Company Limited

- China United Coalbed Methane Corporation (CUCBM)

- Santos Limited

- Arrow Energy Pty Ltd.

- Encana Corporation (Ovintiv Inc.)

- AAG Energy Holdings Ltd.

- G3 Exploration Ltd.

- CONSOL Energy Inc.

- Pioneer Natural Resources Company

- Great Eastern Energy Corporation Ltd. (GEECL)

Frequently Asked Questions

The global Coal Bed Methane market is valued at US$ 22.7 Bn in 2026 and is projected to reach US$ 31.7 Bn by 2033, growing at a CAGR of 4.9% during the forecast period. Growth is supported by NGS India's reported global CBM production of 86 BCM (236 MMSCMD) in 2023, with China and India driving the fastest incremental output growth through government-backed unconventional gas development programs targeting domestic energy security.

Rising global natural gas demand and energy security imperatives, with China's NEA targeting 10 Bcm annually from CBM surface wells and India's Ministry of Coal advancing CBM across major coalfields, compelling domestic unconventional gas development are the major factors identified.

Hydraulic fracturing leads the technology category with approximately 55% of global CBM market revenue, driven by its essential operational role in stimulating low-permeability coal seams to achieve commercial gas flow rates. Research published in Coal Science and Technology (2025) confirms that horizontal well fracturing stimulation is the most effective technical approach for efficient CBM development, with multi-stage fracturing enabling materially superior stimulation outcomes in major producing basins across the United States, Australia, China, and India.

Asia Pacific leads the global Coal Bed Methane market, with China recording record CBM output in Q1 2025 and holding over 8 Tcm of commercially recoverable CBM resources in Shanxi province alone.

The most significant opportunity is CO2-Enhanced CBM (ECBM) sequestration, a dual-benefit technology that simultaneously improves methane recovery by up to 90% and permanently sequesters CO2 underground.

The global Coal Bed Methane market is led by Shell (QGC), PetroChina Company Limited, Santos Limited, ExxonMobil, BP plc, ConocoPhillips, Chevron Corporation, China United Coalbed Methane Corporation (CUCBM), Arrow Energy Pty Ltd., ONGC, Ovintiv Inc. (Encana), CONSOL Energy Inc., AAG Energy Holdings Ltd., G3 Exploration Ltd., Great Eastern Energy Corporation Ltd. (GEECL), and Pioneer Natural Resources Company, among others.