- Bulk Chemicals

- CMP Slurry Market

CMP Slurry Market Size, Share, and Growth Forecast 2026 - 2033

CMP Slurry Market by Product Type (Aluminum Oxide, Ceramic, Cerium Oxide, Silica, Others), by Material (Silica Slurries, Ceria, Alumina & Others), by Application (Silicon Wafers, Optical Substrates, Disk-drive Components, Others), and Regional Analysis, 2026 - 2033

CMP Slurry Market Size and Trend Analysis

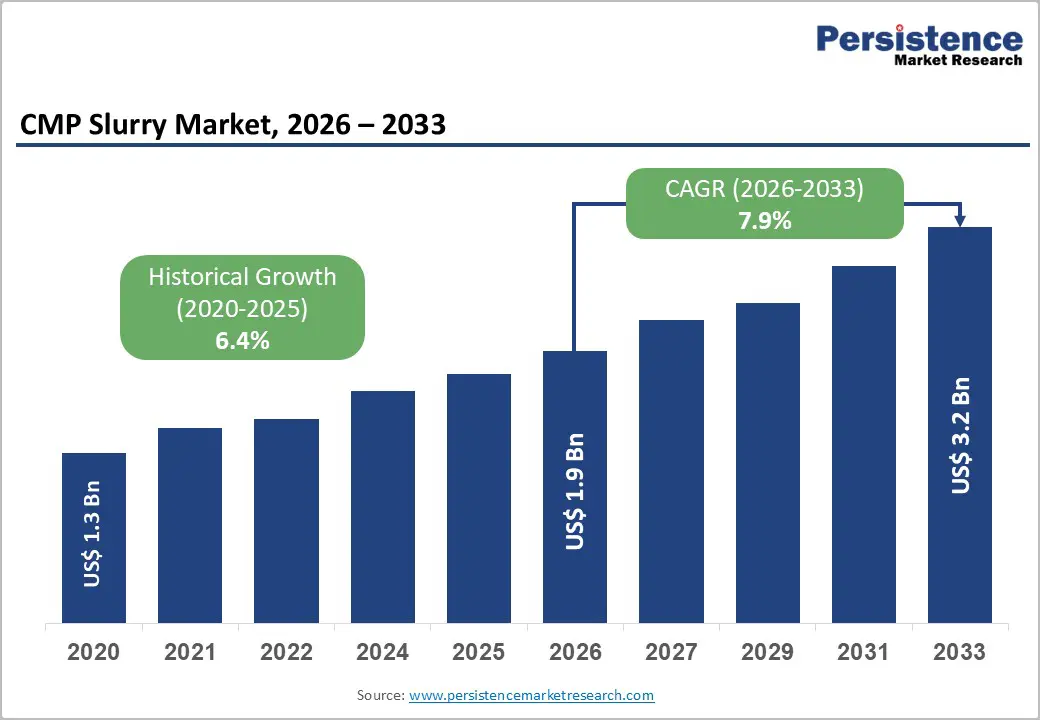

The global CMP slurry market size is likely to be valued at US$ 1.9 billion in 2026 and is expected to reach US$ 3.2 billion by 2033, growing at a CAGR of 7.9% during the forecast period from 2026 to 2033.

This growth is driven by the shift to advanced semiconductor process nodes, the increasing complexity of AI and high-performance computing chip architectures, and rising wafer fabrication investments supported by policies such as the U.S. CHIPS and Science Act and the European Chips Act.

Key Industry Highlights:

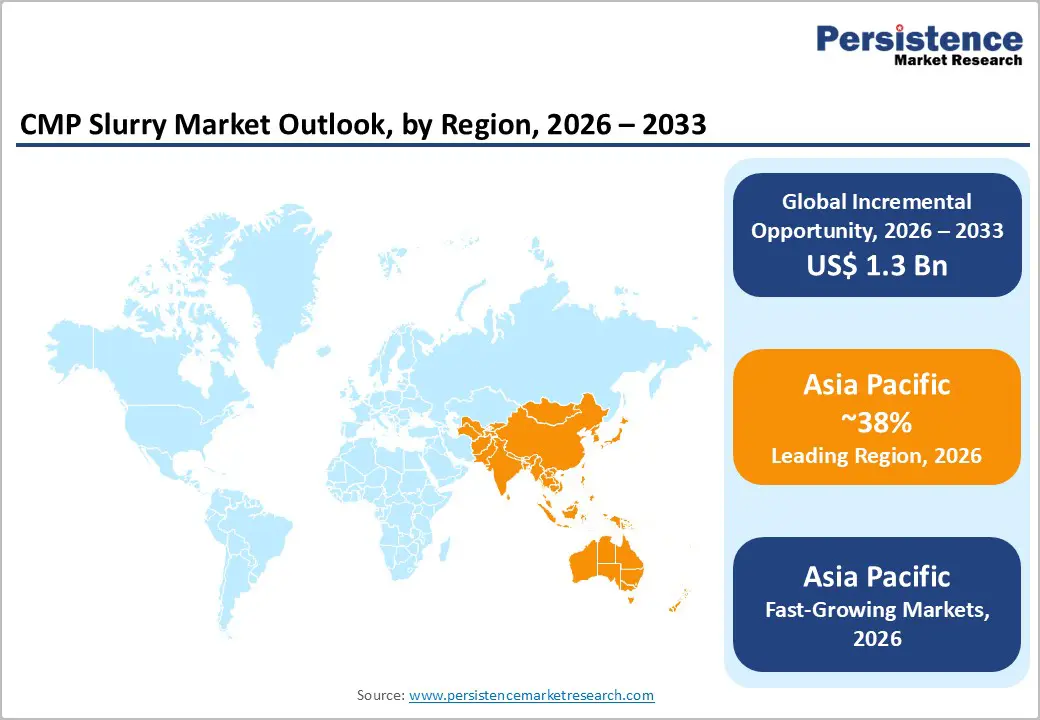

- Leading Region: Asia Pacific leads the global CMP Slurry Market with 38% share, anchored by the dominant fabrication presence of TSMC, Samsung Electronics, and SK Hynix, which collectively account for the majority of sub-5nm advanced-node wafer starts globally, ensuring sustained regional demand leadership through 2033.

- Fastest-Growing Region: Asia Pacific is also the fastest-growing region with a rising CAGR of 9.7%, with China's domestic semiconductor expansion under "Made in China 2025" and India's inaugural fab investments by Tata Electronics and Micron Technology, supported by the Government of India's 50% fiscal incentive program, adding high-growth incremental slurry demand vectors.

- Leading Segment: Silicon Wafers represent the dominant application segment, accounting for approximately 55% of application-based revenue in 2026, driven by SEMI-reported global wafer shipments exceeding 14,197 MSI annually and increasing CMP step-intensity requirements at advanced semiconductor nodes.

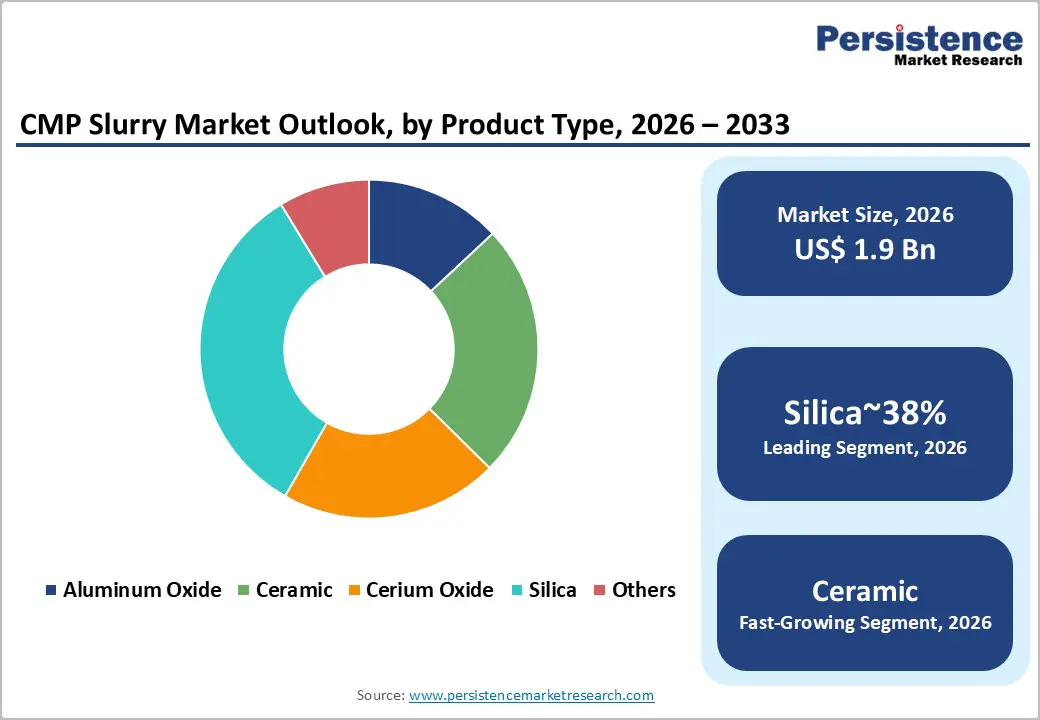

- Fastest-Growing Segment: Silica-based formulations lead the Product Type segment at approximately 38% revenue share in 2026 and are the fastest-evolving material category, driven by their critical role in sub-5nm STI and inter-metal dielectric CMP processes deployed by leading foundries globally.

- Key Opportunity: A primary market opportunity lies in the compound semiconductor manufacturing wave for EV and 5G applications, with announced SiC fab investments exceeding US$ 10 billion from Wolfspeed, STMicroelectronics, and Onsemi creating a structurally additive, specialized slurry demand pipeline.

| Key Insights | Details |

|---|---|

| CMP Slurry Market Size (2026E) | US$ 1.9 Billion |

| Market Value Forecast (2033F) | US$ 3.2 Billion |

| Projected Growth CAGR (2026 - 2033) | 7.9% |

| Historical Market Growth (2020 - 2025) | 6.4% |

Market Dynamics

Drivers - Landmark Semiconductor Policy Investments Scaling Global Fab Capacity and CMP Demand

Government-led semiconductor investment programs across major economies are becoming a key structural driver for the CMP slurry market. The U.S. CHIPS and Science Act, introduced in August 2022, allocated US$ 52.7 billion to strengthen domestic semiconductor manufacturing, research, and workforce development. This initiative has already triggered more than US$ 200 billion in private investments across states such as Arizona, Ohio, Texas, and New York.

The European Chips Act aims to mobilize over €43 billion in combined public and private funding to increase Europe’s share of global chip production to 20% by 2030. Each new wafer fabrication facility requires a steady and increasing supply of CMP slurries across multiple planarization stages. Advanced semiconductor nodes typically involve 12 to 20 CMP steps per wafer, as noted by industry research. This strong policy-backed expansion is expected to sustain long-term growth in slurry demand.

AI Accelerator and High-Bandwidth Memory Proliferation Amplifying Per-Wafer Slurry Intensity

The rapid growth of artificial intelligence platforms, generative AI applications, and large-scale data infrastructure is significantly increasing demand for high-performance semiconductors, thereby boosting CMP slurry consumption. According to the Semiconductor Industry Association, global semiconductor sales reached US$ 526.8 billion in 2023 and are projected to exceed US$ 1 trillion by 2030. AI accelerators developed by leading companies such as NVIDIA, AMD, and Intel are manufactured using advanced process nodes that require more CMP steps per wafer.

The growing adoption of high-bandwidth memory (HBM), which relies on precise tungsten and oxide polishing processes, is further driving slurry demand. As AI training systems increasingly depend on stacked HBM modules, both chip complexity and production volumes continue to rise. This combined effect ensures that slurry consumption per semiconductor unit will steadily increase over the forecast period.

Restraints - Stringent Chemical Waste Regulations Raising Operational Compliance Costs

CMP slurry use generates substantial volumes of hazardous wastewater containing abrasive particles, metal contaminants, and chemical residues, which must be carefully treated before disposal. Regulatory frameworks such as the U.S. Resource Conservation and Recovery Act (RCRA), the European Union’s REACH regulation, and similar policies in Japan and South Korea impose strict requirements on waste management and environmental safety. Semiconductor manufacturers must invest in advanced infrastructure, including filtration systems, slurry recycling units, and wastewater treatment facilities, to meet these standards.

These additional compliance measures significantly increase both capital and operational costs. Smaller foundries and OSAT providers, especially in Southeast Asia, often face financial pressure in adopting advanced slurry technologies due to these regulatory burdens. As a result, compliance challenges can limit the adoption of newer formulations and slow market penetration in cost-sensitive segments, ultimately affecting overall industry growth.

Raw Material Supply Concentration and Price Volatility in Critical Slurry Inputs

The CMP slurry market faces supply chain risks due to the heavy dependence on geographically concentrated raw materials. According to the U.S. Geological Survey, China produces over 85% of the world’s rare earth elements, including cerium, which is widely used in cerium oxide CMP slurries. This high level of concentration exposes manufacturers to potential supply disruptions and price fluctuations.

Trade restrictions, export controls, and geopolitical tensions have already caused periodic spikes in cerium oxide prices, increasing procurement costs for slurry producers. These fluctuations create uncertainty across the supply chain and make long-term planning more challenging. To manage these risks, manufacturers often invest in maintaining inventory buffers or developing alternative abrasive materials, both of which add to operational expenses. Ultimately, these cost pressures can affect product pricing and profit margins, thereby impacting competitiveness in the global market.

Opportunity - Advanced Packaging and 3D-IC Integration Creating Incremental CMP Application Demand

The semiconductor industry’s shift toward advanced packaging technologies is opening new opportunities for CMP slurry applications. Innovations such as chiplet architectures, 2.5D and 3D integrated circuits, and wafer-level packaging require highly planar surfaces for effective bonding and performance. These technologies involve additional CMP steps, including through-silicon-via polishing, redistribution-layer planarization, and hybrid-bonding surface preparation. Each step demands specialized slurry formulations tailored to specific materials and process requirements.

Industry organizations have identified advanced packaging as a key focus area through 2030, highlighting its importance in maintaining performance improvements. Leading semiconductor companies are investing heavily in expanding advanced packaging capabilities, creating sustained demand for high-value CMP slurries. Suppliers that can develop and qualify customized slurry solutions for these applications are well positioned to capture growth in this emerging segment.

Compound Semiconductor Manufacturing for EV and 5G Applications: Unlocking Specialized Slurry Demand

The growing adoption of compound semiconductors such as silicon carbide (SiC) and gallium nitride (GaN) is creating a new and high-growth demand segment for CMP slurry manufacturers. SiC-based power devices are increasingly used in electric vehicles due to their ability to improve energy efficiency and performance. Similarly, GaN semiconductors are widely used in 5G infrastructure and high-frequency applications.

These materials are significantly harder than traditional silicon, requiring specialized CMP slurries with advanced abrasive materials and precise chemical properties. As a result, slurry formulations for compound semiconductors differ significantly from those for conventional solutions. Ongoing investments in SiC and GaN manufacturing facilities across key regions are expected to drive long-term demand. Companies that focus on developing application-specific slurry solutions for these materials will benefit from this expanding market opportunity.

Category-wise Analysis

Product Type Insights

Within the CMP slurry market, the silica segment holds the largest share, accounting for approximately 38% of total product type revenue in 2026. Silica-based slurries are widely used for oxide polishing and shallow trench isolation processes in semiconductor manufacturing. Their strong market position is driven by their versatility, cost efficiency, and proven compatibility with widely used materials such as silicon dioxide and low-k dielectrics.

Industry research consistently identifies silica slurries as the preferred choice for key planarization processes in high-volume manufacturing. As semiconductor technologies advance to smaller nodes below 5nm, the number of CMP steps required per wafer increases, further strengthening demand for silica-based solutions. Their ability to deliver consistent performance and maintain high-quality surface finishes makes them a critical component in modern semiconductor fabrication, ensuring their continued dominance in the market.

Material Insights

Silica slurries also lead the material segment, holding around 40% of total market revenue in 2026. This dominance is mainly due to their essential role in core semiconductor manufacturing processes, including oxide planarization and interlayer dielectric polishing. Silica particles provide excellent control over surface uniformity and help reduce defects, which is critical in advanced semiconductor production where precision is extremely important.

Compared to other abrasive materials, silica offers better process stability and compatibility with cleaning chemistries used after CMP. This simplifies integration into existing manufacturing workflows and reduces operational complexity. Research studies and industry guidelines highlight the effectiveness of silica slurries in achieving high-quality results across various applications. As semiconductor manufacturing continues to evolve, the demand for reliable and high-performance materials like silica is expected to remain strong.

Application Insights

Silicon wafer applications dominate the CMP slurry market, contributing approximately 55% of total application revenue in 2026. CMP processes are widely used in both wafer manufacturing and semiconductor device fabrication, making silicon wafers the largest application area. The global scale of wafer production highlights the significant demand for CMP slurries in this segment.

Advanced semiconductor manufacturing requires highly precise slurry formulations with controlled particle sizes and minimal contamination to ensure defect-free surfaces. Leading semiconductor companies represent major customers for CMP slurry suppliers, and once a product is approved for use, it often results in long-term supply agreements. This creates a stable and recurring revenue stream for manufacturers. The increasing complexity of semiconductor devices further strengthens the importance of CMP processes, ensuring continued demand growth in silicon wafer applications.

Regional Insights

North America CMP Slurry Market Trends

North America plays a critical role in the global CMP slurry market, supported by strong semiconductor research capabilities and increasing manufacturing investments. Government initiatives have encouraged large-scale private investments in new fabrication facilities across the United States. These developments are creating long-term demand for CMP slurries as new fabs become operational. The region also benefits from the presence of leading slurry manufacturers and advanced research institutions that focus on developing next-generation materials.

Continuous innovation in slurry formulations supports the production of advanced semiconductor nodes, helping maintain the region’s competitive edge. Additionally, collaborations between industry players and research organizations are driving improvements in performance and efficiency. As semiconductor demand continues to grow, North America is expected to remain a key hub for both consumption and innovation in the CMP slurry market.

Europe CMP Slurry Market Trends

Europe’s CMP slurry market is driven by a combination of established semiconductor manufacturing capabilities and strong policy support for industry expansion. Regional initiatives aim to increase semiconductor production capacity and reduce reliance on imports, creating opportunities for CMP slurry suppliers. Key countries such as Germany, the Netherlands, and Ireland host major semiconductor manufacturing facilities that contribute to regional demand.

The automotive sector plays a particularly important role, as Europe is a leading consumer of automotive semiconductors. Additionally, strict environmental regulations are encouraging companies to develop sustainable and eco-friendly slurry formulations. This focus on compliance is driving innovation and creating new growth opportunities for material suppliers. As investments in semiconductor manufacturing continue, Europe is expected to strengthen its position in the global CMP slurry market.

Asia Pacific CMP Slurry Market Trends

Asia Pacific is the largest and fastest-growing region in the CMP slurry market, driven by the high concentration of semiconductor manufacturing facilities. Countries such as Taiwan, South Korea, Japan, and China are home to leading semiconductor companies that operate at advanced technology nodes. This makes the region a major consumer of high-performance CMP slurries. Japan also plays a key role as a supplier of advanced slurry materials, with several companies specializing in high-quality formulations.

China is expanding its semiconductor manufacturing capacity, increasing demand for CMP slurries across various technology nodes. Meanwhile, India is emerging as a new market with growing investments in semiconductor production and packaging. Government support and industry partnerships are expected to further boost regional growth. Overall, Asia Pacific will continue to dominate the global CMP slurry market.

Competitive Landscape

The global CMP slurry market is moderately consolidated, with a few leading companies holding a significant share of advanced-node revenues. These companies differentiate themselves through strong technical expertise, proprietary formulations, and long-term relationships with major semiconductor manufacturers. Their ability to meet strict performance and quality requirements gives them a competitive advantage in high-end applications.

Mid-sized and regional players mainly focus on mature-node segments and local markets, where competition is based on cost and availability. Leading companies are investing heavily in research and development to create next-generation slurry solutions compatible with advanced semiconductor technologies. They are also expanding their manufacturing presence in key regions to better serve customers. Additionally, new service models, such as on-site slurry management and delivery systems, are helping suppliers strengthen customer relationships and improve operational efficiency.

Key Developments:

- In October 2024: Entegris Inc. expanded its CMP slurry production capacity in Taiwan to strengthen proximity to leading foundries such as TSMC. This move supports rising demand for advanced-node logic and high-bandwidth memory manufacturing, ensuring supply reliability and faster customer response times.

- In March 2024: Fujimi Incorporated introduced advanced cerium oxide CMP slurries designed for high-selectivity shallow trench isolation at sub-5nm nodes. The innovation enhances defect control and planarization precision, meeting stringent requirements of next-generation semiconductor fabrication processes.

- In September 2023: Cabot Corporation acquired a specialty CMP slurry technology firm to strengthen its portfolio in advanced packaging and heterogeneous integration. This strategic move supports growing demand from chiplet architectures and positions Cabot in high-growth semiconductor applications.

Companies Covered in CMP Slurry Market

- Entegris Inc.

- DuPont de Nemours, Inc.

- Fujimi Incorporated

- Hitachi Chemical Company, Ltd.

- Saint-Gobain Ceramics & Plastics, Inc.

- Showa Denko Materials Co., Ltd.

- BASF SE

- 3M Company

- Evonik Industries AG

- Merck KGaA

- Cabot Corporation

- Dow Chemicals

- Samsung SDI

- KCTech

- Soulbrain Co., Ltd.

- CMC Materials (Merck KGaA)

- Nitta Haas Incorporated

- AGC Inc.

- Ferro Corporation

Frequently Asked Questions

The global CMP Slurry Market is valued at US$ 1.9 Billion in 2026 and is projected to reach US$ 3.2 Billion by 2033, registering a CAGR of 7.9% during the 2026-2033 forecast period. The market demonstrated a historical growth CAGR of 6.4% between 2020 and 2025.

The principal demand drivers are the global surge in semiconductor fabrication investments stimulated by the U.S. CHIPS and Science Act (US$ 52.7 billion) and the European Chips Act (€43 billion), alongside the intensifying adoption of AI accelerators and high-bandwidth memory chips that require significantly higher CMP step counts per wafer at advanced sub-5nm process nodes.

The Silicon Wafers application segment is the leading category, accounting for approximately 55% of application-based revenue in 2026. This dominance is supported by SEMI-reported global silicon wafer shipments exceeding 14,197 MSI and the high-volume nature of wafer polishing across both prime wafer preparation and in-process device fabrication applications.

Asia Pacific leads the global CMP Slurry Market, driven by the concentration of the world's most advanced semiconductor manufacturers, including TSMC, Samsung Electronics, and SK Hynix, which collectively command the highest-volume consumption of precision-grade CMP slurries for advanced logic and memory chip manufacturing.

The expansion of SiC and GaN compound semiconductor manufacturing for electric vehicle powertrains and 5G infrastructure represents a high-value structural opportunity. With over US$ 10 billion in SiC capacity investments announced by Wolfspeed, STMicroelectronics, and Onsemi, this segment creates substantial demand for specialized CMP slurry formulations with dedicated abrasive chemistries.

The leading companies in the global CMP Slurry Market include Entegris Inc., DuPont de Nemours, Inc., Fujimi Incorporated, Cabot Corporation, Hitachi Chemical Company, Ltd., Showa Denko Materials Co., Ltd., Evonik Industries AG, Merck KGaA, BASF SE, 3M Company, Soulbrain Co., Ltd., and KCTech.