- Smart Packaging

- Clinical Trial Packaging Market

Clinical Trial Packaging Market Size, Share, and Growth Forecast, 2026 - 2033

Clinical Trial Packaging Market by Packaging Type (Vials & Ampoules, Kits & Packs, Others), Material Type (Plastic, Glass, Others), End-user, and Regional Analysis for 2026 - 2033

Clinical Trial Packaging Market Size and Trends Analysis

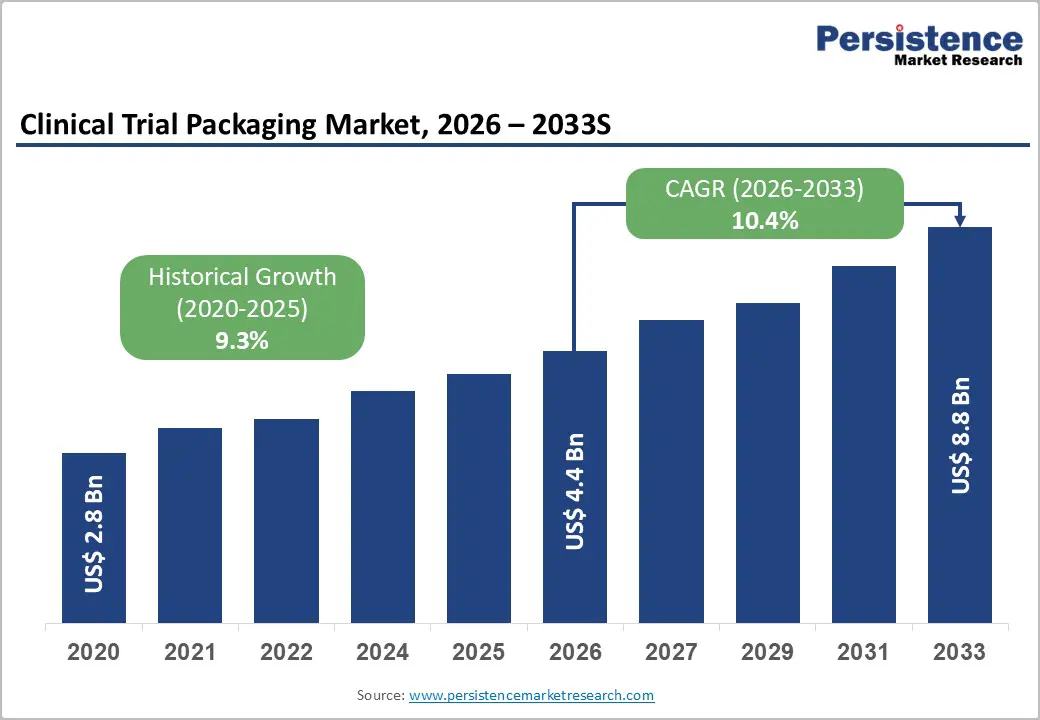

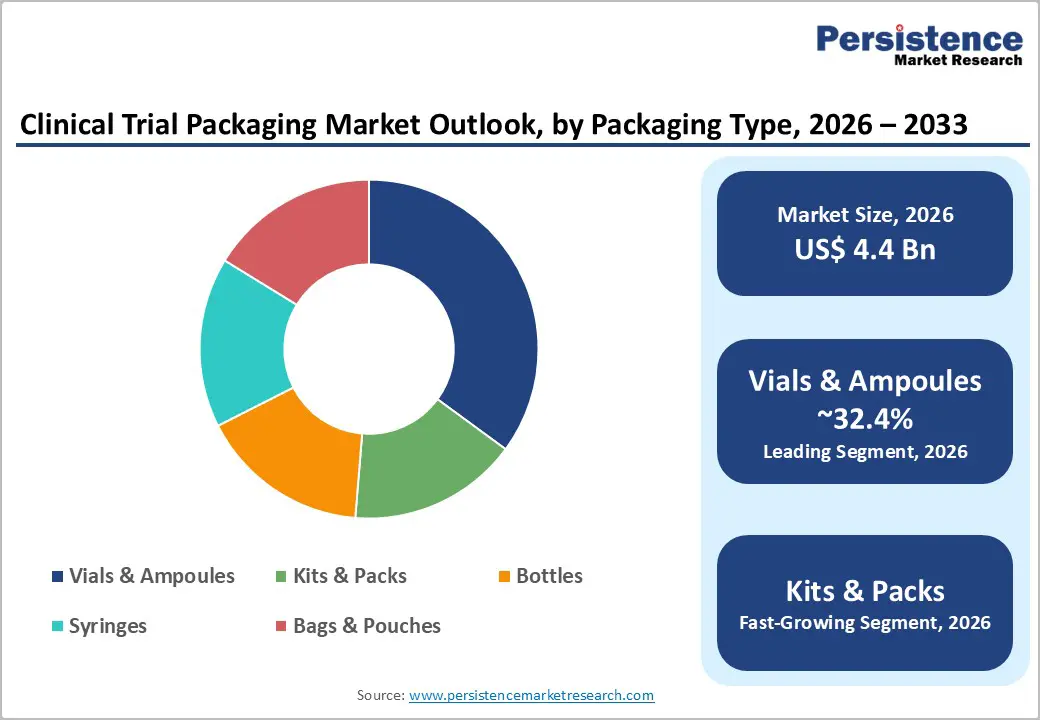

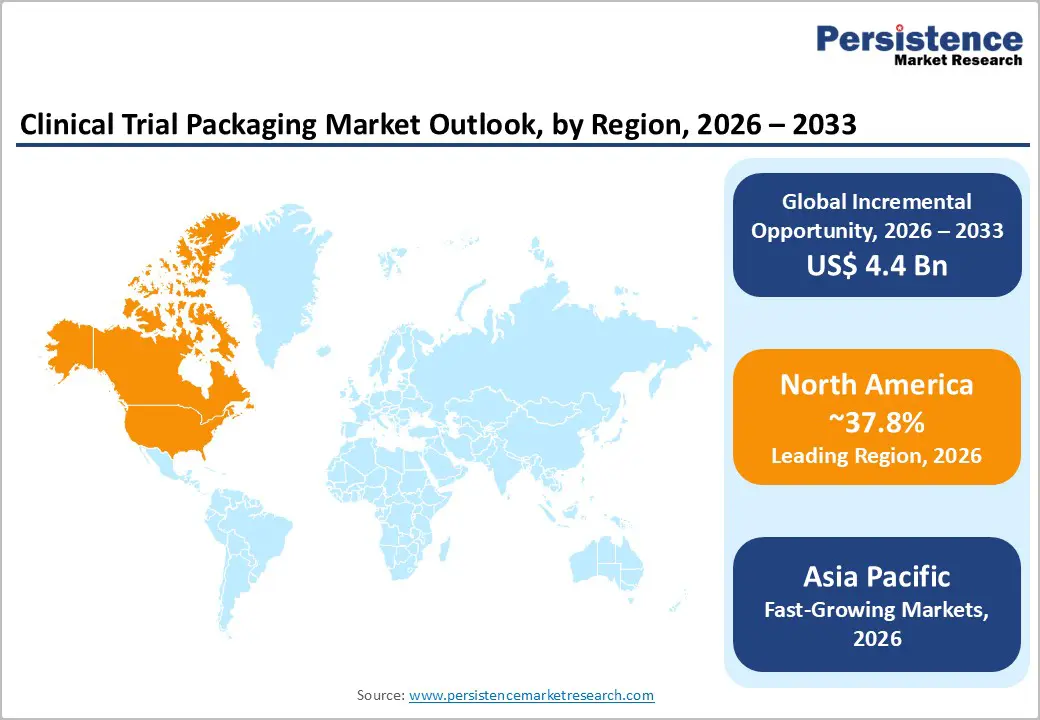

The global clinical trial packaging market size is likely to be valued at US$ 4.4 billion in 2026 and is expected to reach US$8.8 billion by 2033, growing at a CAGR of 10.4% between 2026 and 2033, driven by expanding global clinical trial activity, increasing outsourcing of clinical supply operations, and technological advancement in patient-centric packaging systems.

Pharmaceutical companies and biotechnology firms are placing greater emphasis on efficient clinical supply chains to ensure product integrity, regulatory compliance, and patient safety during trial phases. The market is also benefiting from the rapid adoption of decentralized clinical trials, which require more sophisticated packaging and distribution strategies. Rising investments in cold-chain infrastructure, serialization technologies, and multi-component patient kits are increasing packaging complexity and cost per patient. These structural factors collectively support strong demand for specialized clinical trial packaging solutions worldwide.

Key Industry Highlights:

- Leading Region: North America is projected to hold the leading position in the market, accounting for 37.8% of the market share, supported by strong pharmaceutical R&D activity, a large number of clinical trials, and the presence of major clinical supply service providers.

- Fastest-growing Region: Asia Pacific is projected to be the fastest-growing regional market, driven by increasing clinical trial activity in China, India, and Japan along with expanding contract research and manufacturing infrastructure.

- Investment Plans: Major clinical supply companies are investing in new packaging and distribution facilities, with firms such as Almac Group and Catalent expanding clinical packaging capabilities to support biologics, decentralized trials, and temperature-controlled supply chains, reflecting an industry investment focus growing at over 10% annually.

- Dominant Packaging Type: Vials and ampoules are expected to account for around 32.4% of the market share, due to their extensive use in injectable biologics, vaccines, and sterile pharmaceutical formulations used in clinical trials.

- Leading Material: Plastic materials are estimated to represent the leading packaging material segment with approximately 54.7% share, driven by their lightweight structure, durability, and widespread use in bottles, blister packs, and clinical trial kit components.

| Key Insights | Details |

|---|---|

| Clinical Trial Packaging Market Size (2026E) | US$4.4 Bn |

| Market Value Forecast (2033F) | US$8.8 Bn |

| Projected Growth (CAGR 2026 to 2033) | 10.4% |

| Historical Market Growth (CAGR 2020 to 2025) | 9.3% |

Market Factors - Growth, Barriers, and Opportunity Analysis

Growth Analysis - Rising Global Clinical Trial Activity and R&D Investment

The growth of pharmaceutical and biotechnology research pipelines is a primary driver of the clinical trial packaging market. Increasing investment in drug discovery and development has led to a rising number of clinical trials across multiple therapeutic areas, including oncology, rare diseases, and immunology. As products progress through clinical phases, packaging requirements become more complex due to increasing patient enrollment and multi-site trial structures. Late-stage clinical trials require large volumes of investigational medicinal products (IMPs) that must be packaged, labeled, and distributed in compliance with regulatory guidelines. This complexity significantly increases the demand for specialized packaging solutions such as temperature-controlled containers, tamper-evident labeling, and randomized patient kits. The expansion of biologics and cell-based therapies has further intensified packaging requirements as these therapies often require strict temperature control and protection against environmental exposure. As a result, pharmaceutical companies are increasingly outsourcing clinical supply and packaging operations to specialized service providers that offer validated packaging facilities and global distribution networks.

Growth of Decentralized and Patient-Centric Clinical Trials

Decentralized clinical trials are transforming the traditional trial model by enabling remote participation and direct-to-patient drug delivery. This shift is increasing the complexity of packaging and logistics operations as investigational products must be delivered safely to patients' homes while maintaining regulatory compliance and product integrity. Patient-centric trial designs require packaging solutions that incorporate multiple components, including drug containers, dosing devices, monitoring equipment, and patient instructions. These kits must be carefully assembled and labeled to ensure accurate administration and minimize the risk of dosing errors. Decentralized trials require robust tracking systems and documentation to monitor drug distribution and usage across geographically dispersed patient populations. The growing emphasis on patient convenience and trial accessibility is therefore increasing the demand for customized clinical trial packaging solutions, including pre-assembled kits, tamper-evident packaging, and temperature-controlled shipping systems.

Regulatory Requirements for Traceability and Compliance

Strict regulatory standards governing clinical trials are another major driver of the clinical trial packaging market. Regulatory authorities require sponsors to maintain full traceability of investigational medicinal products throughout the clinical supply chain, from manufacturing to patient administration. Clinical trial packaging must therefore meet stringent requirements related to labeling accuracy, batch identification, and product integrity. Packaging systems must also comply with Good Manufacturing Practices (GMP) and Good Clinical Practices (GCP), ensuring that products remain safe and effective during transportation and storage. To meet these requirements, pharmaceutical companies are investing in advanced packaging technologies such as serialization, barcoding, and digital tracking systems. These technologies enable real-time monitoring of clinical supplies and improve the ability to conduct recalls or audits if necessary. The increasing complexity of compliance requirements continues to drive demand for specialized clinical packaging providers with established regulatory expertise.

Barrier Analysis - High Capital Investment and Infrastructure Requirements

Clinical trial packaging operations require highly specialized infrastructure, including controlled manufacturing environments, validated packaging equipment, and temperature-regulated storage facilities. Establishing such facilities requires substantial capital investment and extensive regulatory qualification processes. Packaging providers must also conduct rigorous validation studies to ensure that packaging materials and systems maintain product stability throughout the supply chain. These validation processes can be time-consuming and expensive, particularly for temperature-sensitive biologic products. As a result, smaller service providers may face barriers to entry, while existing providers must continuously invest in facility upgrades and compliance systems to remain competitive. These financial and operational requirements can slow capacity expansion and limit market entry for new participants.

Complex Global Regulatory Landscape

Clinical trials are frequently conducted across multiple countries, each with its own regulatory requirements for drug packaging, labeling, and distribution. This regulatory diversity creates operational challenges for pharmaceutical companies and packaging providers. Packaging solutions must often be customized to meet local language requirements, labeling standards, and regulatory documentation guidelines. This can increase packaging complexity and raise operational costs, particularly for multinational clinical trials involving numerous trial sites. In addition, regulatory inspections and compliance audits may delay trial timelines if packaging processes do not meet required standards. These challenges highlight the importance of strong regulatory expertise within clinical packaging service providers.

Opportunity Analysis - Expansion of Clinical Trials in Emerging Markets

Emerging markets are becoming increasingly important locations for clinical trials due to lower operational costs, large patient populations, and improving regulatory environments. Countries across Asia Pacific, Eastern Europe, and Latin America are attracting significant clinical research investment from global pharmaceutical companies. The growing presence of clinical trial sites in these regions is creating demand for localized packaging and distribution services. Establishing regional clinical packaging facilities can help reduce shipping times, minimize customs delays, and improve supply chain efficiency. Service providers that expand their presence in emerging markets are likely to benefit from the growing demand for regional clinical supply infrastructure.

Adoption of Smart Packaging and Digital Tracking Technologies

Technological innovation is creating new opportunities in the clinical trial packaging market. Smart packaging technologies, including temperature monitoring sensors, digital tracking systems, and connected devices, are enabling better visibility and control over clinical supply chains. These solutions allow pharmaceutical companies to monitor environmental conditions during product transportation and ensure that investigational drugs remain within required temperature ranges. Real-time tracking systems also improve inventory management and help sponsors maintain regulatory compliance. The integration of digital technologies into clinical packaging is expected to create premium service offerings, particularly for biologic drugs and temperature-sensitive therapies.

Category-wise Analysis

Packaging Type Analysis

Vials and ampoules are anticipated to remain the leading packaging type, accounting for approximately 32.4% of the market share during the forecast period. These packaging formats are widely used for injectable drugs and biologics, which represent a substantial proportion of investigational therapies evaluated in clinical trials. Vials and ampoules offer strong protection against contamination, moisture, and oxygen exposure, making them highly suitable for sterile pharmaceutical products and temperature-sensitive biologics. Their compatibility with validated fill-finish systems and sterile handling processes further strengthens their adoption across early and late-stage clinical trials.

The demand for vial-based packaging is particularly strong in Phase I and Phase II trials, where injectable formulations are commonly tested for safety and efficacy. Pharmaceutical companies rely on validated vial packaging systems to maintain sterility, ensure dosing accuracy, and support compliance with clinical supply chain regulations. For example, oncology drugs and monoclonal antibody therapies frequently utilize glass vials due to their chemical stability and barrier protection. The continued expansion of biologics and biosimilar drug development pipelines is expected to sustain long-term demand for vial and ampoule packaging solutions in clinical research.

Kits and packs are projected to be the fastest-growing packaging type. Clinical trial kits typically contain multiple components required for patient participation, including investigational drugs, dosing devices, sample collection materials, patient instructions, and monitoring tools. These kits simplify logistics and ensure that trial participants receive all required materials in a single package, which improves protocol adherence and reduces operational complexity for clinical trial sponsors.

The growing adoption of decentralized and hybrid clinical trial models is significantly increasing demand for pre-assembled kits that can be delivered directly to patients’ homes. For instance, remote monitoring trials often include kits containing oral medications, wearable devices, and self-sampling tools for blood or saliva collection. These pre-configured kits improve patient convenience while minimizing the risk of dosing errors or missing materials. As decentralized trials become more prevalent, the importance of specialized kit assembly, customized labeling, and patient-centric packaging solutions is expected to expand across global clinical research operations.

Material Type Insights

Plastic is anticipated to remain the dominant material segment, accounting for approximately 54.7% of the market share in 2026. Plastic packaging materials provide several operational advantages, including lightweight construction, cost efficiency, durability, and design flexibility. They are widely used in pharmaceutical bottles, blister packs, syringes, and secondary packaging components that support investigational drug distribution. Plastic materials are particularly valuable in clinical trial kits where packaging weight and durability are critical factors during transportation and storage.

Lightweight plastic containers reduce shipping costs and minimize the risk of product damage during global distribution. In addition, pharmaceutical-grade polymers such as polyethylene (PE) and polypropylene (PP) offer strong chemical resistance and compatibility with a wide range of drug formulations. These materials are frequently used in oral drug bottles, blister packaging for tablets, and prefilled syringe components in clinical studies.

Specialty plastics, including advanced polymer materials such as PVC and multilayer polyethylene variants, are expected to represent the fastest-growing subsegment within the material category. Innovations in polymer science have enabled the development of materials with enhanced barrier properties, improved moisture resistance, and superior compatibility with biologic formulations. These materials are increasingly used in temperature-controlled packaging solutions and specialized drug delivery systems.

For example, multilayer polymer packaging structures are commonly used in blister packs for sensitive oral medications, while high-barrier polymer films are used in flexible pouches designed to protect drugs from oxygen and humidity exposure. Such materials also contribute to reducing overall package weight, which lowers transportation costs and improves supply chain efficiency. As pharmaceutical companies seek safer, more efficient, and sustainable packaging solutions for clinical trials, demand for advanced polymer materials is expected to grow steadily in the coming years.

Regional Insights

North America Clinical Trial Packaging Market Trends - Strong CRO Infrastructure and Regulatory-Driven Packaging Demand

North America is the largest regional market for clinical trial packaging, accounting for approximately 37.8% of the market share in 2026. The region benefits from a strong pharmaceutical industry presence, advanced research infrastructure, and significant investment in drug development. A large concentration of biotechnology companies, contract research organizations (CROs), and pharmaceutical manufacturers creates sustained demand for specialized clinical packaging and supply services.

The U.S. plays a dominant role in the regional market due to its high volume of clinical trials and extensive network of research institutions. Major pharmaceutical companies and research hospitals conduct a substantial portion of global clinical research in the country, generating consistent demand for labeling, packaging, and distribution of investigational medicinal products. For instance, companies such as Thermo Fisher Scientific and Catalent operate extensive clinical supply facilities across the U.S., providing services such as bottle filling, blister packaging, labeling, and cold-chain logistics for global clinical trials. Several factors contribute to North America's market leadership. The region has a highly developed regulatory framework led by the U.S. Food and Drug Administration, which ensures strict oversight of clinical trial operations. Compliance with these regulations requires specialized packaging solutions capable of maintaining product integrity, serialization, and traceability across complex supply chains. As a result, pharmaceutical companies rely heavily on experienced clinical packaging providers with validated GMP-compliant facilities.

Another major driver is the presence of large contract development and manufacturing organizations that provide integrated clinical supply services. Companies such as PCI Pharma Services and Almac Group have expanded their North American clinical packaging infrastructure to support growing demand for biologics and personalized medicine trials. For example, Almac has invested in expanding its clinical supply campus in Pennsylvania to strengthen packaging, labeling, and temperature-controlled distribution capabilities. Investment activity in the region remains strong as companies continue expanding packaging facilities and adopting automation technologies. Cold-chain packaging systems, smart labeling technologies, and direct-to-patient packaging solutions are gaining traction as decentralized trials grow in popularity. The increasing complexity of modern clinical trials, particularly those involving biologics and gene therapies, is expected to sustain demand for advanced packaging services across North America.

Europe Clinical Trial Packaging Market Trends - Biologic Packaging Capabilities and EMA-Led Regulatory Harmonization

Europe represents a significant share of the global clinical trial packaging market, supported by a strong pharmaceutical manufacturing base and an active clinical research ecosystem. Countries such as Germany, the U.K., France, and Spain play key roles in the regional market, supported by strong regulatory frameworks and government investments in life sciences innovation. Germany is widely recognized for its advanced pharmaceutical manufacturing infrastructure and strong biotechnology sector. Several global packaging and pharmaceutical service providers operate specialized clinical packaging facilities in the country. For example, Vetter Pharma operates advanced aseptic filling and packaging facilities in Germany that support clinical trials for injectable biologic therapies.

The company provides sterile packaging solutions for complex drug products such as monoclonal antibodies and injectable vaccines, which are increasingly used in clinical research. The U.K. is another major hub for clinical research, with numerous academic institutions and pharmaceutical companies conducting clinical trials. Organizations such as the National Institute for Health and Care Research have strengthened the country's clinical trial ecosystem by supporting large-scale research initiatives. Global pharmaceutical service providers such as Almac Group operate clinical packaging and labeling facilities in the UK that serve both European and international clinical studies.

France and Spain have also experienced increasing clinical trial activity in recent years. Regulatory reforms implemented through the European Medicines Agency Clinical Trials Regulation have streamlined trial approval processes across European Union member states. This regulatory harmonization has improved operational efficiency for multinational clinical trials, increasing the need for standardized packaging and labeling solutions across the region. The presence of major pharmaceutical packaging manufacturers such as Gerresheimer and SCHOTT AG further strengthens Europe’s role in the clinical trial packaging supply chain. These companies manufacture pharmaceutical-grade glass containers, vials, and syringes, widely used in clinical trials. Their strong manufacturing capabilities support investigational drug development across Europe and contribute to the region’s position as a critical hub for clinical research packaging solutions.

Asia Pacific Clinical Trial Packaging Market Trends - Rapid Clinical Trial Expansion Driven by Cost Advantages and Government Support

Asia Pacific is the fastest-growing regional market for clinical trial packaging. The region is experiencing rapid growth in clinical research activity due to favorable cost structures, expanding pharmaceutical industries, and supportive government policies aimed at attracting international drug development programs. China has emerged as one of the largest clinical trial markets in the world, supported by significant investment in biotechnology innovation and pharmaceutical manufacturing.

Companies such as WuXi AppTec have built integrated research and manufacturing platforms that include clinical supply packaging and logistics capabilities. These services support multinational pharmaceutical companies conducting clinical trials across Asia and global markets. Japan maintains a highly developed regulatory framework and advanced pharmaceutical manufacturing capabilities. The country continues to play an important role in global clinical research, particularly for innovative biologic therapies and regenerative medicine. Pharmaceutical service providers such as Lonza operate clinical supply infrastructure in the region to support biologic drug development and packaging requirements for multinational trials.

India is also emerging as a competitive destination for clinical trials due to its large patient population, skilled scientific workforce, and cost-efficient research infrastructure. Domestic companies such as Piramal Pharma Solutions and Bilcare Research provide clinical trial packaging, labeling, and cold-chain logistics services to global pharmaceutical companies. Bilcare, for example, has developed specialized clinical trial packaging solutions, including blister packaging and patient compliance packaging systems used in multinational clinical studies.

Across the Asia Pacific region, governments are implementing policies designed to strengthen clinical research infrastructure and attract international pharmaceutical investment. China and India have introduced regulatory reforms to accelerate clinical trial approvals, while countries such as Singapore and South Korea are investing heavily in biotechnology research hubs. These developments are encouraging pharmaceutical companies to expand their clinical research activities in the region, which in turn increases demand for specialized clinical trial packaging and supply chain services.

Competitive Landscape

The global clinical trial packaging market is moderately consolidated, with several global pharmaceutical service providers dominating the industry alongside numerous regional packaging specialists. Leading companies typically offer integrated services that combine clinical manufacturing, packaging, labeling, and distribution. These integrated capabilities allow providers to deliver end-to-end clinical supply solutions, reducing complexity for pharmaceutical sponsors. Established companies benefit from extensive regulatory expertise, validated facilities, and global distribution networks, which create strong competitive advantages.

Smaller regional providers also continue to serve niche markets by offering flexible packaging solutions tailored to specific clinical trial requirements. Leading companies in the clinical trial packaging market focus on expanding global infrastructure, integrating manufacturing and packaging services, and adopting advanced technologies such as serialization and smart packaging. Strategic partnerships with pharmaceutical companies and research organizations also play a key role in strengthening long-term market positions.

Key Industry Developments:

- In September 2025, Catalent partnered with Science 37 to support decentralized clinical trials by improving investigational medicinal product (IMP) supply chains and enabling direct-to-patient drug delivery, helping accelerate patient enrollment and expand access to remote clinical studies.

Companies Covered in Clinical Trial Packaging Market

- Catalent

- Almac Group

- PCI Pharma Services

- Thermo Fisher Scientific

- Lonza

- Piramal Pharma Solutions

- Bilcare Research

- Sharp Clinical Services

- UDG Healthcare (Sharp)

- Vetter Pharma International

- Parexel International

- Movianto

- Myonex

- Wasdell Group

- Nipro PharmaPackaging

- West Pharmaceutical Services

Frequently Asked Questions

The global clinical trial packaging market is estimated to be valued at US$4.4 billion in 2026.

The clinical trial packaging market is projected to reach US$8.8 billion by 2033.

Major trends include the growing adoption of decentralized clinical trials, increasing demand for temperature-controlled and biologics packaging, expansion of clinical trial kit assembly services, and the use of smart packaging and serialization technologies to improve traceability and regulatory compliance.

Vials and ampoules represent the leading packaging type, accounting for around 32.4% of the global market share, due to their widespread use in injectable drugs, vaccines, and biologic therapies undergoing clinical trials.

The clinical trial packaging market is expected to grow at a CAGR of 10.4% between 2026 and 2033.

Some of the major companies with strong clinical packaging portfolios include Catalent, Almac Group, PCI Pharma Services, Lonza, and Thermo Fisher Scientific.