- Processed Food

- Chickpea Flour Market

Chickpea Flour Market Size, Share, Growth, and Regional Forecast, 2026 to 2033

Chickpea Flour Market is segmented by Product Type (Desi Chickpea Flour, Kabuli Chickpea Flour), by Nature (Organic, Conventional), End-user (Bakery & Confectionery, Meat Alternatives, Extruded Products & Snacks, Dairy Alternatives & Dairy Products, Cosmetics & Personal Care, Animal Feed, Others), and Regional Analysis from 2026 to 2033

Chickpea Flour Market Share and Trends Analysis

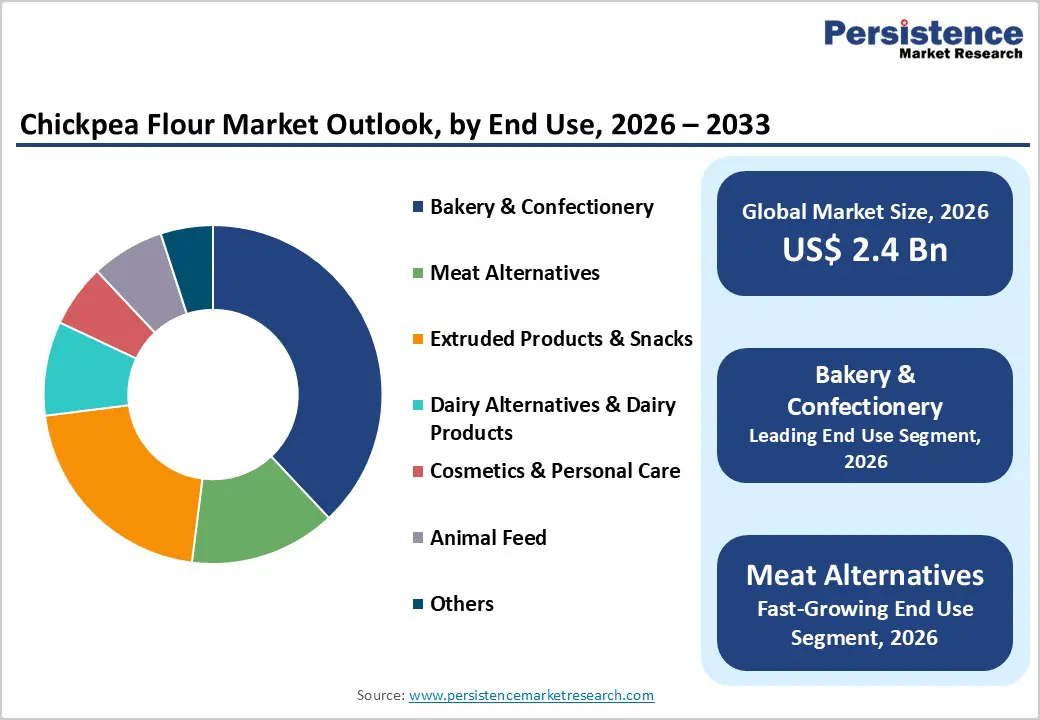

The global chickpea flour market size is expected to be valued at US$ 2.4 billion in 2026 and projected to reach US$ 3.8 billion by 2033, growing at a CAGR of 6.9% between 2026 and 2033.

The market expansion is primarily driven by the rise in global demand for gluten-free and protein-rich plant-based ingredients. As health consciousness rises, consumers are increasingly seeking nutrient-dense alternatives to traditional wheat flour. This trend is supported by the rapid growth of the vegan population and the intensifying focus on clean-label food products. Furthermore, the versatility of chickpea flour in various culinary applications, ranging from ethnic staples to modern functional foods, continues to bolster its market position across both developed and emerging economies.

Key Industry Highlights:

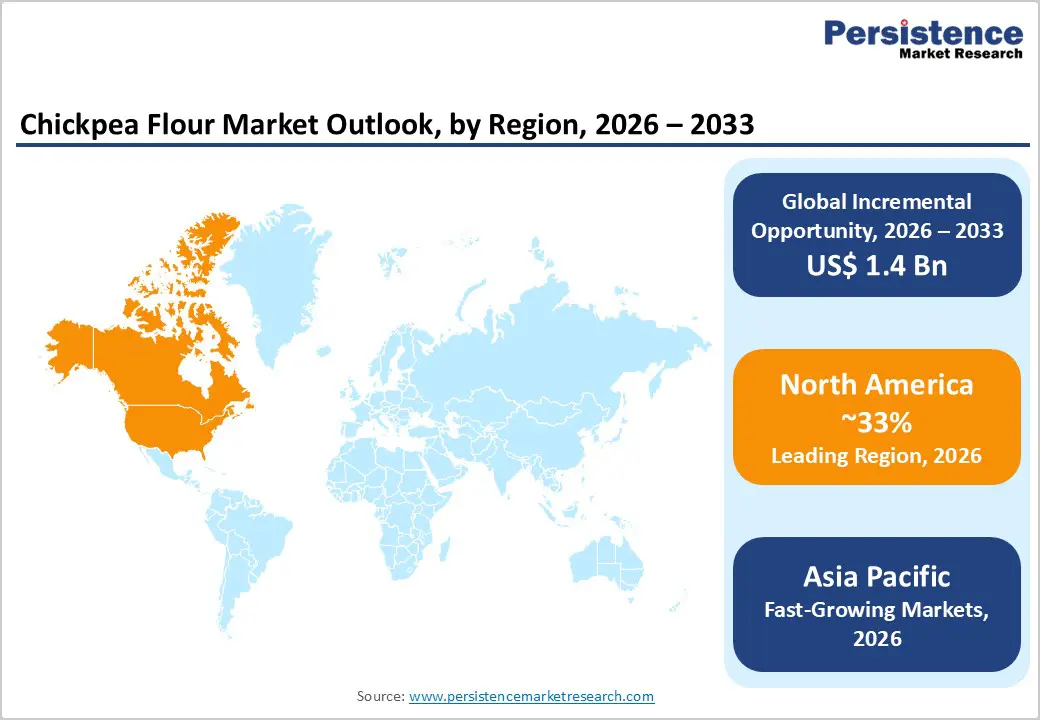

- Leading Region: North America, holding around 33% market share, supported by strong demand for gluten-free foods, plant-based diets, high consumer purchasing power, and rapid innovation in snacks and meat alternatives.

- Fastest-Growing Region: Asia Pacific, fueled by large-scale chickpea consumption in India and Pakistan, expanding packaged flour markets, and rising middle-class demand for convenient, protein-rich foods.

- Fastest-Growing Product Type Segment: Kabuli Chickpea Flour, driven by its mild taste, smoother texture, and suitability for bakery & confectionery products in Western markets.

- Market Drivers: Growing global shift toward plant-based and high-protein diets is accelerating chickpea flour adoption as a nutritious, sustainable ingredient across bakery, snacks, and alternative protein applications.

- Opportunities: Rapid expansion in meat alternatives and plant-based analogues, where chickpea flour’s emulsification and binding properties enable development of high-protein, clean-label plant-based foods.

| Key Insights | Details |

|---|---|

| Global Chickpea Flour Market Size (2026E) | US$ 2.4 Bn |

| Market Value Forecast (2033F) | US$ 3.8 Bn |

| Projected Growth (CAGR 2026 to 2033) | 6.9% |

| Historical Market Growth (CAGR 2020 to 2025) | 5.5% |

Market Dynamics

Driver - Growing Consumer Shift Toward Plant-Based and High-Protein Diets

The primary driver for the industry is the fundamental shift in consumer dietary patterns toward plant-based nutrition. According to the Food and Agriculture Organization (FAO), pulses like chickpeas are vital for sustainable food systems due to their low environmental footprint and high nutritional density. Chickpea flour offers a superior protein profile compared to many cereal grains, making it a staple for fitness enthusiasts and vegans. The American Heart Association highlights the benefits of high-fiber legumes in managing cholesterol and heart health, which has further encouraged mainstream adoption. As major food processors like ADM and Ingredion Incorporated expand their pulse-processing capacities, the accessibility of high-quality chickpea flour has increased, driving its integration into everyday food products globally.

Restraints - Volatility in Raw Material Prices and Supply Chain Disruptions

A significant barrier to market expansion is the unpredictability of chickpea crop yields, which are highly susceptible to climatic fluctuations. The International Grains Council frequently reports on how erratic rainfall and temperature shifts in major producing regions like India, Australia, and the United States lead to price volatility in the global pulse market. When raw chickpea prices spike, manufacturers often face squeezed margins, which can result in higher retail prices for chickpea-based products. Furthermore, logistical hurdles and trade policies in major exporting hubs can cause temporary supply shortages. These environmental and economic uncertainties make it challenging for long-term price stabilization, potentially deterring budget-conscious consumers in developing regions from adopting chickpea flour as a frequent staple.

Opportunity - Rapid Expansion into the Meat Alternatives and Analogues Sector

The Meat Alternatives segment represents the fastest-growing opportunity for chickpea flour through 2033. As the demand for high-moisture meat analogues and plant-based patties surges, manufacturers are turning to chickpea flour for its exceptional emulsification and gelling properties. Unlike soy or wheat-based proteins, chickpea flour is often perceived as a cleaner and less allergenic alternative. As per studies from Persistence Market Research, pulses are becoming the next frontier in the alternative protein revolution. Companies that can provide customized, high-functionality chickpea flours tailored for extrusion processes will likely capture significant market share. This trend is particularly strong in North America and Europe, where the innovation ecosystem for plant-based meat is most mature and consumer interest in sustainable protein is highest.

Category-wise Analysis

Product Type Insights

The desi chickpea flour segment currently holds a significant market position particularly in the Asia Pacific region where it is a foundational ingredient for traditional snacks and savories. Desi chickpeas are generally smaller and have a thicker seed coat, resulting in a flour with a more pronounced flavor and higher fiber content. Conversely, the Kabuli Chickpea Flour segment is gaining immense popularity in Western markets. Kabuli chickpeas are larger, lighter in color, and have a smoother texture, which translates into a milder-tasting flour that is easier to incorporate into neutral-flavored Bakery & Confectionery items. The preference for Kabuli flour is rising in the United States and Europe as it aligns better with the palate of consumers transitioning from refined wheat flours.

Nature Insights

The conventional segment remains the leading segment in terms of volume, primarily due to its lower price point and widespread availability in mass-market retail channels. However, the Organic segment is experiencing the fastest growth as consumer scrutiny over pesticide residues and soil health intensifies. USDA Organic and EU Organic certifications have become powerful marketing tools for premium brands like Bob's Red Mill Natural Foods and Doves Farm Foods. The organic nature of chickpea flour is particularly appealing to the lifestyle segment of the market, where consumers are willing to pay a premium for products that are perceived as being purer and more environmentally responsible. This trend is expected to continue as sustainable agricultural practices become a core focus for global pulse suppliers.

Region-wise Insights

North America Chickpea Flour Market Trends and Insights

North America currently holds the leading market share of 33% in 2025, underpinned by a highly developed health-and-wellness infrastructure and a massive demand for gluten-free products. The United States leads the regional market dynamics, with a strong focus on innovation in the Meat Alternatives and Extruded Products & Snacks sectors. Major players like Ardent Mills and Bob's Red Mill Natural Foods have a strong presence, providing a diverse range of stone-ground and sprouted chickpea flours.

The regulatory framework in the U.S., managed by the FDA, ensures high standards for food safety and labeling, which fosters consumer trust. Furthermore, the region’s innovation ecosystem is characterized by a high volume of startup activity in the plant-based space. The snackification of chickpea flour where it is used in everything from high-protein brownie mixes to savory crackers is a key trend. The high disposable income of North American consumers supports the premiumization of the Organic segment, making it a critical region for global market players to establish their premium brand identities.

Asia Pacific Chickpea Flour Market Trends and Insights

Asia Pacific is identified as the fastest growing segment for the chickpea flour market through 2032. This rapid expansion is primarily driven by the deep-rooted cultural importance of chickpeas in India and Pakistan, combined with the modernization of the food processing industry in China and Australia. India is the world's largest producer and consumer of chickpeas, and Besan (chickpea flour) is a fundamental ingredient in millions of households for daily meals and festive savories like Pakoras and Ladoo.

The growth dynamics in the region are shifting as urban consumers move toward packaged and branded pulse flours for convenience. ITC and Organic Tattva are major players capitalizing on this formalization of the market. Furthermore, Australia has emerged as a major exporter of high-quality Kabuli chickpeas, supplying the global flour manufacturing industry. The rising middle class in the region, with increasing awareness of protein-deficiency and healthy snacking, is expected to maintain Asia Pacific's status as a pivotal growth engine for the global market throughout the forecast period.

Competitive Landscape

The chickpea flour market exhibits a moderately consolidated structure, where global ingredient giants like Ingredion Incorporated, ADM, and Cargill, Incorporated hold significant influence over the large-scale industrial supply chain. These companies leverage their massive processing infrastructure and R&D capabilities to offer standardized, high-functionality flours. However, the retail market remains vibrant and fragmented, with artisanal and specialty brands like Anthony’s Goods and Bob's Red Mill catering to health-conscious home bakers. Key differentiators in this market include the method of milling (stone-ground vs. industrial), the source of the chickpeas (Desi vs. Kabuli), and the presence of organic certifications. Emerging business model trends show a move toward vertical integration, where companies work directly with pulse growers to ensure traceability and quality from farm to fork, a factor that is increasingly important to modern consumers.

Companies Covered in Chickpea Flour Market

- Ingredion Incorporated

- ADM

- AGT Food and Ingredients

- Ardent Mills

- Bob's Red Mill Natural Foods

- Cargill, Incorporated

- Anthony’s Goods

- ITC

- Organic Tattva

- Biona Organic

- Doves Farm Foods

- Others

Frequently Asked Questions

The global chickpea flour market is projected to be valued at US$ 2.4 Bn in 2026.

Growing Consumer Shift Toward Plant-Based and High-Protein Diets is a major factor driving global Chickpea Flour market.

The Global Chickpea Flour market is poised to witness a CAGR of 6.9% between 2026 and 2033.

Rapid Expansion into the Meat Alternatives and Analogues Sector is a significant opportunity in the Chickpea Flour market.

Major players in the Global Chickpea Flour market include Ingredion Incorporated, ADM, AGT Food and Ingredients, Ardent Mills, Bob's Red Mill Natural Foods, Cargill, Incorporated, and others.