- Specialty & Fine Chemicals

- Carbon & Graphite Felt Market

Carbon & Graphite Felt Market Size, Share, and Growth Forecast 2026 - 2033

Carbon & Graphite Felt Market by Raw Material (Rayon Based, PAN Based, Pitch Based), Application (Optic Fibres, Furnace, Heat Shields, Automotive Exhaust Lining, Battery, Others), End-user (Electrical and Electronics, Automotive, Power Generation, Others), and Regional Analysis, 2026 - 2033

Carbon & Graphite Felt Market Size and Trend Analysis

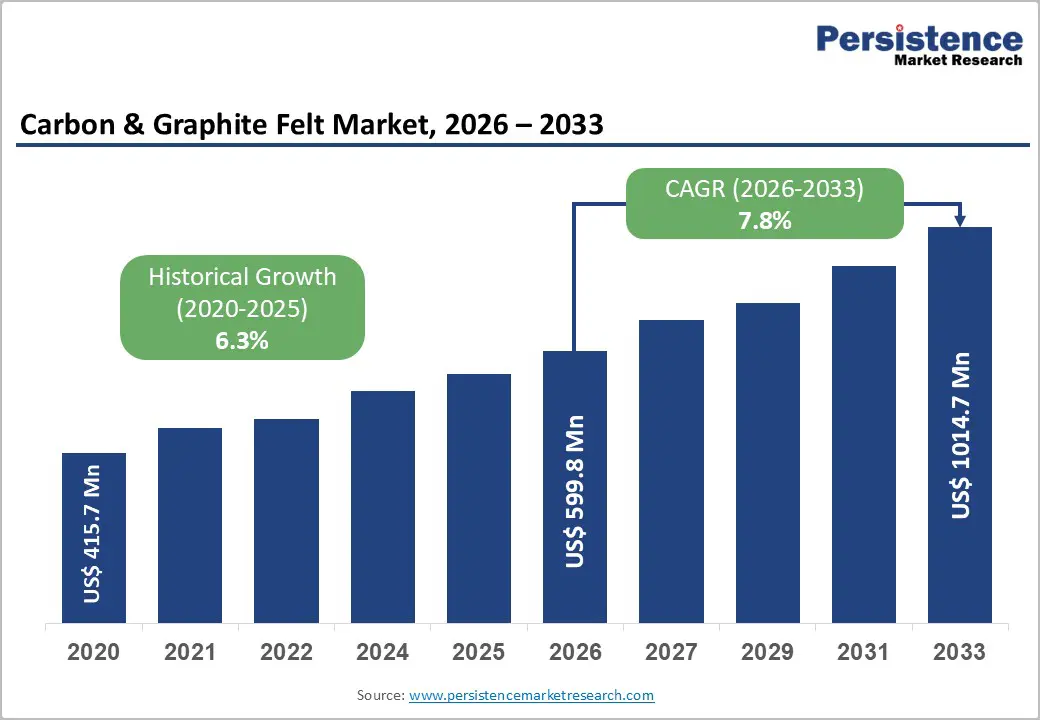

The global carbon & graphite felt market size is likely to be valued at US$ 599.8 Million in 2026 and is expected to reach US$ 1,014.7 Million by 2033, growing at a CAGR of 7.8% during the forecast period from 2026 to 2033. The carbon & graphite felt industry is on a sustained high-growth trajectory, driven by accelerating demand from industrial high-temperature processing, advanced energy storage, and semiconductor manufacturing sectors where the material's exceptional thermal insulation, electrical conductivity, and chemical resistance are structurally irreplaceable.

Key Industry Highlights:

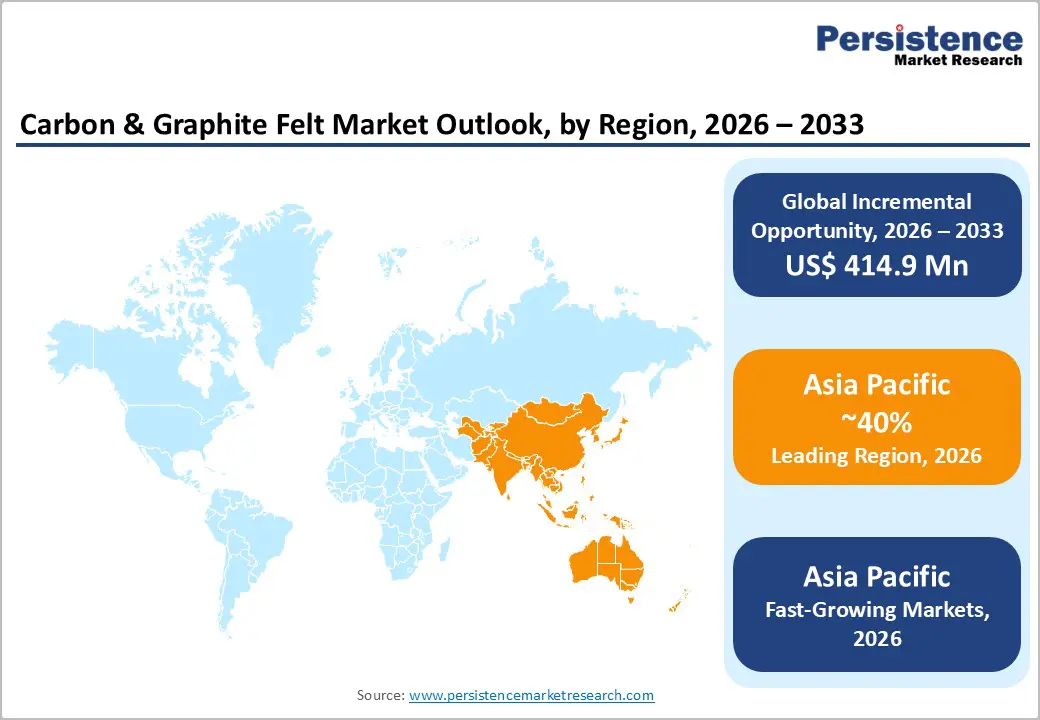

- Leading Region: Asia Pacific leads the global Carbon & Graphite Felt Market with over 40% revenue share, anchored by China's dominant photovoltaic silicon furnace and VRFB deployment base, Japan's precision felt manufacturing from Kureha and Nippon Carbon, and India's expanding solar and semiconductor manufacturing capacity.

- Fastest-Growing Region: Asia Pacific is also the fastest-growing region through 2033, driven by China's large-scale vanadium flow battery grid storage projects, India's PLI scheme for solar module manufacturing, and ASEAN electronics and semiconductor ecosystem expansion, accelerating furnace insulation felt procurement.

- Leading Segment: The Furnace application dominates with approximately 42% share, sustained by the permanently installed base of high-temperature industrial furnaces in photovoltaic silicon, semiconductor, sapphire growth, and heat treatment sectors requiring carbon felt rated to 3,000°C

- Fastest-Growing Segment: The Battery application segment is the fastest-growing category, propelled by VRFB electrode felt demand linked to IRENA's projection of 14 TWh of required stationary storage by 2030, with research confirming modified graphite felt achieving 84% energy efficiency over 250 cycles in vanadium flow battery systems

- Key Opportunity: Grid-scale vanadium redox flow battery deployment represents the most significant long-term opportunity, as each megawatt-hour of installed VRFB capacity directly requires large-area carbon felt electrodes, making manufacturers capable of supplying application-optimized, surface-modified electrode felts uniquely positioned for high-value, recurring supply contracts.

| Key Insights | Details |

|---|---|

|

Carbon & Graphite Felt Market Size (2026E) |

US$ 599.8 Million |

|

Market Value Forecast (2033F) |

US$ 1,014.7 Million |

|

Projected Growth CAGR (2026–2033) |

7.8% |

|

Historical Market Growth (2020–2025) |

6.3% |

DRO Analysis

Drivers - Rapid Expansion of Vanadium Redox Flow Batteries and Grid-Scale Energy Storage Driving Electrode Felt Demand

The global shift toward renewable energy is creating strong and long-term demand for carbon and graphite felt, especially as a key electrode material in vanadium redox flow batteries (VRFBs). These batteries are among the most advanced technologies for large-scale energy storage. In VRFB systems, carbon and graphite felt act as a porous electrode that supports ion exchange within the battery cells. This is possible due to its high surface area, excellent electrical conductivity, and strong resistance to acidic environments.

Studies show that VRFBs using improved graphite felt can reach up to 84% energy efficiency over 250 charge cycles, outperforming many alternative materials. According to the International Renewable Energy Agency, global stationary energy storage capacity must reach 14 terawatt-hours by 2030. This rapid expansion is expected to significantly increase demand for high-performance felt materials in energy storage projects worldwide.

Industrial High-Temperature Furnace Insulation Applications Sustaining Consistent Base Demand

Carbon and graphite felt remain critical insulation materials for high-temperature industrial furnaces, where they deliver unmatched performance. It can operate at temperatures up to 3,000°C, well beyond the capabilities of ceramic fiber or mineral wool alternatives. These materials are widely used in applications such as silicon crystal growth for solar panels and semiconductors, sapphire production, advanced alloy heat treatment, and glass manufacturing.

In 2024, many steel manufacturers upgraded furnace linings with graphite felt to improve energy efficiency and reduce heat loss, highlighting a growing industry preference for reliable high-performance materials. PAN-based graphite felt is especially valued for its low thermal conductivity and high-temperature stability. Its low impurity levels also make it ideal for sensitive applications like monocrystalline silicon production, where maintaining material purity is essential for consistent product quality.

Restraints - High Production Cost and Capital-Intensive Graphitization Processing Limiting Volume Adoption

The production of high-quality graphite felt involves multiple complex and energy-intensive processes, which significantly increase overall manufacturing costs. The process includes stabilization, carbonization at temperatures between 1,000°C and 1,400°C, and graphitization above 2,500°C. Each stage requires advanced furnace systems that are expensive to build and operate.

Among these, the graphitization stage is particularly capital-intensive, limiting production capacity to a few well-established players with strong technical expertise. This high cost structure reduces price competition in the market and keeps average selling prices relatively high. As a result, adoption of graphite felt is slower in cost-sensitive applications where alternative insulation materials may suffice. These barriers also discourage new entrants, making the market less competitive and limiting large-scale expansion in price-driven segments.

Cyclical Demand Weakness in Semiconductor and Solar End-Markets Affecting Near-Term Revenue Visibility

Demand for carbon and graphite felt in the semiconductor and solar industries is highly cyclical, which can impact short-term revenue growth. These industries often go through inventory correction cycles in which manufacturers reduce purchases until existing stock levels normalize. SGL Carbon reported a 22.2% decline in sales from its Graphite Solutions segment in the first half of 2025, mainly due to weak semiconductor demand and high customer inventory levels.

Such cycles create uncertainty for felt manufacturers, especially those heavily dependent on semiconductor and photovoltaic equipment markets. During these periods, companies may delay new investments or capacity expansions. While long-term demand remains strong due to technological growth, these short-term fluctuations can affect financial performance and planning. Managing this volatility remains a key challenge for companies operating in this market.

Opportunity - Semiconductor SiC Power Device Manufacturing Creating Multi-Year Structural Demand for Ultra-High-Purity Graphite Felt

The growing adoption of silicon carbide (SiC) power semiconductors is creating a strong long-term opportunity for high-purity graphite felt. SiC devices are widely used in electric vehicles, industrial drives, and renewable energy systems due to their superior efficiency and performance. The production of SiC wafers requires ultra-clean furnace environments, where graphite felt must have extremely low impurity levels to prevent contamination.

Even minor impurities can affect crystal quality and reduce device performance. As the market shifts from traditional silicon-based components to SiC technology, demand for specialized graphite felt is expected to increase significantly. Once current inventory challenges in the semiconductor sector stabilize, procurement activity is likely to recover strongly. Manufacturers that can deliver consistent, high-purity felt products will be well-positioned to secure long-term supply contracts with leading semiconductor companies.

Flow Battery Scale-Up in Renewable Energy Storage: Presenting a Fast-Growing, High-Volume Electrode Felt Market

The rapid growth of vanadium redox flow batteries for large-scale energy storage presents a major opportunity for carbon and graphite felt manufacturers. Unlike lithium-ion batteries, VRFB systems require a larger volume of felt material per unit of energy storage, making them highly material-intensive. As renewable energy projects expand globally, the need for grid-scale storage is increasing, directly driving demand for electrode felt.

Studies show that modifying carbon felt through processes like heat treatment or chemical doping can significantly improve battery efficiency and performance. This opens opportunities for manufacturers to develop advanced, high-value products tailored for battery applications. With global storage capacity expected to grow rapidly, VRFBs are becoming a key solution for long-duration energy storage. This trend positions electrode-grade graphite felt as one of the most promising growth segments in the carbon materials industry.

Category-wise Analysis

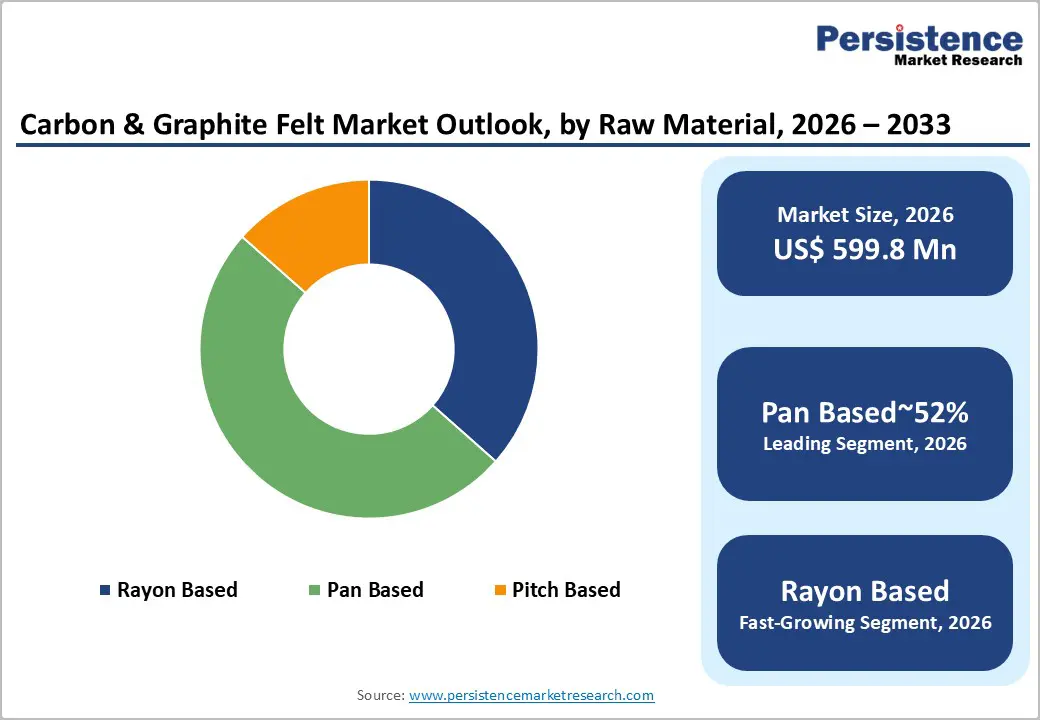

By Raw Material Insights

The PAN-based (Polyacrylonitrile) segment leads the Carbon & Graphite Felt Market, accounting for approximately 52% of total share. This dominance is driven by the superior properties of PAN-based fibers, which provide excellent strength, high purity, controlled porosity, and strong electrical conductivity. These characteristics make PAN-based felt the preferred choice for major applications such as furnace insulation and battery electrodes.

The manufacturing process, which includes pre-oxidation, carbonization, and graphitization, yields a lightweight material with a bulk density of approximately 0.10 g/cm³. Additionally, it offers low thermal conductivity even at high temperatures, making it highly efficient for thermal insulation. Its low impurity levels are especially important in semiconductor applications, where contamination control is critical. Overall, PAN-based graphite felt continues to lead due to its performance reliability across demanding industrial environments.

By Application Insights

The furnace application segment holds the largest share, about 42%, in the Carbon & Graphite Felt Market. This segment benefits from stable and consistent demand due to the large installed base of industrial furnaces globally. These furnaces are used in semiconductor production, solar silicon processing, sapphire growth, and advanced material manufacturing. Carbon and graphite felt is preferred because it can withstand extremely high temperatures up to 3,000°C in controlled environments. Its performance exceeds that of traditional insulation materials, especially in high-precision applications. Meanwhile, the battery segment is emerging as the fastest-growing application area. This growth is mainly driven by increasing demand for VRFB systems in renewable energy storage. As global energy storage installations increase, battery-related demand for graphite felt is expected to grow faster than furnace applications over the coming years.

By End-user Insights

The Electrical and Electronics segment dominates the market, contributing approximately 38% of total revenue. This leadership is supported by strong demand from semiconductor manufacturing and energy storage system production. Graphite felt is widely used in silicon wafer production, SiC crystal growth, and photovoltaic manufacturing processes. It is also an essential electrode material in flow batteries. These applications are part of rapidly growing industries, ensuring steady long-term demand. Although short-term fluctuations may occur due to industry cycles, the overall demand outlook remains strong. The Power Generation segment is the fastest-growing end-user category, driven by increasing deployment of renewable energy storage solutions. As utility-scale battery installations expand, demand for electrode-grade graphite felt is expected to rise significantly, supporting strong growth in this segment.

Regional Insights

North America Carbon & Graphite Felt Market Trends

North America plays a key role in the Carbon & Graphite Felt Market, supported by strong industrial and technological capabilities. The United States leads the region with significant investments in semiconductor manufacturing and energy storage systems. Government initiatives, such as funding for semiconductor production and energy storage development, are driving demand for graphite felt used in high-temperature furnace applications.

New semiconductor facilities require advanced insulation materials, creating additional opportunities for market growth. The region also benefits from a strong aerospace and defense sector, where graphite felt is used in thermal protection systems. Leading suppliers in North America continue to expand their production capabilities to meet rising demand. As semiconductor activity recovers and energy storage projects grow, the region is expected to see steady market expansion over the forecast period.

Europe Carbon & Graphite Felt Market Trends

Europe is a technologically advanced market with a strong focus on innovation and sustainability. Countries such as Germany lead in specialty graphite production and industrial applications. Investments in renewable energy and battery storage, supported by environmental policies, are increasing demand for graphite felt. The region’s automotive and power electronics industries also contribute to growth, particularly in SiC semiconductor applications. Manufacturers are expanding production capacities to meet rising demand from both industrial and energy sectors. Europe’s commitment to renewable energy targets is encouraging large-scale energy storage projects, which directly support the growth of graphite felt demand. Overall, the region is expected to maintain steady growth, driven by strong industrial capabilities and policy support.

Asia Pacific Carbon & Graphite Felt Market Trends

Asia Pacific is the largest and fastest-growing market, accounting for over 40% of global revenue. This growth is mainly driven by China’s dominance in solar manufacturing, semiconductor production, and energy storage deployment. The country has a well-established graphite supply chain and is actively investing in large-scale VRFB projects.

Japan contributes with high-quality manufacturing and advanced material expertise, while India is emerging as a growing market due to expanding solar and electronics industries. Southeast Asian countries are also developing their semiconductor ecosystems, increasing demand for furnace insulation materials. The region’s strong industrial base and rapid adoption of renewable energy technologies are expected to drive continued growth in the Carbon & Graphite Felt Market.

Competitive Landscape

The carbon & graphite felt market is moderately consolidated, with a few major players holding significant market share. Leading companies benefit from advanced manufacturing capabilities, strong R&D, and established customer relationships. Key competitive factors include product quality, purity levels, and the ability to customize materials for specific applications. Companies are focusing on developing high-performance felt products for semiconductor and energy storage applications.

Strategic moves such as acquisitions and partnerships are helping firms strengthen their market position. There is also growing interest in developing specialized electrode materials for flow batteries. Long-term supply agreements and collaboration with energy storage companies are becoming common strategies. Overall, the market is evolving with a focus on innovation, quality, and application-specific product development.

Key Developments:

- July, 2024: Mersen acquired GMI Group to strengthen its North American presence in advanced materials. The acquisition enhances graphite purification, machining, and felt insulation capabilities, supporting aerospace, semiconductor, and energy sectors.

- August, 2022: SGL Carbon SE announced a mid-range, double-digit-million-euro investment to expand graphite felt production across Germany, North America, and China. The Meitingen facility expansion focuses on soft-felt production for semiconductor, solar, and energy-storage markets.

Companies Covered in Carbon & Graphite Felt Market

- Mersen

- HPMS Graphite

- CGT Carbon GmbH

- Carbon Composites, Inc.

- Kureha Corporation

- Saginaw Carbon

- Allied Metallurgy Resources LLC

- Beijing Great Wall Co., Ltd.

- SGL Carbon SE

- Olmec Advance Materials Ltd.

- Coidan Graphite Products Ltd.

- Bay Carbon Inc.

- AMK Metallurgical Machinery Group Co., Ltd.

- Nippon Carbon Co., Ltd.

- Toray Industries, Inc.

Frequently Asked Questions

The global Carbon & Graphite Felt Market is estimated at US$ 599.8 Million in 2026 and is projected to reach US$ 1,014.7 Million by 2033, growing at a CAGR of 7.8%, driven by accelerating VRFB energy storage deployments aligned with IRENA's 14 TWh global storage target by 2030, and expanding high-temperature furnace installations for photovoltaic silicon, SiC semiconductor, and advanced materials processing sectors globally.

The key drivers are the rapid expansion of vanadium redox flow battery installations for grid-scale renewable energy storage, where graphite felt achieves 84% energy efficiency over 250 cycles as electrodes, and the sustained high demand from industrial high-temperature furnace insulation applications across photovoltaic silicon pulling, semiconductor crystal growth, and advanced heat treatment sectors requiring materials rated to 3,000°C.

The Furnace application segment leads with approximately 42% market share, driven by its permanent and continuously expanding installed base in monocrystalline silicon pulling furnaces, SiC crystal growth reactors, sapphire growth systems, and industrial heat treatment furnaces globally, all of which require carbon and graphite felt insulation with consistent performance at extreme temperatures in vacuum or inert gas atmospheres.

Asia Pacific leads with over 40% of global revenues, anchored by China's dominant position in photovoltaic silicon production and VRFB deployment, Japan's precision manufacturing capabilities at Kureha Corporation and Nippon Carbon, and India's expanding solar module and semiconductor manufacturing investment programs creating new furnace insulation and electrode felt procurement demand.

The most significant opportunity is grid-scale vanadium redox flow battery scale-up for renewable energy storage, where each megawatt-hour of installed capacity requires large-area high-performance felt electrodes. Manufacturers capable of delivering application-optimized, surface-modified PAN-based electrode felts, improving VRFB reaction kinetics and cycle efficiency, can secure long-term, high-value supply contracts as global VRFB deployments accelerate through 2033.

The leading participants include Mersen, SGL Carbon SE, Kureha Corporation, Nippon Carbon Co., Ltd., Beijing Great Wall Co., Ltd., CGT Carbon GmbH, Carbon Composites, Inc., Saginaw Carbon, Bay Carbon Inc., Coidan Graphite Products Ltd., HPMS Graphite, Olmec Advance Materials Ltd., AMK Metallurgical Machinery Group Co., Ltd., and Allied Metallurgy Resources LLC, with Mersen and SGL Carbon SE holding leading global positions through diversified production infrastructure, high-purity processing capability, and active expansion strategies.