- Automotive

- Car Leasing Market

Car Leasing Market Size, Share, and Growth Forecast, 2026 - 2033

Car Leasing Market by Lease Type (Open-End, Closed-End, Finance), Vehicle Type (Hatchbacks, Sedans, Sports Utility Vehicles (SUVs), Electric Vehicles (EVs), Luxury Cars), End-User (Individual Consumers, Corporate Enterprises, Small & Medium Enterprises (SMEs), Government Organizations), and Regional Analysis for 2026 - 2033

Car Leasing Market Share and Trends Analysis

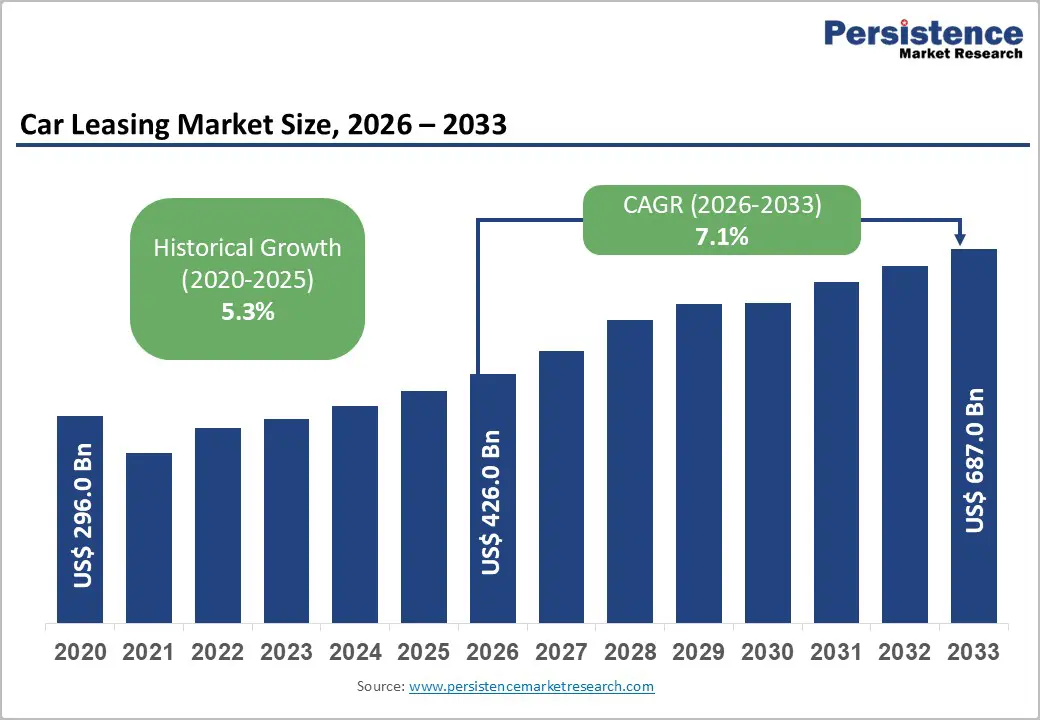

The global car leasing market size is likely to be valued at US$ 426.0 billion in 2026, and is estimated to reach US$ 687.0 billion by 2033, growing at a CAGR of 7.1% during the forecast period 2026 - 2033.

The promising growth trajectory of the market is primarily owing to the steady shift of vehicle acquisition models from outright ownership toward structured mobility financing. Leasing is becoming a central vehicle procurement strategy for corporate fleets and individual drivers alike, as it reduces upfront capital requirements and transfers residual value exposure to leasing providers. Data from the International Energy Agency (IEA) shows that global electric vehicle sales exceeded 17 million units in 2024. Leasing models are supporting fleet electrification programs by allowing companies to manage battery depreciation risks and rapid technology cycles more effectively.

Governments across North America and Europe are implementing stricter emissions-reduction policies and corporate decarbonization frameworks that encourage companies to renew fleets more frequently through leasing arrangements. For example, the European Automobile Manufacturers’ Association (ACEA) reports that corporate fleets account for nearly 60% of new passenger vehicle registrations in Europe. Vehicle affordability pressures are further bolstering the financial case for leasing among consumers and small businesses. According to the Federal Reserve Bank of St. Louis, global average new-vehicle prices have increased by more than 25% between 2019 and 2024, making predictable monthly lease payments more appealing. Technology adoption is also reshaping the operating model of leasing companies. Fleet management platforms, telematics-enabled pricing systems, and digital subscription services are improving fleet utilization and predictive maintenance capabilities.

Key Industry Highlights

- Vehicle Type Dominance: Sports utility vehicles (SUVs) are anticipated to dominate with nearly 42% market share in 2026, reflecting strong consumer preference for larger vehicles with enhanced safety features.

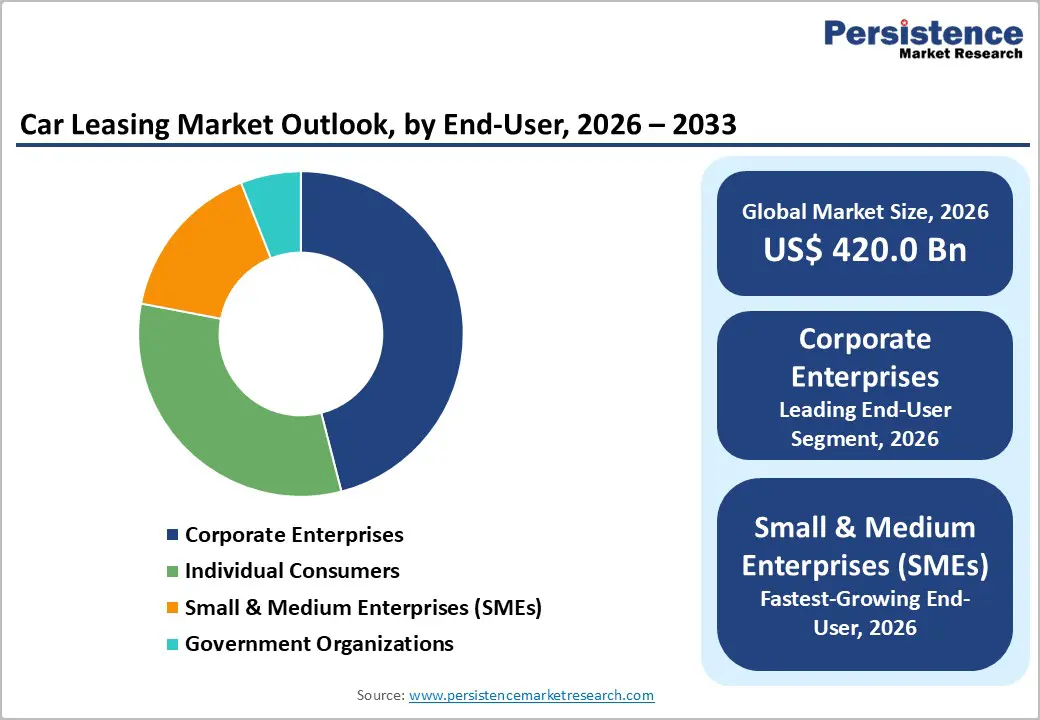

- End-User Leadership: Corporate enterprises are expected to lead with about 46% revenue share in 2026, as organizations continue outsourcing fleet ownership to leasing providers.

- Fastest-growing End-User: Small & medium-sized enterprises (SMEs) are likely to expand the fastest, with a nearly 9% CAGR through 2033, driven by increased demand for logistics fleets and flexible financing solutions.

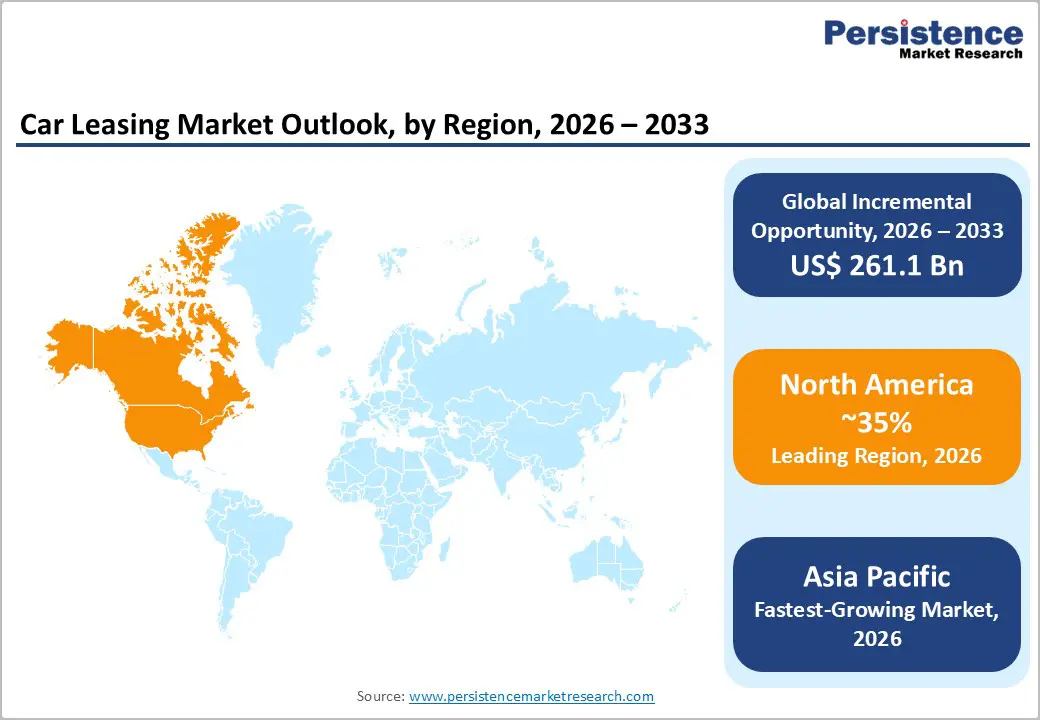

- Regional Landscape: North America is poised to command roughly 35% market share in 2026, owing to a mature automotive financing infrastructure.

- Fastest-growing Market: Asia Pacific is set to emerge as the fastest-growing market, with a CAGR of about 9% from 2026 to 2033, driven by rapidly expanding mobility services.

- Investment Outlook: Strategic investments in electric-vehicle fleet leasing, digital mobility subscription platforms, and advanced residual-value analytics are expected to shape competitive differentiation and profitability.

- September 2025: Ford Motor Company and General Motors launched dealer programs that enabled their financing arms to pre-purchase electric vehicles, allowing customers to continue receiving the US$ 7,500 U.S. federal EV tax credit through leasing deals.

| Key Insights | Details |

|---|---|

| Car Leasing Market Size (2026E) | US$ 426.0 Bn |

| Market Value Forecast (2033F) | US$ 687.0 Bn |

| Projected Growth (CAGR 2026 to 2033) | 7.1% |

| Historical Market Growth (CAGR 2020 to 2025) | 5.3% |

Market Factors - Growth, Barriers, and Opportunity Analysis

Corporate Fleet Electrification Programs Are Accelerating Leasing Adoption

Corporate decarbonization commitments are increasingly pushing companies toward vehicle leasing rather than direct ownership. Several multinational corporations are implementing science-based emissions targets aligned with frameworks from the Science Based Targets initiative (SBTi) and the United Nations Global Compact, which require reductions in Scope 1 and Scope 3 transport emissions. Leasing allows organizations to transition their fleets to electric vehicles without assuming long-term technology risk or uncertainty about battery residual value. Fleet electrification policies across the European Union (EU) are providing additional stimulus to the adoption of car leasing models.

Leasing providers are responding by introducing integrated EV fleet packages that include charging infrastructure, energy management software, and battery lifecycle monitoring. This model is reducing operational complexity for corporate clients while creating recurring service revenue streams for leasing firms. As electric vehicles remain technologically dynamic and residual values are uncertain, many companies are opting for three- to four-year leasing contracts that allow fleet upgrades as battery technology improves. This structural shift is expected to sustain long-term demand for leasing across developed markets.

Rising Vehicle Costs and Interest Rate Dynamics to Favor Leasing Models

Vehicle affordability trends are shifting consumers toward financing alternatives such as leasing. According to data from the U.S. Federal Reserve Economic Data (FRED), the average price of new vehicles in the United States rose from approximately US$ 36,000 in 2019 to over US$ 48,000 in 2024, reflecting supply chain disruptions, semiconductor shortages, and increased electrification costs. Higher prices are increasing the financial burden of ownership, particularly for urban consumers and small businesses. Leasing spreads these costs into predictable monthly payments and avoids depreciation risk, making it financially attractive.

Financial institutions and automakers are also increasingly integrating leasing into vehicle sales strategies. Automotive captive finance companies, such as those operated by global automakers, are providing competitive leasing rates supported by residual value forecasting and asset remarketing capabilities. These programs are improving customer acquisition and retention while enabling automakers to maintain stronger control over vehicle lifecycle management. As vehicle prices continue to rise globally, leasing penetration is expected to expand across both developed and emerging automotive markets.

Residual Value Volatility in Electric Vehicles Is Increasing Financial Risk

Residual value uncertainty remains a major structural challenge for leasing companies. Electric vehicle technology is evolving rapidly, creating uncertainty around long-term resale values. According to the International Transport Forum (ITF), depreciation rates for early EVs have historically been 10-20% higher than comparable internal combustion vehicles due to battery degradation concerns and rapid technology upgrades. Leasing companies must accurately forecast residual values to maintain profitability, and miscalculations can significantly affect balance sheets.

Advances in battery technology and government incentives are also driving price volatility in secondary vehicle markets. For example, aggressive EV price reductions by major manufacturers in 2023 and 2024 significantly impacted used EV valuations across North America and Europe. Leasing firms must therefore implement sophisticated residual value analytics and remarketing strategies to mitigate losses. Without accurate forecasting models, residual risk could limit aggressive expansion into EV leasing.

Interest Rate Volatility and Credit Risk Are Affecting Leasing Economics

The profitability of car leasing businesses is closely tied to interest rate conditions and credit risk. Leasing companies typically finance vehicle purchases through debt markets or bank credit facilities, making them sensitive to borrowing costs. According to the World Bank Global Economic Prospects report, global interest rates increased sharply between 2022 and 2024 as central banks tightened monetary policy to combat inflation. Higher borrowing costs increase lease payment structures and can reduce demand from cost-sensitive customers.

Credit risk is also becoming more significant as leasing expands into emerging markets and small-business segments. Defaults on lease contracts can lead to costly vehicle repossession and remarketing processes. Economic downturns may also increase delinquency rates among individual consumers and SMEs. Leasing providers are therefore investing heavily in risk-assessment algorithms and digital credit-scoring tools to manage portfolio exposure. Persistent interest rate volatility could constrain aggressive market expansion in the near term.

Emerging Markets to Lay the Foundations for High-Growth Leasing Ecosystems

Emerging automotive markets have become a hotbed of expansion opportunities for players in the car leasing market. Countries across Asia, Latin America, and parts of Eastern Europe are experiencing rapid urbanization and rising middle-class income levels. According to the World Bank, urban populations in Asia are projected to increase by more than 800 million people by 2035, creating strong demand for personal mobility and fleet services. However, vehicle ownership costs remain high relative to household income in many emerging economies, making leasing an attractive alternative.

Fleet leasing for ride-hailing services, logistics providers, and corporate mobility programs is growing rapidly in cities such as Jakarta, Bangkok, and Mexico City. Several leasing providers are partnering with mobility platforms and local financial institutions to expand access to vehicle financing. These markets are expected to contribute a substantial share of incremental demand, potentially representing over US$ 120 billion in additional leasing revenue globally by 2033. Strategic investments in localized financing models and digital leasing platforms are likely to unlock further growth.

Digital Mobility Platforms Are Creating Subscription-Based Leasing Models

Digital transformation is enabling new mobility financing models that combine leasing with subscription services. Technology platforms are allowing customers to access vehicles through flexible monthly subscriptions that include insurance, maintenance, and fleet management. According to the ITF, mobility-as-a-service (MaaS) platforms are expected to reshape urban transportation systems by integrating multiple mobility options within unified digital ecosystems.

Automakers and leasing companies are increasingly experimenting with flexible vehicle subscription programs targeted at urban professionals and corporate fleets. According to Christian Dahlheim, Volkswagen (VW) Financial Services CEO, the company is integrating rental operations more closely with leasing and subscription services across Europe to strengthen its mobility ecosystem and improve vehicle lifecycle management. The strategy enables VW to increase recurring revenue from short-term rentals, fleet leasing, and subscription models while maintaining stronger control over used-vehicle remarketing and customer relationships throughout the vehicle ownership cycle. As digital platforms scale, subscription-based leasing models could represent a growing share of the mobility financing market. Analysts estimate that these services could generate US$ 50-70 billion in annual leasing revenue globally by 2033, particularly in major metropolitan areas.

Category-wise Analysis

Vehicle Type Insights

SUVs are poised to dominate in 2026, accounting for approximately 42% of the car leasing market's revenue share. Consumer preferences for larger vehicles with enhanced safety features, higher seating positions, and greater cargo capacity are driving demand across North America, Europe, and Asia. Automakers are also prioritizing SUV production due to higher margins and global consumer demand trends. Leasing companies are therefore expanding SUV offerings across both consumer and corporate fleet programs. In corporate mobility programs, SUVs are increasingly used for executive transportation and field service operations because they offer durability and versatility across different driving conditions.

Electric vehicles are likely to represent the fastest-growing vehicle type in leasing, with an estimated CAGR of around 13% between 2026 and 2033. Leasing has become a preferred financing mechanism for EV adoption because it reduces consumer exposure to battery depreciation and technology obsolescence. Governments across Europe, China, and the United States are providing incentives for EV purchases and corporate fleet electrification, which is accelerating leasing demand. Leasing firms are also integrating EV-specific services, such as charging infrastructure management and battery health monitoring, creating additional value for customers.

End-User Insights

Corporate enterprises are expected to account for an estimated 46% of the car leasing market share in 2026. Corporate fleets rely on leasing to manage capital expenditure while maintaining operational flexibility. Sales teams, logistics companies, consulting firms, and service providers frequently use leased vehicles to support business operations. Leasing allows organizations to outsource fleet maintenance, insurance management, and asset depreciation, improving cost predictability. Organizations are also increasingly integrating vehicle leasing programs into compensation structures because they reduce upfront vehicle costs, provide predictable monthly payments, and offer tax-efficient salary packaging that improves employees’ take-home income. In Europe, corporate fleet programs account for a majority of new vehicle registrations, reinforcing the importance of leasing in enterprise mobility strategies.

Small & medium-sized enterprises are expected to represent the fastest-growing leasing end-user, expanding at an estimated CAGR of approximately 9% between 2026 and 2033. SMEs often lack access to large capital reserves or favorable financing options for vehicles, making leasing an attractive alternative. Digital leasing platforms and fintech partnerships are also enabling SMEs to access faster credit approvals and flexible lease structures. For example, an Indian used-car leasing startup, PumPumPum, provides subscription-based leasing for pre-owned vehicles with bundled services such as maintenance and insurance, targeting young professionals, small businesses, and corporate fleets. As small businesses increasingly rely on vehicle fleets for delivery services, field operations, and logistics, leasing demand within this segment is expected to grow significantly.

Regional Insights

North America Car Leasing Market Trends

North America is expected to account for approximately 35% of the car leasing market value in 2026, making it the largest hub for vehicle leasing products and services. The United States dominates regional demand due to high vehicle ownership rates, a well-developed automotive financing infrastructure, and a strong presence of captive finance companies operated by major automakers. According to the U.S. Federal Reserve, leasing accounted for nearly 23% of new-vehicle financing transactions in the United States in 2024, underscoring its importance in automotive sales strategies.

Corporate fleet management programs and ride-hailing vehicle financing are major drivers of demand in the region. Companies are increasingly outsourcing fleet operations to leasing providers that offer integrated maintenance and telematics services. EV adoption is also accelerating due to federal incentives introduced under the Inflation Reduction Act, which provides tax credits for EV purchases and fleet electrification. Leasing firms are leveraging these incentives to expand EV leasing portfolios. Market growth here is also being supported by digital leasing platforms, the expansion of subscription-based vehicle services, and rising vehicle prices, which are encouraging consumers to adopt leasing rather than outright purchases.

Europe Car Leasing Market Trends

Europe is projected to become the second-largest market for car leasing, accounting for an estimated 32% of global sales in 2026. Leasing penetration in Europe is particularly high among corporate fleets, where vehicle leasing is widely used as part of employee mobility benefits and company car programs. According to the ACEA, corporate fleets account for a majority of new passenger car registrations across many European markets. Leasing companies are therefore deeply integrated into corporate mobility ecosystems. The region is also experiencing rapid electrification of vehicle fleets due to stringent emissions regulations under the EU’s Fit for 55 climate package.

A growing number of European governments are implementing policies that encourage businesses to transition from company cars to low-emission or EVs. Key growth drivers include Germany, the U.K., France, and the Netherlands, where strong regulatory frameworks and high corporate fleet adoption rates sustain demand for leasing services. France, for instance, relaunched its “social leasing” EV program to enable low-income households to access electric cars through subsidized leasing contracts. Under the program, eligible households can lease an EV for as little as €95- €200 per month, with no upfront payment, supported by state subsidies of up to €7,000 per vehicle to reduce monthly costs and accelerate the transition to low-emission mobility. Leasing firms are playing a critical role by providing EV financing solutions and fleet management services.

Asia Pacific Car Leasing Market Trends

Asia Pacific is expected to be the fastest-growing regional market for car leasing models, with an estimated CAGR of approximately 9% between 2026 and 2033, on the back of robust automotive ecosystems of China, Japan, South Korea, and India. China continues to dominate regional vehicle demand and remains the world’s largest automobile market. Leasing providers are expanding fleet financing programs that support ride-hailing platforms, corporate mobility services, and urban logistics operators. National policies are also accelerating the transition toward electric mobility. Government incentives and industrial policies are encouraging leasing companies to develop financing products for EVs that are reducing adoption barriers for both businesses and consumers. In developed markets such as Japan and South Korea, established leasing companies are focusing on enterprise fleet management services and integrated mobility solutions.

Emerging economies across South Asia and Southeast Asia are increasingly adopting leasing as a practical strategy for vehicle acquisition. Startups, technology firms, and logistics operators are expanding their fleets but are prioritizing capital efficiency. Leasing arrangements are helping these organizations access vehicles without large upfront investments while maintaining operational flexibility. Countries such as India, Indonesia, Thailand, and Vietnam are witnessing rising demand for fleet financing among e-commerce delivery companies and mobility service providers. Digital platforms are also transforming the leasing ecosystem by streamlining vehicle selection, credit approvals, and fleet management through integrated online systems. Partnerships between leasing companies and financial technology (fintech) firms are improving access to credit for SMEs and self-employed drivers. These developments are enabling broader market participation and are strengthening the region’s leasing infrastructure.

Competitive Landscape

The global car leasing market structure is moderately fragmented, featuring a diverse group of automotive captive finance companies, independent leasing providers, and fleet management specialists. Large multinational leasing organizations dominate corporate fleet contracts as they possess extensive vehicle remarketing networks and sophisticated residual value forecasting systems. Leading companies are typically holding individual market shares ranging between 5% and 8%, while smaller regional providers are focusing on niche markets and specialized fleet segments such as commercial service vehicles or employee mobility programs. Automotive manufacturers are also strengthening their financial arms to maintain direct customer relationships throughout the vehicle lifecycle. These divisions, often structured as original equipment manufacturer (OEM) captive finance entities, benefit from preferential access to vehicle supply and manufacturer-backed incentives.

Competitive dynamics are increasingly evolving as digital technologies are transforming leasing operations and customer engagement models. Leasing providers are deploying advanced analytics platforms that improve residual value estimation, fleet utilization monitoring, and predictive maintenance planning. These capabilities are helping companies reduce operational costs while improving asset performance across large vehicle fleets. Partnerships with mobility service providers and fintech companies are becoming more common as leasing firms expand into flexible vehicle access programs. Subscription-based leasing services are allowing customers to change vehicles or terminate contracts with minimal administrative friction.

Key Industry Developments

- In March 2026, Chinese automotive brands Omoda and Jaecoo teamed up with Australian salary-packaging provider Smartgroup to introduce novated leasing options through their dealership network. The initiative is leveraging Australia’s Fringe Benefits Tax (FBT) exemption for eligible electric vehicles, which is lowering effective ownership costs and making novated leasing an increasingly attractive financing route for EV buyers.

- In January 2026, Kia India partnered with Avis Leasing to expand its vehicle leasing and subscription offerings under the Kia Lease program, providing flexible contracts with tenures of 36-60 months, multiple mileage options, and no upfront payment. The collaboration aims to strengthen Kia’s mobility ecosystem and broaden access to alternative vehicle ownership models in India.

- In December 2025, BNP Paribas entered exclusive negotiations to acquire Athlon, the car-leasing subsidiary of Mercedes-Benz Group, in a deal valued at about € 1 billion (US$ 1.2 billion) to strengthen its European vehicle leasing operations through its Arval unit. The acquisition would add roughly 400,000 vehicles to Arval’s fleet, bringing its total to nearly 2.3 million.

Companies Covered in Car Leasing Market

- ALD Automotive S.A.

- LeasePlan Corporation N.V.

- Hertz Global Holdings, Inc.

- Enterprise Holdings, Inc.

- Toyota Financial Services Corporation

- Volkswagen Financial Services AG

- BMW Group Financial Services

- Mercedes-Benz Mobility AG

- Arval Service Lease S.A.

- Santander Consumer Finance S.A.

- Element Fleet Management Corp.

- Athlon Car Lease International B.V.

- Sixt SE

- Ayvens Group N.V.

Frequently Asked Questions

The global car leasing market is projected to reach US$ 426.0 billion in 2026.

The shift of vehicle acquisition models toward structured mobility financing, and growing preference for leasing as a central vehicle procurement strategy for corporate fleets as well as individual drivers are driving the market.

The market is poised to witness a CAGR of 7.1% from 2026 to 2033.

Enablement of companies to manage battery depreciation risks by leasing models, tightening implementation of emissions reduction policies and corporate decarbonization frameworks, and reduction in vehicle affordability are key market opportunities.

ALD Automotive S.A., LeasePlan Corporation N.V., Hertz Global Holdings, Inc., and Enterprise Holdings, Inc. are some of the key players in the market.