- Home Care & Utilities

- Built-in Hobs Market

Built-in Hobs Market Size, Share, and Growth Forecast 2026 - 2033

Built-in Hobs Market by Product Type (Gas Hobs, Electric Hobs, Induction Hobs, Ceramic Hobs, Hybrid Hobs), Fuel Type (Natural Gas, LPG, Electric), Installation Type (Built-in, Modular/Semi-integrated, Freestanding), End-User (Residential, Commercial), and Regional Analysis, 2026 - 2033

Built-in Hobs Market Size and Trend Analysis

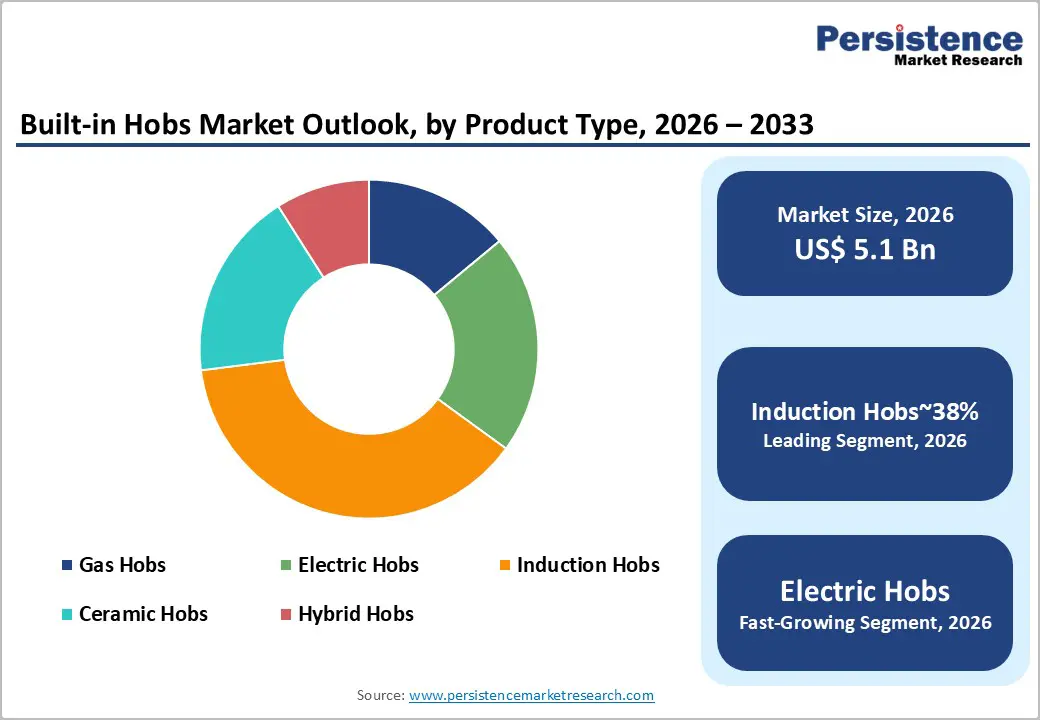

The global built-in hobs market size is likely to be valued at US$ 5.1 billion in 2026 and is expected to reach US$ 7.2 billion by 2033, growing at a CAGR of 5.1% during the forecast period from 2026 to 2033. The Built-in Hobs Market is progressing on a stable, multi-driver growth trajectory, underpinned by the global expansion of modular kitchen design culture, rapid adoption of induction and smart-electric cooking technology, and strong residential construction activity across urbanizing economies.

Key Industry Highlights:

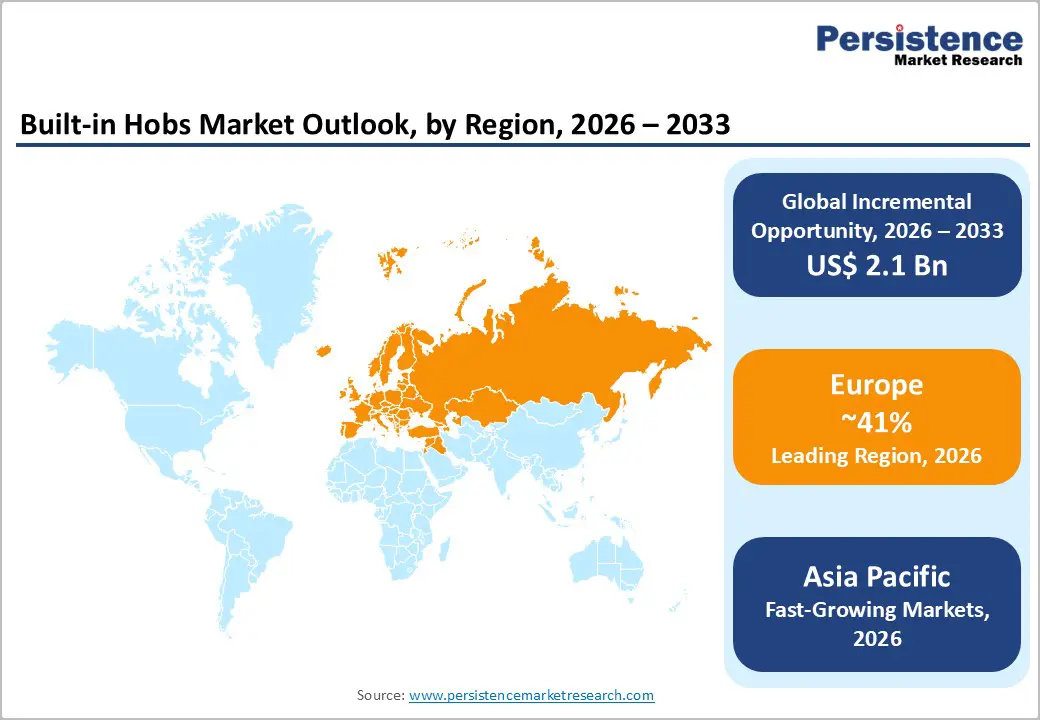

- Leading Region: Europe leads the global Built-in Hobs Market with 41% share, anchored by premium induction hob innovation from BSH Hausgeräte, Miele, and Siemens, EU energy efficiency regulation driving gas-to-induction transition, and high kitchen renovation spending in Germany, France, U.K., and Spain

- Fastest-Growing Region: Asia Pacific is the fastest-growing region through 2033, driven by China's urban residential construction scale, Japan's projected 7.0% CAGR in built-in hob demand through 2035, and India's rapidly expanding modular kitchen market growing at approximately 10% CAGR through 2032

- Leading Segment: Induction Hobs dominate the By Product Type category with approximately 38% revenue share, driven by 85% energy efficiency, smart connectivity features, premium design aesthetics, and direct alignment with government policies restricting new gas appliance installations across major residential markets

- Fastest-Growing Segment: Electric Hobs are also the fastest-growing product type segment, with approximately 40% of consumers now actively preferring electric over gas systems, reinforced by new launches from Miele and Siemens at IFA 2025, incorporating AI cookware intelligence and integrated downdraft extraction

- Key Opportunity: The gas phase-out policy wave across EU member states and U.S. state-level gas restriction mandates represents the most significant structural market opportunity, creating a large, policy-guaranteed replacement demand pipeline for electric and induction built-in hob manufacturers through the 2033 forecast horizon.

| Key Insights | Details |

|---|---|

|

Built-in Hobs Market Size (2026E) |

US$ 5.1 Billion |

|

Market Value Forecast (2033F) |

US$ 7.2 Billion |

|

Projected Growth CAGR (2026–2033) |

5.1% |

|

Historical Market Growth (2020–2025) |

4.6% |

DRO Analysis

Drivers - Induction Hob Adoption Accelerated by Superior Energy Efficiency and Tightening Regulatory Standards

The shift from traditional gas and electric coil hobs to induction cooking systems is a major factor driving growth in the Built-in Hobs Market. Induction technology heats cookware directly using electromagnetic energy, achieving energy efficiency of 85%, which is much higher than gas stoves and electric coil hobs. This results in noticeable energy savings and reduced carbon emissions for households.

At the same time, government regulations are supporting this transition. For example, the European Union’s Ecodesign Regulation is pushing for better energy performance in household appliances, while several countries are planning to phase out gas appliances in new homes. Consumer preferences are also shifting, with around 40% of buyers now choosing induction hobs due to their efficiency and safety. These combined regulatory and consumer trends are steadily increasing the adoption of induction hobs across the global market.

Rising Urbanization and Modular Kitchen Penetration Driving Structural Volume Demand

The Built-in Hobs Market is growing strongly due to increasing urbanization and the rising popularity of modular kitchens across both developed and emerging economies. As more people move to cities, there is a growing demand for modern housing with well-designed kitchen spaces. Built-in hobs fit perfectly into modular kitchens as they are integrated into countertops, offering a clean look, better space utilization, and easy maintenance.

These features make them a preferred choice among homeowners and interior designers. In countries like India, the modular kitchen market is expanding at a strong pace, supported by rising incomes, urban housing development, and lifestyle upgrades. Similarly, in Japan, demand for built-in hobs is expected to grow steadily, driven by residential renovations and new apartment construction. These trends are creating long-term and stable demand for built-in hobs across different product categories globally.

Restraints - High Installation and Retrofit Costs Limiting Adoption in Cost-Sensitive Market Segments

One of the key challenges in the Built-in Hobs Market is the high installation and retrofit cost, especially for induction hobs. Many homes, particularly older properties, require electrical upgrades such as dedicated circuits to support induction systems, which increases the overall installation cost beyond the appliance price. In cost-sensitive regions like Latin America, Southeast Asia, and parts of Eastern Europe, this added expense can discourage consumers from purchasing or upgrading to built-in hobs.

The older homes may not have suitable kitchen layouts, cabinet sizes, or ventilation systems that match modern built-in hob requirements. This means homeowners often need to invest in additional renovations, making the transition more complex and expensive. As a result, these costs and infrastructure challenges slow down adoption rates and delay replacement cycles, especially in markets where affordability remains a key decision factor for consumers.

Gas Infrastructure Dependency and Consumer Habitual Preference in Developing Markets

In many developing countries, strong reliance on gas infrastructure continues to limit the adoption of electric and induction built-in hobs. Well-established natural gas pipelines and LPG distribution networks make gas cooking convenient and widely accessible for households. At the same time, many consumers prefer gas cooking because they are familiar with it and value features such as visible flame control and compatibility with traditional cookware.

Cooking habits and cultural preferences also play an important role in slowing the shift toward induction technology. In addition, in countries such as India and parts of the Middle East and Latin America, government subsidies on gas further reduce its cost, making it more economical compared to electric alternatives. These factors reduce the financial and practical motivation for consumers to switch, slowing down the growth of induction and electric built-in hobs in these markets.

Opportunities - Smart and Connected Induction Hobs as a Premium Segment with Rapidly Expanding Consumer Appeal

The growing integration of smart technology into induction hobs presents a major opportunity in the Built-in Hobs Market. Modern consumers, especially in premium segments, are increasingly interested in connected appliances that offer convenience and advanced features. Smart induction hobs now come with touchscreen controls, mobile app connectivity, automatic pan detection, and AI-based cooking assistance, which enhance the overall cooking experience. These features also allow manufacturers to charge higher prices, increasing profitability. Leading brands are actively investing in this segment.

Siemens introduced its iQ500 inductionAir Plus cooktop with integrated ventilation and app connectivity, while Miele launched its KM 8000 induction hob with intelligent temperature control. These innovations highlight the industry’s focus on premium, connected solutions. As demand for smart homes continues to grow, connected induction hobs are expected to become a high-growth and high-margin segment in the market.

Electrification Policy and Gas Phase-Out Mandates Creating Structural Replacement Demand Across Mature Markets

Government policies promoting electrification and restricting gas usage are creating strong growth opportunities in the Built-in Hobs Market, particularly in developed regions. In Europe, countries such as the Netherlands and Denmark are already limiting new gas connections in residential buildings, encouraging the adoption of electric and induction hobs. These efforts are part of broader environmental goals under initiatives like the European Green Deal, which focuses on reducing carbon emissions and improving energy efficiency.

In the United States, states like California have introduced policies to restrict gas connections in new construction projects. These regulations are pushing builders, developers, and homeowners to choose electric or induction hobs as the standard option. This policy-driven shift is creating a long-term replacement cycle, offering significant growth potential for manufacturers that can deliver energy-efficient, technologically advanced, and competitively priced products.

Category-wise Analysis

By Product Type Insights

Induction hobs have become the leading product type in the Built-in Hobs Market, contributing around 38% of total revenue and showing the fastest growth among all categories. Their popularity is driven by multiple advantages, including high energy efficiency, faster heating, precise temperature control, and easy-to-clean flat surfaces. These benefits align well with modern consumer needs and government energy efficiency goals.

Surveys show that about 40% of consumers now prefer induction hobs over gas due to safety and energy-saving features, indicating a clear shift in buying behavior. Major companies such as BSH Hausgeräte, Miele, Siemens, and Electrolux are heavily investing in induction technology, further strengthening their market position. While gas hobs still hold a significant share, especially in Asia Pacific and Latin America, their dominance is gradually declining as more consumers switch to advanced induction solutions in both new installations and renovation projects.

By Fuel Type Insights

The electric segment leads the Built-in Hobs Market by fuel type, accounting for approximately 52% of total revenue. This dominance is mainly due to the widespread adoption of induction and ceramic electric hobs, which are commonly used in modern kitchens. Electric hobs are increasingly preferred by architects and designers because they eliminate the need for gas pipelines, simplify installation, and support cleaner, emission-free cooking.

These features also align with green building standards and sustainability goals. In countries like Japan, electric hobs already represent a significant share of demand, supported by government policies promoting all-electric homes. Although natural gas and LPG hobs continue to have a large installed base, their market share is gradually decreasing due to stricter energy regulations and the growing focus on electrification. This trend is expected to continue as more regions adopt policies encouraging energy-efficient electric cooking solutions.

By Installation Type Insights

Built-in hobs dominate the installation type segment, accounting for about 58% of total market revenue. Their popularity is closely linked to the growing demand for modular kitchens and modern home designs. Built-in hobs are installed directly into countertops, creating a sleek and seamless appearance that enhances the overall kitchen aesthetic. They are widely used in premium residential projects, luxury apartments, and high-end renovations where design and functionality are equally important.

These hobs also support integrated ventilation systems and match well with other built-in appliances, making them a preferred choice for complete kitchen solutions. Meanwhile, the modular or semi-integrated segment is growing rapidly, especially in markets like India and Southeast Asia. In these regions, consumers often purchase complete kitchen packages that include cabinets, countertops, and appliances, driving increased adoption of built-in hob solutions as part of bundled offerings.

By End-user Insights

The residential segment is the largest end-user category in the Built-in Hobs Market, accounting for nearly 79% of total revenue. This strong demand is driven by increasing urbanization, rising housing construction, and a growing preference for modern kitchen appliances. As more people move into cities, the demand for new homes and apartments increases, leading to higher adoption of built-in hobs. In developed markets, renovation activities are also contributing significantly, as homeowners upgrade their kitchens with advanced induction systems.

The ongoing shift from gas to induction cooking is accelerating product replacement cycles. According to global housing data, urban growth is strongest in regions like Asia, Africa, and Latin America, further supporting demand. The commercial segment, including restaurants and hotels, is also growing steadily as businesses adopt induction hobs to improve efficiency, enhance safety, and reduce heat levels in professional kitchens.

Regional Insights

North America Built-in Hobs Market Trends

North America is witnessing a significant shift toward electric and induction hobs, mainly driven by regulatory changes and evolving consumer preferences. In the United States, policies restricting gas connections, especially in states like California, are encouraging the adoption of electric cooking solutions in new homes. At the same time, high-income consumers are investing more in kitchen renovations, boosting demand for premium built-in hobs.

The growing popularity of smart homes is also supporting this trend, as consumers prefer appliances that offer app control and advanced features. In Canada, government initiatives promoting clean energy are further encouraging the replacement of gas appliances with efficient electric alternatives. The region is home to several major appliance brands, creating a competitive and innovation-driven market. Overall, the shift toward energy-efficient, smart, and sustainable kitchen solutions is driving strong growth in the North America built-in hobs market.

Europe Built-in Hobs Market Trends

Europe is the most advanced market for induction hobs and leads globally in terms of innovation and adoption. Germany plays a key role, with major manufacturers like BSH Hausgeräte, Miele, and Siemens driving product development and technological advancements. These companies regularly introduce new products at major industry events, maintaining Europe’s leadership in this segment. Other countries such as France and the United Kingdom are also seeing increased demand for energy-efficient cooking appliances due to strict building regulations.

Spain is emerging as a fast-growing market, supported by urban development and rising consumer awareness of energy savings. The European Union’s Ecodesign Regulation is further pushing manufacturers to improve product efficiency, creating a competitive advantage for advanced induction hobs. Overall, strong regulatory support and high consumer awareness are making Europe a key growth region for built-in hob manufacturers.

Asia Pacific Built-in Hobs Market Trends

Asia Pacific is the largest and fastest-growing market for built-in hobs, driven by rapid urbanization, increasing disposable incomes, and rising demand for modern kitchen solutions. China leads the region with strong housing construction activity and growing interest in premium appliances among urban consumers. Government initiatives promoting energy efficiency are also encouraging the adoption of electric and induction hobs.

Japan is experiencing steady growth, supported by residential renovations and a shift toward all-electric homes. Meanwhile, India is emerging as a high-growth market, with increasing adoption of modular kitchens and premium appliances in urban areas. The built-in kitchen appliances market in India is expected to grow significantly in the coming years, supported by lifestyle changes and higher consumer spending. Overall, strong economic growth and changing consumer preferences are driving demand for built-in hobs across the Asia Pacific region.

Competitive Landscape

The global built-in hobs market is moderately consolidated, with several global players leading through innovation and strong brand positioning. Key companies include BSH Hausgeräte, Miele, Electrolux, Siemens, Whirlpool, Samsung, LG, and Haier. These companies compete by offering advanced induction technologies, smart connectivity features, and high-quality materials such as durable ceramic glass surfaces.

Recent product launches, such as Miele’s intelligent cookware system and Siemens’ connected cooktops, highlight the focus on innovation. Companies are also adopting new business strategies, including selling complete kitchen appliance ecosystems and expanding direct-to-consumer channels. In addition to global brands, regional players like Elica, Smeg, and Gorenje compete by focusing on unique designs and niche premium segments. Overall, competition in the market is driven by technology, product design, and the ability to meet evolving consumer demand for smart and energy-efficient kitchen solutions.

Key Developments:

- In September, 2025: Miele & Cie. KG introduced the KM 8000 induction hob at IFA 2025, featuring the M Sense system for automatic temperature control and power adjustment. The launch also included the modular outdoor kitchen concept ‘Dreams’, strengthening its premium innovation positioning.

- In December, 2024: Siemens AG launched the iQ500 inductionAir Plus cooktop, combining built-in downdraft ventilation, BratSensor Plus precision cooking, durable diamondProtect coating, and Home Connect integration, specifically targeting premium smart kitchen solutions and enhancing user convenience and energy-efficient cooking experiences.

- In October, 2024: BSH Hausgeräte GmbH expanded its Bosch and Siemens portfolios by introducing advanced induction hobs with AI-assisted cooking and ovens with steam and pyrolytic cleaning features, aligning with integrated kitchen trends and strengthening its presence in modern, premium kitchen appliance segments globally.

Companies Covered in Built-in Hobs Market

- Whirlpool Corporation

- Samsung Electronics

- BSH Hausgeräte GmbH

- Miele & Cie. KG

- Siemens AG

- Electrolux AB

- LG Electronics

- Panasonic Corporation

- Haier Group

- Fisher & Paykel Appliances

- Smeg S.p.A.

- Elica S.p.A.

- Gorenje Group

- GE Appliances

Frequently Asked Questions

The global Built-in Hobs Market is estimated at US$ 5.1 Billion in 2026 and is projected to reach US$ 7.2 Billion by 2033, growing at a CAGR of 5.1%, driven by induction hob adoption, rising urbanization, modular kitchen expansion, and tightening energy efficiency regulations across Europe, North America, and Asia Pacific markets.

The primary growth drivers are the accelerating consumer and policy-led transition to induction hobs, which achieve 85% energy efficiency versus 45% for gas, and the sustained expansion of modular kitchen culture in urbanizing markets. EU Ecodesign Regulation, gas restriction policies in California and multiple EU member states, and smart home integration trends are collectively accelerating the replacement of gas and basic electric hobs with premium induction systems.

Induction Hobs lead the By Product Type segment with approximately 38% revenue share, underpinned by superior energy conversion efficiency, precise temperature control, fast heating response, easy-clean ceramic glass surfaces, and strong alignment with EU energy performance regulations. Leading OEMs including Miele, Siemens, and BSH Hausgeräte are concentrating premium product development investment in induction platforms with smart connectivity and AI-assisted cooking features.

Europe leads the global Built-in Hobs Market, anchored by Germany's world-class appliance manufacturing base, home to BSH Hausgeräte, Miele, and Siemens, and supported by EU Ecodesign energy regulations, progressive gas phase-out policies, and strong kitchen renovation markets in France, U.K., Spain, and Germany that consistently drive premium induction hob specifications in both new builds and refurbishment projects.

The most significant opportunity is the policy-driven replacement demand wave created by gas appliance phase-out regulations across EU member states and multiple U.S. states. This legislative framework creates a guaranteed, large-scale structural substitution market for induction and electric built-in hob manufacturers, particularly those offering smart, app-connected, energy-rated platforms that qualify under ENERGY STAR and EU appliance energy label frameworks.

The leading participants include BSH Hausgeräte GmbH, Miele & Cie. KG, Siemens AG, Electrolux AB, Whirlpool Corporation, Samsung Electronics, LG Electronics, Haier Group, Panasonic Corporation, GE Appliances, Fisher & Paykel Appliances, Smeg S.p.A., Elica S.p.A., and Gorenje Group, with BSH Hausgeräte and Miele commanding the leading premium technology positions globally through proprietary induction platforms and smart kitchen ecosystem strategies.