- Automotive Components & Materials

- Automotive Valves Market

Automotive Valves Market Size, Share, and Growth Forecast, 2026 - 2033

Automotive Valves Market by Product Type (Mono-metallic Valves, Others), Vehicle Type (Two-Wheeler, Others), Material Used (Steel, Others), Sales Channel (Original Equipment Manufacturer [OEM], Aftermarket), and Regional Analysis for 2026 – 2033

Automotive Valves Market Size and Trends Analysis

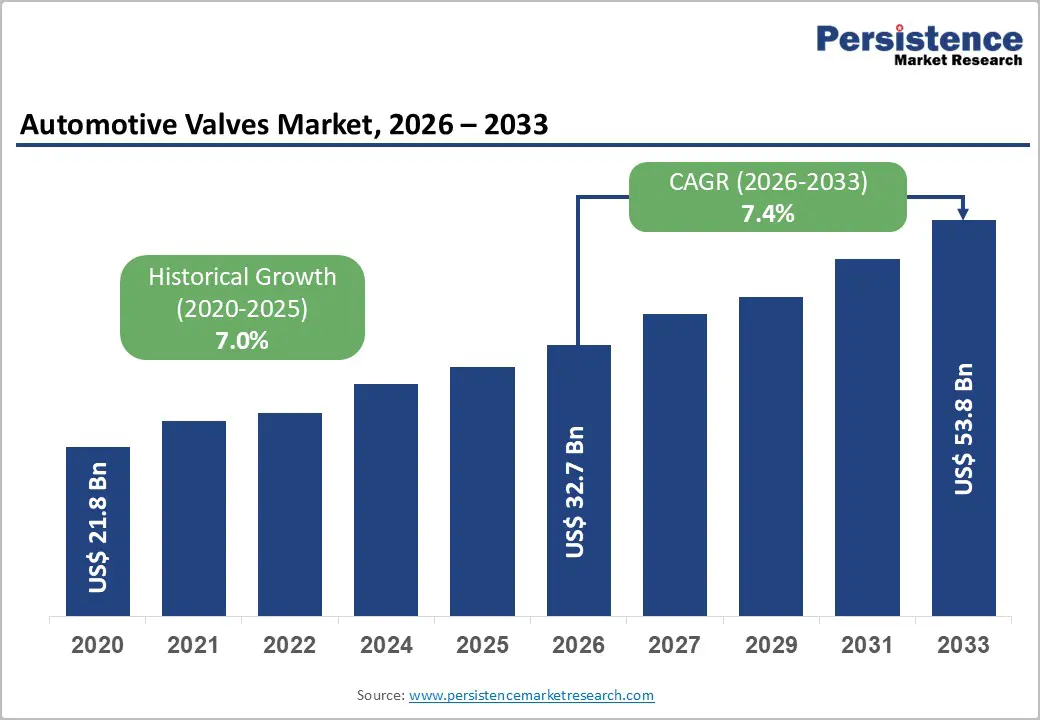

The global automotive valves market size is likely to be valued at US$32.7 billion in 2026, and is expected to reach US$53.8 billion by 2033, growing at a CAGR of 7.4% during the forecast period from 2026 to 2033, driven by the increasing prevalence of stringent emission norms, rising vehicle production volumes, and growing adoption of advanced valve technologies in turbocharged and hybrid powertrains. Growing demand for high-performance, lightweight automotive valves, especially hollow valves and plated/coated variants for passenger cars and HCVs, is accelerating adoption across OEM and aftermarket channels.

Advances in sodium-filled hollow valves and nickel-alloy materials are further increasing uptake by improving thermal management and durability under high-temperature conditions. The increasing recognition of automotive valves as critical to engine efficiency, emissions compliance, and fuel economy in the emerging EV transition and BS-VI/China VI markets remains a major driver of market growth.

Key Industry Highlights:

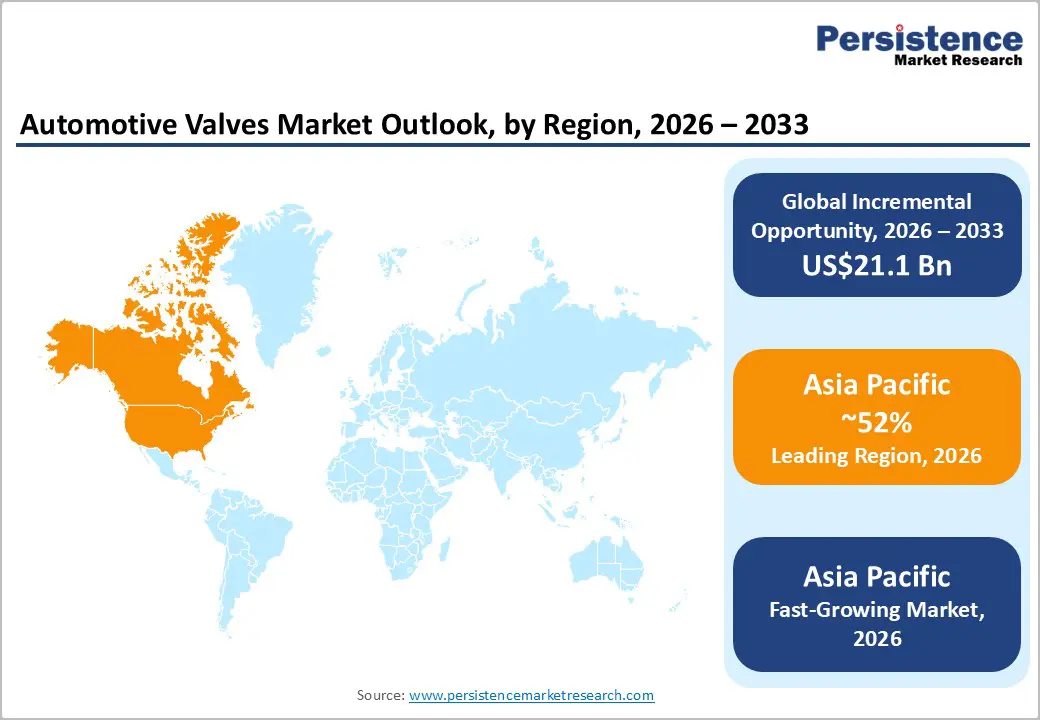

- Leading Region: Asia Pacific, anticipated to account for a 52% market share in 2026, driven by a dominant vehicle production base, rapid HCV and passenger car growth, and strong demand in China and India.

- Fastest-growing Region: Asia Pacific, fueled by expanding emission-compliant engine platforms, rising aftermarket demand, and growing investments in valve manufacturing.

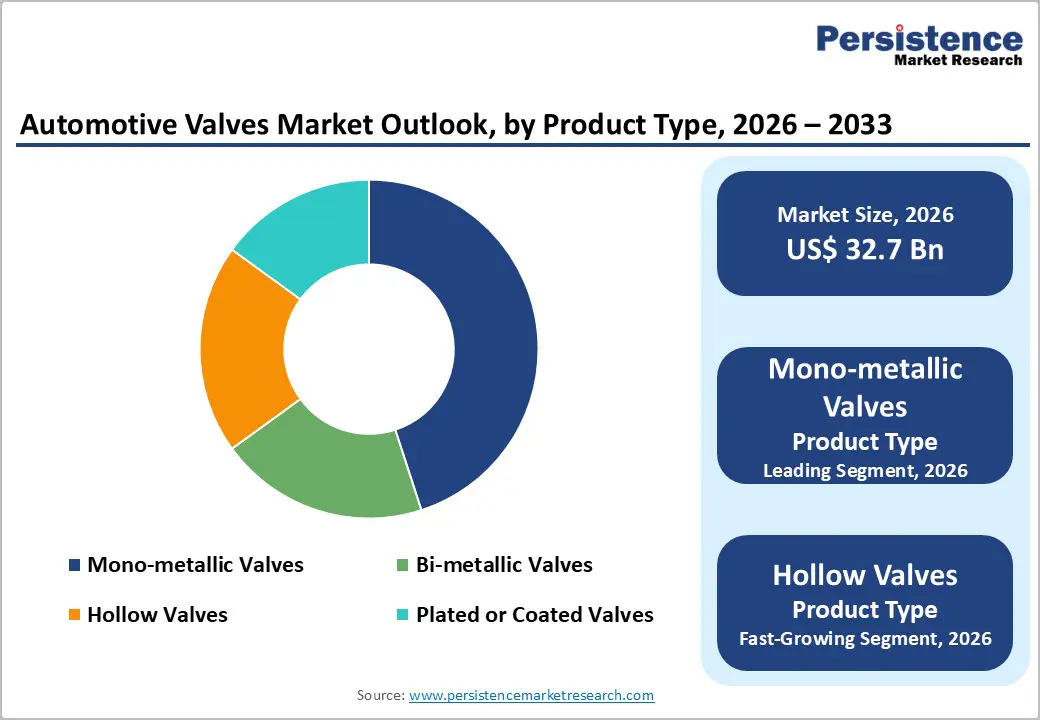

- Dominant Product Type: Mono-metallic valves, to hold approximately 45% of the market share, as they remain the cost-effective workhorse in mass-volume applications.

- Leading Vehicle Type: Passenger car, to contribute nearly 48% of the market revenue, due to the highest production volumes and valve count per vehicle.

- In January 2026, Tata Motors reported that HCV truck sales jumped about 41% year-on-year, with 12,691 heavy trucks sold compared to 8,990 in January 2025, driven by increased infrastructure activity and long-haul freight demand.

| Report Attribute | Details |

|---|---|

|

Automotive Valves Market Size (2026E) |

US$32.7 Bn |

|

Market Value Forecast (2033F) |

US$53.8 Bn |

|

Projected Growth CAGR (2026-2033) |

7.4% |

|

Historical Market Growth (2020-2025) |

7.0% |

Market Factors – Growth, Barriers, and Opportunity Analysis

Growth Analysis – Stringent Emission Norms and Turbocharged Engine Proliferation

Stringent emission norms have become a powerful force reshaping engine design and vehicle engineering across global markets. Governments are tightening limits on carbon dioxide, nitrogen oxides, and particulate emissions to address air quality concerns and climate change commitments. As a result, automakers are under pressure to extract higher efficiency from smaller engines while maintaining performance levels that consumers expect. Traditional large-displacement engines struggle to meet these requirements without significant penalties in fuel consumption and emissions.

Turbocharged engines have emerged as a practical response to this regulatory landscape. By forcing additional air into the combustion chamber, turbochargers enable smaller engines to produce power comparable to larger naturally aspirated units. This downsizing approach reduces fuel consumption under normal driving conditions, thereby directly supporting compliance with emission standards. Advancements in turbo technology, such as variable-geometry turbines, improved thermal management, and electronic control systems, have addressed earlier concerns regarding turbo lag, durability, and drivability. The proliferation of turbocharged engines is also influenced by consumer demand for vehicles that balance efficiency with responsive performance.

Rising Aftermarket Demand and Vehicle Longevity

Rising aftermarket demand is closely linked to the increasing longevity of vehicles, as modern automobiles are designed to remain operational for longer periods than in the past. Improvements in engine engineering, corrosion protection, electronic reliability, and manufacturing quality have extended average vehicle lifespans, thereby encouraging owners to retain their vehicles well beyond the initial warranty period. The focus of spending gradually shifts from new vehicle purchases to maintenance, repair, and replacement of worn components.

The need for regular servicing and component replacement increases, thereby directly stimulating demand in the aftermarket. Components such as filters, brake systems, suspension parts, sensors, and engine-related components experience higher wear over time and must be replaced to ensure safety, performance, and regulatory compliance. Rising costs of new vehicles have made repairs and upgrades a more economical choice for consumers, further strengthening aftermarket activity.

Barrier Analysis – High Raw Material Costs and Supply Chain Volatility

High raw material costs and supply chain volatility have become persistent challenges for manufacturing and industrial sectors worldwide. Prices of key inputs such as steel, aluminum, copper, plastics, and specialty chemicals are increasingly influenced by geopolitical tensions, fluctuations in energy prices, environmental regulations, and demand imbalances. These factors make raw material pricing unpredictable, complicating cost planning and reducing margin stability for manufacturers.

Supply chain volatility further amplifies this pressure. Disruptions caused by trade restrictions, transportation bottlenecks, labor shortages, and extreme weather events can delay the availability of critical materials and components. Even short-term interruptions may force manufacturers to rely on spot purchases at higher prices or alternative suppliers with limited capacity. This instability increases lead times and raises inventory carrying costs, placing additional strain on operational efficiency. To manage these risks, companies are adopting diversified sourcing strategies, increasing local or regional procurement, and investing in supplier relationships to ensure continuity. Some manufacturers are also redesigning products to reduce material intensity or substitute scarce inputs with more readily available alternatives.

Transition to Electric Vehicles to reduce Valve Content

The transition to electric vehicles is fundamentally altering the demand landscape for traditional internal-combustion-engine components, including engine valves. In conventional vehicles, valves play a critical role in controlling air and fuel intake as well as exhaust gas flow, making them essential for engine operation. However, battery-electric vehicles eliminate the combustion process entirely, thereby eliminating the need for complex valvetrain systems and the multiple valves associated with them.

As electric vehicle adoption accelerates, overall vehicle production growth is increasingly driven by powertrains that rely on electric motors, inverters, and battery systems rather than mechanical engine parts. This shift directly reduces valve content per vehicle, as fully electric models require none, and hybrid vehicles often use smaller, less complex engines with fewer valves compared to traditional gasoline or diesel engines. Even where internal combustion engines remain part of the drivetrain, they are optimized for efficiency rather than high performance, further limiting valve complexity and volume.

Opportunity Analysis – Growth in Hollow Valves and Advanced Coatings for Turbo/Hybrid Engines

The growth in hollow valves and advanced coatings is being driven by the increasing use of turbocharged and hybrid engines, which operate under more demanding thermal and mechanical conditions than conventional engines. Turbocharging increases exhaust-gas temperatures and cylinder pressures, placing significant stress on engine valves, particularly exhaust valves. Hollow valves address this challenge by reducing overall valve weight and allowing internal cooling, often through sodium filling, which helps dissipate heat more efficiently during operation.

Lower valve mass improves engine response and reduces inertia within the valvetrain, supporting higher engine speeds and improved fuel efficiency. This is especially important in hybrid engines, where frequent start-stop cycles and rapid load changes require components that can withstand repeated thermal shocks without compromising durability. Hollow valve designs help maintain consistent performance under these fluctuating operating conditions. Advanced coatings further enhance valve performance by providing protection against heat, corrosion, and wear.

Expansion in Aftermarket and Remanufacturing Programs

Expansion in the aftermarket and remanufacturing programs is being driven by a combination of cost awareness, sustainability priorities, and longer vehicle ownership cycles. As vehicles remain in use for extended periods, demand for replacement parts, repairs, and performance restoration continues to rise. Vehicle owners and fleet operators increasingly prefer cost-effective alternatives to new components, especially for high-value parts, making remanufactured products an attractive option.

Remanufacturing involves restoring used components to functional standards comparable to those of new parts through cleaning, inspection, machining, and replacement of worn components. This process significantly reduces material consumption and energy use compared to producing new components, aligning with growing environmental expectations from regulators and customers. For manufacturers, remanufacturing programs offer an opportunity to maintain quality standards while strengthening customer loyalty through branded aftermarket offerings.

Category-wise Analysis

Product Type Insights

Mono-metallic valves are anticipated to dominate the market, accounting for approximately 45% of the market share in 2026, due to their balanced combination of cost efficiency, reliability, and wide applicability across conventional and mild hybrid engines. These valves are manufactured from a single alloy, simplifying production while ensuring consistent mechanical strength and thermal performance under normal operating conditions. For high-volume vehicle segments, mono-metallic valves offer an economical solution that meets durability and emission requirements without added complexity. Rane Engine Valve Limited is an Indian auto components manufacturer. Rane produces a wide range of engine valves, including mono-metallic valves made from single alloy steels for passenger cars, commercial vehicles, tractors, and two-/three-wheelers supplied to major OEMs such as Hyundai, Ashok Leyland, and others.

Hollow valves represent the fastest-growing product type, propelled by direct support of modern engine demands for higher efficiency, lower emissions, and improved performance. By reducing valve mass and often incorporating internal cooling (such as sodium filling), hollow valves enhance thermal management and reduce stress at elevated engine speeds, particularly in turbocharged and hybrid powertrains. Lighter valves decrease inertia in the valvetrain, enabling quicker response and better fuel economy without sacrificing durability. Galesburg, Mich., Power management company Eaton announced its Vehicle Group has introduced its next-generation sodium-filled hollow-head valves, which improve fuel economy, reduce emissions, and increase performance in gas-powered engines. The valves feature a unique design that lowers the cylinder chamber temperature while mitigating engine knock.

Vehicle Type Insights

Passenger cars are expected to dominate the market, contributing nearly 48% of revenue in 2026. With rising vehicle ownership in emerging economies and steady replacement demand in mature markets, passenger cars require the highest volume of engine components relative to commercial vehicles and two-wheelers. Continuous improvements in fuel efficiency, emissions compliance, and passenger-car performance drive sustained demand for advanced engine components. Aisan Industry Co., Ltd., a Japanese automotive parts supplier that produces exhaust and intake valves mainly for passenger vehicle engines used by Toyota and other major OEMs worldwide. Aisan’s precision valve components are used in high-volume passenger cars to improve combustion efficiency and emissions performance, underscoring that passenger car production accounts for the largest share of engine valve consumption compared with commercial or off-highway applications.

HCVs (heavy commercial vehicles) are the fastest-growing vehicle segment, driven by expanding infrastructure, logistics demand, and industrial activity, which increases long-distance freight movement. Unlike passenger cars, which are tied more directly to consumer purchasing cycles, HCV demand is closely linked to economic growth, urbanization, and supply chain expansion. Governments in emerging markets are investing in highways and freight corridors, encouraging fleet upgrades to newer, higher-capacity trucks. Tata Motors, India’s largest commercial vehicle manufacturer. In January 2026, Tata Motors reported that HCV truck sales jumped about 41 % year-on-year, with 12,691 heavy trucks sold compared to 8,990 in January 2025, driven by increased infrastructure activity and long-haul freight demand. This growth in the HCV segment outpaced other commercial vehicle categories, reflecting strong investment in logistics and fleet modernization.

Regional Insights

North America Automotive Valves Market Trends

North America's advanced powertrain development, robust research and development capabilities, and high public awareness of emission compliance benefits are driving growth in the region. Production systems in the U.S. and Canada offer strong support for automotive valve programs, ensuring broad accessibility across various sectors, including mono-metallic, passenger car, and OEM markets. The rising demand for high-performance, convenient, and easily integrable valve designs is further fueling adoption, as these innovations enhance engine efficiency and overcome challenges posed by older designs.

Advancements in automotive valve technology, such as stable hollow structures, improved nickel-alloy delivery systems, and specialized turbo enhancements, are attracting significant investments from both public and private sectors. Government initiatives and EPA campaigns continue to promote these technologies to address emission risks, fuel economy concerns, and the rise of hybrid vehicles, thus creating sustained market demand. The increasing focus on HCV grades and specialized applications, especially for passenger cars, is expanding the range of automotive valve applications.

Europe Automotive Valves Market Trends

Europe is experiencing significant growth, driven by heightened awareness of the benefits of emissions compliance, robust regulatory frameworks, and government-backed initiatives focused on automotive electrification and hybridization. Countries, including Germany, France, Italy, and Spain, have well-established OEM networks (e.g., Volkswagen Group, Stellantis, and Renault) that support the widespread use of automotive valves and promote the adoption of innovative delivery methods, including hollow and nickel-alloy solutions. These high-performance valve formulations are particularly appealing to passenger car manufacturers, regulation-conscious OEMs, and heavy commercial vehicle (HCV) operators, as they offer improved efficiency and coverage.

Technological advancements in automotive valve design, such as enhanced sodium filling, application-specific delivery, and improved coated grades, are further driving market growth. European authorities are increasingly supporting research and trials for both standard and specialized valves, boosting market confidence. The region's emphasis on low-emission alternatives aligns with broader goals of reducing CO emissions and preparing for Euro 7 standards. Public awareness campaigns are expanding the market's reach across both the passenger car and commercial vehicle segments, while suppliers continue to invest in manufacturing and in developing new valve variants to enhance performance and efficiency.

Asia Pacific Automotive Valves Market Trends

The Asia Pacific region is expected to dominate and be the fastest-growing market, accounting for 52% of revenue by 2026. This growth is driven by increasing awareness of vehicle production, government initiatives, and the expansion of application programs across the region. Countries such as China, India, Japan, and South Korea are actively promoting valve technologies to tackle emission concerns and meet the growing demand for hybrid vehicles. Automotive valves are particularly appealing in these regions due to their cost-effectiveness, ease of integration, and suitability for large-scale adoption in both passenger cars and heavy commercial vehicles (HCVs), serving both urban and rural populations.

Technological advancements are enabling the development of stable, effective, and easy-to-install automotive valves that can withstand harsh operating conditions and minimize thermal dependence. These innovations are crucial for reaching domestic OEMs and enhancing engine coverage. The increasing demand for monometallic valves, along with their applications in passenger cars and by OEMs, is driving market expansion. Additionally, public-private partnerships, higher vehicle spending, and growing investments in valve research and manufacturing capacity are further driving market growth. The convenience of valve delivery, combined with improved durability and a reduced risk of failure, makes valves a preferred solution.

Competitive Landscape

The global automotive valves market features competition between established Tier-1 engine component leaders and emerging regional suppliers. In North America and Europe, Denso Corporation and BorgWarner Inc. lead through strong R&D, distribution networks, and OEM ties, bolstered by innovative hollow and nickel-alloy programs. In Asia Pacific, Aisin Seiki Co., Ltd. advances with localized solutions, enhancing accessibility. Hollow delivery boosts thermal performance, cuts weight risks, and enables mass integrations across engines. Strategic partnerships, collaborations, and acquisitions merge expertise, expand portfolios, and speed commercialization. Coated formulations solve wear issues, aiding penetration in high-output applications.

Key Industry Developments

- In August 2025, Nissan became the first to use cold spray technology for valve seats in automotive engines. This process was applied to its 1.5-liter turbocharged engine, developed for the third-generation e-POWER hybrid powertrain. The Qashqai compact crossover, produced at Nissan's Sunderland facility in the UK, was the first vehicle to feature this new system.

- In October 2024, Danfoss Power Solutions launched the next-generation Level 1 AxisPro® valve, completing the Vickers by Danfoss servo-performance lineup. The valve featured a digital amplifier, industry-leading network protocols, and enhanced performance. Pro-FX™ Configure v2 was also introduced, offering an intuitive, real-time configuration platform for faster installations. These valves targeted demanding industrial applications such as presses and factory automation systems.

Companies Covered in Automotive Valves Market

- Denso Corporation

- Hitachi Astemo, Ltd.

- BorgWarner Inc.

- Robert Bosch GmbH

- Valeo S.A.

- Aisin Seiki Co., Ltd.

- DRiV Automotive Inc.

- Eaton Corporation

- Continental AG

- MAHLE GmbH

Frequently Asked Questions

The global automotive valves market is projected to reach US$32.7 billion in 2026.

Growth in vehicle production and fleet expansion, particularly in passenger cars and heavy commercial vehicles, is driving higher consumption of engine parts due to both OEM demand and long-term maintenance requirements.

The automotive valves market is poised to witness a CAGR of 7.4% from 2026 to 2033.

Rising adoption of turbocharged and hybrid powertrains is creating opportunities for advanced components such as hollow valves, lightweight materials, and high-temperature coatings to meet higher performance and durability requirements.

Denso Corporation, BorgWarner Inc., MAHLE GmbH, Eaton Corporation, and Aisin Seiki Co., Ltd. are the key players.