- Automotive Components & Materials

- Automotive Rain Sensor Market

Automotive Rain Sensor Market Size, Share, and Growth Forecast 2026 - 2033

Automotive Rain Sensor Market by Vehicle Type (Passenger Cars, Light Commercial Vehicles, Heavy Commercial Vehicles, Electric Vehicles), Sales Channel (OEMs, Aftermarket), and Regional Analysis for 2026 - 2033

Automotive Rain Sensor Market Size and Trend Analysis

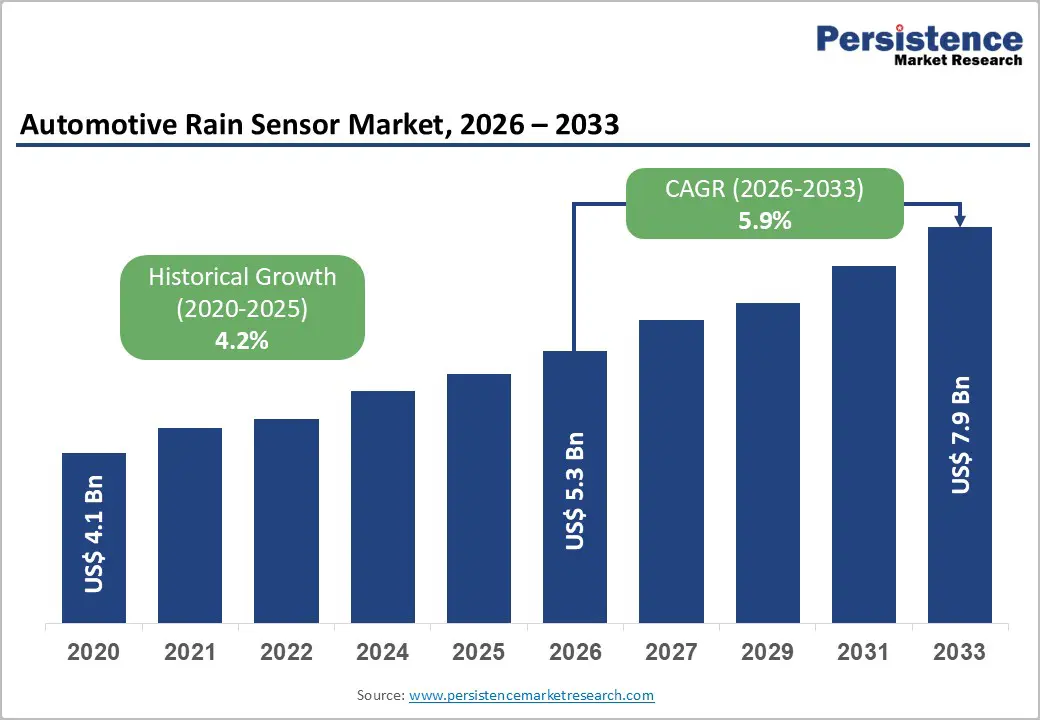

The global automotive rain sensor market size is supposed to be valued at US$ 5.3 billion in 2026 and is projected to reach US$ 7.9 billion by 2033, growing at a CAGR of 5.9% between 2026 and 2033.

The expansion is driven by rising integration of Advanced Driver Assistance Systems (ADAS), stronger safety and comfort expectations from consumers, and growing penetration of automatic wiper control features across vehicle segments, particularly in passenger cars and electric vehicles where user experience and automation are core differentiators.

Key Industry Highlights:

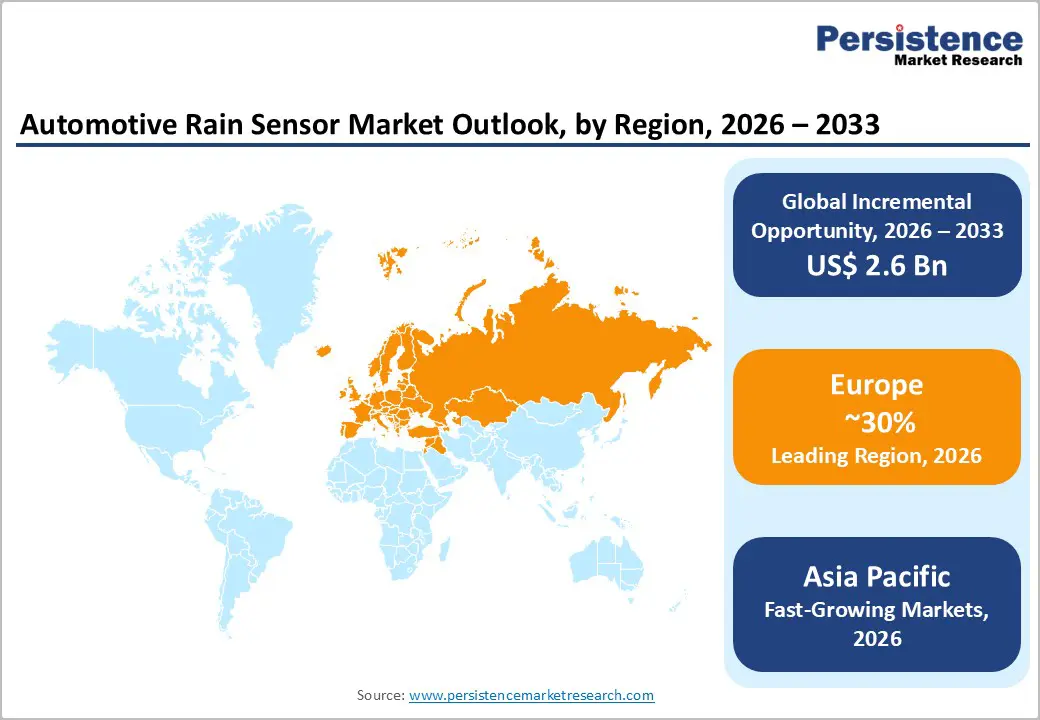

- Leading Region: Europe is expected to remain the leading regional market for automotive rain sensors, driven by stringent Euro NCAP safety ratings, high penetration of ADAS, and widespread consumer expectations for automated convenience features across Germany, the U.K., France, and Spain.

- Fastest-growing Region: The fastest-growing regional market is projected to be Asia Pacific, where massive vehicle production in China, Japan, India, and South Korea, combined with rapid EV adoption and rising ADAS penetration, creates strong demand for rain-sensing technologies.

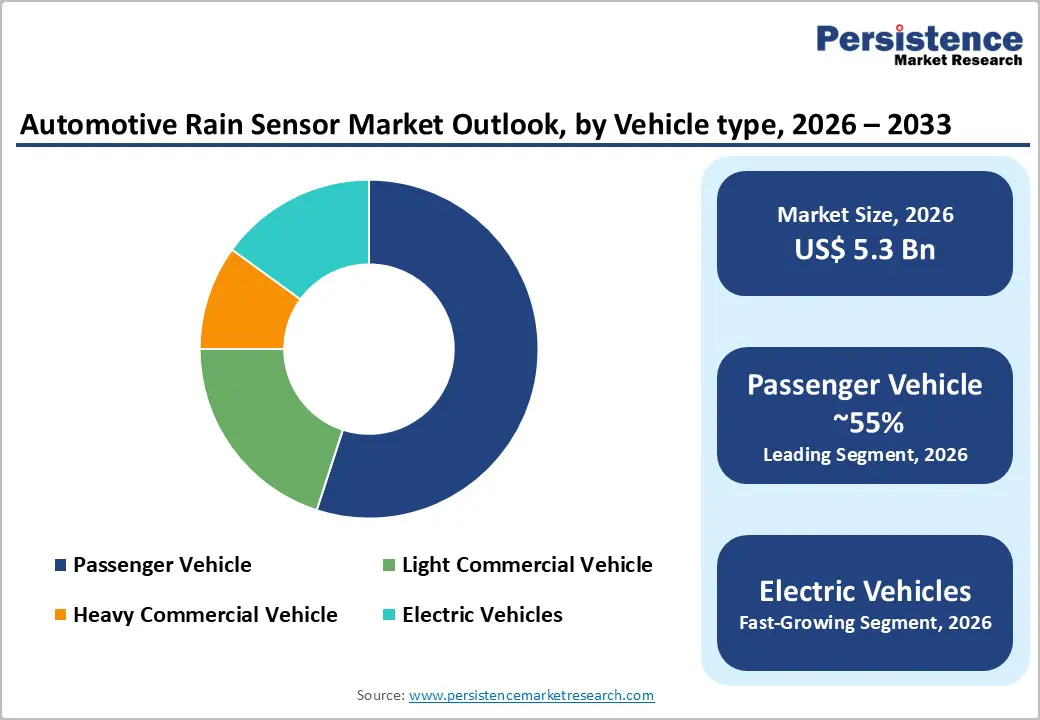

- Leading Segment: Among vehicle types, Passenger Cars dominate the market, accounting for approximately 70% of revenues due to their large production volumes and high fitment rates of comfort and safety features, including automatic rain-sensing wipers.

- Fastest-growing Region: The fastest-growing vehicle segment is Electric Vehicles, as global EV sales surpassed 17 million in 2024 and are expected to exceed 20 million in 2025, with rain sensors becoming standard in smart, connected EV platforms.

- Opportunities: A key market opportunity lies in integration with autonomous driving and next-generation ADAS systems, where rain sensors ensure clear visibility for cameras and sensors, supporting the transition toward higher levels of vehicle automation and safety.

| Key Insights | Details |

|---|---|

| Automotive Rain Sensor Market Size (2026E) | US$ 5.3 Bn |

| Market Value Forecast (2033F) | US$ 7.9 Bn |

| Projected Growth (CAGR 2026 to 2033) | 5.9% |

| Historical Market Growth (CAGR 2020 to 2024) | 4.2% |

Market Dynamics

Drivers - Rising adoption of ADAS and regulatory push for enhanced vehicle safety

A primary growth drive for the Automotive Rain Sensor Market is the accelerating adoption of Advanced Driver Assistance Systems (ADAS) in passenger and commercial vehicles worldwide. Regulatory programs such as Euro NCAP now award higher safety ratings to vehicles equipped with automatic rain-sensing wipers, recognizing their role in reducing driver distraction by maintaining optimal visibility without manual intervention. In the United States, the National Highway Traffic Safety Administration (NHTSA) has proposed guidelines requiring all ADAS-equipped vehicles to maintain unobstructed camera views under adverse weather conditions by 2027, further incentivizing integration of intelligent wiper systems tied to rain sensors. Data from the Partnership for Analytics Research in Traffic Safety (PARTS) shows that 10 ADAS features had surpassed 50% market penetration by 2023, with collision warning and automatic emergency braking reaching 91% to 94% in the U.S. passenger vehicle market, demonstrating strong momentum for sensor-based safety systems that include rain detection as a complementary component.

Expanding Electric Vehicle Production and Smart Vehicle Technologies

Another key driver is the rapid growth of electric vehicles (EVs), where rain sensors are increasingly standard equipment to support premium user experiences and integration with connected vehicle ecosystems. According to the International Energy Agency (IEA), global electric car sales exceeded 17 million units in 2024, representing more than 20% of new car sales, and are projected to surpass 20 million in 2025, accounting for one in every four new vehicles sold globally. As automakers prioritize cabin comfort, automation, and Internet of Things (IoT) connectivity in electrified platforms, rain sensors that seamlessly integrate with vehicle control networks, Vehicle-to-Everything (V2X) systems, and real-time weather exchanges become essential. This trend is particularly pronounced in China, where the government's push toward smart transportation systems and local manufacturers such as BYD and Geely incorporating rain sensors in EVs to meet rising consumer expectations accelerate demand, positioning rain sensor suppliers at the forefront of smart vehicle innovation.

Restraints - High Integration Costs and Price Sensitivity in Emerging Markets

A significant restraint for the Automotive Rain Sensor Market is the cost pressure faced by OEMs, especially in price-sensitive emerging economies where vehicle affordability remains a top priority. Rain sensors require precise optical or infrared components, windshield integration using specialized adhesives, and electronic control units for signal processing, all of which add to bill-of-materials costs. In markets such as South Asia and parts of Latin America, where compact and budget vehicles dominate, automakers often limit advanced features to higher trim lines, restricting rain sensor penetration. Additionally, the need for sensor calibration, compatibility with different windshield types, and integration with CAN bus or LIN vehicle networks increases engineering and validation expenses, which can discourage adoption in cost-constrained segments.

Technical challenges in diverse weather conditions and false triggering

Another restraint is the challenge of ensuring consistent, reliable performance across a wide range of weather and environmental conditions. Rain sensors operate on optical principles typically infrared beams reflected within the windshield and can be affected by ambient light interference, condensation, ice, snow, or contaminants like dirt and road spray. False triggering, where wipers activate unnecessarily, or failure to detect light rain can erode consumer trust and lead to warranty claims. Regulatory fragmentation, with differing automotive safety standards across regions such as FMVSS 104 in North America, UNECE R48 in Europe, and local requirements in Asia, requires multiple product variants and separate testing protocols, extending development cycles by 4-6 months and raising compliance costs for global suppliers.

Opportunity - Integration with autonomous driving and next-generation ADAS platforms

A major opportunity lies in the evolution toward higher levels of vehicle automation and the proliferation of sophisticated ADAS architectures. As vehicles progress toward Level 2 and Level 3 automated driving, maintaining clear sensor and camera sightlines becomes mission-critical for functions like lane-keeping, adaptive cruise control, and autonomous emergency braking. Rain sensors that communicate in real time with electronic wiper controls, heating elements, and even Head-Up Displays (HUDs) ensure that forward-facing cameras and LiDAR units remain unobstructed during rain events. In India, ADAS penetration reached 8.3% of passenger vehicle sales in H1 2025, up from 6.2% in H1 2024, representing 33% growth, with features like collision warning, pedestrian avoidance, and adaptive cruise control gaining traction. Companies such as Mahindra and Hyundai-Kia are embedding these systems in new models, creating a growing installed base where integrated rain sensing adds value. Suppliers that develop compact, energy-efficient, multi-functional sensors combining rain, light, and solar detection can differentiate themselves and capture premium contracts.

Expansion in aftermarket and retrofit opportunities for older vehicle fleets

The aftermarket segment presents a substantial growth opportunity, particularly in regions with large, aging vehicle fleets where owners seek to upgrade to modern convenience and safety features. While OEM channels dominate new vehicle installations, millions of vehicles on the road today lack factory-fitted rain sensors, creating a retrofit market for universal or semi-custom rain-sensing kits compatible with existing wiper systems. Specialty electronics retailers, automotive accessory distributors, and online platforms offer pathways to reach consumers interested in DIY installations or professional upgrades. Advances in sensor miniaturization, modular designs, and cost reduction through Micro-Electro-Mechanical Systems (MEMS) and nanotechnology-based sensors improve the feasibility and affordability of aftermarket solutions. Furthermore, fleet operators in commercial and logistics sectors increasingly prioritize driver safety and vehicle uptime, making automatic wiper activation attractive for maintaining visibility in heavy rain, especially for Light Commercial Vehicles and Heavy Commercial Vehicles operating across diverse weather zones.

Category-wise Analysis

Vehicle Type Insights

Within Vehicle Type, Passenger Cars account for the largest share of the Automotive Rain Sensor Market, estimated at approximately 70% of global revenues. Passenger vehicles represent the bulk of worldwide automotive production and sales, and rain sensors have become standard or widely available optional equipment in mid- to high-trim variants across brands. Consumers in developed markets such as North America, Europe, and East Asia increasingly expect automated convenience features, and rain-sensing wipers enhance the premium feel and user experience, particularly in regions with frequent rainfall. The rising penetration of ADAS in passenger cars, combined with automakers' efforts to differentiate through cabin comfort and technology, drives sustained fitment rates. While Electric Vehicles are the fastest-growing segment in unit terms global EV sales exceeded 17 million in 2024 and are projected to reach 20 million in 2025their absolute volumes still trail traditional car production, making passenger cars the dominant revenue contributor over the near to medium term.

Sales Channel Insights

By Sales Channel, OEMs command an estimated around 85% share of the Automotive Rain Sensor Market. Most rain sensors are integrated at the vehicle assembly stage, either supplied directly by Tier-1 electronics and sensor specialists such as Bosch, Denso, Valeo, and Continental, or embedded within larger systems modules like instrument clusters, mirror assemblies, or ADAS suites. OEM installations benefit from design-in relationships, long-term supply agreements, and co-development programs that ensure seamless integration with windshield bonding processes, vehicle electrical architectures, and software calibration routines.

The Aftermarket channel, while a smaller segment offers stable replacement demand for failed sensors in high-mileage vehicles and serves a niche of enthusiasts and fleet operators seeking retrofits. However, the high reliability and long service life of modern rain sensors, combined with their tight integration into vehicle glass and electronics, limits aftermarket penetration, making OEM channels the primary growth engine for suppliers.

Regional Insights

North America Automotive Rain Sensor Market Trends

North America, led by the United States, represents a mature and technology-intensive market for automotive rain sensors, where consumer expectations for comfort and convenience features are high and regulatory frameworks support advanced safety technologies. The region produces more than 11 million passenger cars annually and has a large installed base of light trucks, SUVs, and crossovers, vehicle categories that increasingly offer rain-sensing wipers as standard or popular optional equipment.

The U.S. innovation ecosystem benefits from the presence of leading automotive electronics suppliers, semiconductor firms such as Texas Instruments, STMicroelectronics, and NXP Semiconductors, and specialized sensor manufacturers, all collaborating to advance optical and infrared sensing technologies. Companies such as Gentex Corporation, known for electrochromic mirrors and integrated driver monitoring systems, showcase at industry events such as CES 2025 how rain sensors can be combined with other cabin electronics to deliver integrated safety and convenience solutions.

Europe Automotive Rain Sensor Market Trends

Europe is a global leader in automotive safety standards and advanced driver assistance adoption, with rain sensors widely deployed across passenger vehicle platforms in Germany, the U.K., France, and Spain. The region's stringent Euro NCAP protocols award higher safety ratings to vehicles equipped with automatic wiper control, recognizing the technology's contribution to maintaining clear visibility and reducing driver workload during rain events. European automakers, including premium and volume brands, have long integrated rain sensors into mid-range and higher trims, and regulatory harmonization under UNECE R48 and the Automotive Electromagnetic Compatibility Directive (AEMCD) ensures that sensors meeting EU standards can be deployed across member states with minimal modification.

Germany's automotive sector, home to Bosch, Continental, Hella, and other Tier-1 suppliers, drives innovation in sensor fusion, where rain sensors interact with adaptive lighting, automatic climate control, and multi-zone HVAC systems to optimize cabin comfort. The region's strong commitment to electrification and decarbonization under the European Green Deal further boosts adoption, as new EV and plug-in hybrid platforms incorporate comprehensive electronics suites that include rain and light sensing as baseline features.

Asia Pacific Automotive Rain Sensor Market Trends

Asia Pacific is the largest and fastest-growing regional market for automotive rain sensors, underpinned by massive vehicle production in China, Japan, South Korea, and India, as well as expanding capacity in ASEAN countries. China alone accounts for approximately one-third of global motor vehicle production, exceeding 30 million units annually, and is the world's dominant hub for electric vehicle manufacturing, with nearly 80% of global EV battery cell production and the bulk of downstream vehicle assembly. Chinese automakers such as BYD, Geely, NIO, and others integrate advanced electronics including rain sensors into their fast-growing EV lineups to meet consumer demands for smart, connected vehicles and to align with government policies promoting intelligent transportation systems.

Japan brings deep expertise in precision sensor manufacturing and early adoption of driver assistance technologies, with brands like Toyota, Honda, Nissan, and Denso Corporation leading the way. In April 2024, Denso unveiled a high-resolution rain sensor designed specifically for hybrid and plug-in hybrid models, reflecting the industry's focus on energy efficiency and seamless integration with electrified powertrains. India is experiencing rapid growth in ADAS penetration, reaching 8.3% of passenger vehicle sales in H1 2025, with new models from Mahindra, Hyundai, Kia, and Honda incorporating rain-sensing wiper systems alongside collision warning, lane control, and adaptive cruise features.

Competitive Landscape

The automotive rain sensor market exhibits a moderately concentrated structure, with a handful of global Tier-1 suppliers, Bosch, Denso, Valeo, and Continental, holding a combined market share exceeding 50%. These companies leverage scale economies, extensive R&D capabilities, established relationships with major OEMs, and integrated supply chains spanning sensor components, optical elements, and software algorithms. Competition centers on enhancing detection accuracy, reducing false triggering, improving performance in challenging conditions such as ice and snow, and integrating rain sensors with broader ADAS and cabin electronics ecosystems. Emerging trends include platform-based sensor designs, integration of artificial intelligence for improved signal processing, and business models built around co-development with automakers for electrified and autonomous vehicle platforms.

Key Developments:

- In June 2025, Innoviz Technologies Ltd. unveiled InnovizSMART Long-Range, a cutting-edge LiDAR sensor featuring precise object detection from distances of up to 400 meters, even in challenging outdoor conditions such as dust, sunlight, and rain.

- In September 2024, Bosch expanded its commercial-vehicle technology portfolio at IAA Transportation 2024, emphasizing software functions that integrate environmental sensing, including rain detection, into fleet management suites.

Companies Covered in Automotive Rain Sensor Market

- Bosch

- Denso

- Valeo

- Continental

- Delphi Technologies

- Gentex Corporation

- Hella

- Autoliv

- Magna International

- SABIC

- Texas Instruments

- STMicroelectronics

- NXP Semiconductors

- Other Key Players

Frequently Asked Questions

The global Automotive Rain Sensor Market is projected to reach approximately US$ 7.9 Bn by 2033, supported by rising ADAS adoption, growing electric vehicle production, and increasing consumer demand for automated comfort and safety features across all vehicle segments.

The main demand driver is the accelerating integration of Advanced Driver Assistance Systems (ADAS) and regulatory push for enhanced vehicle safety, with programs like Euro NCAP and NHTSA guidelines recognizing automatic rain-sensing wipers as contributors to improved visibility and reduced driver distraction.

Passenger Cars form the dominant segment, accounting for approximately 55% of market revenues, driven by high production volumes, widespread availability of rain-sensing wipers in mid- to high-trim variants, and strong consumer expectations for automated convenience features.

Europe is expected to lead, supported by stringent Euro NCAP safety ratings, high ADAS penetration, advanced automotive electronics infrastructure, and consumer preference for comfort technologies across Germany, the U.K., France, and Spain.

Leading companies include Robert Bosch GmbH, DENSO CORPORATION, Valeo S.A., Continental AG, Gentex Corporation, Hella (Forvia Group), Delphi Technologies, Magna International, and semiconductor suppliers such as Texas Instruments, STMicroelectronics, and NXP Semiconductors.