- Automotive Components & Materials

- Automotive Wipers Market

Automotive Wipers Market Size, Share, and Growth Forecast for 2026-2033

Automotive Wipers Market by Blade type (Traditional Bracket Blades, Low-Profile Beam Blades, Hybrid Blades), Technology (Standard Mechanical Systems, Smart Systems, Energy-Efficient & Eco-Friendly Systems), End-Use (Passenger Vehicles, Commercial Vehicles, Two-Wheelers, Off-Highway Vehicles), and Regional Analysis for 2026-2033

Automotive Wipers Market Share and Trends Analysis

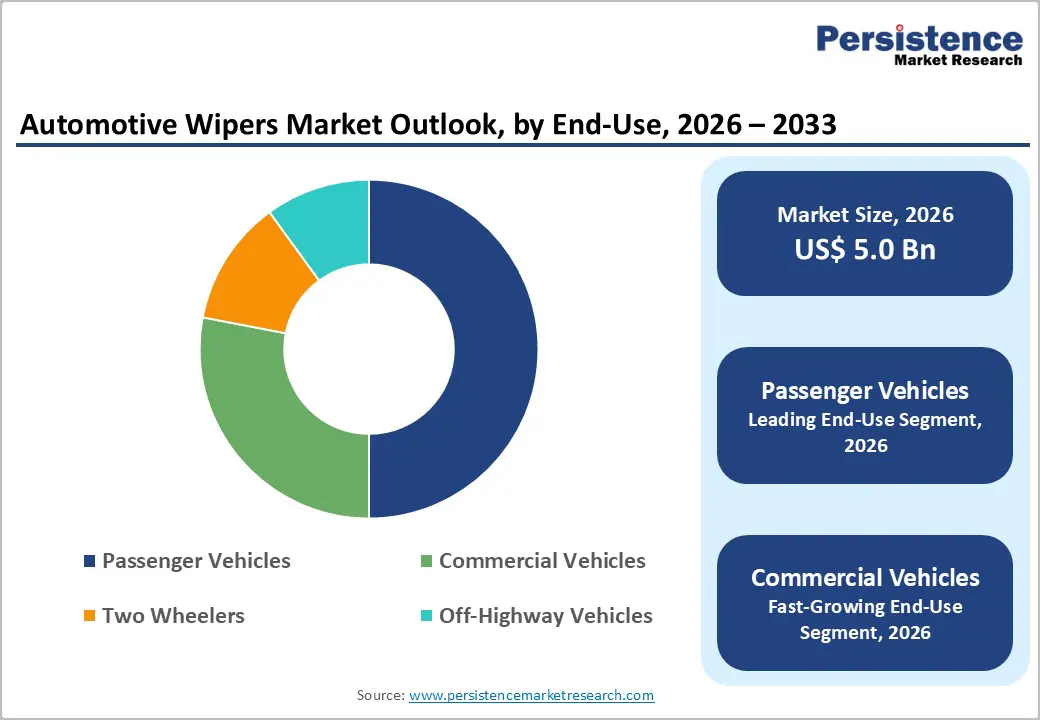

The global automotive wipers market size is likely to be valued at US$ 5.0 billion in 2026, and is projected to reach US$ 6.8 billion by 2033, growing at a CAGR of 4.5% during the forecast period 2026 - 2033.

Market growth is being supported by steady global vehicle production and mandatory safety regulations that are requiring clear driver visibility under diverse weather conditions. Regulatory bodies across North America, Europe, and Asia Pacific are continuing to enforce performance standards for windshield wiping systems, which is sustaining original equipment manufacturer (OEM) demand across passenger and commercial vehicle segments. In addition, increasing adoption of beam and hybrid wiper blade technologies is improving durability and aerodynamic efficiency, contributing to higher average selling prices and stable value growth. The expanding global vehicle parc is generating recurring aftermarket demand, as wiper blades require periodic replacement due to wear and environmental exposure.

This replacement cycle is creating predictable revenue streams that are complementing OEM volumes. At the same time, manufacturers are integrating smart features such as rain-sensing activation and energy-efficient motor systems, which are aligning with broader trends toward connected and electrified vehicles. The competitive landscape is showing moderate consolidation, with leading players strengthening differentiation through innovation, material science advancements, and long-term OEM partnerships.

Key Industry Highlights

- Dominant Blade Type: Traditional bracket blades are projected to lead with approximately 55% market share in 2026, while low-profile beam blades are expected to grow fastest at a 6.3% CAGR through 2033, owing to their aerodynamic benefits.

- Technology Leadership: Standard mechanical wiper systems are anticipated to hold around 60% share in 2026, whereas smart wiper systems are forecast to grow the fastest at about 7.1% CAGR through 2033, supported by increasing electronic integration.

- End-Use Leadership: Passenger vehicles are expected to dominate with nearly 50% revenue share in 2026, while commercial vehicles are projected to expand at the fastest rate, registering an estimated 2026-2033 CAGR of 5.5%.

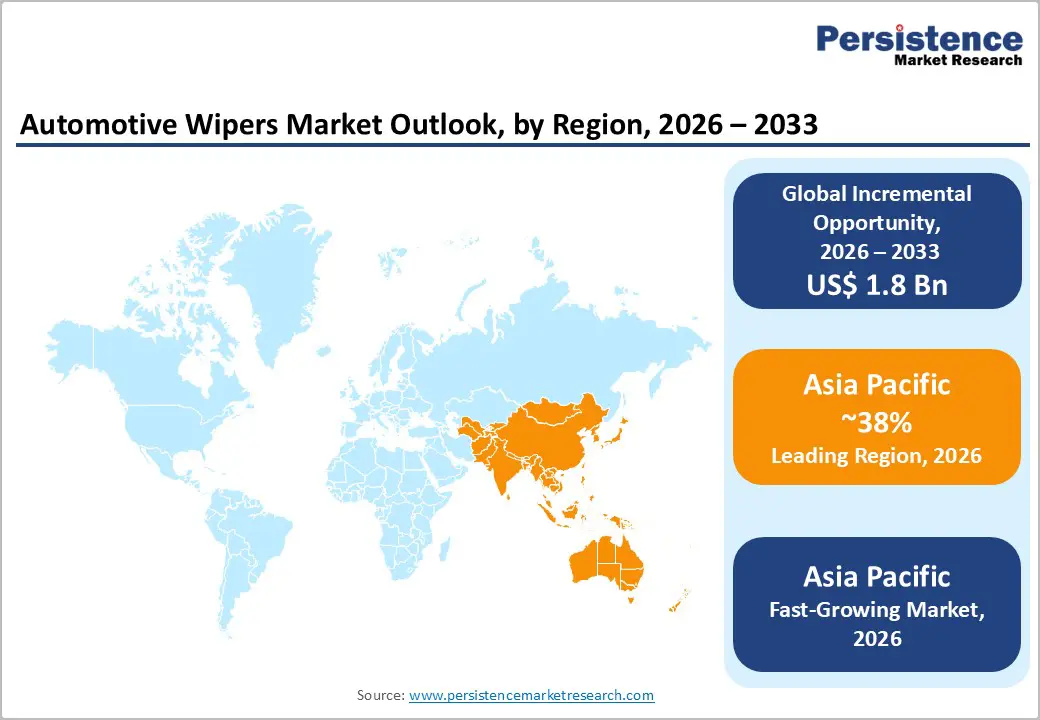

- Regional Dominance: Asia Pacific is projected to account for about 38% market share in 2026 and remain the fastest-growing market at roughly 5.2% CAGR through 2033, driven by massive vehicle production growth in China, India, and ASEAN.

- Competitive Focus: Competitive dynamics center on smart system innovation, localized cost-efficient manufacturing, and aftermarket expansion to secure recurring replacement-driven revenues.

| Key Insights | Details |

|---|---|

| Automotive Wipers Market Size (2026E) | US$ 5.0 Bn |

| Market Value Forecast (2033F) | US$ 6.8 Bn |

| Projected Growth (CAGR 2026 to 2033) | 4.5% |

| Historical Market Growth (CAGR 2020 to 2025) | 4.2% |

Market Factors – Growth, Barriers, and Opportunity Analysis

Safety Regulations and Technology Adoption to Stoke Vehicle Production

Vehicle production remains the core demand driver for the automotive wipers market, directly supporting OEM fitment and aftermarket replacement volumes. According to the International Organization of Motor Vehicle Manufacturers (OICA), vehicle production exceeded 85 million units in 2025, reflecting a strong recovery from the 2020 downturn. The expanding vehicle parc, particularly across Asia Pacific and Latin America, continues to elevate replacement demand. As windshield wipers are mandatory safety components across all vehicle categories, demand scales in direct proportion to vehicle population growth. This structural linkage provides volume stability and limits downside risk during short-term automotive market fluctuations.

Regulatory emphasis on vehicle safety and visibility standards further reinforces market demand and replacement cycles. Stringent safety regulations enforced by bodies such as the U.S. National Highway Traffic Safety Administration (NHTSA) and the European Commission (EC) mandate functional and performance-compliant windshield wipers across vehicle categories. Requirements related to driver visibility, adverse weather operation, and periodic inspections sustain consistent aftermarket activity. In Europe, for example, UN Economic Commission for Europe (UNECE) Regulations R33 and R43 indirectly reinforce wiper performance requirements, encouraging adoption of higher-efficiency blade designs. The Society of Automotive Engineers (SAE) also highlights rising OEM integration of rain-sensing systems, particularly in mid-range and premium vehicles, accelerating the shift toward advanced wiper technologies.

Cost, Supply Chain, and Market Complexity

Cost sensitivity remains a primary challenge for the automotive wipers market, particularly for price-driven passenger and fleet vehicles. Advanced beam blades, hybrid designs, and electronically integrated wiper systems carry higher production costs due to premium materials and embedded sensors. Fleet operators and entry-level vehicle OEMs often continue to rely on conventional mechanical blades to minimize expenses, slowing adoption of higher-value products. Limited standardization across vehicle platforms further increases design and production complexity, raising inventory management costs. Competitive pressure from regional suppliers also forces cost-based pricing, constraining margins for advanced technologies. Environmental compliance requirements for recyclable materials and eco-friendly production add an additional cost layer, especially for premium blade manufacturing.

Supply chain volatility compounds these structural challenges, particularly for technology-enabled wiper systems. The Dutch government intervened to control semiconductor supplier Nexperia, causing disruptions in chip supply from China and delaying deliveries of rain-sensing and electronically integrated modules. Delays in specialized rubber, polymer, and electronic components further affect production schedules and aftermarket availability. High initial investment requirements for advanced wipers restrict adoption among smaller OEMs, while regulatory and logistics uncertainties amplify operational risks. These factors limit the speed of technology adoption and maintain dependence on conventional blade designs in many markets, moderating overall revenue growth potential.

Urbanization, Electrification, ADAS Integration, and Aftermarket Expansion

The rapid urbanization and changing vehicle ownership patterns create new demand avenues for the automotive wipers market across multiple vehicle categories. In India and Southeast Asia, rising use of two wheelers and urban mobility EVs such as electric scooters and auto rickshaws has prompted niche wiper needs, especially in monsoon prone regions. Growth in electrified commercial fleets, exemplified by Amazon and Flipkart deploying electric delivery vans in major cities, increases demand for energy efficient wiper systems that integrate with EV power management. These systems help reduce auxiliary power draw and improve overall vehicle efficiency, aligning with sustainability goals set by fleet operators. Local OEMs are responding with compact, cost effective wiper variants tailored for urban and EV platforms.

The integration with advanced visibility and safety systems and strengthening aftermarket networks offers further upside. Clean windshield performance is critical for advanced driver assistance systems (ADAS) used in vehicles such as the Honda Accord and Toyota Camry, where camera based lane assist and adaptive cruise control depend on unobstructed sensor views; this drives higher adoption of smart rain sensing wipers. Organized aftermarket expansion, backed by service networks such as Bosch Car Service and digital parts marketplaces such as Mighty Auto Parts, enhances accessibility of beam and hybrid blades. As replacement cycles remain steady and consumers increasingly opt for premium blades, manufacturers can capture recurring revenue and higher per unit value across diverse markets.

Category-wise Analysis

Blade Type Insights

Traditional bracket blades are projected to lead with approximately 55% of the automotive wipers market revenue share in 2026, due to cost efficiency, universal fitment, and broad use across entry level passenger vehicles and commercial fleets. These blades remain prevalent in replacement channels where affordability and wide compatibility are priorities. For example, at the AAPEX Show held in November 2025, multiple aftermarket suppliers showcased heavy duty hybrid and conventional blades designed for all weather durability and easy replacement, underscoring ongoing demand for bracket and conventional designs in fleet and retail markets. These developments reinforce stable demand for basic blades across diverse service networks.

Low profile beam blades are expected to be the fastest growing blade type with a 6.3% CAGR from 2026 to 2033 as OEMs increase adoption of aerodynamic and high performance designs. Reflecting this trend, Petra Automotive launched its PetraBlades Premium Beam Wiper Blades, aimed at enhanced visibility and durability in challenging weather conditions, signaling rising industry focus on premium beams. Hybrid blades continue to grow as an intermediate choice, combining improved wiping performance with moderate pricing, appealing to aftermarket buyers seeking performance upgrades without premium costs.

Technology Insights

Standard mechanical systems are anticipated to remain the dominant technology with about 60% of the automotive wipers market share in 2026, due to their simplicity, reliability, and low cost across mass market passenger vehicles and commercial fleets. Their continued leadership is reinforced by extensive replacement networks where compatibility and low service costs are critical. Ongoing product portfolio updates that maintain mechanical designs, such as extended coverage blade applications for new electric vehicles, further support this dominant position. For example, Denso expanded its wiper blade coverage to include new EV models from brands such as BYD and Polestar, demonstrating continued mechanical blade relevance even in evolving vehicle platforms.

Smart wiper systems are projected to be the fastest growing technology segment with a 7.1% CAGR between 2026 and 2033, driven by rising sensor integration and ADAS compatibility in new models. Valeo, for instance, introduced its A.U.R.A. rain and ambient sensor module, enabling windshield wipers to work in tandem with environmental sensing for improved performance and comfort, highlighting the shift toward intelligent systems. Energy efficient & eco friendly systems also gain traction in markets with strong emissions and sustainability standards, aligning with electrification trends and regulatory emphasis on reduced energy draw.

End Use Insights

Passenger vehicles are expected to remain the largest end use segment, likely to hold around 50% of market revenues in 2026, supported by high production volumes and frequent blade replacement cycles. Demand is further reinforced by OEM feature upgrades in mainstream models to improve driver safety and visibility. For example, Tata Motors’ Nexon included rain sensing windshield wipers in select trims, reflecting OEM adoption of advanced wiper technology even in compact passenger vehicles. Enhanced blade performance and integration with vehicle electronics encourage recurring aftermarket replacement cycles. Consumer preference for improved visibility and driving safety further strengthens sustained blade demand across urban and suburban markets.

Commercial vehicles are projected to be the fastest growing end use segment with a 5.5% CAGR through 2033, driven by expanding logistics operations and ecommerce fleet deployments requiring durable, high-performance wiper systems. Cebi Group opened a new production line in Slovakia for automotive wiper motors, increasing capacity to serve commercial OEMs in Europe, including delivery van fleets. Two wheelers and off highway vehicles are also showing rising demand in Asia Pacific due to mechanization in agriculture and construction, creating niche opportunities for compact and specialized wiper solutions tailored to these vehicle platforms.

Regional Insights

North America Automotive Wipers Market Trends

North America is an important regional market for automotive wipers, driven by the U.S. through strict safety standards, high replacement rates, and widespread adoption of advanced vehicle technologies. OEM and aftermarket sales are reinforced by harsh winter conditions, which create frequent blade replacement cycles. Rain-sensing and aerodynamic wipers are increasingly included in passenger and commercial vehicles, improving visibility, driver convenience, and safety. Established aftermarket networks across urban and rural areas guarantee accessibility to both conventional and advanced wiper systems. Consumer awareness of vehicle safety and integration of ADAS features further stimulate demand.

Recent developments highlight ongoing innovation in all-weather performance. For example, Kia America launched enhanced windshield wiper software for EV9 models that alerts drivers to snow or ice obstruction, improving visibility under winter conditions Additionally, Valeo expanded its Premium wiper series to improve fit and wiping efficiency for North American vehicles, emphasizing durability in extreme climates. These examples reflect a regional focus on performance, safety, and advanced wiper integration for both OEM and aftermarket applications.

Europe Automotive Wipers Market Trends

Europe is a highly significant regional market for automotive wiper technologies, led by Germany, the U.K., France, and Spain, where premium vehicle penetration and harmonized EU safety regulations drive demand for advanced wiper solutions. OEMs increasingly integrate beam and smart wiper systems to meet visibility and safety requirements for both passenger and commercial vehicles. Aftermarket demand is supported by organized service networks that reinforce consistent replacement cycles. Consumer preference for comfort, convenience, and reliability continues to drive adoption of advanced wiper technologies. Regulatory emphasis on eco-friendly components also encourages energy-efficient blade solutions.

Innovation trends in Europe further strengthened the market. AUMOVIO SE, a German automotive technology company, advanced sensor-based wiper control systems for passenger and commercial vehicles, enhancing performance under varied weather conditions. OEMs also expanded testing for durability in high-rainfall and winter climates, reinforcing long-term reliability. These initiatives demonstrate Europe’s commitment to integrating smart and eco-friendly wiper systems into vehicles, ensuring safety, energy efficiency, and high-performance standards.

Asia Pacific Automotive Wipers Market Trends

Asia Pacific is estimated to lead with 38% of the automotive wipers market sales in 2026, and is also projected to be the fastest-growing region at a 5.2% CAGR through 2033, driven by rapid motorization, rising disposable incomes, and large-scale vehicle production in China, India, Japan, and ASEAN countries. The region supports both OEM and aftermarket demand due to frequent vehicle registration growth, diverse climatic conditions, and expanding service networks. Advanced wiper systems, including beam blades and rain-sensing technologies, are increasingly integrated into passenger, commercial, and off-highway vehicles. Government incentives for EV adoption and urban fleet modernization further accelerate demand for advanced wiper technologies. OEM and aftermarket collaboration is creating scalable growth opportunities in high-density metropolitan areas.

In China, smart wiper blade adoption surged following the launch of passenger vehicles equipped with rain-sensing and automatic activation systems, particularly in urban SUV and mid-range car segments. In addition, Geely Auto invested a huge amount in Ningbo to establish a safety testing facility validating wiper performance and visibility systems for new vehicles. These initiatives reinforce the region’s focus on high-quality, technologically advanced wiper solutions that meet OEM and consumer expectations, positioning Asia Pacific for sustained long-term growth.

Competitive Landscape

The global automotive wipers market structure is moderately consolidated, with leading vendors including Bosch, Valeo, Denso, Trico, Robert Bosch Automotive Steering, Aisin Seiki, and Continental controlling a significant share of revenue. These established players leverage strong OEM relationships, global distribution networks, and integrated wiper system solutions spanning traditional, beam, and smart technologies. Heavy investments in R&D enable them to maintain leadership in aerodynamic blade design, rain-sensing wiper systems, and energy-efficient solutions.

Regional and niche competitors, such as Anco Wipers and Federal-Mogul Motorparts, focus on specialized segments, aftermarket expansion, and localized manufacturing advantages. Entry barriers include OEM approval cycles, material sourcing, and strict regulatory compliance across vehicle safety standards. Emerging trends in vehicle electrification, ADAS integration, and smart blade technologies are enabling software and sensor-focused companies to participate via partnerships with traditional manufacturers. Market consolidation is expected to continue gradually as global leaders acquire smaller suppliers or collaborate through technology integration to expand both geographically and across advanced wiper solutions.

Key Industry Developments

- In December 2025, Geely Auto inaugurated the Geely Safety Centre in Ningbo, China, with an investment of US$ 284 million, establishing the world’s largest automotive safety testing facility. The center conducts 27 tests, including high-speed crash, battery/ADAS, and pedestrian safety assessments, and features the longest indoor crash track (293.39 m) and largest altitude-climate wind tunnel.

- In October 2025, Pep Boys expanded its windshield wiper blade assortment across store locations and online, adding premium and all-season options to better serve customer needs for improved visibility and weather performance. The update is part of a broader strategy to enhance accessory sales and capture a larger share of the vehicle maintenance market.

- In June 2025, Petra Automotive Products introduced PETRABLADES premium beam wiper blades, designed for enhanced all-weather performance with even pressure distribution and durable construction to improve driver visibility in rain, snow, and sleet. The new product line aims to strengthen Petra’s aftermarket portfolio by offering higher reliability and longer service life compared to traditional frame-style blades

Companies Covered in Automotive Wipers Market

- Bosch

- Valeo

- Denso

- Trico

- Federal-Mogul

- Aisin Seiki

- Hyundai Mobis

- Continental

- Magneti Marelli

- Nippon Wiper

- Hanon Systems

- Mando Corporation

Frequently Asked Questions

The global automotive wipers market is projected to reach US$ 5.0 billion in 2026.

Increasing vehicle production, growing vehicle parc, regulatory emphasis on visibility and safety, and technological adoption in wiper systems are driving market growth.

The market is poised to witness a CAGR of 4.5% between 2026 and 2033.

Rapid motorization in emerging economies, integration of smart and energy-efficient wiper systems, and recurring aftermarket replacement demand are key opportunities.

Bosch, Valeo, Denso, Trico, Robert Bosch Automotive Steering, Aisin Seiki, and Continental are some of the leading players.