- Automotive

- Automotive eCall Market

Automotive eCall Market Size, Share, and Growth Forecast, 2026 - 2033

Automotive eCall Market by Vehicle Type (Passenger Cars, Commercial Vehicles, Others), Trigger Type (Automatically Initiated eCall, Manually Initiated eCall, Others), Propulsion Type, Connectivity Type, and Regional Analysis for 2026 - 2033

Automotive eCall Market Size and Trends Analysis

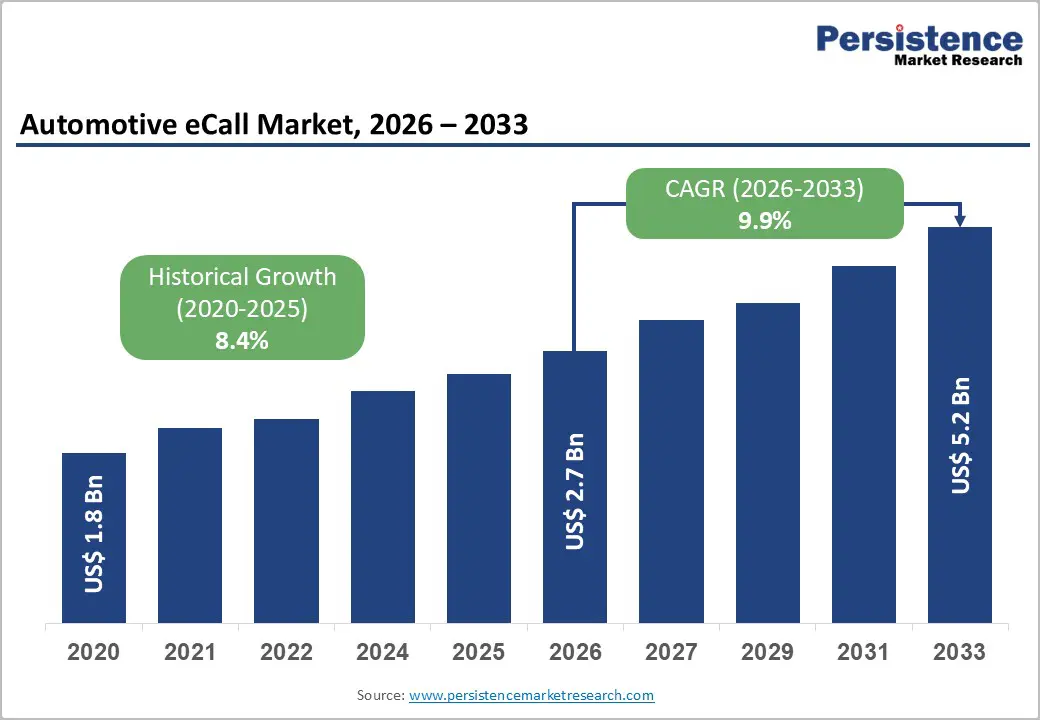

The global automotive eCall market size is likely to be valued at US$2.7 billion in 2026 and is expected to reach US$5.2 billion by 2033, growing at a CAGR of 9.9% between 2026 and 2033, driven by regulatory mandates, rapid advancements in vehicle connectivity, and the increasing integration of safety-critical systems within modern automotive architectures. The transition toward 4G/5G-enabled emergency communication systems and the proliferation of electric and connected vehicles are accelerating adoption. OEMs and suppliers are investing in telematics platforms that support emergency response, predictive safety, and real-time vehicle diagnostics.

Key Industry Highlights:

- Leading Region: Europe is projected to account for approximately 38.2% of the market share, driven by mandatory 112-based eCall regulations and strong automotive manufacturing infrastructure.

- Fastest-growing Region: Asia Pacific is the fastest-growing region, supported by rapid electric vehicle adoption, expanding vehicle production, and increasing integration of connected safety technologies across China, India, and Southeast Asia.

- Investment Plans: Significant investments are being directed toward 4G/5G-enabled telematics upgrades, software-defined vehicle platforms, and V2X communication technologies, particularly by OEMs and tier-1 suppliers aiming to replace legacy 2G/3G-based systems.

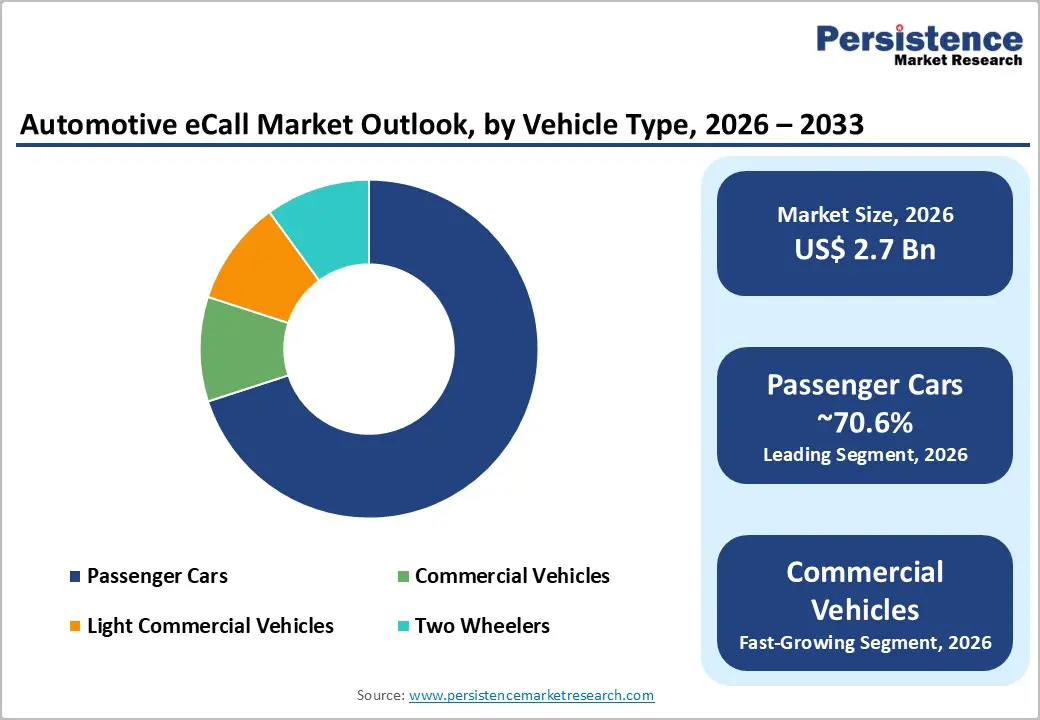

- Dominant Vehicle Type: Passenger cars dominate the market with an anticipated 70.6% market share, supported by regulatory mandates and large-scale global production volumes.

- Leading Trigger Type: Automatically initiated eCall leads with an anticipated 65.4% market share, owing to its integration with crash detection systems and its critical role in ensuring immediate emergency response without driver intervention.

| Key Insights | Details |

|---|---|

| Automotive eCall Market Size (2026E) | US$2.7 Bn |

| Market Value Forecast (2033F) | US$5.2 Bn |

| Projected Growth (CAGR 2026 to 2033) | 9.9% |

| Historical Market Growth (CAGR 2020 to 2025) | 8.4% |

DRO Analysis

Driver Analysis - Regulatory Mandates Driving Universal Adoption

Regulatory enforcement remains the most significant growth catalyst for the automotive eCall market. The European Union mandates the installation of 112-based eCall systems in all new passenger cars and light commercial vehicles, creating a standardized baseline for deployment. Recent regulatory updates emphasize compatibility with next-generation communication networks, particularly 4G and 5G, as legacy 2G/3G networks are being phased out. This transition is creating a mandatory upgrade cycle, compelling OEMs and suppliers to redesign embedded systems. The regulatory push ensures sustained demand for compliant hardware, software integration, and certification services, reinforcing long-term market stability.

Expansion of Electric and Connected Vehicles

The rapid growth of electric vehicles (EVs) and connected mobility ecosystems is significantly influencing eCall adoption. Global EV sales surpassed 17 million units in 2024, reflecting strong momentum in electrification. EV platforms rely heavily on centralized electronic architectures and continuous connectivity, making them inherently compatible with integrated emergency communication systems. As vehicles evolve into software-defined platforms, eCall functionality is increasingly embedded within broader telematics and safety systems rather than deployed as standalone modules. This convergence enhances system efficiency and reduces incremental deployment costs, accelerating adoption across vehicle segments.

Rising Emphasis on Crash Response and Public Safety Integration

Governments and transportation authorities are prioritizing faster emergency response mechanisms to reduce road fatalities. Advanced telematics systems now enable real-time crash detection, location tracking, and automatic communication with emergency services. Increasing collaboration between automotive manufacturers, telecom providers, and emergency response agencies is strengthening the ecosystem for connected safety solutions. The integration of eCall with broader intelligent transportation systems is expanding its role beyond compliance, positioning it as a critical component of next-generation road safety infrastructure.

Restraint Analysis - Dependence on Legacy Communication Infrastructure

A significant portion of existing eCall systems relies on 2G and 3G networks, which are being systematically phased out across major markets. This creates a technology obsolescence risk, as older systems may become non-functional before the end of a vehicle’s lifecycle. OEMs and fleet operators face additional costs related to system upgrades, retrofitting, and recertification. The transition to 4G/5G also introduces hardware redesign requirements, increasing development complexity and extending product validation timelines.

Regulatory Fragmentation and Compliance Complexity

Despite progress toward harmonization, regional differences in regulatory frameworks continue to pose challenges. Variations in certification processes, data privacy requirements, and telecommunications standards require suppliers to develop market-specific solutions. This increases engineering costs, complicates global platform standardization, and slows time-to-market. For multinational OEMs and tier-1 suppliers, managing multiple compliance pathways reduces operational efficiency and impacts scalability.

Opportunity Analysis - High-Growth Potential in Asia Pacific Markets

Asia Pacific represents a major expansion opportunity due to rapid vehicle production growth and increasing adoption of connected technologies. Countries such as China, India, and Japan are experiencing strong demand for advanced automotive safety systems, driven by urbanization, regulatory evolution, and rising consumer awareness. The region’s dominance in EV manufacturing further accelerates the integration of telematics and emergency communication systems. Suppliers that establish localized production and scalable platforms can capitalize on high-volume demand and cost advantages.

Emergence of Software-Driven and Service-Based Ecall Models

The shift toward software-defined vehicles is enabling the development of highly flexible and scalable eCall architectures, including tethered and third-party service (TPS) models. These solutions reduce reliance on dedicated embedded hardware by leveraging smartphone connectivity, cloud computing, and over-the-air (OTA) software updates, allowing OEMs to deploy emergency communication features more efficiently across a wider range of vehicle price segments. This transition is particularly valuable for mid-range and entry-level vehicles, where cost sensitivity has traditionally limited the adoption of advanced safety systems. By integrating eCall into broader connected service ecosystems, automakers can also unlock recurring revenue streams through subscription-based offerings such as emergency assistance, roadside support, vehicle tracking, and remote diagnostics. For instance, companies such as HARMAN International and Qualcomm Incorporated are actively developing cloud-enabled automotive platforms that support real-time communication, data analytics, and service scalability, reinforcing the shift toward software-centric business models.

Expansion into New Vehicle Segments and Mobility Use Cases

The application of eCall systems is expanding beyond passenger cars into commercial fleets, two-wheelers, and shared mobility platforms, significantly broadening the addressable market. In commercial fleets, eCall integration enhances driver safety, fleet visibility, and operational efficiency, enabling faster emergency response and minimizing downtime in logistics and transportation operations. For example, suppliers such as ZF Friedrichshafen AG are focusing on connected safety solutions tailored for commercial vehicles, integrating emergency communication with fleet management systems. In the two-wheeler segment, particularly in emerging markets such as India and Southeast Asia, rising accident rates and urban congestion are driving demand for compact, cost-effective emergency communication modules. Shared mobility platforms and ride-hailing services are also beginning to incorporate eCall functionality as part of their safety infrastructure, enhancing passenger trust and regulatory compliance. As mobility ecosystems evolve, eCall is increasingly integrated with adjacent technologies such as predictive maintenance, driver behavior monitoring, real-time accident analytics, and insurance telematics, transforming it from a standalone emergency feature into a multifunctional safety and data platform. This convergence is expected to significantly increase market penetration while creating new opportunities for innovation and service differentiation.

Category-wise Analysis

Vehicle Type Insights

Passenger cars dominate with an anticipated 70.6% market share in 2026, due to regulatory mandates, high global production volumes, and early adoption of embedded safety technologies. Mandatory eCall implementation in this category, particularly across European markets, has established a strong compliance-driven baseline, ensuring that most newly produced passenger vehicles are equipped with integrated emergency communication systems. In addition, passenger cars benefit from advanced electronic architectures, centralized control units, and standardized telematics platforms, which simplify eCall integration at the OEM level. For example, leading automakers such as BMW, Mercedes-Benz, and Volkswagen have embedded eCall functionalities within their connected car ecosystems, enabling automatic crash alerts and real-time location tracking. The extensive global vehicle parc further supports recurring demand for upgrades, especially as legacy systems transition from 2G/3G to 4G/5G connectivity.

Commercial vehicles are the fastest-growing segment and are witnessing accelerated growth due to increasing safety requirements, higher operational risks, and the rising importance of fleet management solutions. Fleet operators across logistics, public transportation, and construction sectors are increasingly adopting telematics-enabled safety systems to improve driver safety, asset utilization, and regulatory compliance. eCall systems in commercial vehicles enable immediate emergency response in case of accidents, reducing downtime and potential financial losses. For instance, logistics companies are integrating eCall with fleet monitoring platforms to enable real-time incident reporting and route optimization. Light commercial vehicles serve as a transitional category, benefiting from both regulatory influence and fleet adoption trends. Meanwhile, two-wheelers are emerging as a niche but promising segment, particularly in countries such as India and Southeast Asian markets, where high accident rates and dense urban traffic are driving demand for connected safety solutions.

Trigger Type Insights

Automatically initiated eCall leads with an anticipated 65.4% market share in 2026, as they are designed to activate instantly during severe collisions without requiring any manual intervention. These systems are typically integrated with airbag deployment sensors, crash detection algorithms, and onboard diagnostics, enabling them to transmit critical data such as vehicle location, time of incident, and crash severity to emergency response centers. Their ability to function even when occupants are unconscious or unable to respond makes them indispensable for regulatory compliance and life-saving interventions. For example, several European OEMs have implemented automatic eCall systems that trigger immediately upon airbag deployment, ensuring rapid communication with emergency services. This reliability and alignment with safety regulations make automatic eCall the standard configuration in most factory-installed systems.

Manually initiated eCall is the fastest-growing segment and is expanding rapidly due to its versatility and broader applicability beyond severe accidents. These systems allow drivers or passengers to activate emergency assistance through a dedicated in-vehicle button, making them useful for breakdowns, minor collisions, medical emergencies, or security concerns. As connected vehicle ecosystems evolve, manual eCall is increasingly integrated with infotainment systems, mobile applications, and cloud-based service platforms. For instance, many premium vehicles now include SOS buttons linked to concierge and roadside assistance services, providing immediate support in non-critical scenarios. Growth in this segment is further driven by rising consumer expectations for proactive safety features and enhanced convenience, particularly in connected and software-defined vehicles where user-initiated services play a central role.

Regional Insights

North America Automotive eCall Market Trends - Telematics-Driven Adoption without Federal Mandate

North America represents a significant growth market driven by advancements in connected vehicle technologies and increasing focus on road safety. While eCall is not mandated at the federal level, the region is witnessing strong adoption of telematics-based crash notification systems that function similarly to eCall. The U.S. leads the market, supported by a mature automotive ecosystem, high penetration of connected vehicles, and strong consumer demand for safety and convenience features. OEMs such as General Motors (with OnStar) and Ford Motor Company (with SYNC emergency assistance) have already embedded automatic crash notification systems across a wide range of models, demonstrating how eCall-like functionality is being commercialized without direct regulatory mandates.

Key growth drivers include the expansion of vehicle-to-everything (V2X) communication, increasing integration of telematics in vehicles, and rising awareness of emergency response solutions. Technology providers such as Qualcomm are strengthening V2X ecosystems through acquisitions and chipset innovations, enabling faster and more reliable communication between vehicles and infrastructure. Automakers are embedding eCall-like capabilities within broader connected service platforms, combining emergency response with navigation, diagnostics, and predictive alerts.

Insurance providers are also playing a role by promoting usage-based insurance models that leverage telematics data, incentivizing the adoption of connected safety features. Regulatory developments focus on improving emergency response infrastructure and integrating vehicle data with public safety systems. Initiatives led by the National Highway Traffic Safety Administration are enhancing 911 system compatibility with vehicle-generated crash data, which strengthens the case for automated emergency communication technologies. Investment in smart transportation and digital infrastructure, particularly in urban corridors, is supporting real-time data exchange between vehicles and emergency services. The presence of leading technology firms and strong R&D capabilities continues to accelerate innovation, positioning North America as a key region for advanced, software-driven eCall evolution.

Europe Automotive eCall Market Trends-Regulation-Led Standardization and 112 eCall Dominance

Europe is projected to lead the market with approximately 38.2% market share in 2026, driven by stringent regulatory mandates and a well-established automotive industry. The mandatory implementation of 112-based eCall systems across all new passenger cars and light commercial vehicles has created a uniform and enforceable framework, ensuring widespread adoption. This regulatory clarity has enabled OEMs and suppliers to standardize system design and scale deployment efficiently across the region. Germany, the U.K., France, and Spain are the key contributors, supported by strong vehicle production and advanced supplier ecosystems. Major European OEMs such as BMW, Volkswagen, and Stellantis have integrated eCall into their connected vehicle platforms, often linking it with digital cockpit systems and telematics services. On the supplier side, companies such as Continental AG and Robert Bosch GmbH are leading innovation in telematics control units and embedded communication modules, enabling compliance with evolving regulatory standards.

The region benefits from a high level of regulatory harmonization, which simplifies cross-border deployment and ensures interoperability of emergency services. Recent updates to eCall standards emphasize compatibility with 4G/5G networks, prompting OEMs to upgrade existing systems and phase out legacy technologies. This transition is creating a significant replacement and modernization cycle, particularly for vehicles equipped with older communication modules. Investment in connected vehicle technologies and digital infrastructure continues to accelerate market growth. European governments are also focusing on road safety and sustainability initiatives, further strengthening demand for advanced emergency communication systems. The integration of eCall with broader intelligent transportation systems and smart city projects is enhancing its functionality, positioning Europe as the most mature and regulation-driven market globally.

Asia Pacific Automotive eCall Market Trends - EV Expansion and High-Growth Telematics Integration

Asia Pacific is the fastest-growing region, driven by rapid industrialization, increasing vehicle production, and strong adoption of electric vehicles. China dominates the regional market due to its large automotive manufacturing base and leadership in EV production, while Japan and South Korea contribute through advanced technological innovation. India and Southeast Asia offer significant growth potential due to rising vehicle ownership and increasing focus on road safety.

Key growth drivers include rising consumer awareness of vehicle safety, expanding government initiatives, and the rapid development of connected vehicle ecosystems. Chinese automakers such as BYD and SAIC Motor are integrating advanced telematics and emergency response features into electric vehicles, aligning with the country’s broader smart mobility strategy. In Japan, suppliers like DENSO Corporation are advancing connected safety technologies, supporting OEMs with integrated telematics and communication modules.

The region’s cost advantages in electronics manufacturing, particularly in China and Southeast Asia, enable large-scale production of telematics components at competitive prices. This supports the deployment of eCall systems across both premium and mid-range vehicle segments. In India, increasing regulatory focus on vehicle safety and the expansion of digital infrastructure are creating a favorable environment for future adoption, especially in urban areas with high traffic density. Investment trends indicate strong growth in telematics infrastructure and smart mobility solutions.

Governments across the region are exploring frameworks to integrate vehicle data with emergency response systems, similar to global best practices. OEMs are embedding advanced safety features into new models, while partnerships between automakers and technology firms are accelerating innovation. The combination of high production volumes, rapid electrification, and digital transformation positions Asia Pacific as the primary growth engine for the automotive eCall market over the forecast period.

Competitive Landscape

The global automotive eCall market exhibits a moderately concentrated structure at the hardware level and a more fragmented landscape in software and service segments. Leading tier-1 suppliers dominate system integration and component supply, while smaller players focus on specialized software solutions and regional deployments. Competitive positioning is influenced by technological capability, regulatory compliance, and global manufacturing presence. Key players are focusing on technology convergence, platform integration, and global expansion. Strategies emphasize software-defined architectures, cost optimization, and scalable solutions. Companies are leveraging partnerships, acquisitions, and innovation to strengthen their competitive position and address evolving regulatory and technological requirements.

Key Industry Developments

- In January 2025, Robert Bosch GmbH showcased its next-generation connected vehicle solutions at IAA Mobility, emphasizing software-defined architectures that integrate emergency communication, vehicle control, and real-time data processing to enhance safety and response capabilities.

Companies Covered in Automotive eCall Market

- Robert Bosch GmbH

- Continental AG

- DENSO Corporation

- Valeo SA

- HARMAN International

- Aptiv PLC

- ZF Friedrichshafen AG

- Autoliv Inc.

- Visteon Corporation

- Panasonic Automotive Systems

- NXP Semiconductors

- Infineon Technologies AG

- Qualcomm Incorporated

- Thales Group

- u-blox Holding AG

- Quectel Wireless Solutions

Frequently Asked Questions

The global automotive eCall market is expected to be valued at US$2.7 billion in 2026.

The automotive eCall market is projected to reach US$5.2 billion by 2033.

Key trends include the transition from 2G/3G to 4G/5G communication systems, increasing adoption of software-defined vehicle architectures, integration of eCall with connected services and V2X technologies, and the expansion of eCall functionality into electric vehicles and commercial fleets.

The passenger cars segment leads the market, holding an anticipated 70.6% share, driven by regulatory requirements and large-scale production volumes.

The automotive eCall market is expected to grow at a CAGR of 9.9% from 2026 to 2033.

Some of the major players include Robert Bosch GmbH, Continental AG, DENSO Corporation, Valeo SA, and HARMAN International.