- Hardware & Software IT Services

- Data Management Platforms Market

Data Management Platforms Market Size, Share, and Growth Forecast 2026 - 2033

Data Management Platforms Market by Data Source (First Party Data, Second Party Data and Third-Party Data), by Deployment (Cloud-based and On-premises), and End- user (Media Agency, Brand/Retailer, Publisher and Ad Network) and Regional Analysis for 2026 - 2033

Data Management Platforms Market Size and Trend Analysis

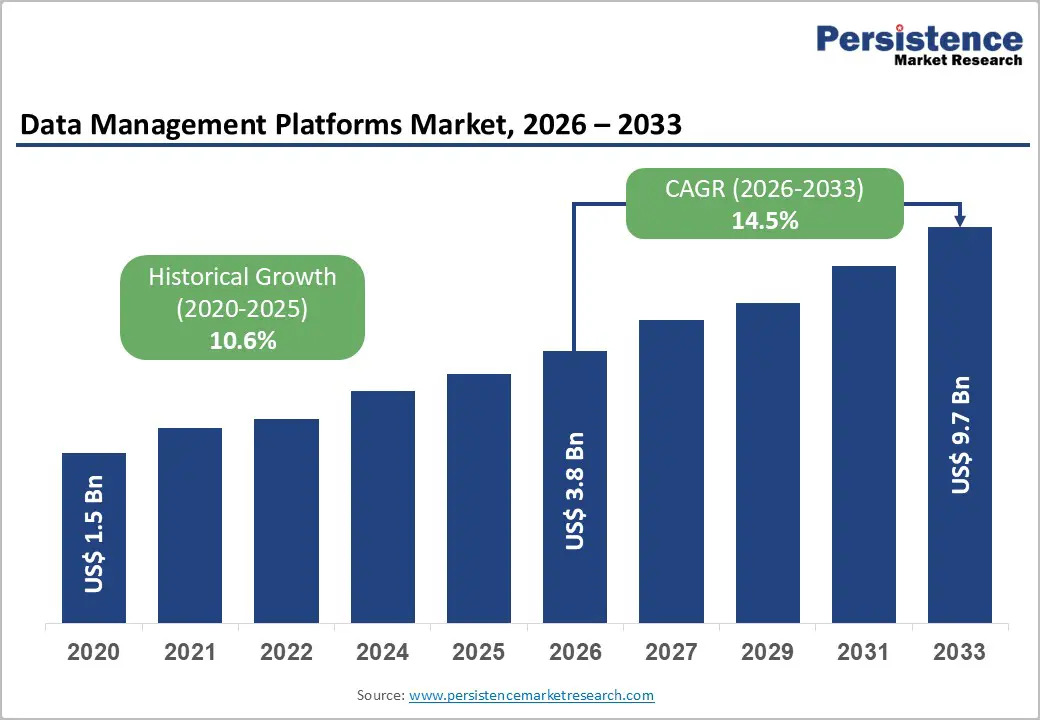

The global Data Management Platforms (DMPs) Market size was valued at US$ 3.8 Bn in 2026 and is projected to reach US$ 9.7 Bn by 2033, growing at a CAGR of 14.4% between 2026 and 2033. Is market expansion driven by escalating demand for the first-party data strategies as advertisers pivot away from deprecated third-party cookies, along with intensified regulatory pressures, including GDPR, CCPA, and emerging global data privacy frameworks mandating transparency in data collection and usage.

Key Market Highlights

- Leading region: North America dominates the Data Management Platforms Market, driven by the concentration of major DMP vendors, advanced enterprise data adoption, stringent privacy regulations such as CCPA, and substantial investments by advertisers and publishers in first-party data strategies and omnichannel marketing.

- Fastest-growing region: Asia Pacific is the fastest-growing market for data management platforms, fueled by rapid e-commerce expansion in China and India, escalating digital advertising investments, government digital transformation initiatives, and the emergence of local vendors innovating around live streaming and retail media ecosystems.

- Dominant segment: First-Party Data dominates as the primary data source segment, accounting for roughly 52% of platform focus, driven by third-party cookie deprecation, superior ROI metrics, and regulatory compliance incentives pushing advertisers and publishers toward zero and first-party data strategies.

- Fastest growing segment: Cloud-Based Deployment is the fastest-growing deployment segment, commanding 60% of market revenue and expanding rapidly due to scalability advantages, cost efficiency, seamless integration with modern data stacks, and native compatibility with privacy frameworks and real?time activation requirements.

- Key market opportunity: Integration of DMPs with Retail Media Networks and Customer Data Platforms, combined with AI-powered audience intelligence and autonomous optimization, represents the most attractive growth opportunity as retailers and brands monetize first-party data through direct advertiser relationships and personalized, real-time customer engagement.

| Key Insights | Details |

|---|---|

|

Data Management Platforms Market Size (2026E) |

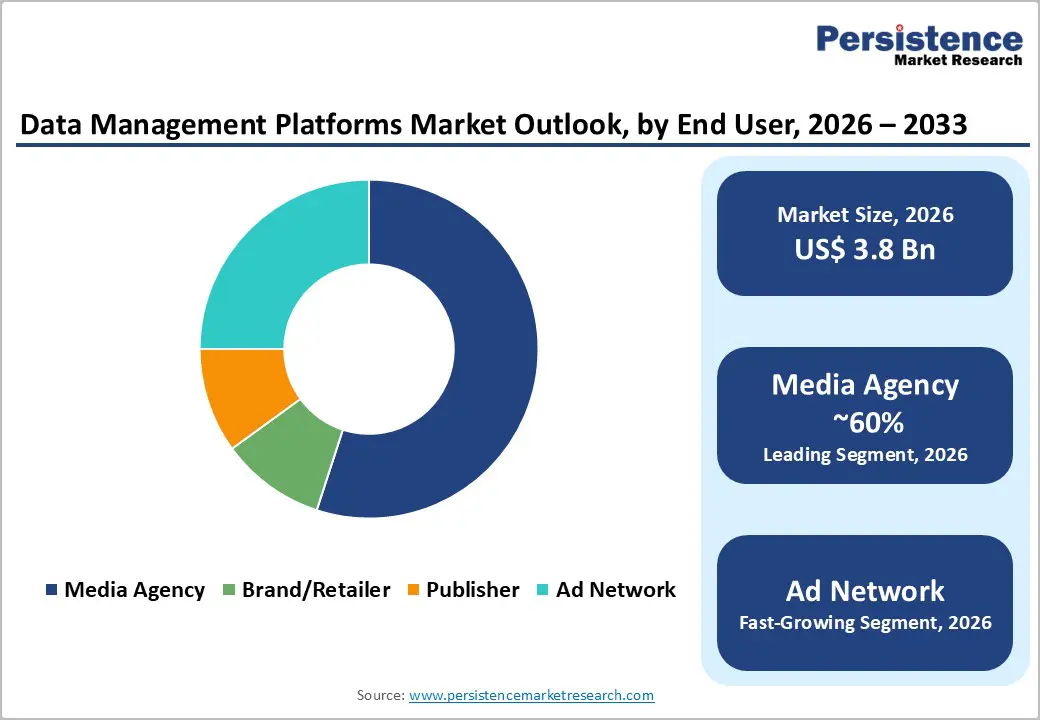

US$ 3.8 Bn |

|

Market Value Forecast (2033F) |

US$ 9.7 Bn |

|

Projected Growth (CAGR 2026 to 2033) |

14.4% |

|

Historical Market Growth (CAGR 2020 to 2024) |

10.6% |

Market Dynamics

Market Growth Drivers

Transition to First?Party Data and Privacy?Compliant Marketing Strategies

The accelerating deprecation of third-party cookies, driven by Google Chrome's phased rollout beginning in early 2024 and extending through 2026, 2026 is fundamentally reshaping how advertisers collect and activate audience data. Research indicates that 71% of publishers in Q1 2026 recognized first-party data as a critical source of advertising performance improvement, up from 64% in 2024, with 85% expecting first-party data's monetization role to expand further in 2026. First-party data strategies deliver measurable advantages, including 8× higher return on ad spend and 25% lower cost per acquisition compared to third-party approaches, incentivizing heavy investment in data management platforms that unify, segment, and activate proprietary customer data across channels. As the Data Migration Market grows in parallel with infrastructure modernization, enterprises are increasingly migrating legacy audience data to cloud-based DMPs equipped with consent management, identity resolution, and real-time activation capabilities.

Regulatory Compliance and Real?Time Omnichannel Marketing Demands

Stringent data privacy regulations, including GDPR in Europe, CCPA in California, and eight additional U.S. state laws expected by 2026, have made compliance and transparency non-negotiable across the advertising ecosystem. DMPs that embed privacy-by-design principles, automated consent workflows, and audit trails for data usage are becoming essential infrastructure for brands, agencies, and publishers. Simultaneously, competitive pressures demand real-time, cross-channel activation of personalized content and offers, requiring DMPs to integrate seamlessly with DSPs, SSPs, CRMs, and analytics platforms. The complexity of managing fragmented data across websites, mobile applications, CRM systems, and offline touchpoints necessitates centralized platforms that provide a single customer view and enable instantaneous campaign adjustments, driving sustained DMP adoption, especially among large enterprises handling massive data volumes.

Market Restraints

High Implementation Costs and Complex Data Integration Challenges

Despite strong adoption momentum, DMPs require substantial upfront capital investment, particularly for enterprises managing large-scale data operations across multiple channels and geographies. Deployment costs include hardware infrastructure, software licensing, integration with legacy systems, and hiring specialized data engineering and analytics talent, which are especially prohibitive for small and mid-sized marketing departments and agencies. Additionally, achieving clean, unified customer data requires extensive data governance, validation, and enrichment processes, often delayed by technical debt in legacy marketing technology stacks and organizational inertia around data standardization and access controls.

Cybersecurity Risks and Data Breach Liabilities

As DMPs centralize vast quantities of sensitive customer data, including personally identifiable information, behavioural data, and purchase history, they become attractive targets for cyber-attacks and data theft. High-profile breaches and evolving regulatory penalties for non-compliance create litigation and reputational risks that can deter adoption, particularly among risk-averse industries such as financial services and healthcare. Furthermore, managing consent at scale across global jurisdictions with disparate rules, handling right-to-deletion requests, and maintaining audit trails adds operational complexity and cost burden that slower organizations struggle to manage.

Market Opportunities

Convergence of DMPs with Customer Data Platforms and Retail Media Networks

The boundary between traditional DMPs and Customer Data Platforms (CDPs) is blurring, with leading providers such as Oracle, Adobe, and Salesforce expanding unified platforms that combine audience segmentation, first-party data activation, and real-time personalization. Simultaneously, the explosive growth of retail media networks, where retailers like Walmart, Amazon, and Target leverage their proprietary customer data to offer direct advertiser access, creates immense opportunities for DMPs that can securely manage, segment, and monetize retail audiences. Are retailers building sophisticated DMP capabilities to enable first-party audience sales and direct advertiser relationships, generating new revenue streams that dwarf traditional advertising margins?

AI-Powered Predictive Analytics and Autonomous Campaign Optimization

The integration of machine learning, artificial intelligence, and automated optimization into DMPs is unlocking new value propositions for clients, including predictive audience modelling, real-time churn prediction, and autonomous campaign optimization across channels. Platforms like Innovid, Rocket Fuel, and Lotame are embedding AI-driven features that identify lookalike audiences, predict customer lifetime value, and dynamically adjust messaging and media allocation to maximize ROI. As AI capabilities mature and become more accessible to mid-market advertisers, DMPs that offer intuitive AI-powered workflows without requiring extensive data science expertise are expected to experience accelerated adoption. Additionally, the emergence of privacy-safe identity solutions and contextual targeting alternatives, such as Google's Privacy Sandbox and proprietary identity networks, is creating opportunities for DMPs to position themselves as bridges between traditional targeting and emerging privacy. first technologies.

Category wise Insights

Data Source Analysis

First-Party Data dominates the data Management platforms market by data source composition, accounting for an estimated 52% of strategic focus and revenue potential as advertisers prioritize zero? and first?party data collection and activation. The shift is driven by deprecating third-party cookies, privacy regulations, and superior performance metrics first-party data sources deliver direct customer insights from website interactions, mobile apps, CRM systems, and loyalty programs, enabling granular segmentation and personalization without reliance on external data brokers.

Second-party data, shared through direct partnerships between complementary brands or via industry data collaboratives, represents approximately 20% of demand, providing quality-assured enrichment and audience expansion capabilities while maintaining transparency and compliance.

Deployment Analysis

Cloud-based deployment is the dominant deployment model, commanding approximately 60% of the data management platforms market by revenue, driven by scalability, flexibility, rapid time-to-value, and cost efficiency relative to on-prem alternatives. Cloud DMPs enable advertisers to instantly scale compute and storage capacity during seasonal campaigns or promotional spikes, then scale down during low-demand periods, avoiding capital expenditure on underutilized hardware.

On-premise deployment, representing roughly 40% of the market, remains prevalent among large financial institutions, regulated industries, and enterprises with extreme data residency requirements or legacy infrastructure investments requiring extended depreciation cycles.

End?User Analysis

Media Agencies and Advertisers/Brands collectively dominate the end-user landscape, accounting for an estimated 65% of DMP demand and revenue, reflecting their role as primary drivers of audience targeting strategy and programmatic media buying. Agencies manage multi-client data operations, requiring sophisticated DMPs for tag management, audience modelling, cross-device tracking, campaign reporting, and ROI attribution features that justify premium DMP pricing.

Publishers represent an estimated 15% of demand, leveraging DMPs to aggregate first-party audience data from their digital properties, enrich segments with contextual and behavioural signals, and maximize CPM yields for both direct-sold and programmatic inventory.

Regional Insights

North America Data Management Platforms Market Trends

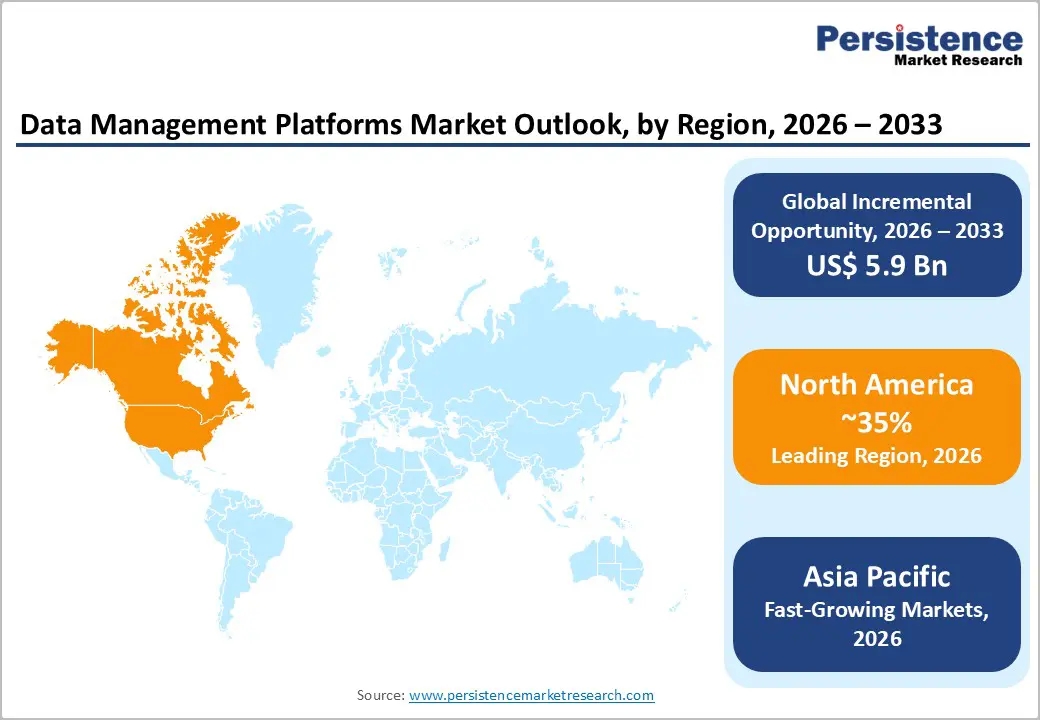

North America, led by the United States, dominates the global Data Management Platforms Market, commanding roughly 35% of revenue due to the concentration of major DMP vendors (Oracle BlueKai, Adobe Audience Manager, Salesforce DMP, Neustar, Lotame), a sophisticated advertising technology ecosystem, and advanced enterprise data capabilities. The U.S. DMP market is projected to grow at a CAGR of 11.1% from 2026 to 2033, driven by the imperative to transition to first-party data strategies, compliance with CCPA and emerging state privacy laws, and escalating demand for omnichannel personalization and retail media enablement.

Regulatory pressures from the FTC, state attorneys general, and the CMA (in U.K.–based cross-border operations) have elevated expectations around consent management, data governance, and security compliance, making privacy-first and transparent DMP solutions increasingly valuable. The region's robust venture capital ecosystem and innovation culture continue to spawn DMP startups and feature innovations, though consolidation among larger platforms remains active, with Adobe, Oracle, and Salesforce continuously expanding portfolios through acquisition and product development.

Europe Data Management Platforms Market Trends

Europe, constrained by GDPR and related regulations, has historically seen slower DMP adoption, yet the market is experiencing renewed growth as publishers and advertisers implement first-party data strategies compliant with EU directives. Key markets such as Germany, the U.K., France, and Spain are adopting DMPs to manage first-party audience data, implement consent workflows, and support emerging regulatory frameworks around AI risk assessments and identity resolution.

European data privacy regulations continue to harmonize, with EDPB guidelines, ePrivacy Directive updates, and forthcoming AI Act implementations creating incentives for sophisticated, audit-ready DMP solutions. Regional vendors emphasizing compliance, interoperability with European martech providers, and privacy-by-design architecture are gaining traction alongside global leaders, supporting moderate but steady market expansion across the region through 2033.

Asia Pacific Data Management Platforms Market Trends

Asia Pacific is the fastest?growing regional market for data management platforms, driven by rapid e?commerce expansion, digital advertising growth in China, India, and Southeast Asia, and increasing digitalization of marketing operations among large enterprises. China holds the largest market share in the region, with major platforms like Alibaba, ByteDance, and Tencent embedding DMP capabilities into their ecosystem offerings, and domestic martech vendors innovating rapidly around live-streaming commerce and mini-program monetization. India's DMP market is expanding alongside the country's digital advertising growth, with government initiatives promoting digital payments and e-commerce adoption creating opportunities for data management and audience activation platforms serving mid-market brands and growing e-commerce retailers.

Japan and South Korea feature mature advertising markets and tech-savvy advertisers increasingly investing in audience data capabilities, while ASEAN economies present emerging opportunities as digital advertising penetration rises. The region's manufacturing advantages, large-scale e-commerce ecosystems, and availability of technical talent are attracting DMP providers and creating a vibrant landscape of domestic and global vendors competing on price, localization, and industry-specific features, positioning Asia Pacific for CAGR potentially exceeding 18% through 2033.

Competitive Landscape

The Data Management Platforms Market is moderately consolidated, with leading players such as Oracle Corporation (through BlueKai), Adobe Systems Incorporated (through Audience Manager), and Salesforce commanding substantial combined market share, while a diverse set of specialized vendors including Neustar, Inc., Lotame Solutions, Inc., Innovid, Cxense ASA, and Rocket Fuel, Inc. compete on differentiation, vertical expertise, and niche capabilities.

Market leaders emphasize integrated platforms combining DMPs with CDP, DSP, and analytics capabilities, leveraging cross-selling to existing customer bases and creating switching costs. Emerging business models include API-first, composable platforms allowing modular integration with client technology stacks; privacy-safe identity solutions and contextual targeting alternatives; and AI-powered audience intelligence and autonomous optimization.

Key Market Developments

- In October 2025, CertifyOS launched an end-to-end Provider Data Management Platform, Provider Hub, designed to eliminate fragmentation and reduce costs in healthcare operations. This platform unifies and automates the management of provider data, including credentialing, directories, claims, and rosters, into a single, AI-powered source of truth. By cleansing, normalizing, and validating data from over 1,600 primary sources, CertifyOS aims to reduce manual efforts, minimize data silos, and lower operational costs.

- In April 2025, BlueConic introduced the Customer Growth Engine (CGE), a next-generation platform that transcends traditional Customer Data Platforms (CDPs). Designed to transform first-party data into actionable revenue strategies, the CGE leverages AI-driven audience intelligence, predictive modeling, and omnichannel orchestration to enhance customer acquisition, retention, and lifetime value.

Companies Covered in Data Management Platforms Market

- A.O. Smith

- Bosch Thermotechnology Corp.

- Ariston Holding N.V.

- Rheem Manufacturing Company.

- Rinnai America Corporation.

- Bradford White Corporation, USA.

- Noritz America Corp

- Whirlpool.

- Westinghouse Electric Corporation.

- Bajaj Electricals India.

- Others Key Players

Frequently Asked Questions

The global Data Management Platforms Market is projected to reach approximately US$ 9.7 billion by 2033, expanding from US$ 3.8 billion in 2026, at a forecast CAGR of 14.4% between 2026 and 2033.

Key demand drivers include the transition to first‑party data strategies as third‑party cookies deprecate, escalating regulatory compliance pressures from GDPR, CCPA, and emerging global data privacy laws, and intensifying demand for omnichannel marketing, real‑time audience activation, and AI‑powered personalization across customer touchpoints.

First‑Party Data leads the Data Management Platforms Market by data source composition, accounting for approximately 52% of strategic platform focus and revenue potential, driven by superior performance metrics, regulatory compliance advantages, and deprecating third‑party cookies forcing advertisers and publishers to prioritize owned customer data strategies.

North America, particularly the United States, dominates the global Data Management Platforms Market, commanding approximately 35% of revenue through the concentration of major vendors, sophisticated advertising technology ecosystems, and substantial investments by enterprises in data unification and audience activation platforms.

Major players include Oracle Corporation, Adobe Systems Incorporated, Neustar, Inc., Salesforce, Inc., Innovid, Lotame Solutions, Inc., The Trade Desk, Inc., Rocket Fuel, Inc., MediaMath, Inc., Krux Digital, LLC, eXelate, Inc., Cxense ASA, KBM Group LLC, Turn Inc., and Nielsen Marketing Cloud.