- Construction & Engineering

- Artificial Intelligence (AI) in Construction Market

Artificial Intelligence (AI) in Construction Market Size, Share, and Growth Forecast, 2026 - 2033

Artificial Intelligence (AI) in Construction Market by Component (Software Solutions, Hardware & Edge Devices, Services), Application (Project Management & Planning, Field Operations & Site Management, Risk Compliance & Safety Management, Supply Chain & Logistics Optimization, Quality Control & Defect Detection, Others), Technology (ML & DL, Computer Vision, NLP, Robotics & Autonomous Systems, Generative AI, Digital Twin & Simulation Intelligence), and Regional Analysis for 2026 - 2033

Artificial Intelligence (AI) in Construction Market Share and Trends Analysis

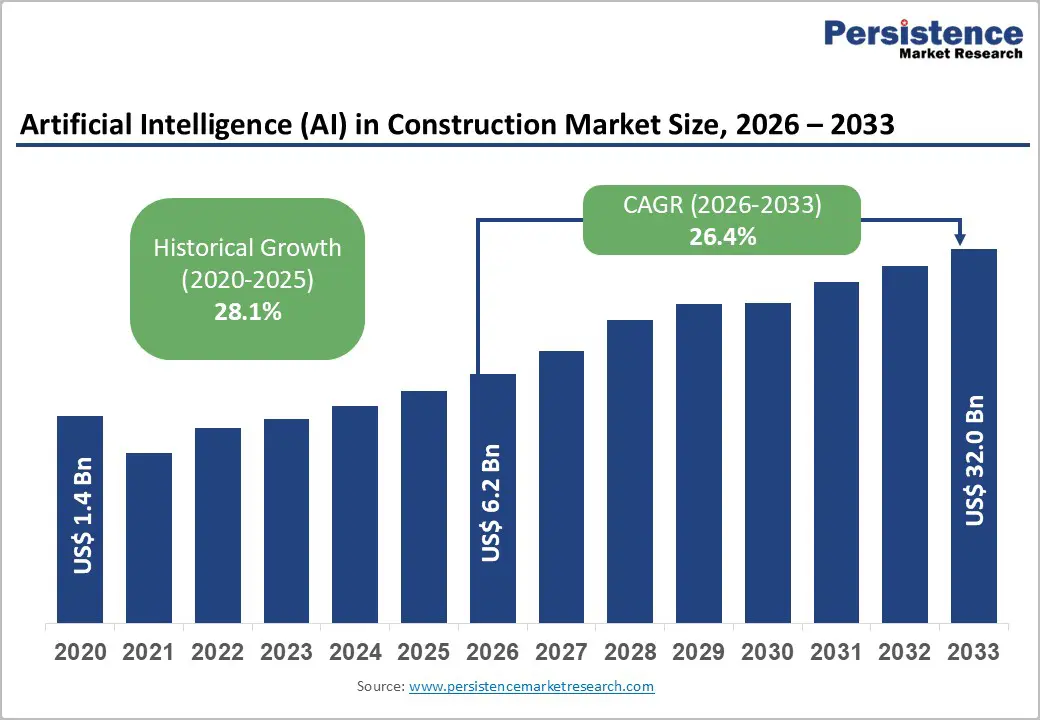

The global artificial intelligence (AI) in construction market size is likely to be valued at US$ 6.2 billion in 2026, and is estimated to reach US$ 32.0 billion by 2033, growing at a CAGR of 26.4% during the forecast period 2026 - 2033.

Sustained productivity gaps in construction, rising infrastructure investment, and the heightened need for data-driven risk mitigation across project lifecycles are aiding market expansion. AI adoption is increasingly shifting from point solutions toward integrated platforms embedded in planning, design, execution, and asset management workflows. Public infrastructure stimulus programs in the United States, Europe, and the Asia Pacific are increasingly mandating digital reporting, safety compliance, and performance transparency, indirectly accelerating AI uptake. At the same time, advances in computer vision, cloud computing, and generative AI are lowering deployment friction and improving return on investment for large and mid-sized contractors. From 2026 onward, market growth is expected to remain strong but structurally moderate as AI penetration deepens across Tier-1 contractors and infrastructure owners. Growth is increasingly supported by scale-driven use cases, such as predictive cost control, autonomous site monitoring, and digital twins, rather than pilot deployments. The market is therefore evolving from a technology-led expansion phase into a value-realization phase, where vendors capable of delivering measurable productivity and risk-reduction outcomes are expected to capture disproportionate value.

Key Industry Highlights

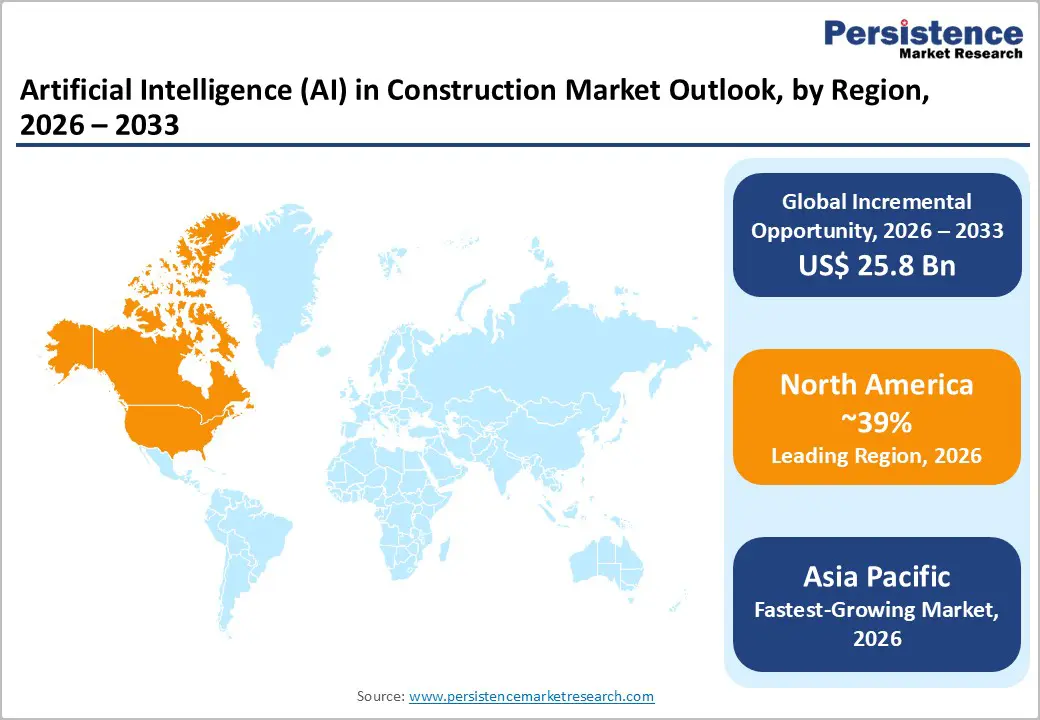

- Dominant Region: North America is expected to account for around 39% of the market share in 2026, driven by high digital maturity among contractors and sustained infrastructure spending supported by federal and state programs.

- Fastest-Growing Market: The Asia Pacific market is slated to register the highest 2026 - 2033 CAGR of around 31%, underpinned by large-scale urbanization and government-led smart infrastructure initiatives.

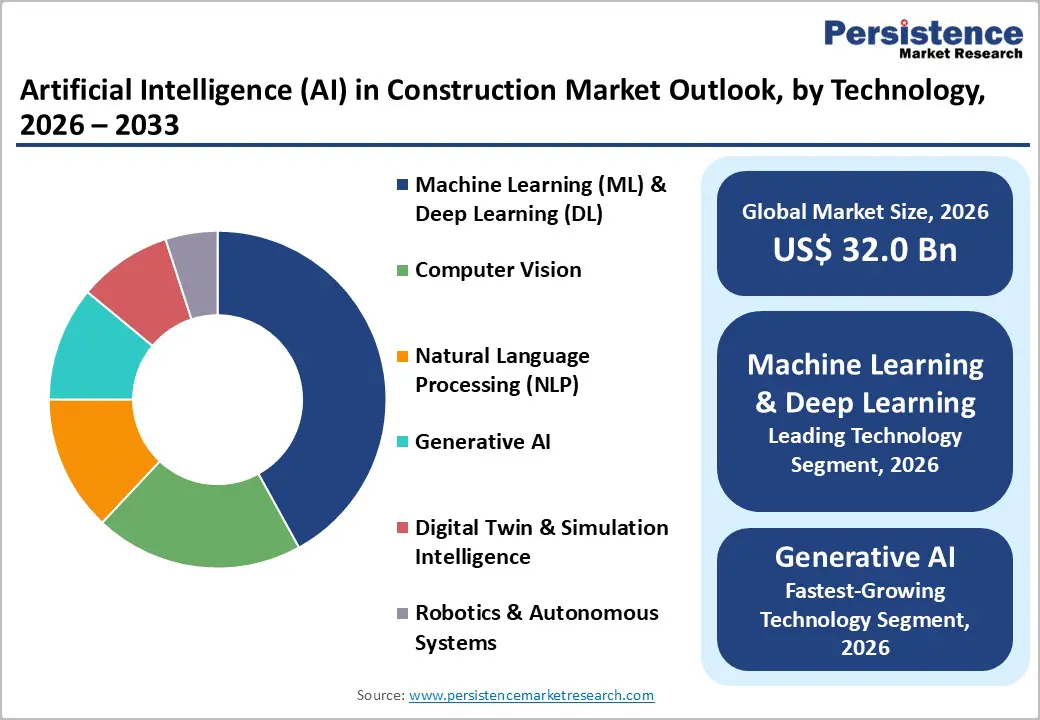

- Leading Component: AI software solutions are expected to dominate with an estimated 63.5% revenue share in 2026, reflecting strong demand for predictive project management, computer vision, and BIM-integrated analytics.

- Prime Application Area: Project management and scheduling applications are projected to contribute approximately 35% of total market revenue in 2026, supported by the widespread adoption of AI for cost forecasting and real-time progress monitoring for large and complex projects.

- Competitive Trends: The market features global construction software providers, industrial technology firms, and cloud players competing through domain-specific AI models, deep integration with building information modeling (BIM), and partnerships with original equipment manufacturers (OEMs).

- January 2026: OFA Group launched QikBIM, an AI-powered platform that converts 2D drawings into coordinated architectural, structural, and mechanical, electrical, & plumbing (MEP) BIM models in hours for projects up to 16,000 square feet.

| Key Insights | Details |

|---|---|

| Artificial Intelligence (AI) in Construction Market Size (2026E) | US$ 6.2 Bn |

| Market Value Forecast (2033F) | US$ 32.0 Bn |

| Projected Growth (CAGR 2026 to 2033) | 26.4% |

| Historical Market Growth (CAGR 2020 to 2025) | 24% |

Market Factors - Growth, Barriers, and Opportunity Analysis

Infrastructure-Led Digital Mandates and Productivity Pressure

The primary factor driving growth in the AI in construction market is the accelerating convergence of large-scale infrastructure spending and mandatory digital compliance frameworks. Governments are expanding capital expenditure on transportation, energy, and urban infrastructure while simultaneously tightening requirements around project transparency, safety reporting, and lifecycle cost management. According to the World Bank and the Organisation for Economic Co-operation and Development (OECD), global infrastructure investment needs exceed US$ 3.7 trillion annually through 2030, with advanced economies increasingly tying funding eligibility to digital project controls and reporting standards. However, construction productivity has remained stagnant for decades, growing at less than 1% annually in most developed economies, according to data from the International Labour Organization (ILO) and national statistical agencies. AI-enabled project management, computer vision-based site monitoring, and predictive analytics are increasingly being adopted as operational tools rather than innovation initiatives. These systems are enabling real-time visibility into schedule slippage, cost overruns, and safety risks, directly addressing the sector’s chronic inefficiencies.

Regulatory bodies are also reinforcing this shift. Agencies such as the U.S. Federal Highway Administration, the UK Infrastructure and Projects Authority, and the European Commission (EC) are expanding the use of BIM and digital construction standards for public projects. AI systems layered on top of BIM environments are being adopted to automate compliance checks, optimize sequencing, and simulate risk scenarios. For example, the EC is actively promoting BIM 2.0 that integrates AI as the core driver, automating design via generative algorithms that evaluate thousands of options for structural efficiency, energy use, costs, and compliance in hours. As infrastructure pipelines remain elevated over the next decade, AI adoption is continuing to shift from discretionary spend to an operational necessity, materially supporting market expansion.

Fragmented Data Ecosystems and Integration Complexity

A key structural restraint is the fragmentation of construction data across legacy systems, subcontractors, and asset owners, which is constraining scalable AI deployment. Construction projects typically involve dozens of independent stakeholders using heterogeneous software, manual documentation, and non-standardized data formats. This fragmentation significantly increases the cost and complexity of training AI models, particularly for predictive analytics and generative design applications. Integration costs remain non-trivial. Industry interviews and studies indicate that data preparation and system integration can account for 30-45% of total AI deployment costs in large construction projects. For mid-sized contractors, this cost burden delays adoption and extends payback periods beyond acceptable thresholds.

Regulatory uncertainty around data ownership and liability is also acting as a drag. AI-driven decisions related to safety, design optimization, or scheduling raise questions around accountability in the event of failure. Construction remains a highly risk-averse industry, and unresolved legal frameworks around AI-assisted decision-making are slowing adoption in safety-critical workflows. Until interoperability standards, data governance frameworks, and liability clarity improve, AI adoption is expected to remain uneven across contractor tiers and regions.

AI-Enabled Digital Twins for Infrastructure Lifecycle Management

AI-enabled digital twins are currently revolutionizing infrastructure asset lifecycles by providing a continuous stream of operational intelligence. Asset owners are presently demanding sophisticated platforms that unify the design, construction, and maintenance phases into a single source of truth. These digital replicas use real-time sensor data to monitor structural health and simulate diverse operational scenarios, which effectively reduces the risk of unforeseen failures. According to data from the Organisation for Economic Co-operation and Development (OECD), global infrastructure assets represent trillions of dollars in value, meaning even modest efficiency gains will have created multi-billion-dollar market opportunities. Stakeholders should prioritize implementing scalable AI systems today to ensure they achieve maximum financial returns throughout the lifespans of their transportation and utility networks.

Government regulations in Europe and the Asia Pacific are currently accelerating this technological momentum through strict mandates for carbon tracking and energy oversight. Authorities are increasingly requiring precise durability measures and lifecycle sustainability reports, which AI-powered digital twins are providing through automated data analysis. Solution providers are presently linking construction-phase tools to long-term operations to secure multi-year service agreements and predictable income streams. By the time the next decade concludes, firms that have developed compatible systems will have successfully solidified their leadership in a highly regulated global market. This strategic alignment is allowing internal teams to focus on high-value outcomes while integrated platforms future-proof their investments against sudden policy shifts.

Category-wise Analysis

Component Insights

In 2026, software solutions are set to occupy a dominant position, accounting for approximately 63.5% of the AI in construction market revenue. This leadership is primarily driven by strong demand for computer vision platforms, project management analytics, and BIM-integrated modules. Contractors are presently prioritizing these digital tools because they offer faster deployment cycles and measurable return on investment (ROI) through schedule optimization. By the time the current investment cycle concludes, the adoption of Software-as-a-Service (SaaS) models will have successfully lowered entry barriers for mid-sized firms. This strategic shift is ensuring that advanced analytics become a standard component of modern construction workflows.

AI-enabled services are anticipated to post the highest CAGR of around 30% from 2026 to 2033. This rapid expansion is driven by rising integration complexity and significant data engineering requirements within the sector. Construction firms are currently seeking specialized expertise in consulting and workforce training to address critical skill shortages and manage sophisticated AI ecosystems. Vendors are successfully creating high-margin revenue streams by bundling these managed services with their existing software offerings. By the end of the next decade, these service-led models will have transformed from optional add-ons into essential support frameworks for large-scale infrastructure projects.

Application Insights

Project management and scheduling are likely to remain the leading applications in 2026, accounting for an estimated 35% of the market revenue. Construction firms are increasingly deploying AI to optimize schedules, forecast costs, and track progress across complex portfolios. These systems are improving capital efficiency by identifying delays and budget deviations early in the project lifecycle. Large-scale infrastructure developments are accelerating adoption as asset owners are requiring continuous, data-backed visibility across multi-year execution timelines. AI-enabled project controls are also supporting more disciplined decision-making by integrating historical performance data with real-time site inputs, which is strengthening governance and reducing financial risk for owners and lenders.

On-site execution and safety analytics are emerging as the fastest-growing application segment, projected to expand at an approximate CAGR of 31% during the 2026 - 2033 forecast period. Construction companies are increasingly adopting computer vision-based safety monitoring, autonomous inspection drones, and real-time quality control systems to improve site-level accountability. Regulators and insurers are continuing to tighten safety and compliance expectations, which is reinforcing demand for objective, auditable data streams. AI-driven on-site systems are also reducing dependence on manual inspections while improving response times to hazards and defects. As workforce availability remains constrained, these technologies are becoming essential tools for maintaining productivity while meeting stricter safety and documentation standards.

Technology Insights

Machine learning (ML)-based predictive analytics are poised to dominate the technology landscape in 2026, with an estimated 42% share of the artificial intelligence in construction market revenue. Construction stakeholders are increasingly relying on ML models to predict costs, schedules, and execution risks using structured historical and real-time project data. These systems remain preferred due to their transparency, explainability, and lower computational intensity compared to advanced neural architectures. Project owners and contractors are using ML-driven insights to support auditability and governance, particularly in regulated public infrastructure projects. As capital providers demand clearer risk attribution, interpretable predictive models continue to play a central role in enterprise decision-making and contract oversight.

Generative and multimodal AI are poised to be the fastest-growing technology segment between 2026 and 2033. Construction firms are increasingly deploying generative systems for automated design generation, document interpretation, and conversational coordination tools across planning and execution stages. Multimodal models are integrating text, images, and sensor data to streamline workflows such as design reviews and compliance documentation. Adoption is accelerating as firms are seeking to shorten design cycles, reduce administrative workloads, and improve collaboration across distributed teams. As generative capabilities mature, these technologies are expected to be embedded in core construction platforms rather than operate as standalone tools.

Regional Insights

North America Artificial Intelligence (AI) in Construction Market Trends

North America is expected to command an estimated 39% of the AI in construction market share in 2026, benefiting from high digital maturity across large contractors, infrastructure owners, and engineering firms, which is supporting faster integration of AI into core construction workflows. Construction industry stakeholders are increasingly embedding AI into project management, safety monitoring, and cost control systems to manage complex, multi-year programs. Strong presence of established technology vendors and construction software providers is also enabling faster commercialization and enterprise-scale deployment of AI solutions across public and private projects.

The United States remains the region's primary growth engine, supported by sustained infrastructure spending under the Infrastructure Investment and Jobs Act (IIJA). Transportation, utilities, and energy projects are increasingly requiring advanced digital oversight, which is accelerating the adoption of AI-driven analytics and compliance tools. Public agencies and asset owners are demanding greater transparency, predictive risk management, and lifecycle performance tracking. As regulatory scrutiny and funding oversight are intensifying, AI systems are becoming essential for meeting reporting obligations and improving capital efficiency. North America is therefore expected to retain its leadership position while setting adoption benchmarks for other regions.

Europe Artificial Intelligence (AI) in Construction Market Trends

Europe occupies a central place in the market for construction AI solutions, primarily due to the implementation of strict EC regulatory mandates for BIM and lifecycle reporting. Regional authorities are presently enforcing these standards to ensure that all infrastructure projects comply with the sustainability goals of the European Union (EU) Green Deal. National digital construction strategies in Germany, the United Kingdom (UK), and the Nordic countries are actively accelerating the adoption of Artificial Intelligence (AI) to automate carbon tracking and energy modeling. By the time these mandates reach full maturity, stakeholders will have successfully integrated standardized data governance frameworks that align with ISO 19650 requirements. This strategic focus is turning the region into a global leader for high-fidelity digital deliverables and transparent environmental reporting.

The European market is also marked for a robust growth trajectory through 2033, as contractors prioritize digital transformation to mitigate rising material costs. Engineering firms are currently deploying AI-enabled project management tools to reduce construction waste and optimize resource allocation on large-scale public works. Furthermore, the mandatory use of Common Data Environments (CDEs) is fostering real-time collaboration across multidisciplinary teams, significantly reducing design errors. These advancements are expected to enable European firms to establish a mature ecosystem where digital-twin-ready handover packages are a standard contractual requirement. This ongoing evolution is ensuring that the regional construction sector achieves unprecedented levels of operational efficiency and long-term asset durability.

Asia Pacific Artificial Intelligence (AI) in Construction Market Trends

Asia Pacific is anticipated to be the fastest-growing market for artificial intelligence in construction, with a CAGR of approximately 32% from 2026 to 2033. This rapid expansion is primarily following large-scale urbanization and the development of infrastructure megaprojects across China, India, and Southeast Asia. Government-led smart city initiatives, such as India’s Smart Cities Mission and China’s City Brain platforms, are presently driving the integration of advanced sensors and real-time data analytics. This trajectory is successfully turning the region into a global hub for high-volume, tech-enabled building projects that prioritize long-term urban resilience.

Cost-efficient AI solutions and mobile-first deployments are playing a critical role in the digital transformation of Asian worksites. Construction teams are currently utilizing 5G-connected mobile devices and wearable sensors to monitor worker safety and track material usage in real time. These localized technologies are enabling contractors to manage complex logistics and mitigate labor shortages without incurring prohibitive upfront capital costs. The widespread adoption of these accessible digital tools will be instrumental in bridging the productivity gap in the construction industry across developing economies. This ongoing innovation ensures that regional developers can deliver massive residential and commercial projects with greater precision and significantly reduced operational waste.

Competitive Landscape

The global AI in construction market structure exhibits a moderately fragmented structure. Leading players, such as Autodesk, Oracle (Aconex), Procore Technologies, and Bentley Systems, are competing alongside specialized firms such as Alice Technologies and Doxel. These organizations are collectively capturing value by offering a diverse mix of BIM integrated platforms and industrial technology solutions. Market leaders are differentiating themselves by delivering domain-specific AI models that provide quantifiable productivity gains. This focus on localized expertise is ensuring that contractors can achieve immediate ROI through highly accurate project forecasting and automated risk management.

Strategic partnerships between software vendors, heavy equipment manufacturers, and cloud providers are currently intensifying as firms seek to offer comprehensive end-to-end solutions. Industry participants are presently forming deep integrations between AI platforms and cloud infrastructures, such as Microsoft Azure and Amazon Web Services (AWS), to enhance data interoperability. These collaborations are allowing project teams to unify fragmented site data into a single source of truth, which significantly reduces the administrative burden of manual reporting. These alliances are set to transform isolated digital tools into seamless, automated ecosystems that manage the entire asset lifecycle. This ongoing consolidation of technology is ensuring that construction firms can maintain high-margin operations while navigating increasingly complex regulatory and sustainability requirements.

Key Industry Developments

- In January 2026, Caterpillar partnered with Nvidia to integrate AI into construction equipment via the Cat AI Assistant on its Cat 306 CR Mini Excavator, leveraging Nvidia's Jetson Thor platform for real-time operator support, safety guidance, and service scheduling. The system processes 2,000 machine messages per second to build digital twins of construction sites using Nvidia Omniverse, enabling material optimization and scenario testing.

- In November 2025, Attentive.ai raised US$ 30.5 million in a Series B funding round to accelerate Beam AI, the company's automated takeoff platform serving over 1,100 contractors. The investment allows the company to expand into estimating, bidding, and collaboration workflows amid surging U.S. infrastructure demand.

- In July 2025, Parspec secured US$20 million in Series A funding to automate the procurement of MEP products through the construction supply chain using AI. The platform extracts specifications from drawings, matches compliant products from a 6 million-item database updated daily from 4,000 manufacturer sites, and streamlines quoting and submittals.

Companies Covered in Artificial Intelligence (AI) in Construction Market

- Autodesk, Inc.

- Bentley Systems, Incorporated

- Trimble Inc.

- Oracle Corporation

- SAP SE

- Dassault Systèmes SE

- Hexagon AB

- NVIDIA Corporation

- Procore Technologies, Inc.

- IBM Corporation

- Siemens AG

- Topcon Corporation

- Nemetschek Group

- Oracle Construction and Engineering

Frequently Asked Questions

The global artificial intelligence (AI) in construction market is projected to reach US$ 6.2 billion in 2026.

Construction efficiency deficits, increasing funding for public works, and the intensified requirement for analytical risk management throughout the asset lifespan are driving the market.

The market is poised to witness a CAGR of 26.4% from 2026 to 2033.

Public infrastructure investments in the United States, Europe, and Asia Pacific are increasingly mandating digital reporting, safety compliance, and performance transparency, accelerating AI uptake and unlocking high-value opportunities.

Autodesk, Inc., Bentley Systems, Trimble Inc., and Oracle Corporation are some of the key players in the market.