- Hardware & Software IT Services

- AI Edge Devices PCB Market

AI Edge Devices PCB Market Size, Share, and Growth Forecast, 2026 - 2033

AI Edge Devices PCB Market by Product (Single-layer PCB, Multi-layer PCB, High-Density Interconnect (HDI) PCB, Flexible PCB (FPC), Package Substrate, Others), Application (Consumer Electronics, Automotive, Manufacturing, Healthcare, Smart Cities, Surveillance / Security, Telecom, Others), and Regional Analysis for 2026 - 2033

AI Edge Devices PCB Market Size and Trends Analysis

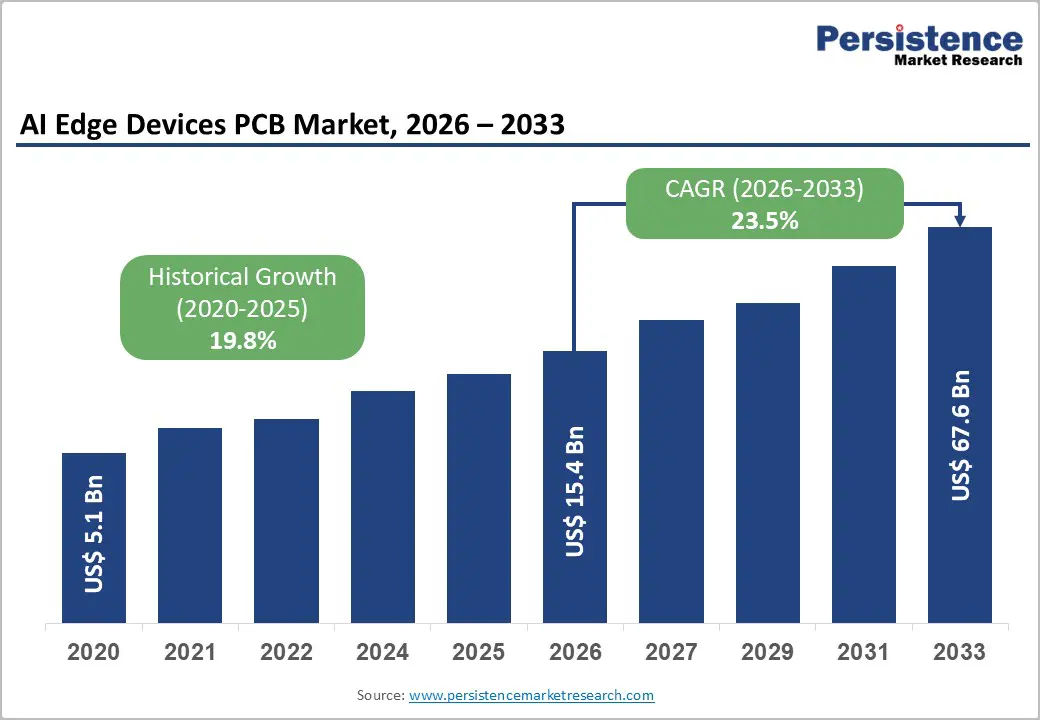

The global AI edge devices PCB market size is projected to rise from US$15.4 billion in 2026 to US$67.6 billion by 2033. It is anticipated to witness a CAGR of 23.5% during the forecast period from 2026 to 2033, driven by the rapid adoption of AI inference workloads in edge hardware, where printed circuit boards must support high-density interconnects, advanced thermal management, and reliable signal integrity for heterogeneous processors and sensors. Rising deployment of smart factories, autonomous systems, and intelligent IoT endpoints is accelerating demand for specialized PCBs that enable low-latency, on-device analytics while maintaining compact footprints and power efficiency.

Key Industry Highlights:

- Leading Product: Multi-layer PCB dominates the market with over 35% share in 2026, exceeding US$ 5.4 Bn, driven by the need for compact hardware capable of supporting high-density AI processors, memory modules, and multiple sensors in edge devices. Package Substrates represent the fastest-growing segment, supported by increasing adoption of AI accelerators, GPUs, and system-in-package (SiP) architectures, which require advanced chip packaging and high I/O density for faster edge computing performance.

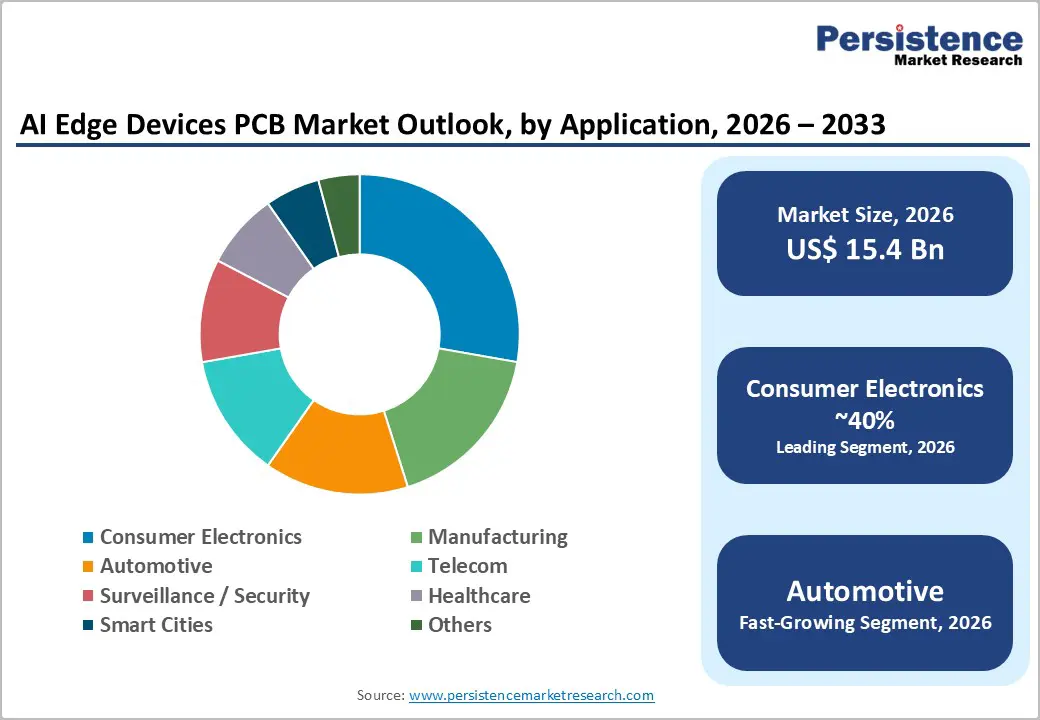

- Leading Application: Consumer Electronics holds the largest share with over 40% in 2026, valued at more than US$ 6.2 Bn, fueled by the widespread integration of AI capabilities in smartphones, wearables, smart cameras, and home assistants. These devices require compact, high-density PCBs that support multiple connectivity modules, sensors, and processors while maintaining low power consumption.

- Fast-growing Application: Automotive is projected to be the fastest-growing, driven by the rising adoption of ADAS, autonomous driving technologies, connected vehicles, and electric mobility platforms, all of which require high-performance PCB architectures for real-time sensor data processing and AI computation.

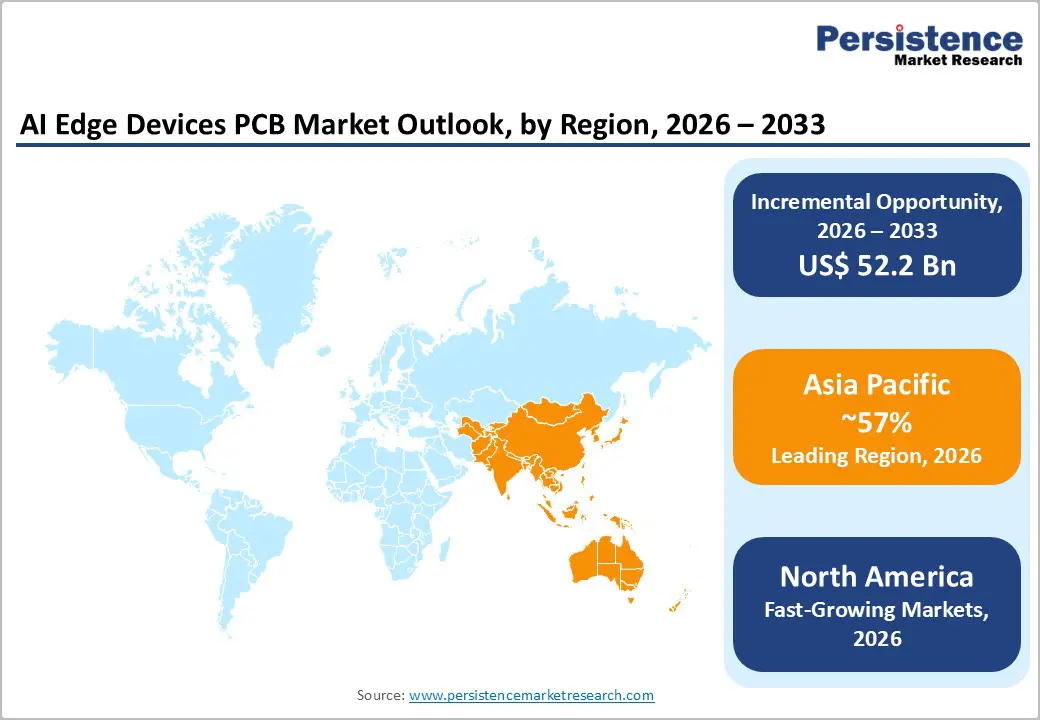

- Leading Region: Asia Pacific leads the market with over 57% share in 2026, reaching approximately US$ 9 Bn, supported by strong electronics manufacturing ecosystems in China, Taiwan, South Korea, and Japan, along with expanding semiconductor and telecom infrastructure. North America is expected to grow rapidly, driven by strong innovation in AI chips, industrial IoT, and autonomous systems.

| Global Market Attribute | Key Insights |

|---|---|

| AI Edge Devices PCB Market Size (2026E) | US$15.4 Bn |

| Market Value Forecast (2033F) | US$67.6 Bn |

| Projected Growth (CAGR 2026 to 2033) | 23.5% |

| Historical Market Growth (CAGR 2020 to 2025) | 19.8% |

Market Dynamics

Driver - Rapid Growth of 5G Connectivity and Intelligent Devices

The global rollout of 5G communication infrastructure is significantly accelerating the adoption of AI-enabled edge devices, which require advanced PCB architectures. According to a study, global 5G subscriptions surpassed 2.6 billion in 2025, enabling ultra-low-latency connectivity for edge AI applications. Devices such as smart cameras, industrial sensors, autonomous drones, and connected vehicles rely on sophisticated circuit boards that support high-speed data processing and communication. The expansion of smart cities and intelligent transportation systems requires large deployments of edge devices integrated with AI processors. These devices demand compact, lightweight, and high-performance PCBs, such as flexible circuits and HDI boards. As telecom operators continue to expand next-generation connectivity networks globally, manufacturers are increasing investments in advanced PCB fabrication technologies to meet rising demand from AI edge computing systems.

Expansion of Edge AI and IoT Devices Across Consumer and Industrial Applications

The rapid proliferation of edge-based artificial intelligence devices is a major factor in the development of advanced printed circuit boards capable of handling high computational workloads locally. According to a study, more than 50% of AI data processing is expected to occur at the edge by 2026, reflecting a shift away from centralized cloud architectures. Edge AI devices require high-density PCB architectures to integrate processors, sensors, and memory modules within compact form factors. As industries deploy intelligent devices for real-time decision-making, PCB designs must support higher signal integrity, improved thermal management, and multilayer configurations.

Restrain - High Fabrication Complexity and Capital-Intensive Manufacturing

AI edge devices increasingly require HDI, any-layer, and very high-layer-count PCBs, which substantially raise fabrication complexity, yield risk, and capital requirements for manufacturers. Processes such as laser microvia drilling, via-in-pad plating, fine-line patterning below 3/3 mil, and advanced surface finishes require expensive equipment and tight process control, which many small and mid-size PCB fabs struggle to adopt at scale. This cost and capability barrier constrains capacity additions and leads to supply bottlenecks in advanced HDI boards used in AI servers, telecom edge nodes, and high-end automotive ECUs, thereby tempering the pace at which AI edge PCB supply matches surging demand.

Thermal Management and Reliability Challenges in High-Power Edge Systems

AI accelerators and high-speed networking components generate substantial heat in small enclosures, and failure to manage these loads through appropriate stack-ups, copper thickness, and vias degrades reliability and shortens product lifecycles. Designers must also address signal integrity at multi-gigabit data rates across dense interconnects, which complicates layout and potentially increases re-spins and time-to-market. These engineering and reliability challenges slow the deployment of next-generation AI edge hardware, particularly in safety-critical sectors such as healthcare and industrial automation, where qualification cycles are stringent.

Opportunity - Rising Adoption of AI-Powered Smart Surveillance Systems

Governments and municipalities worldwide are increasingly investing in intelligent surveillance infrastructure to enhance public safety and urban monitoring capabilities. According to United Nations urbanization statistics, nearly 68% of the global population is projected to live in urban areas by 2050, driving expansion of smart city infrastructure. AI-powered cameras deployed across transportation networks, airports, and public spaces rely on embedded processors capable of performing real-time video analytics. These systems require high-performance PCBs to integrate imaging sensors, edge AI processors, and communication modules. As smart surveillance systems become more advanced, demand for HDI and flexible PCB architectures capable of supporting edge computing workloads is expected to increase significantly.

Growing Demand from Autonomous Vehicles and Intelligent Automotive Systems

Modern vehicles increasingly incorporate AI-driven systems such as advanced driver assistance systems (ADAS), autonomous driving modules, and intelligent infotainment systems. According to the International Energy Agency (IEA), global sales of electric vehicles are expected to exceed 20 million units in 2025, accelerating integration of advanced electronics across automotive platforms. AI-enabled systems within vehicles require compact, high-density PCBs capable of supporting high-speed computing and sensor fusion operations. As automotive manufacturers expand into investments in autonomous mobility technologies, PCB suppliers are developing advanced designs capable of operating in high-temperature and vibration-prone environments.

Category-wise Analysis

Product Insights

Multi-layer PCB capturing more than 35% share in 2026 with a value exceeding US$ 5.4 Bn, due to these devices requiring compact hardware capable of handling high computing loads and fast data transfer. Multiple conductive layers allow designers to integrate high-density AI chips, memory, and sensors within a small board, which is essential for compact edge devices. They also provide better signal integrity and reduced electromagnetic interference, ensuring reliable processing of high-speed AI workloads and real-time data communication.

The package substrates demonstrate a significant growth rate as edge AI processors require high-density interconnections and advanced chip packaging to support faster data processing. As edge devices integrate AI accelerators, GPUs, and high-performance memory, package substrates enable efficient signal routing and reduced latency between chips. They also support miniaturization and higher I/O density. Increasing demand for system-in-package (SiP) and heterogeneous integration in edge computing is accelerating the need for advanced package substrate technologies.

Application Insights

Consumer electronics hold over 40% market share in 2026, with a value exceeding US$ 6.2 Bn, as modern devices increasingly require on-device intelligence for faster and more private data processing. Products such as smartphones, smart cameras, wearables, and home assistants integrate AI chips that need compact, high-density PCBs capable of supporting multiple sensors, processors, and connectivity modules. These devices also demand low power consumption and high processing efficiency. The high global production volume and rapid product upgrade cycles in consumer electronics significantly increase the demand for AI-optimized PCBs.

Automotive is expected to grow at the highest rate due to the increasing integration of AI-enabled driver assistance, autonomous driving systems, and in-vehicle computing platforms. Modern vehicles require high-performance PCBs to support real-time data processing from cameras, LiDAR, radar, and sensors directly at the edge. The shift toward electric vehicles and connected car ecosystems demands compact, high-reliability PCB architectures for onboard AI modules.

Regional Insights

North America AI Edge Devices PCB Market Trends

North America is expected to grow at a significant rate, led by the U.S., and represents a pivotal hub for AI edge hardware innovation, underpinned by strong semiconductor, cloud, and networking ecosystems that create sustained demand for advanced PCBs. U.S. technology companies are at the forefront of edge AI chip and hardware development, and investments in industrial IoT, autonomous mobility pilots, and defense-grade edge systems are catalyzing the adoption of high-reliability HDI. Federal initiatives supporting domestic semiconductor manufacturing and secure critical infrastructure further encourage localized sourcing of high-end PCBs for AI edge devices. Telecom operators in the U.S. are deploying AI-enhanced 5G and edge computing platforms for low-latency applications in gaming, AR/VR, and enterprise services, requiring high-performance RF and backplane PCBs in distributed data centers.

Asia Pacific AI Edge Devices PCB Market Trends

Asia Pacific holds over 57% share in 2026, reaching US$ 9 Bn value. China’s significant investments in edge AI infrastructure, AI servers, and 5G networks drive surging demand, particularly for data centers and telecom edge equipment. India and ASEAN economies are expanding their electronics manufacturing capabilities under incentives for mobile devices, telecom equipment, and automotive components, opening new opportunities for localized AI edge PCB production. Asia Pacific is projected to capture more than 40% of global edge AI hardware revenue over the coming years, reflecting both domestic consumption and export-oriented manufacturing. Regional strengths in cost-effective, high-volume PCB fabrication, combined with government support for semiconductor and electronics ecosystems, position Asia Pacific as the key growth engine for AI edge devices PCBs.

Europe AI Edge Devices PCB Market Trends

Europe is expected to hold more than 20% share by 2026, supported by strong automotive, industrial machinery, and telecom sectors, with Germany, the U.K., and France acting as primary demand centers for advanced PCB technologies. German OEMs are accelerating deployment of AI-enabled ADAS and EV platforms, increasing the content of HDI and rigid-flex PCBs in vehicles for sensor fusion, power electronics, and digital cockpits. Initiatives in smart manufacturing and Industry 4.0 under programs such as national industrial strategies are driving the adoption of AI-enabled robotics and predictive maintenance, adding to demand for industrial-grade PCBs. Harmonization of technical standards and environmental regulations, including RoHS and upcoming sustainability reporting rules, further shape sourcing and design choices for AI edge PCBs in the region.

Competitive Landscape

The AI Edge Devices PCB market is moderately consolidated, with several large global manufacturers dominating advanced PCB production. Leading companies compete based on technological capabilities, production scale, and specialization in high-density interconnect and semiconductor substrate technologies. Firms are investing heavily in research and development to support next-generation computing platforms, including AI processors, autonomous systems, and high-speed communication modules. Manufacturers are expanding production facilities in Asia and North America to strengthen supply chain resilience and reduce dependence on single-region manufacturing hubs.

Key Industry Developments

- In September 2025, Zhen Ding Technology Holding Co., Ltd. showcased its latest AI-focused PCB and semiconductor substrate technologies at SEMICON Taiwan 2025, highlighting advanced solutions such as 28-layer high-end substrates, 138×138 mm large substrates, and HLC+HDI boards designed for AI servers and high-performance computing.

Companies Covered in AI Edge Devices PCB Market

- Zhen Ding Technology Group

- Unimicron Technology Corporation

- Nippon Mektron

- TTM Technologies

- Compeq Manufacturing

- Nan Ya PCB

- AT&S

- Samsung Electro-Mechanics

- Ibiden Co., Ltd.

- Tripod Technology

- Shennan Circuits

- Others

Frequently Asked Questions

The global AI Edge Devices PCB market is projected to be valued at US$15.4 Bn in 2026.

The growing need for real-time data processing and low-latency computing drives the market growth.

The AI edge devices PCB market is expected to witness a CAGR of 23.5% from 2026 to 2033.

The growing adoption of AI-enabled IoT devices is creating strong demand for HDI and advanced package substrate PCBs to support faster processing and miniaturized designs, which is creating strong growth opportunities.

Zhen Ding Technology Group, Unimicron Technology Corporation, Nippon Mektron, TTM Technologies, Compeq Manufacturing, Nan Ya PCB are among the leading key players.