- Specialty & Fine Chemicals

- Aerospace Foam Market

Aerospace Foam Market Size, Share, and Growth Forecast, 2026 - 2033

Aerospace Foam Market by Foam Type (Polyurethane Foam, Metal Foam, Others), Application (Aircraft Seating, Insulation, Others), Aircraft Type, and Regional Analysis for 2026 - 2033

Aerospace Foam Market Size and Trends Analysis

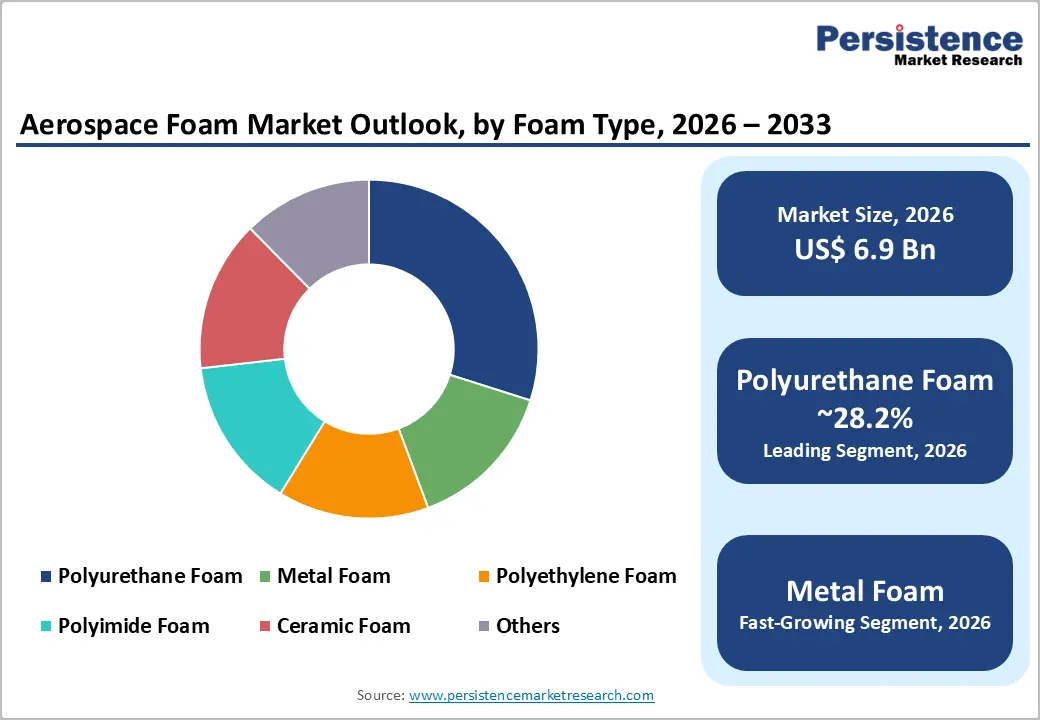

The global aerospace foam market size is likely to be valued at US$6.9 billion in 2026 and is expected to reach US$10.4 billion by 2033, growing at a CAGR of 6.1% between 2026 and 2033, driven by increasing aircraft production, expansion of the global fleet, and stringent cabin safety and lightweighting requirements.

Rising passenger traffic and cargo demand are reinforcing OEM production cycles and aftermarket replacement demand, positioning aerospace foams as a critical material in seating, insulation, sealing, and acoustic systems.

Key Industry Highlights:

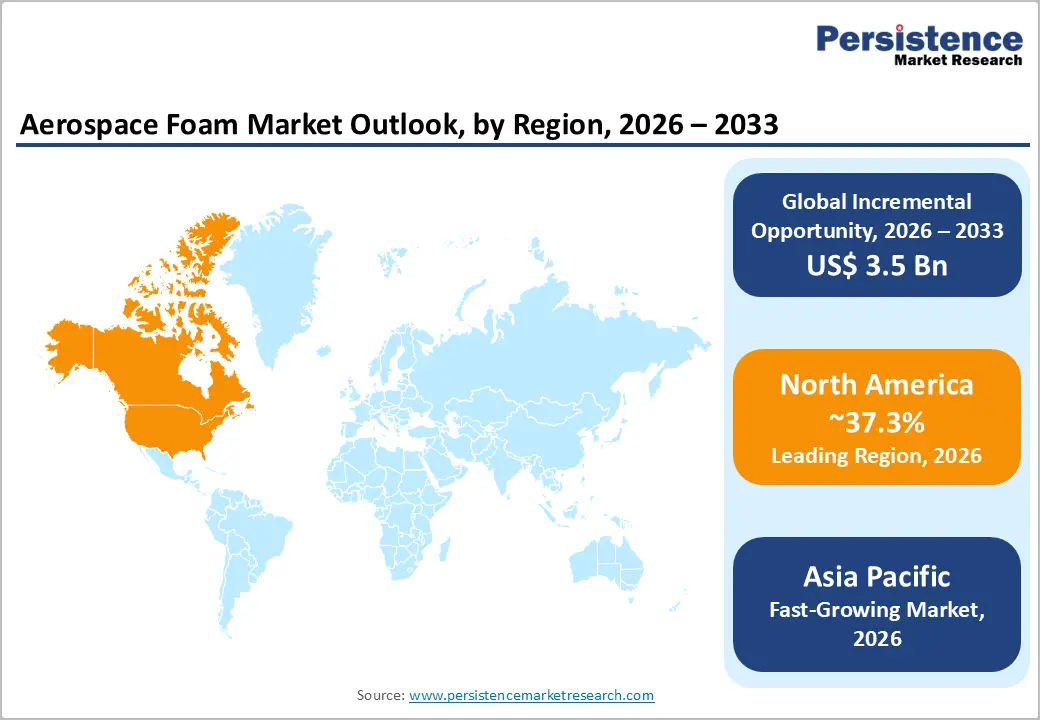

- Leading Region: North America is projected to account for approximately 37.3% of the market share, driven by strong OEM production, a large commercial fleet, and a well-established MRO ecosystem.

- Fastest-growing Region: Asia Pacific is the fastest-growing region, supported by rising air passenger traffic and increasing aircraft deliveries.

- Investment Plans: Major industry participants are focusing on investments in lightweight and sustainable foam technologies, along with regional manufacturing expansion, particularly in Asia Pacific, where localization strategies are accelerating to capture high-growth demand.

- Dominant Foam Type: Polyurethane foam is anticipated to hold approximately 28.2% of the market share, due to its versatility, cost-efficiency, and widespread use in aircraft interiors.

- Leading Application: Aircraft seating is estimated to hold 34.5% of market share due to high installation volumes and frequent replacement cycles across commercial aircraft fleets.

| Key Insights | Details |

|---|---|

| Aerospace Foam Market Size (2026E) | US$6.9 Bn |

| Market Value Forecast (2033F) | US$10.4 Bn |

| Projected Growth (CAGR 2026 to 2033) | 6.1% |

| Historical Market Growth (CAGR 2020 to 2025) | 2.1% |

Market Factors - Driver, Restraint, and Opportunity Analysis

Driver Analysis - Fleet Expansion and Air Traffic Growth

Sustained growth in the global aircraft fleet and passenger traffic is directly increasing demand for aerospace foam materials. Commercial aviation has witnessed consistent long-term expansion, with passenger traffic increasing multiple-fold over the past two decades. Aircraft deliveries continue to rise to meet both replacement and new demand, particularly in emerging markets across Asia Pacific and the Middle East. This expansion drives foam consumption across both OEM and aftermarket channels. Each new aircraft requires significant volumes of foam for seating, insulation, acoustic panels, and sealing systems. A growing installed fleet increases demand for maintenance, repair, and overhaul (MRO), where foam components are frequently replaced due to wear, compliance updates, and cabin retrofits. The combined effect creates a stable and recurring demand base, strengthening long-term market visibility.

Stringent Safety and Flammability Regulations

Regulatory requirements governing fire safety, smoke emission, and toxicity are reinforcing the adoption of certified aerospace-grade foams. Aviation authorities impose strict standards on materials used in aircraft interiors, particularly for seating, insulation, and cabin structures. Foam materials must meet rigorous criteria for flame resistance, heat release, and smoke density. These regulatory requirements elevate the importance of high-performance foams that are specifically engineered for aviation use. Suppliers with certified materials and established testing capabilities benefit from strong entry barriers and long-term contracts with OEMs and Tier 1 suppliers. Compliance-driven replacement cycles also support aftermarket demand, as older materials are upgraded to meet evolving standards. This regulatory environment strengthens pricing stability and limits substitution by lower-cost alternatives.

Growth in Defense and Military Aviation

Rising global defense expenditure and military fleet modernization programs are expanding the application scope of aerospace foams. Governments are increasing investments in advanced fighter jets, transport aircraft, and unmanned systems to enhance defense capabilities. These platforms require high-performance materials capable of withstanding extreme conditions, including temperature fluctuations, vibration, and mechanical stress. Aerospace foams are increasingly used in military applications such as insulation, acoustic dampening, impact protection, and structural components. Compared to commercial aviation, military applications demand higher performance specifications, creating opportunities for premium-priced materials. This segment is expected to grow faster than commercial aviation in value terms, contributing to overall market expansion and diversification.

Restraint Analysis - High Certification and Qualification Costs

Extensive testing and certification requirements significantly increase product development timelines and costs. Aerospace foam materials must undergo rigorous evaluation for flammability, toxicity, durability, and mechanical performance before approval for use in aircraft. This process can take several years and requires substantial investment in testing infrastructure and compliance documentation. These high barriers to entry limit participation to established players with strong technical capabilities. Smaller manufacturers face challenges in scaling operations due to the cost and complexity of certification. The result is slower innovation cycles and delayed commercialization of new materials, even when performance advantages are evident.

Supply Chain Constraints and Raw Material Volatility

Dependence on specialized raw materials and complex supply chains creates vulnerability to disruptions. Aerospace foams rely on petrochemical derivatives, specialty additives, and precision manufacturing processes. Fluctuations in raw material prices and availability can directly impact production costs and margins. Supply chain disruptions can delay aircraft manufacturing schedules, affecting both OEM demand and aftermarket supply. These challenges also increase inventory costs and create pricing pressure when suppliers are unable to pass on cost increases to customers immediately. The combination of supply uncertainty and cost volatility remains a persistent challenge for market participants.

Opportunity Analysis - Sustainable and Lightweight Material Innovation

Growing emphasis on sustainability and fuel efficiency is driving demand for advanced lightweight and recyclable foam materials. Airlines and aircraft manufacturers are prioritizing weight reduction to improve fuel efficiency and reduce carbon emissions. This has increased interest in high-performance foams that offer superior strength-to-weight ratios. Innovations in recycled-content foams and low-density materials are gaining traction, particularly in seating and interior applications. Manufacturers that can combine sustainability with regulatory compliance and performance reliability are well-positioned to capture premium market segments. This trend is expected to accelerate as environmental regulations and corporate sustainability goals become more stringent.

Expansion in Asia Pacific Aerospace Ecosystem

Rapid aviation growth in Asia Pacific is creating opportunities for localized production and supply chain integration. Countries such as China, India, and Southeast Asian nations are investing heavily in aviation infrastructure, aircraft manufacturing, and MRO facilities. This regional expansion is increasing demand for aerospace materials, including foams. Localization strategies, including regional manufacturing facilities and partnerships with local OEMs and suppliers, can reduce lead times and improve cost efficiency. The growing presence of aircraft assembly lines and maintenance hubs in the region further enhances demand for foam materials. Asia Pacific represents a significant growth opportunity for both global and regional players.

Category-wise Analysis

Foam Type Insights

Polyurethane foam is anticipated to remain the leading segment, accounting for approximately 28.2% of the market share over the forecast period. Its dominance is driven by its versatility, cost-efficiency, and well-balanced mechanical properties, including flexibility, resilience, and long-term durability under varying cabin conditions. Polyurethane foams are extensively utilized in aircraft seating systems, sidewall panels, insulation layers, and overhead storage compartments due to their ability to meet stringent flammability and smoke emission standards. For instance, rigid polyurethane foams are commonly integrated into thermal insulation panels, while flexible variants are used in seat cushioning to enhance passenger comfort. Their well-established global supply chain, ease of customization, and compatibility with multiple aircraft interior designs further reinforce their position as the preferred material for high-volume aerospace applications.

Metal foam is anticipated to be the fastest-growing segment, driven by increasing adoption in structural and high-performance aerospace applications. These materials offer exceptional strength-to-weight ratios, high energy absorption capacity, and superior thermal and vibration damping characteristics, making them suitable for next-generation aircraft designs. Metal foams are increasingly being explored in applications such as impact-resistant panels, engine components, and structural reinforcements where weight reduction without compromising strength is critical. For example, aluminum foam is being evaluated for use in aircraft flooring and protective barriers due to its lightweight yet robust nature. Although currently representing a smaller share in terms of overall volume, ongoing advancements in material engineering and manufacturing processes are expected to accelerate adoption, particularly in defense and advanced commercial aircraft platforms.

Application Insights

Aircraft seating is anticipated to account for 34.5% of market share in 2026, supported by its high volume demand and recurring replacement cycles. Each commercial aircraft is equipped with a large number of seats, all of which require foam-based cushioning and structural support materials. These components are frequently upgraded or replaced to enhance passenger comfort, reduce overall aircraft weight, and comply with evolving safety and fire-resistance regulations. For example, premium economy and business-class seating configurations increasingly utilize advanced foam materials that provide improved ergonomics and durability while minimizing weight. The continuous introduction of lightweight seating designs by airlines further reinforces demand for high-performance foams, making this segment a consistent revenue contributor.

Insulation is anticipated to be the fastest-growing application segment, driven by rising demand for thermal efficiency, acoustic performance, and fuel optimization. Aerospace foams play a critical role in maintaining cabin temperature stability and reducing noise levels, which directly impacts passenger experience and operational efficiency. Advanced foam-based insulation systems are widely used in fuselage walls, ceilings, and flooring to enhance thermal management and soundproofing. For instance, lightweight foam insulation materials are increasingly adopted in long-haul aircraft to improve energy efficiency and reduce fuel consumption. Growth in this segment is also supported by retrofit programs, where aging aircraft are upgraded with modern insulation technologies to meet current performance and regulatory standards.

Regional Insights

North America Aerospace Foam Market Trends - OEM-Driven Demand & MRO-Led Replacement Cycle in the U.S.

North America is projected to lead the market, accounting for 37.3% of the market share, with the U.S. serving as the primary growth engine. The region benefits from a highly integrated aerospace manufacturing ecosystem supported by major OEMs such as Boeing and a dense network of Tier 1 suppliers. Strong demand is generated across both new aircraft production and aftermarket services, particularly in maintenance, repair, and overhaul (MRO), where foam components in seating, insulation, and sealing systems are frequently replaced. The presence of large airline fleets and continuous cabin refurbishment programs further sustains consistent material demand.

Regulatory frameworks governed by agencies such as the Federal Aviation Administration play a critical role in shaping market dynamics. Strict flammability and safety compliance standards ensure continuous demand for certified aerospace foams and create high entry barriers for new suppliers. Innovation is a defining characteristic of the region, with companies like Rogers Corporation and UFP Technologies investing in high-performance, lightweight, and flame-retardant materials. In recent developments, suppliers have expanded capabilities in engineered foam components for electric aircraft and advanced air mobility platforms, reinforcing the region’s position as a hub for next-generation aerospace material innovation. Continuous retrofit programs by North American airlines to enhance passenger experience and reduce fuel consumption further support steady market growth.

Europe Aerospace Foam Market Trends - Regulation-Backed Innovation & Sustainable Materials Leadership in Europe

Europe represents a mature yet innovation-driven aerospace foam market, with key countries including Germany, the U.K., France, and Spain playing central roles in aerospace manufacturing and materials development. The region’s aerospace ecosystem is anchored by major OEMs such as Airbus, which drives demand for advanced interior materials, including high-performance foams. Europe’s strong regulatory framework, enforced by the European Union Aviation Safety Agency, ensures strict adherence to safety, fire resistance, and environmental standards.

Material innovation remains a key focus, with companies such as BASF, Covestro, and Evonik Industries investing in advanced polymers, lightweight foams, and sustainable material solutions. A notable development includes Zotefoams expanding its European manufacturing footprint through the acquisition of facilities in Spain in 2025, strengthening regional supply chain resilience and production capacity. Strategic investments and cross-border collaborations are enhancing innovation pipelines and enabling faster commercialization of new materials. While growth rates are comparatively moderate, Europe continues to be a high-value market characterized by premium product demand, strong engineering expertise, and leadership in sustainable aerospace materials.

Asia Pacific Aerospace Foam Market Trends - Rapid Fleet Expansion & Localization-Driven Growth in Asia Pacific

Asia Pacific is the fastest-growing region in the aerospace foam market, driven by rapid expansion in air travel and increasing aircraft deliveries. Major economies such as China, India, Japan, and Southeast Asian nations are experiencing significant growth in aviation demand, supported by rising middle-class populations and increasing disposable incomes. This surge in passenger traffic is translating into higher aircraft procurement and fleet expansion, directly boosting demand for aerospace materials, including foams.

The region is also emerging as a key manufacturing and assembly hub. For instance, COMAC is advancing domestic aircraft production programs, increasing local demand for certified materials. Similarly, Hindustan Aeronautics Limited continues to expand its defense and aerospace manufacturing capabilities, contributing to regional material consumption. Global OEMs such as Airbus have also expanded assembly and engineering operations in Asia, strengthening localization trends. Investments in MRO infrastructure across countries such as Singapore and India are further driving aftermarket demand for foam components used in insulation and seating systems.

Government initiatives aimed at strengthening domestic aerospace industries, along with cost advantages in manufacturing, are accelerating supply chain localization. The integration of regional suppliers into global aerospace value chains is increasing demand for high-quality, certified foam materials. These factors collectively position Asia Pacific as a critical growth engine, with strong long-term potential supported by both volume expansion and industrial development.

Competitive Landscape

The global aerospace foam market is moderately fragmented, with a mix of global material manufacturers and specialized regional suppliers. Leading players hold significant market influence due to their technical expertise, certification capabilities, and long-standing relationships with OEMs and Tier 1 suppliers. High entry barriers, driven by stringent regulatory requirements and qualification processes, limit new entrants and maintain competitive stability.

Market leaders are focusing on innovation, regulatory compliance, and regional expansion. Key strategies include developing lightweight and sustainable materials, strengthening certification capabilities, and establishing localized production facilities to improve supply chain efficiency and responsiveness.

Key Industry Developments:

- In April 2025, Zotefoams plc unveiled Ecozote PE/R LD24 FR, a closed-cell, flame-retardant foam with 30% post-consumer recycled content at the Aircraft Interiors Expo, aiming to support sustainability goals while maintaining compliance with stringent aerospace safety standards.

- In November 2025, Zotefoams plc announced the acquisition of Overseas Konstellation Company S.A. (OKC) in Spain, strengthening its manufacturing footprint in Europe and enhancing its product portfolio for high-performance technical foams.

Companies Covered in Aerospace Foam Market

- Zotefoams plc

- Rogers Corporation

- Evonik Industries AG

- BASF SE

- DuPont de Nemours, Inc.

- Solvay S.A.

- Covestro AG

- SABIC

- Armacell International S.A.

- UFP Technologies, Inc.

- Boyd Corporation

- General Plastics Manufacturing Company

- Recticel NV

- Nitto Denko Corporation

- Sekisui Chemical Co., Ltd.

- Trelleborg AB

Frequently Asked Questions

The aerospace foam market is estimated to be valued at US$6.9 billion in 2026.

The aerospace foam market is projected to reach US$10.4 billion by 2033.

Key trends include increasing adoption of lightweight and fuel-efficient materials, rising focus on sustainable and recyclable foam solutions, growing demand from aircraft cabin modernization programs, and advancements in high-performance foams for insulation and structural applications.

Polyurethane foam is the leading segment, accounting for approximately 28.2% of the market share, driven by its versatility and widespread use in aircraft interiors.

The aerospace foam market is expected to grow at a CAGR of 6.1% from 2026 to 2033.

Major players include Zotefoams plc, Rogers Corporation, Evonik Industries AG, BASF SE, and DuPont de Nemours, Inc.