- Aerospace & Defense

- Aero Engine Fan Blade Market

Aero Engine Fan Blade Market Size, Share, and Growth Forecast, 2026 – 2033

Aero Engine Fan Blade Market by Material Type (Titanium Alloys, Composites, Aluminum Alloys), Aircraft Type (Narrow-Body, Wide-Body, Regional), Application (Commercial, Military, General Aviation), and Regional Analysis 2026 – 2033

Aero Engine Fan Blade Market Size and Trends Analysis

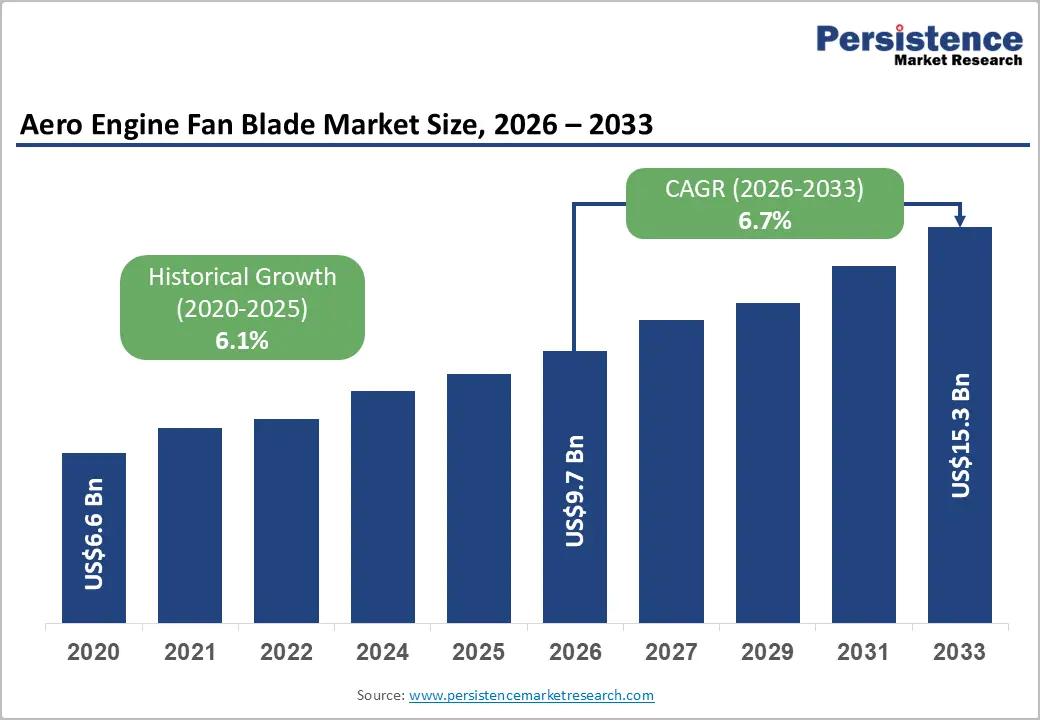

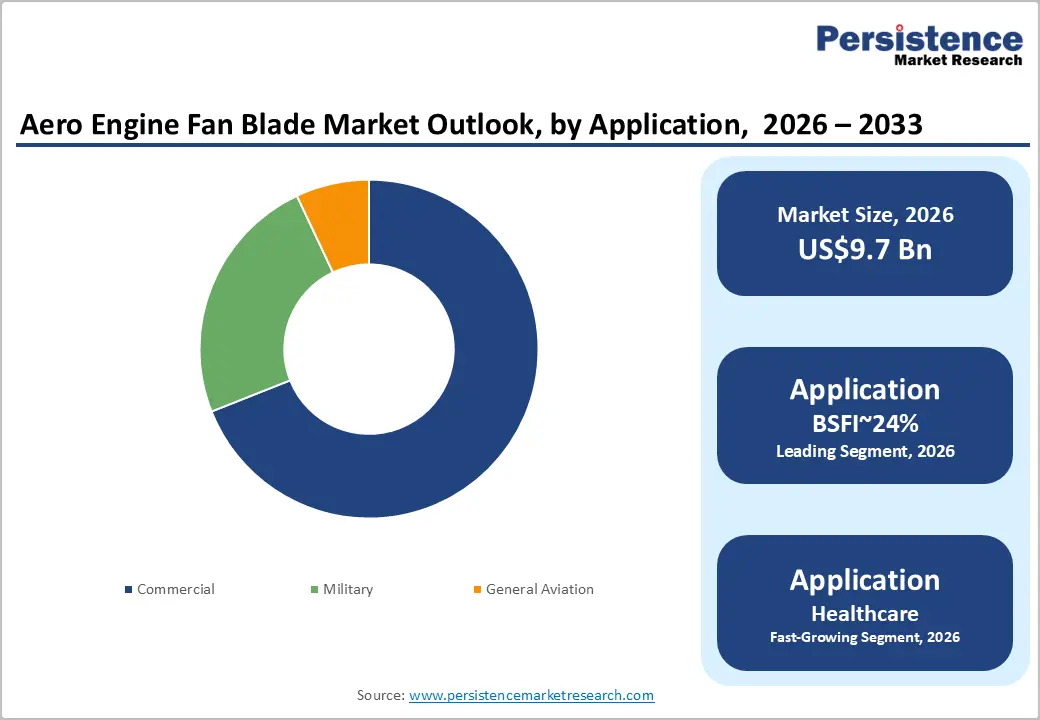

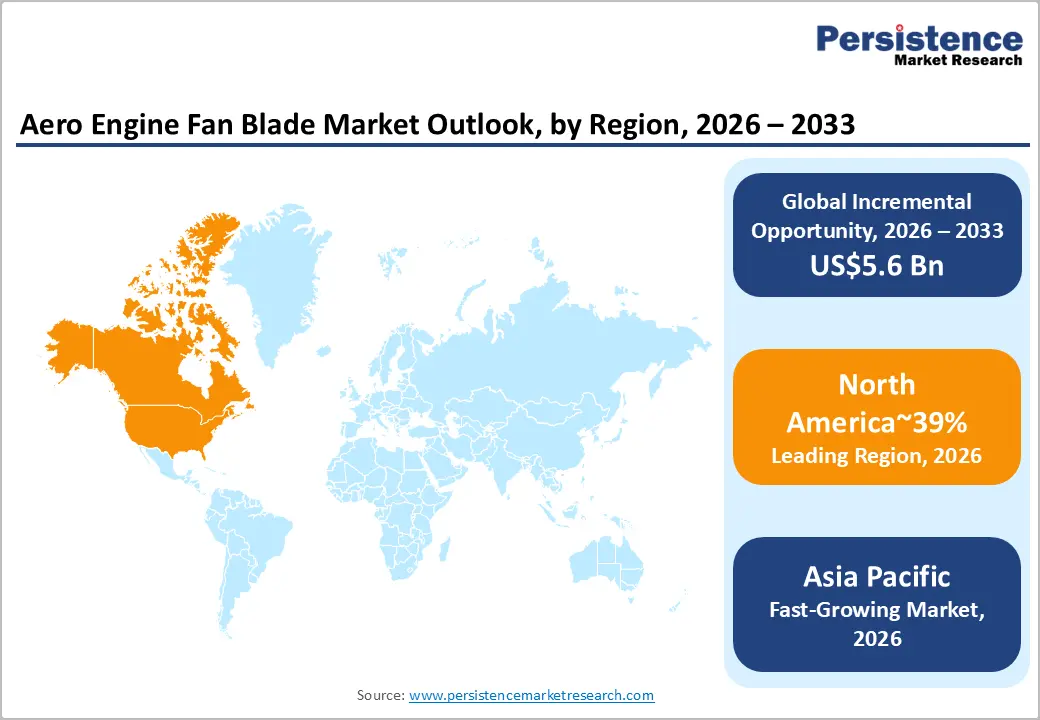

The global aero engine fan blade market size is likely to be valued at US$9.7 billion in 2026 and is expected to reach US$15.3 billion by 2033, growing at a CAGR of 6.7% during the forecast period from 2026 to 2033, driven by the rise in air travel demand, which fuels fleet expansion and engine replacements.

The market is scaling rapidly due to the urgent aviation industry shift toward high-bypass ratio engines that maximize fuel efficiency and minimize carbon footprints. Major aerospace OEMs are transitioning to advanced composite materials to reduce engine weight. Military modernization programs further boost demand amid global defense spending increases.

Key Industry Highlights:

- Leading Region: North America is expected to dominate, holding a projected share of around 36% in 2026, driven by a concentration of advanced aerospace manufacturing, increased adoption of composite blades, and vertically integrated propulsion ecosystems.

- Fastest-growing Region: Asia Pacific is anticipated to grow the fastest due to accelerating aircraft fleet expansion, sovereign aerospace industrialization strategies, and cross-sector propulsion adoption.

- Leading Material Type: Titanium alloys are expected to lead accounting with approximately 47% share in 2026, driven by established industrial adoption, high production throughput, structural durability, and deployment across high-bypass turbofan architectures in commercial and military platforms.

- Leading Application: Commercial aviation is projected to dominate due to fleet scale, lifecycle replacement intensity, and suitability across passenger transport use cases, with approximately 69% share in 2026.

| Key Insights | Details |

|---|---|

| Aero Engine Fan Blade Market Size (2026E) | US$9.7 Bn |

| Market Value Forecast (2033F) | US$15.3 Bn |

| Projected Growth (CAGR 2026 to 2033) | 6.7% |

| Historical Market Growth (CAGR 2020 to 2025) | 6.1% |

Market Factors – Growth, Barriers, and Opportunity Analysis

Growth Analysis – Regulatory Decarbonization Mandates Reshaping Fan Blade Engineering

Stringent global aviation emission frameworks are structurally reshaping aero engine design priorities. Decarbonization mandates are accelerating the integration of advanced high bypass propulsion architectures. Regulatory bodies such as the Federal Aviation Administration and European Union Aviation Safety Agency are tightening certification benchmarks. Multilateral commitments under the International Civil Aviation Organization reinforce long-term carbon neutrality pathways. These compliance thresholds elevate performance expectations across propulsion subsystems and materials. Fan blade aerodynamics increasingly determine fuel burn efficiency and lifecycle emissions intensity. Engine platforms, therefore, prioritize lightweight composite structures with enhanced fatigue tolerance. This regulatory convergence embeds structural demand for technologically differentiated blade configurations.

Larger diameter fan systems enable higher bypass ratios and improved propulsive efficiency. Advanced composite fan blades support weight reduction while sustaining structural integrity. Programs such as CFM International technology demonstrators signal an architectural transition toward open fan configurations. This evolution reconfigures supplier requirements across materials processing and precision manufacturing. Certification compliance intensifies testing protocols across stress, impact, and durability thresholds. Capital allocation increasingly shifts toward automation and composite fabrication capabilities. Airline fleet modernization cycles internalize emissions compliance within procurement strategies. These dynamics elevate value concentration within high-performance fan blade segments.

Defense Aviation Modernization Driving Structural Demand for Advanced Fan Blades

Comprehensive military aviation modernization is structurally elevating demand for advanced fan blades. Next-generation fighter platforms and unmanned systems require higher thrust density engines. These propulsion systems operate under extreme thermal and mechanical stress conditions. Fan blades must therefore deliver superior fatigue resistance and structural stability. Engine retrofits increasingly replace legacy components with lightweight composite architectures. Life extension programs prioritize efficiency gains and reduced lifecycle maintenance burdens. This upgrade cycle sustains aftermarket demand alongside new platform production. Rising geopolitical tensions reinforce stable procurement pipelines across defense propulsion ecosystems.

Elevated defense allocations secure long-duration engine development and sustainment contracts. Propulsion modernization emphasizes additive manufacturing and advanced ceramic composite integration. These technologies enhance stealth performance and high-speed operational capabilities. Manufacturing complexity increases certification intensity and precision quality assurance requirements. Localization initiatives are expanding domestic propulsion manufacturing capabilities across emerging markets. Strategic co-production frameworks reconfigure global supply chain dependencies. Value creation increasingly concentrates on high specification materials processing and integration. These forces embed durable institutional demand across military fan blade supply chains.

Barrier Analysis – Capital Intensity and Manufacturing Complexity Constraining Market Scalability

The structural intricacy of advanced fan blades embeds significant capital intensity across production ecosystems. Manufacturing requires specialized multi-axis machining systems and composite processing infrastructure. Autoclave curing environments and contamination-controlled facilities elevate fixed cost burdens. Precision tooling and nondestructive inspection technologies further expand upfront investment requirements. Certification pathways under global aviation regulators impose extended validation cycles. These compliance obligations lengthen commercialization timelines and defer revenue realization. Research and development expenditure rises alongside aerodynamic and materials innovation complexity. Such cumulative financial thresholds restrict rapid scaling across emerging manufacturing entrants.

High entry barriers consolidate production within established tier one propulsion suppliers. Limited supplier diversity reduces flexibility during cyclical fleet expansion phases. Sudden order surges strain capacity due to constrained certified manufacturing throughput. Cost recovery models, therefore, prioritize long-term contractual stability over volume agility. Margin structures reflect the heavy depreciation of capital-intensive composite fabrication assets. Smaller firms face disproportionate financing risk within safety-critical certification regimes. Supply chain concentration increases exposure to bottlenecks in specialty materials sourcing. The following structural costs temper competitive intensity across the fan blade market.

Manufacturing Sophistication and Process Complexity Limiting Production Efficiency

Modern aero engine fan blades represent highly intricate structural assemblies. Integrated blade disc architectures demand extreme dimensional precision and balance control. Composite fabrication through resin transfer molding requires tightly controlled process parameters. These manufacturing pathways depend on specialized multi-axis machining centers. Highly skilled technicians are essential for composite layup and curing oversight. Titanium alloys exhibit high strength and low machinability characteristics. Rapid tool degradation increases downtime and raises consumable expenditure. Such process intensity constrains throughput scalability across production facilities.

Advanced inspection protocols further elevate manufacturing cycle duration. Nondestructive testing and microstructural validation ensure airworthiness compliance. Process deviations can compromise fatigue life and aerodynamic performance stability. Rework rates carry significant cost implications within safety-critical environments. Capital allocation must support automation and precision metrology integration. Workforce training investments remain substantial due to technical skill scarcity. These operational constraints elevate fixed cost absorption across manufacturing units. Collectively, technical complexity embeds structural inefficiencies within blade production economics.

Opportunity Analysis – Sustainable Propulsion Convergence Expanding Strategic Value Capture

The convergence of open fan, hybrid electric, and alternative fuel systems expands intellectual property intensity. Early certification of advanced blade architectures establishes durable technological benchmarks across propulsion platforms. Programs such as CFM International demonstrators illustrate next-generation open fan integration. Certified high-performance blade configurations command structural pricing differentiation within engine contracts. Long-duration service agreements embed recurring replacement demand over multi-decade lifecycles. This strengthens control over proprietary spare parts and performance upgrade pathways. Intellectual property ownership, therefore, concentrates margin capture within leading propulsion integrators. Such positioning reinforces strategic insulation from commoditized component competition.

Advanced composite materials redefine maintenance, repair, and overhaul service requirements. Manufacturers, including Safran and GE Aerospace, are expanding integrated service ecosystems. Digital twin deployment supports predictive maintenance across converged propulsion architectures. Service models such as Rolls-Royce Holdings’ long-term care programs illustrate lifecycle monetization frameworks. Sustainable blade technologies also improve eligibility for environmentally aligned financing instruments. Green capital access strengthens balance sheet flexibility for research-intensive development cycles. Circular material recovery strategies reduce exposure to volatile specialty metal markets.

Additive Manufacturing and Digital Intelligence Transforming Lifecycle Value Capture

The integration of additive manufacturing is redefining blade design freedom and efficiency. Layered fabrication enables intricate internal cooling geometries previously unattainable through machining. Material deposition precision reduces waste and optimizes structural weight distribution. Complex hollow architectures enhance thermal resilience under elevated operating gradients. Process flexibility shortens prototyping cycles and accelerates aerodynamic iteration. These efficiencies recalibrate cost structures across high-performance blade production. Digital engineering platforms increasingly align manufacturing with data-driven validation workflows. Such convergence strengthens technological differentiation within propulsion supply chains.

AI-enabled digital twin systems expand predictive maintenance capabilities across blade lifecycles. Embedded sensors facilitate continuous monitoring of stress accumulation and microfracture propagation. Real-time diagnostics reduce unplanned removals and catastrophic in-service failures. Maintenance strategies shift from interval-based inspections toward condition-based optimization. This transition expands specialized aftermarket services for advanced component manufacturers. High-margin lifecycle contracts reinforce recurring revenue visibility across propulsion programs. Data integration enhances collaboration between OEMs and maintenance ecosystems. These changing aspects create durable competitive insulation within intelligent blade platforms.

Category–wise Analysis

Material Type Insights

Titanium alloys are expected to lead the aero engine fan blade market, accounting for approximately 47% share in 2026, supported by its superior strength-to-weight profile and thermal stability under sustained operating loads. The material remains the baseline standard for high-bypass turbofan architectures deployed across commercial and military fleets. Proven integration within propulsion platforms such as the LEAP engines developed by CFM International reinforces confidence in long-cycle durability and containment performance.

Established global forging ecosystems and multi-decade lifecycle validation sustain procurement continuity among OEMs and Tier suppliers. High resistance to fatigue and foreign object damage strengthens its suitability for safety-critical rotating assemblies. This combination of mature supply infrastructure and predictable performance economics sustains titanium alloys’ structural dominance.

Composites are expected to be the fastest-growing segment, driven by the industry’s shift toward lightweight propulsion architectures and fuel-efficiency optimization. Advanced carbon-fiber reinforced polymer blades reduce mass and enhance aerodynamic efficiency within next-generation engines. Adoption within platforms such as the LEAP-1A program demonstrates measurable emissions and fuel burn improvements. Scaling composite fabrication technologies and automated layup systems are lowering manufacturing friction over time.

Continued R&D investments by propulsion leaders, including GE Aerospace and Safran, are accelerating structural integration. As open-fan and hybrid propulsion concepts mature, composite blade penetration is positioned to expand across future engine platforms.

Application Insights

The commercial segment is estimated to dominate, accounting for approximately 69% share in 2026, anchored by the scale and utilization intensity of the global airline fleet. High aircraft deployment rates necessitate recurring replacement of life-limited rotating components across narrow-body and wide-body platforms. Sustained production backlogs at major airframers such as Airbus and Boeing reinforce long-term engine delivery visibility. MRO cycles generate predictable aftermarket demand for certified fan blade assemblies and containment systems.

Passenger traffic recovery and route expansion sustain fleet modernization initiatives across emerging and mature corridors. This installed base depth and lifecycle-driven replacement cadence structurally entrenches commercial aviation as the dominant application segment.

The military segment is expected to be the fastest-growing segment, propelled by defense fleet modernization and next-generation propulsion development programs. Advanced combat aircraft, including the Lockheed Martin F-35 platform and emerging air dominance initiatives, require higher thrust-to-weight performance envelopes. Engines supporting these systems operate under extreme thermal and mechanical gradients, elevating material and design specifications. Defense procurement cycles prioritize durability, mission readiness, and extended service life under high-stress conditions.

Escalating geopolitical tensions are reinforcing sustained propulsion investment across major military powers. These dynamics accelerate demand for technologically advanced fan blades within sovereign defense ecosystems.

Regional Insights

North America Aero Engine Fan Blade Market Trends

North America is expected to remain the leading regional market, accounting for approximately 36% of the global share in 2026, supported by deep aerospace manufacturing integration and platform-level engine dominance. The region is positioned to sustain structural leadership through concentrated OEM presence, advanced materials engineering capabilities, and alignment between defense procurement cycles and commercial aircraft production programs. Demand is anticipated to remain anchored in narrow-body and wide-body engine platforms, while sustained military aviation programs reinforce high-performance blade development.

Regulatory enforcement around emissions and fuel efficiency is expected to accelerate composite fan blade penetration, strengthening the shift toward lightweight architectures and ceramic matrix composite integration.

The U.S. is projected to function as the primary structural anchor of regional momentum, shaping procurement intensity, certification frameworks, and innovation direction. Federal aviation oversight is expected to continue influencing global compliance standards, positioning domestic manufacturers at the forefront of next-generation blade validation and environmental performance benchmarks. Defense modernization programs are anticipated to sustain funding flows into adaptive propulsion architectures and thermal-resistant material platforms, reinforcing long-term technology leadership.

Aftermarket expansion is expected to remain a stabilizing force, as the large installed aircraft base drives blade replacement cycles, repair demand, and predictive maintenance adoption.

Asia Pacific Aero Engine Fan Blade Market Trends

Asia Pacific is expected to register the fastest-growing trajectory, as commercial fleet expansion and localized aerospace manufacturing accelerate across major economies. The region is positioned to outpace global averages due to sustained narrow-body aircraft demand, expanding low-cost carrier penetration, and rapid air passenger traffic growth. Large-scale aircraft procurement programs are anticipated to reinforce original equipment demand for advanced composite and titanium fan blades.

Governments are expected to intensify indigenous engine development strategies, strengthening domestic supply chains and reducing reliance on imported propulsion systems. Joint venture structures are anticipated to remain central to technology transfer, composite manufacturing scale-up, and precision machining capability expansion. Expanding maintenance, repair, and overhaul infrastructure is expected to further anchor aftermarket demand as regional fleet utilization rates remain elevated.

China is projected to function as the principal structural anchor, shaping production scale, certification momentum, and upstream material localization. National aerospace programs are expected to drive consistent engine platform upgrades and blade performance optimization across domestic aircraft platforms. Industrial policy support is likely to accelerate composite fabrication capacity and automated blade finishing systems within state-backed manufacturing clusters.

Vendor strategies are anticipated to prioritize local assembly integration, supply chain resilience, and lifecycle servicing depth to secure long-term airline contracts. This manufacturing-driven acceleration is expected to position Asia Pacific as the primary global growth engine in aero engine fan blade production and industrial scaling.

Europe Aero Engine Fan Blade Market Trends

Europe is expected to remain a structurally stable market, supported by its integrated aerospace manufacturing base and coordinated regulatory framework. The region is positioned to sustain high-value production through Airbus-led aircraft output and concentrated engine manufacturing clusters across Western Europe. Demand is anticipated to remain anchored in next-generation propulsion programs emphasizing fuel efficiency, noise reduction, and lifecycle emissions compliance.

Harmonized certification oversight is expected to accelerate advanced composite blade deployment and ultra-high bypass ratio engine architectures. The competitive structure is likely to remain consolidated around major OEM platforms, reinforcing technological depth and long-cycle supply agreements. Policy-driven efficiency mandates are expected to shape procurement specifications, ensuring a sustained transition toward lightweight, thermally resilient fan blade configurations across both commercial and defense aviation segments.

The U.K. is projected to function as the regional innovation anchor, shaping propulsion technology direction through advanced demonstrator programs and scaled composite manufacturing. National industrial strategy is expected to prioritize next-generation engine validation and blade aerodynamic optimization aligned with European decarbonization targets. OEM-led production scaling is anticipated to reinforce localized supply chain depth while expanding automated composite layup and high-precision machining capacity.

Certification alignment across European authorities is expected to streamline cross-border deployment of efficiency-enhancing propulsion systems, positioning the region to sustain long-term technological leadership in advanced aero engine fan blade engineering.

Competitive Landscape

The global aero engine fan blade market is highly consolidated, with leadership concentrated among global propulsion manufacturers including GE Aerospace, Rolls-Royce, Pratt & Whitney, Safran Aircraft Engines, and MTU Aero Engines. Collectively, these top five participants account for approximately 85% of the global share, reinforcing an oligopolistic structure defined by certification control and proprietary materials engineering. Structural barriers remain exceptionally high due to capital intensity, restricted intellectual property regimes, and stringent aviation qualification standards.

Incumbents benefit from entrenched Control over certified blade geometries, and thermal-resistant material systems sustain technological lock-in across commercial and military propulsion programs.

Differentiation is anchored in platform integration, where blade design aligns with proprietary engine cores, digital twin modeling, and lifecycle maintenance ecosystems. Tier-two suppliers operate within tightly structured risk-sharing partnerships, while independent entrants face limited access to certification pathways. Industry dynamics indicate gradual reinforcement of incumbent dominance through joint ventures, adaptive propulsion programs, and expansion of global maintenance networks.

As efficiency mandates and next-generation engine architectures advance, consolidation is expected to persist, favoring vertically integrated OEMs with certified technology portfolios and scalable advanced manufacturing infrastructure.

Key Industry Developments:

- In February 2026, Rolls-Royce secured a multi-billion-pound investment from the U.K. government to transition the UltraFan from a demonstrator to a certified production engine. This funding accelerated the commercial availability of the world's most efficient large engine, offering airlines a 25% fuel burn reduction and lower carbon emissions for next-gen widebody travel.

- In November 2025, GE Aerospace invested USD 14 million to expand its high-tech manufacturing facility in Pune, increasing production of critical components for GEnx and LEAP engines and strengthening the global aerospace supply chain.

- In October 2025, Safran Aero Boosters and BMT Aerospace partnered to manufacture key components for Pratt & Whitney's F135 engines, enhancing the durability and technological edge of fan components for 5th-generation fighter jets.

Companies Covered in Aero Engine Fan Blade Market

- GE Aerospace

- Rolls-Royce

- Pratt & Whitney

- Safran Aircraft Engines

- CFM International

- MTU Aero Engines

- GKN Aerospace

- IHI Corporation

- Honeywell Aerospace

- Kawasaki Heavy Industries

- Howmet Aerospace

- Triumph Group

- Albany International

- Williams International

- Aviadvigatel

Frequently Asked Questions

The global aero engine fan blade market is projected to be valued at US$9.7 billion in 2026 and is expected to reach US$15.3 billion by 2033, driven by fleet expansion, engine replacement cycles, and the transition toward high-bypass ratio and fuel-efficient propulsion architectures.

Stringent aviation emission regulations are compelling OEMs to redesign propulsion systems around higher bypass ratios and lighter materials. Fan blades now play a critical role in fuel burn optimization, aerodynamic efficiency, and lifecycle emissions reduction. As regulators tighten certification standards, manufacturers are accelerating the adoption of advanced composites, digital twin validation, and precision manufacturing to meet performance and compliance thresholds.

The aero engine fan blade market is forecast to grow at a CAGR of 6.7% from 2026 to 2033, reflecting sustained commercial aircraft production, military modernization programs, and increasing penetration of lightweight composite blade technologies.

North America is expected to lead the market, accounting for approximately 36% share in 2026, supported by a concentrated aerospace manufacturing base, strong OEM presence, advanced materials engineering capabilities, and high composite blade integration across both commercial and defense propulsion platforms.

The aero engine fan blade market is highly consolidated, dominated by major propulsion manufacturers including GE Aerospace, Rolls-Royce, Pratt & Whitney, Safran Aircraft Engines, and MTU Aero Engines. These companies compete through certified blade geometries, proprietary material systems, vertically integrated engine platforms, and long-term service agreements that reinforce technological and contractual lock-in.