- Technology

- 3D Glasses Market

3D Glasses Market Size, Share, and Growth Forecast 2026 - 2033

3D Glasses Market by Product Type (Anaglyph, Polarized, Shutter), Distribution Channel (Online, Offline), End-user (Industrial, Consumer, Electronic, Aerospace), and Regional Analysis for 2026 - 2033

3D Glasses Market Size and Trend Analysis

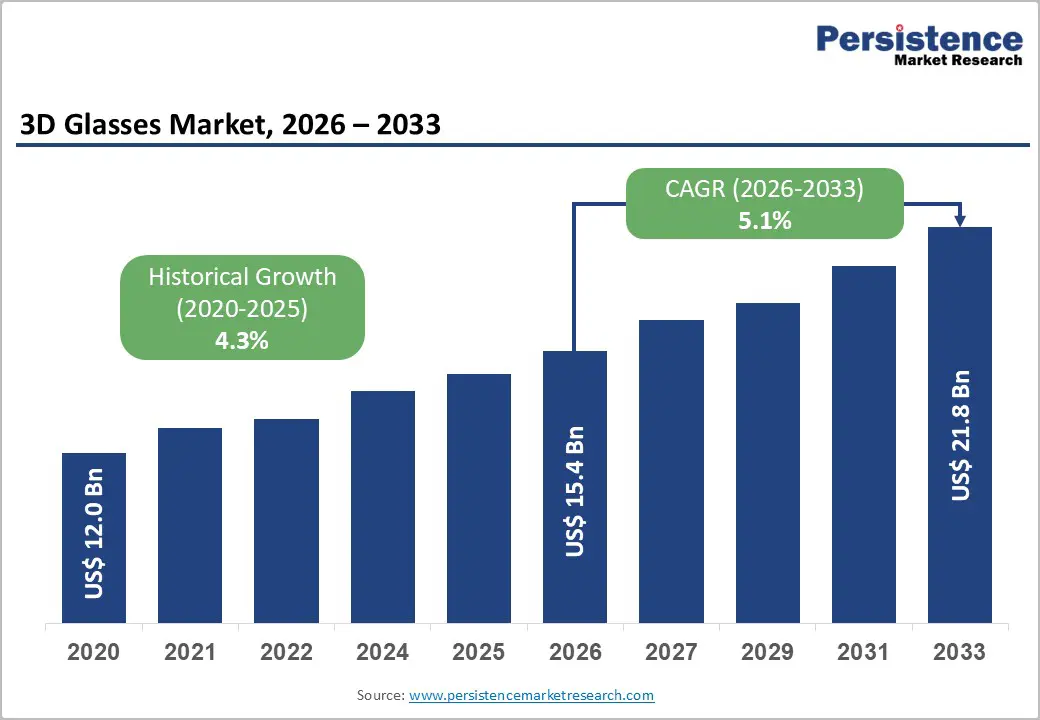

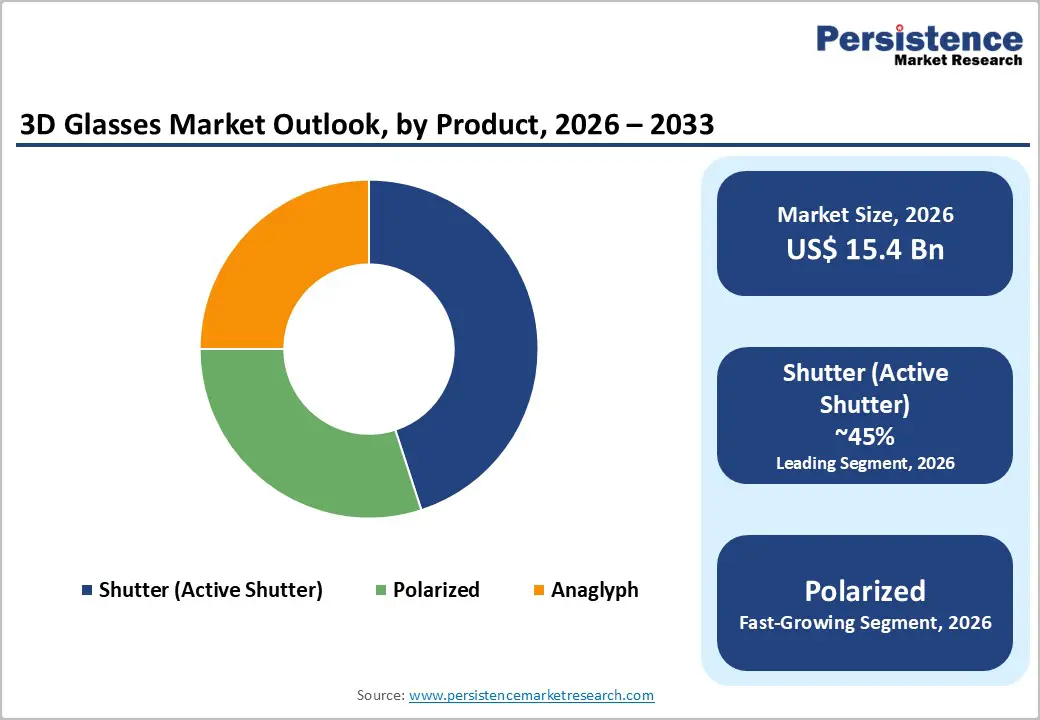

The global 3D glasses market is valued at US$ 15.4 billion in 2026 and is projected to reach US$ 21.8 billion by 2033, growing at a CAGR of 5.1% between 2026 and 2033.

This growth is primarily driven by the rising consumer and enterprise demand for immersive visual experiences across entertainment, gaming, and industrial visualization applications, coupled with the rapid integration of 3D display technologies into consumer electronics. Ongoing investment in augmented reality (AR) and virtual reality (VR) infrastructure, supported by major technology firms and cinema exhibitors, continues to expand the addressable demand.

Key Industry Highlights:

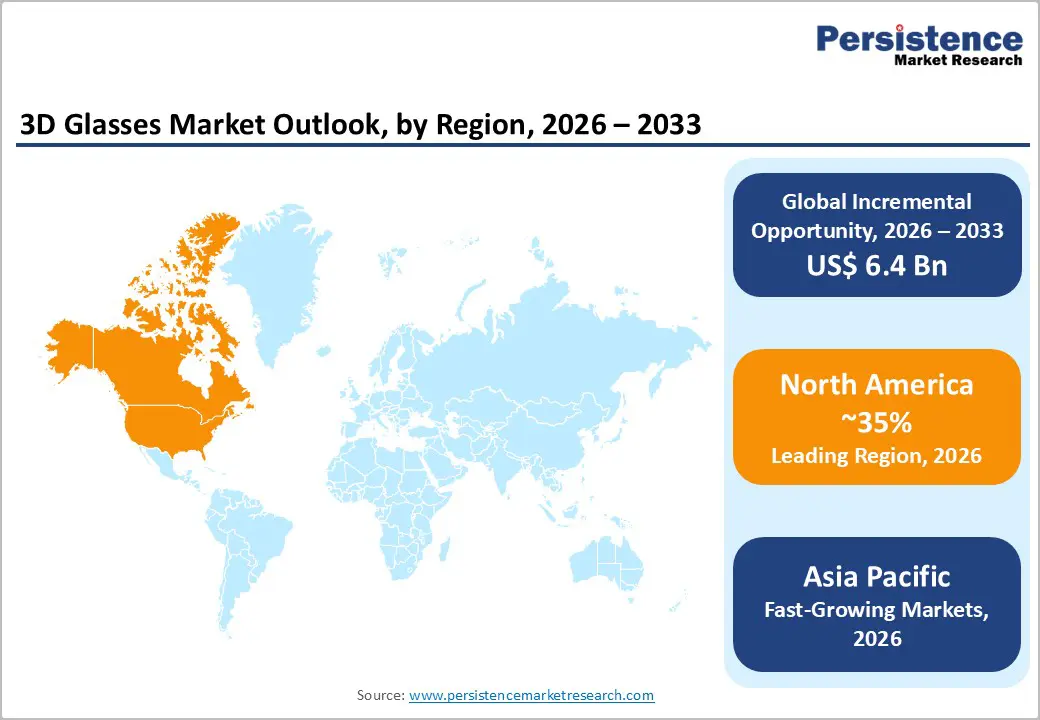

- Leading Region - North America leads the global 3D Glasses market with approximately 33% revenue share, driven by premium cinema investment, a mature consumer electronics ecosystem, and institutional adoption in healthcare and defense sectors, particularly in the U.S.

- Fastest-Growing Region - Asia Pacific is the fastest-growing region, led by China, India, Japan, and ASEAN markets, underpinned by expanding smartphone penetration, increasing cinema infrastructure, and India's position as a global 3D glasses exporter to over 196 countries.

- Dominant Segment - Active Shutter 3D glasses dominate the product type category with approximately 45% market share, supported by widespread use in consumer 3D televisions, gaming monitors, and professional simulation, with NVIDIA reinforcing its ecosystem in 2024.

- Fastest-Growing Segment - The Aerospace end-user segment is emerging as the fastest-growing vertical, fueled by increasing adoption of VR-based pilot training systems and in-flight entertainment platforms, highlighted by Airbus' VR Flight Trainer launch in October 2024 and Hainan Airlines' Rokid AR deployment.

- Opportunity - The integration of stereoscopic visualization in robotic surgery is growing at approximately 18% YoY, according to Intuitive Surgical's 2024 data, offering a high-value, recurring opportunity for specialized 3D glasses suppliers serving hospital procurement cycles.

| Key Insights | Details |

|---|---|

| 3D Glasses Market Size (2026E) | US$ 15.4 Bn |

| Market Value Forecast (2033F) | US$ 21.8 Bn |

| Projected Growth CAGR (2026 - 2033) | 5.1% |

| Historical Market Growth (2020-2025) | 4.3% CAGR |

DRO Analysis

Drivers - Rising Demand for Immersive Entertainment and 3D Cinema Experiences

The global entertainment industry's shift toward premium and immersive formats is a primary catalyst for the 3D Glasses market. The worldwide theatrical market has seen a strong post-pandemic rebound, with Gower Street Analytics revising its 2024 global box office estimate to US$ 32.3 Bn, a figure that directly drives demand for 3D eyewear at cinema venues. RealD Inc., the industry's largest polarized 3D solutions provider, operates across more than 26,500 auditoriums globally, ensuring consistent replacement procurement of passive 3D glasses.

A YouGov survey in August 2024 found that 33% of U.S. consumers attended 3D screenings, with younger adult demographics driving this growth. The North American exhibition industry collectively reinvested over US$ 1.5 Bn into theatre modernization in 2024 alone, according to Cinema United, underscoring the structural demand for 3D eyewear as a recurring accessory at premium exhibition facilities worldwide.

Expanding Applications in AR/VR, Gaming, and Industrial Visualization

The growing adoption of immersive technologies across gaming, industrial simulation, and enterprise visualization is creating sustained demand for advanced shutter and polarized 3D glasses. The global gaming industry continues to expand, with Sensor Tower's Global Mobile Gaming Industry Outlook 2024 reporting that the U.S. mobile gaming market generated US$ 22.2 Bn in 2023, projected to grow to US$ 33.5 Bn by 2028.

In the industrial and aerospace domain, Airbus launched its VR Flight Trainer in October 2024, integrating 3D visualization tools for pilot training. Meanwhile, in medical robotics, Intuitive Surgical reported approximately 18% year-over-year growth in global da Vinci procedures in 2024, expanding the requirement for compatible stereoscopic 3D visualization eyewear in operating theatres. These high-value industrial end-uses are redefining the premium segment of the 3D glasses market.

Restraints - High Cost and Fragility of Active Shutter Technology

Active shutter 3D glasses, which require internal electronics, synchronization modules, and rechargeable batteries to align with display refresh rates, remain significantly more expensive and fragile than passive alternatives. This elevated cost structure poses a critical barrier to widespread adoption, particularly in price-sensitive segments such as public healthcare institutions and budget multiplex chains.

Shutter glasses from leading brands can cost 5 to 15 times as much as passive polarized equivalents, limiting large-scale procurement in education, military training, and community entertainment. The maintenance overhead, battery replacement cycles, and susceptibility to RF interference from adjacent electronics further compound the total cost of ownership, reducing the competitive attractiveness of shutter-based solutions when institutions weigh them against the consistently more affordable polarized and anaglyph alternatives.

Threat from Glasses-Free 3D Display Technologies

The emergence of autostereoscopic (glasses-free) 3D display technologies represents a structural threat to the demand for wearable 3D optics. The global Glasses-Free 3D Display market is estimated at US$ 1.72 Bn in 2025 and is projected to grow at a CAGR of 16.6% through 2032. In March 2025, Samsung Electronics unveiled the Odyssey 3D monitor at its Texas event, featuring AI-powered 2D-to-3D conversion without the need for eyewear.

MOPIC also showcased glasses-free 3D solutions at CES 2025. As lenticular lens and parallax barrier technologies scale in consumer electronics, the addressable use case for traditional 3D glasses in certain segments, particularly home entertainment, is poised to erode gradually over the forecast period.

Opportunities - Growing Adoption of 3D Visualization in Medical Robotics and Surgical Simulation

The integration of stereoscopic 3D visualization in minimally invasive surgery represents a high-value, recurring growth opportunity for premium 3D glasses manufacturers. Robotic-assisted surgical procedures, including those powered by the da Vinci Surgical System from Intuitive Surgical, grew approximately 18% year-over-year globally in 2024, substantially increasing demand for compatible passive and active 3D eyewear at hospital procurement levels. In addition, the U.S.

FDA had authorized 69 AR/VR-integrated medical devices by September 2024, a figure that is expanding annual purchasing cycles for compatible visualization eyewear. Unlike entertainment applications that are subject to content cycle volatility, medical 3D glasses demand is characterized by institutional procurement contracts, strict hygiene-compliance replacement schedules, and regulatory-driven adoption, providing market participants with predictable, high-margin revenue streams largely insulated from mainstream entertainment trends.

Aerospace Training and Defense Simulation as an Emerging High-Value Segment

The aerospace and Défense sector is emerging as one of the fastest-growing end-use verticals for advanced 3D glasses, driven by increasing investment in immersive pilot training, virtual cockpit simulation, and mission rehearsal systems. Airbus deployed its VR Flight Trainer in October 2024, designed to provide pilots with immersive, portable training experiences through virtual cockpit and 3D visualization technologies.

Hainan Airlines became the first major carrier to deploy Rokid AR glasses for in-flight entertainment in February 2024, signaling commercial aviation's appetite for wearable 3D visual platforms. AR developer Rokid also secured nearly US$ 70 Mn in investment funding in 2024 to scale its 3D eyewear and spatial computing product lines, as reported by Forbes.

Category-wise Analysis

Product Type Insights

Among the three primary product types of Anaglyph, Polarized, and Shutter the Shutter (Active Shutter) segment holds the dominant position in the 3D Glasses market, accounting for approximately 45% of market share. This leadership is underpinned by active shutter technology's superior 3D depth perception capabilities, making it the preferred choice for consumer 3D televisions, high-end gaming monitors, and professional visualization applications.

The technology operates through electronically synchronized lenses that alternate between opaque and transparent states at high frequencies typically above 120 Hz matching the refresh rate of compatible 3D displays. In 2024, NVIDIA Corporation updated its 3D Vision protocol to support dual 120 Hz displays, expanding compatibility across gaming monitors. The segment's strength is further reinforced by its status as the standard for premium home theatre systems and broadcast production environments.

Distribution Channel Insights

The Online distribution channel accounts for the leading share in the 3D Glasses market, holding approximately 58% of revenue. The rapid expansion of global e-commerce platforms including Amazon, Flipkart, Alibaba, and brand-specific websites has substantially lowered entry barriers for both established and emerging 3D eyewear manufacturers. The accessibility of detailed product specifications, consumer reviews, and competitive pricing online has made digital retail the preferred purchasing channel, especially for consumer-grade anaglyph and polarized products priced below US$ 30.

Additionally, the ability to access global inventories and benefit from direct-to-consumer shipping has enabled companies like American Paper Optics and dimensional Inc. to efficiently serve both individual and bulk institutional buyers. Post-pandemic behavioural shifts toward digital commerce, particularly across Asia Pacific and North America, continue to reinforce the online channel's dominance.

End-user Insights

The consumer segment is the dominant end-user category in the 3D Glasses market, contributing approximately 47% of total market revenue. This leadership is driven by mass-market demand for 3D glasses across cinema attendance, home theatre systems, and gaming applications. YouGov's August 2024 survey confirmed that 33% of American consumers attended 3D screenings, with younger demographics actively seeking immersive entertainment formats, including 4DX and 3D cinema.

The widespread availability of affordable anaglyph and polarized 3D glasses, particularly through e-commerce channels, has democratized access for households and individual users. Consumer demand is also being buoyed by the growing penetration of 3D-compatible gaming consoles and smart TVs, which require compatible eyewear for the full immersive experience, anchoring consumer electronics as a key consumption sub-segment within the broader Consumer end-user category.

Regional Insights

North America 3D Glasses Market Trends

North America represents the largest regional market for 3D Glasses, accounting for approximately 33% of global revenue. The United States drives this dominance, supported by a dense network of premium cinema exhibitors, a highly developed consumer electronics ecosystem, and robust enterprise spending on immersive visualization.

The North American theatre exhibition sector invested over US$ 1.5 Bn in 2024 in auditorium upgrades, according to Cinema United, creating consistent procurement cycles for both active shutter and polarized 3D eyewear. States including California, Texas, Florida, New York, and Illinois collectively account for over 50% of domestic 3D glasses purchases, driven by high population density and household income levels.

From an innovation standpoint, North America serves as a global hub for 3D glasses R&D and product launches, with companies such as NVIDIA Corporation, RealD Inc., Quantum3D, and American Paper Optics headquartered in the region. The FDA's authorization of 69 AR/VR integrated medical devices by September 2024 has additionally expanded 3D eyewear adoption into clinical and surgical simulation environments.

Europe 3D Glasses Market Trends

Europe holds a significant and stable share in the global 3D Glasses market, with Germany, the United Kingdom, France, and Spain accounting for the largest consumption volumes on the continent. Germany benefits from a mature industrial base and robust demand for 3D visualization in automotive engineering and manufacturing simulation, while the U.K. maintains demand through its cinema-going culture and growing enterprise AR deployments. I

Regulatory harmonization under the EU's CE Marking framework and standards from organizations such as the European Telecommunications Standards Institute (ETSI) ensure product conformity for active shutter glasses distributed across member states. France and Spain are increasingly adopting 3D technologies in the education and vocational training sectors, with institutions procuring stereoscopic eyewear for STEM simulations.

Asia Pacific 3D Glasses Market Trends

Asia Pacific is both the largest manufacturing base and the fastest-growing consumption region in the global 3D Glasses market. The region accounts for over 40% of global unit volume, driven by the consumer electronics powerhouses of China, Japan, South Korea, and the rapidly expanding middle-class markets of India and ASEAN nations. India alone has exported 3D glasses to more than 196 countries globally, with key trading partners including Singapore (US$ 62.33 Mn), the USA (US$ 57.52 Mn), and the UAE (US$ 21.7 Mn) together representing approximately 48% of India's total 3D glasses exports.

China's technology-forward policy environment, including the 'Made in China 2025' initiative, is stimulating domestic production and commercialization of advanced 3D display and eyewear technologies. Samsung Electronics and LG Electronics continue to dominate premium product segments from their South Korean bases, while Optima Asia serves the growing projection and visualization demand across commercial and educational sectors. Japan's strong robotics and surgical technology ecosystem supports specialized 3D eyewear procurement.

Competitive Landscape

The global 3D Glasses market exhibits a moderately fragmented competitive structure, characterized by the coexistence of large multinational consumer electronics corporations and specialized niche manufacturers. Key differentiators employed by market leaders include proprietary synchronization protocols, optical coating technologies, and compatibility with premium display ecosystems.

Companies such as Samsung Electronics, Sony India, NVIDIA Corporation, and LG Electronics compete on breadth of product ecosystems and brand trust, while specialists like RealD Inc., American Paper Optics, and dimensional Inc. differentiate through depth of cinema-grade or niche consumer solutions. R&D investments are increasingly directed toward lightweight materials, AI-assisted display synchronization, and dual-mode functionality.

Key Developments:

- In April 2025, Samsung launched a glasses-free 3D display along with a 27-inch QD-OLED monitor priced at €2250 / £1900 / $2000, delivering an immersive 3D experience and allowing users to see themselves, significantly enhancing user engagement and market appeal

- In April 2025, Sony Electronics expanded its Spatial Reality Display SDK to version 2.5.0, improving OpenXR support and rendering quality, targeting integration in film production and creative industrial design applications.

Companies Covered in 3D Glasses Market

- Epson America, Inc.

- NVIDIA Corporation

- Panasonic Corporation of North America

- Samsung Electronics

- Sony India

- American Paper Optics

- eDimensional Inc.

- LG Electronics

- Optoma Asia

- Quantum3D

- RealD Inc.

Frequently Asked Questions

The global 3D Glasses market is valued at US$ 15.4 Bn in 2026 and is projected to reach US$ 21.8 Bn by 2033, growing at a CAGR of 5.1% over the forecast period.

The primary demand drivers include the resurgence of global cinema box office revenues with the 2024 global box office reaching US$ 32.3 Bn alongside rapidly expanding AR/VR applications in gaming, healthcare, and industrial simulation.

The Active Shutter segment leads the 3D Glasses market by product type, holding approximately 45% market share. Its leadership is attributed to superior 3D depth performance in consumer 3D TVs, gaming systems, and professional visualization platforms, supported by NVIDIA's 3D Vision ecosystem and ongoing compatibility expansions.

North America is the dominant region, accounting for approximately 33% of global market revenue. The United States leads within the region, supported by 26,500+ RealD-equipped auditoriums, major consumer electronics OEMs, significant medical and Défense institutional demand, and a culture of early technology adoption. Investment of over US$ 1.5 Bn in theatre modernization in 2024 continues to reinforce this regional dominance.

The leading companies operating in the global 3D Glasses market include RealD Inc., Samsung Electronics, NVIDIA Corporation, Sony India, LG Electronics, Epson America Inc., Panasonic Corporation of North America, American Paper Optics, eDimensional Inc., Optoma Asia, and Quantum3D.