- Biotechnology

- Pyrogen Testing Market

Pyrogen Testing Market Size, Trends, Share, Growth, and Regional Forecast, 2025 to 2032

Pyrogen Testing Market by Product & Service (Instruments, Consumables, and Services), by Test (In-vitro-based Pyrogen Tests, Rabbit Pyrogen Tests, Limulus Amebocyte Lysate Tests, and Others), by End User, and Regional Analysis from 2025 to 2032

Pyrogen Testing Market Share and Trends Analysis

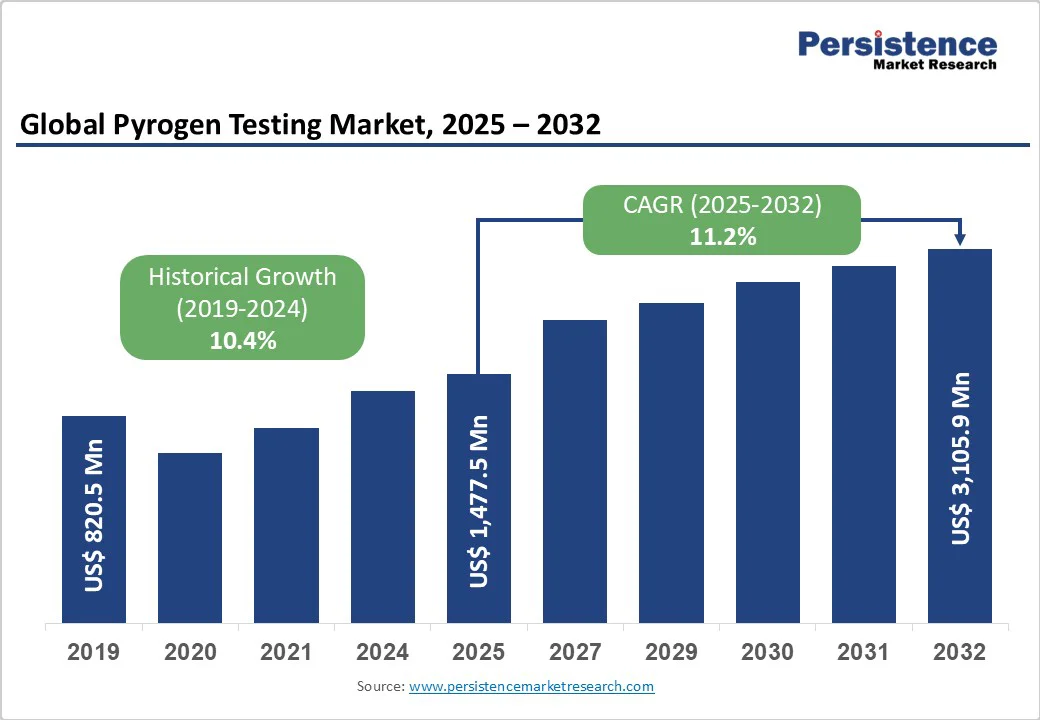

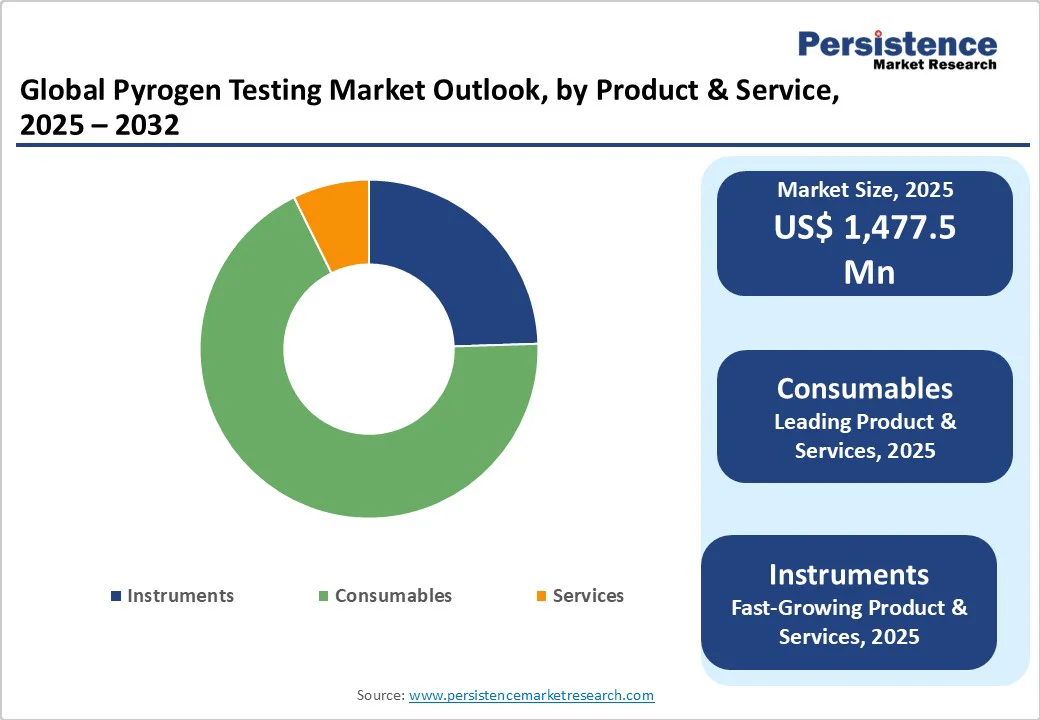

The global pyrogen testing market size is likely to be valued at US$ 1,477.5 million in 2025 and is projected to reach US$ 3,105.9 million by 2032, growing at a CAGR of 11.2% during the forecast period from 2025 to 2032.

Global demand for pyrogen testing is rising as the biopharmaceutical and medical device industries expand the production of biologics, vaccines, and sterile injectables. Increasing regulatory requirements for endotoxin and pyrogen safety, along with growing adoption of advanced in-vitro testing methods, are driving market growth.

Key Industry Highlights:

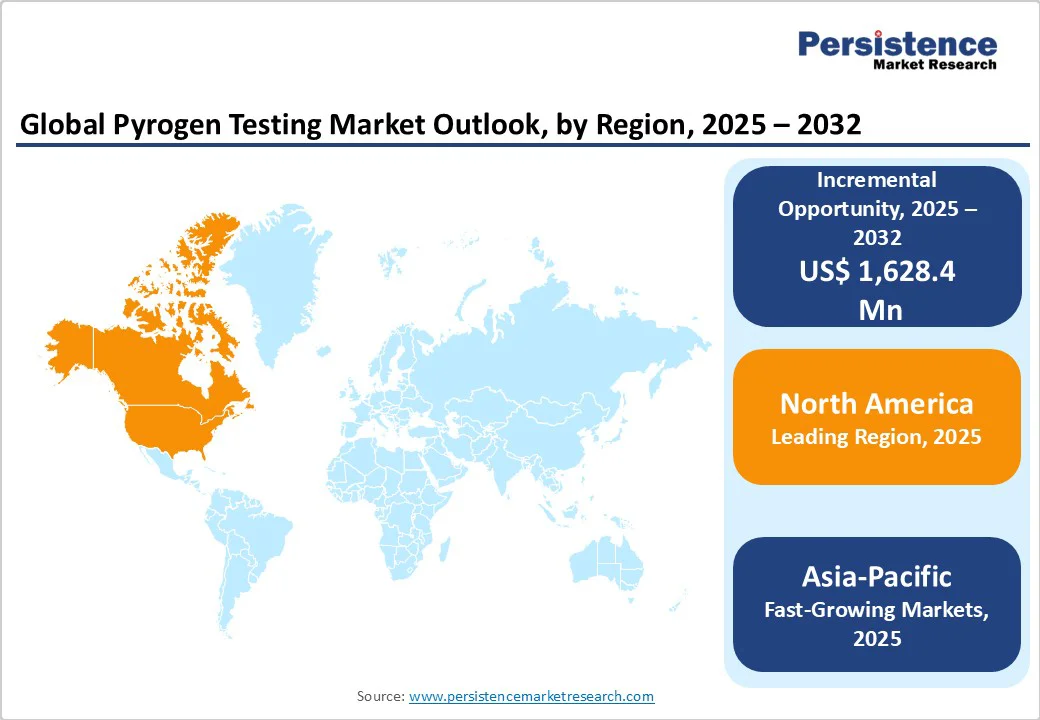

- Leading Region: North America dominates the global market, supported by a strong presence of the biopharmaceutical and medical device industry, increasing investments, and stringent regulatory standards.

- Fastest-Growing Region: Asia Pacific is expanding rapidly due to expanding biologics and vaccine manufacturing, increasing healthcare infrastructure, and rising regulatory harmonization with global standards.

- Leading Test Segment: Limulus Amebocyte Lysate (LAL) test leads the segment due to its strong integration into pharmaceutical quality control workflows and proven accuracy in endotoxin detection.

- Fastest-Growing Test Segment: In-vitro-based pyrogen testing is the fastest-growing segment, driven by increasing adoption of animal-free testing methods, regulatory support for alternatives to the Rabbit Pyrogen Test.

- Investments: The growing investments support the development, regulatory validation, and commercialization of advanced benchtop devices that provide faster, more sustainable, and animal-free alternatives to traditional pyrogen and endotoxin testing methods.

| Key Insights | Details |

|---|---|

| Pyrogen Testing Market Size (2025E) | US$ 1,477.5 Mn |

| Market Value Forecast (2032F) | US$ 3,105.9 Mn |

| Projected Growth (CAGR 2025 to 2032) | 11.2% |

| Historical Market Growth (CAGR 2019 to 2024) | 10.4% |

Market Dynamics

Driver - Growing Production of Biologics, Biosimilar, and Shift Toward In-Vitro Pyrogen Testing

The demand for biologics, biosimilars, and vaccines majorly drives the pyrogen testing market. Increasing prevalence of chronic diseases, patent expirations boosting biosimilar output, and global immunization programs are fueling large-scale manufacturing of sterile injectables.

For instance, according to the Department of Pharmaceuticals, Government of India, around 24 drugs are expected to lose their patents between 2022 and 2030, encouraging biosimilar development and increasing the volume of products requiring pyrogen testing.

The pyrogen testing market is increasingly shifting from traditional animal-based methods, such as the Rabbit Pyrogen Test and LAL (Limulus Amebocyte Lysate) assay, toward advanced in-vitro testing solutions. In-vitro methods offer faster, more reproducible, and standardized results while reducing reliance on animals. Among these, the Monocyte Activation Test (MAT) has emerged as a leading approach, providing reliable pyrogen detection for biologics, vaccines, and sterile injectables.

Companies are actively investing in research and development (R&D) and launching innovative in-vitro solutions.

For instance, in July 2024, FUJIFILM Wako Pure Chemicals Corporation launched LumiMAT, a next-generation MAT-based pyrogen detection kit, and PYROSTAR Neo+, a recombinant protein reagent for endotoxin detection, offering globally accessible alternatives to traditional testing methods. Regulatory bodies, including the European Pharmacopeia, now endorse MAT as an accepted alternative, accelerating its adoption and driving market growth.

Restraints - High Costs of Newer Advanced Testing Methods & Equipment

Adopting modern pyrogen testing methods such as the Monocyte Activation Test (MAT) and recombinant Factor C (rFC) assays requires significant investment in specialized instruments, reagents, and validation processes.

These tests often have higher upfront costs compared to traditional LAL or Rabbit Pyrogen Tests, creating a financial burden for small- and mid-sized manufacturers. Additional expenses for staff training and compliance documentation further raise the overall cost of implementation, slowing down adoption rates, particularly in emerging markets.

Moreover, the stringent and time-consuming regulatory approval process is restraining the market growth of the pyrogen testing market. Manufacturers must adhere to rigorous guidelines set by bodies such as the Food and Drug Administration (FDA), European Medicines Agency (EMA), and United States Pharmacopeia (USP), which demand extensive validation studies, detailed documentation, and robust quality control measures.

These requirements often lead to higher operational costs, product launch delays, and longer market entry timelines. Additionally, frequent updates to regulatory standards and the need to revise testing protocols create further complexity, slowing the adoption of innovative pyrogen testing solutions.

Opportunity - Expanding Medical Device Industry Boosts Pyrogen Testing Demand

The rapid expansion of the medical device sector presents a significant opportunity for the pyrogen testing market, as increasing production of implantable devices and surgical instruments drives demand for rigorous safety testing. Regulatory requirements for pyrogen and endotoxin testing create a continuous need for reliable and advanced testing solutions.

For example, in January 2025, BD announced plans to expand its U.S. manufacturing network for syringes, needles, and IV catheters, highlighting the potential for pyrogen testing providers to support growing device production while ensuring compliance with safety standards.

As regulatory requirements for pyrogen and endotoxin testing become more stringent, many small and mid-sized biopharmaceutical and medical device manufacturers lack the in-house expertise, equipment, or resources to perform advanced testing.

This increases reliance on Contract Research Organizations (CROs) and specialized third-party laboratories that provide validated, compliant pyrogen testing services. Outsourcing reduces operational costs, ensures faster turnaround, and mitigates regulatory risks.

Category-wise Analysis

By Product & Service, Consumables Dominate Globally Due to Recurring Demand in Routine Pyrogen and Endotoxin Testing

The consumables segment is projected to dominate the pyrogen testing market in 2025, accounting for a revenue share of 54.9%.

The segment’s strong performance is primarily driven by the high demand for single-use reagents, test kits, and assay materials required for routine pyrogen and endotoxin testing in biopharmaceutical and medical device manufacturing. Continuous adoption of advanced testing methods, regulatory mandates for product safety, and the need for consistent, reliable results further fuel the growth of consumables.

By Test, Ability to Detect Extremely Low Levels of Endotoxins makes LAL Tests the Leading Category

The Limulus Amebocyte Lysate (LAL) tests segment is projected to dominate the pyrogen testing market in 2025, accounting for a revenue share of 57.8%. This is due to its high sensitivity, rapid detection capability, and regulatory approval from agencies such as the FDA, EMA, and USP. It is the industry standard for identifying bacterial endotoxins in pharmaceuticals, biologics, and medical devices, offering faster, more ethical, and cost-effective testing compared to traditional rabbit-based methods.

By End User, Pharmaceutical Companies Lead the Market Globally Due to the Extensive Production of Biologics, Vaccines, and Injectable Drugs

The pharmaceutical companies segment is projected to dominate the pyrogen testing market in 2025, accounting for a revenue share of 65.1%. This is due to the growing production of biologics, biosimilars, and sterile injectable drugs, all of which require stringent pyrogen and endotoxin testing to meet regulatory standards.

Pharmaceutical companies conduct frequent quality control testing across multiple stages of manufacturing to ensure product safety and avoid costly recalls. Additionally, patent expirations and the resulting surge in biosimilar development have further increased testing volumes, boosting the segment’s growth.

Region-wise Insights

North America Pyrogen Testing Market Trends

North America is expected to dominate globally with a value share of 37.8% in 2025, with the U.S. leading the region due to the presence of a well-established biopharmaceutical and medical device industry, robust regulatory framework, and high R&D spending.

For instance, in April 2025, Novartis announced a planned US$ 23 billion investment over five years in U.S. infrastructure, adding seven new facilities and expanding manufacturing and research capabilities. Such expansions are expected to increase production volumes, further boosting demand for pyrogen testing solutions.

The region’s strict FDA guidelines mandate comprehensive endotoxin and pyrogen testing for biologics, vaccines, and medical devices, driving continuous demand. Additionally, the surge in biosimilar launches post-patent expiry of key biologics and increased investments in advanced testing technologies, such as MAT and recombinant Factor C assays, further contribute to market growth.

Europe Pyrogen Testing Market Trends

Europe is expected to reach a stable growth driven by strong regulatory support for non-animal testing methods, rising biologics and biosimilar production, and increased vaccine manufacturing capacity.

The European Pharmacopeia has officially phased out the Rabbit Pyrogen Test (RPT) and fully deleted it from all monographs effective July 1, 2025, requiring marketing authorization holders to adopt non-animal pyrogen testing methods by January 1, 2026. The European Pharmacopeia’s endorsement of the Monocyte Activation Test (MAT) as an accepted alternative to the Rabbit Pyrogen Test has accelerated the adoption of in-vitro assays across the region.

Additionally, growing investments by pharmaceutical and biotechnology companies, along with the presence of advanced research infrastructure in countries such as Germany, Switzerland, and the U.K., further drive market growth in the region.

For instance, in August 2025, Cotton Mouton Diagnostics (CMD), a UK-based diagnostics technology company, received a £500,000 (US$571,460 million) investment from CPI Enterprises under the Innovate UK Catapult Investment Pilot to advance αBET, a sustainable benchtop instrument offering an efficient and user-friendly alternative to traditional endotoxin and pyrogen testing.

Asia and Pacific Pyrogen Testing Market Trends

Asia Pacific is expected to register a relatively higher CAGR of around 14.6% between 2025 and 2032, fueled by the rapid expansion of biopharmaceutical manufacturing, rising vaccine production, and increasing government initiatives to strengthen healthcare infrastructure. Countries such as India, China, and South Korea are investing heavily in biologics, biosimilars, and sterile injectable facilities to meet both domestic and export demand.

Companies are also expanding their testing capabilities to address the rising need for pyrogen detection. For instance, in July 2022, Merck opened its first Microbiology Application and Training (MAT) Lab in Jigani, Bengaluru, with a €200,000 (US$208,990) investment.

The lab provides sterility, pyrogen, and rapid bioburden testing services, along with training and method development support for pharma and biopharma manufacturers, significantly enhancing regional testing capacity. Growing regulatory harmonization with U.S. FDA and EMA standards further drives the adoption of advanced pyrogen and endotoxin testing solutions across the region.

Competitive Landscape

The global pyrogen testing market is highly competitive, with major players such as Charles River Laboratories, Inc, Lonza, Merck KGaA, Thermo Fisher Scientific, Inc., and bioMérieux SA dominating the industry through robust product portfolios, global distribution networks, and continuous innovation in testing solutions.

These companies focus on developing advanced in-vitro assays, recombinant Factor C reagents, and automated platforms to improve accuracy, efficiency, and regulatory compliance. Strategic initiatives, mergers & acquisitions, capacity expansions, and partnerships with biopharma manufacturers further strengthen their market presence and drive growth.

Key Industry Developments:

- In October 2023, Lonza launched the PyroCell MAT Rapid System and PyroCell MAT Human Serum (HS) Rapid System, which cut testing time from two days to two hours, providing pharma manufacturers with faster, rabbit-free pyrogen testing options while supporting the industry’s shift toward animal-free methods.

- In August 2023, Lonza launched the Nebula Absorbance Reader, a new microplate reader optimised for streamlined endotoxin and pyrogen testing.

Companies Covered in Pyrogen Testing Market

- Charles River Laboratories, Inc

- Lonza

- Merck KGaA

- Thermo Fisher Scientific, Inc.

- Associates of Cape Cod, Inc.

- GenScript Biotech Corporation

- bioMérieux SA

- FUJIFILM Wako Pure Chemical Corporation

- Eurofins Scientific

- WuXi AppTec

- Hycult Biotech

- Cormica Ltd

- Nelson Laboratories, LLC - A Sotera Health company

Frequently Asked Questions

The global market is projected to be valued at US$ 1,477.5 Mn in 2025.

Increasing biologics, vaccine, and sterile injectable production, which require stringent endotoxin and pyrogen testing is driving the global market.

The global pyrogen testing market is poised to witness a CAGR of 11.2% between 2025 and 2032.

Government initiatives, increasing investments in biopharmaceutical and medical device manufacturing, and the expansion of vaccine and sterile injectable production are creating significant growth opportunities in the market.

Charles River Laboratories, Inc., Lonza, Merck KGaA, and Thermo Fisher Scientific, Inc, are some of the key players in the market.