- Executive Summary

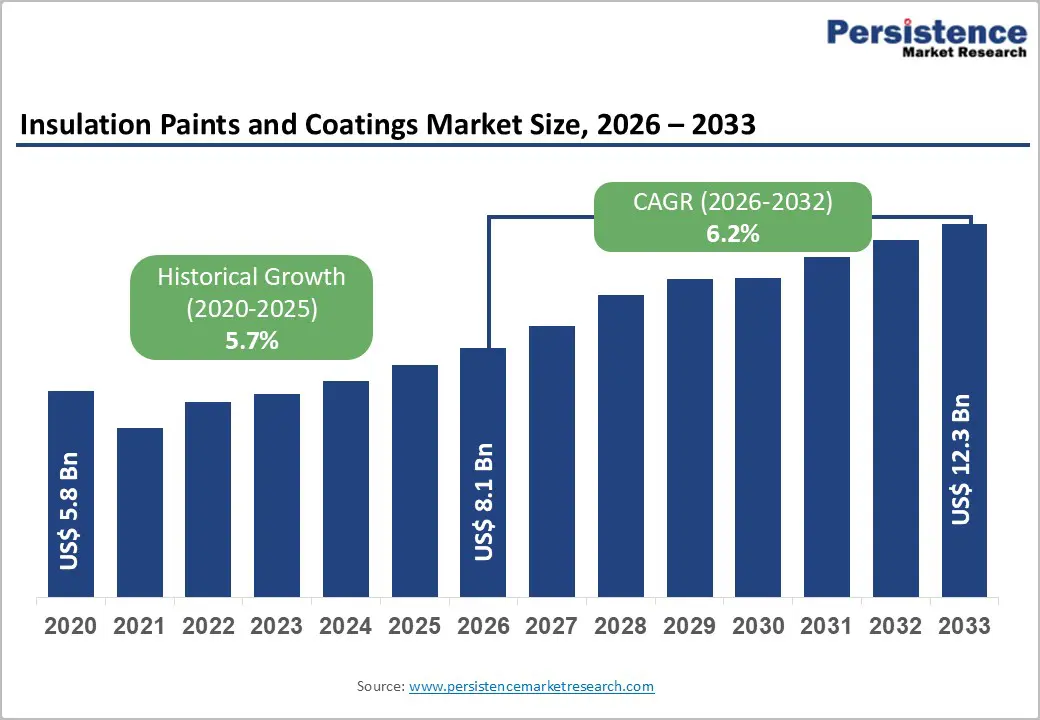

- Global Insulation Paints and Coatings Market Snapshot 2026 and 2033

- Market Opportunity Assessment, 2026 - 2033, US$ Bn

- Key Market Trends

- Industry Developments and Key Market Events

- Demand Side and Supply Side Analysis

- PMR Analysis and Recommendations

- Market Overview

- Market Scope and Definitions

- Value Chain Analysis

- Macro-Economic Factors

- Global GDP Outlook

- Global Construction Industry Overview

- Global Automotive Industry Overview

- Forecast Factors - Relevance and Impact

- COVID-19 Impact Assessment

- PESTLE Analysis

- Porter's Five Forces Analysis

- Geopolitical Tensions: Market Impact

- Regulatory and Technology Landscape

- Market Dynamics

- Drivers

- Restraints

- Opportunities

- Trends

- Price Trend Analysis, 2020 - 2033

- Region-wise Price Analysis

- Price by Segments

- Price Impact Factors

- Global Insulation Paints and Coatings Market Outlook: Historical (2020 - 2025) and Forecast (2026 - 2033)

- Key Highlights

- Global Insulation Paints and Coatings Market Outlook: Product Type

- Introduction/Key Findings

- Historical Market Size (US$ Bn) and Volume (Tons) Analysis by Product Type, 2020-2025

- Current Market Size (US$ Bn) and Volume (Tons) Forecast, by Product Type, 2026-2033

- Acrylic

- Epoxy

- Polyurethane

- Alkyd

- YSZ

- Market Attractiveness Analysis: Product Type

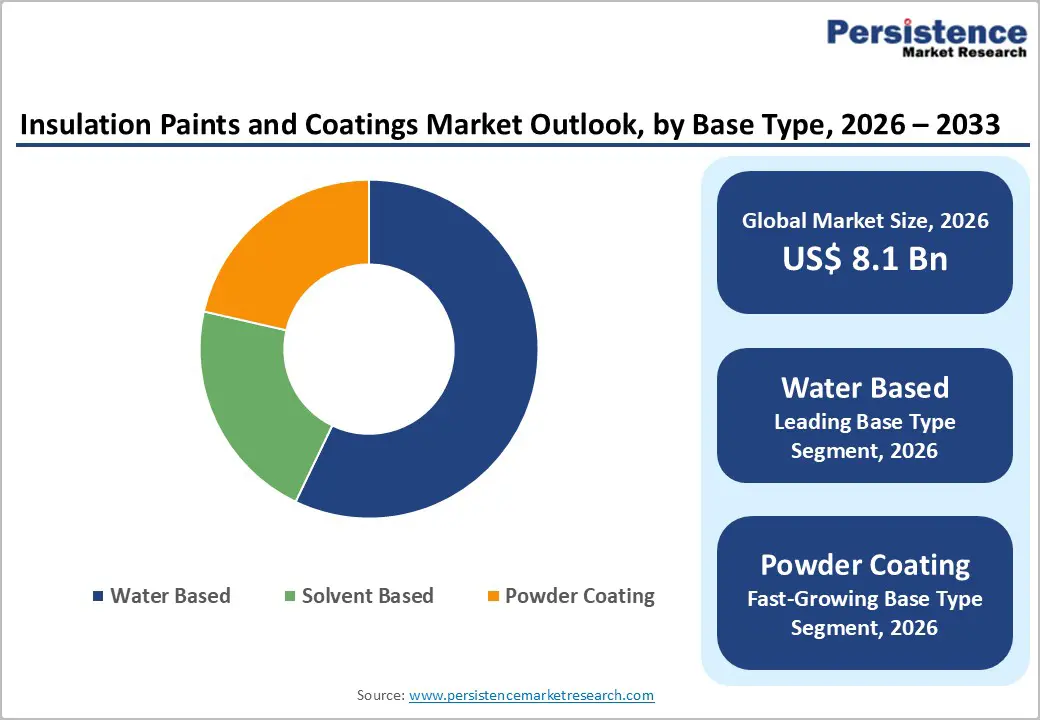

- Global Insulation Paints and Coatings Market Outlook: Base Type

- Introduction/Key Findings

- Historical Market Size (US$ Bn) and Volume (Tons) Analysis by Base Type, 2020-2025

- Current Market Size (US$ Bn) and Volume (Tons) Forecast, by Base Type, 2026-2033

- Water Based

- Solvent Based

- Powder Coating

- Market Attractiveness Analysis: Base Type

- Global Insulation Paints and Coatings Market Outlook: End Use Industry

- Introduction/Key Findings

- Historical Market Size (US$ Bn) and Volume (Tons) Analysis by End Use Industry, 2020-2025

- Current Market Size (US$ Bn) and Volume (Tons) Forecast, by End Use Industry, 2026-2033

- Manufacturing

- Buildings & Construction

- Oil & Gas

- Automotive

- Marine

- Aerospace

- Others

- Market Attractiveness Analysis: End Use Industry

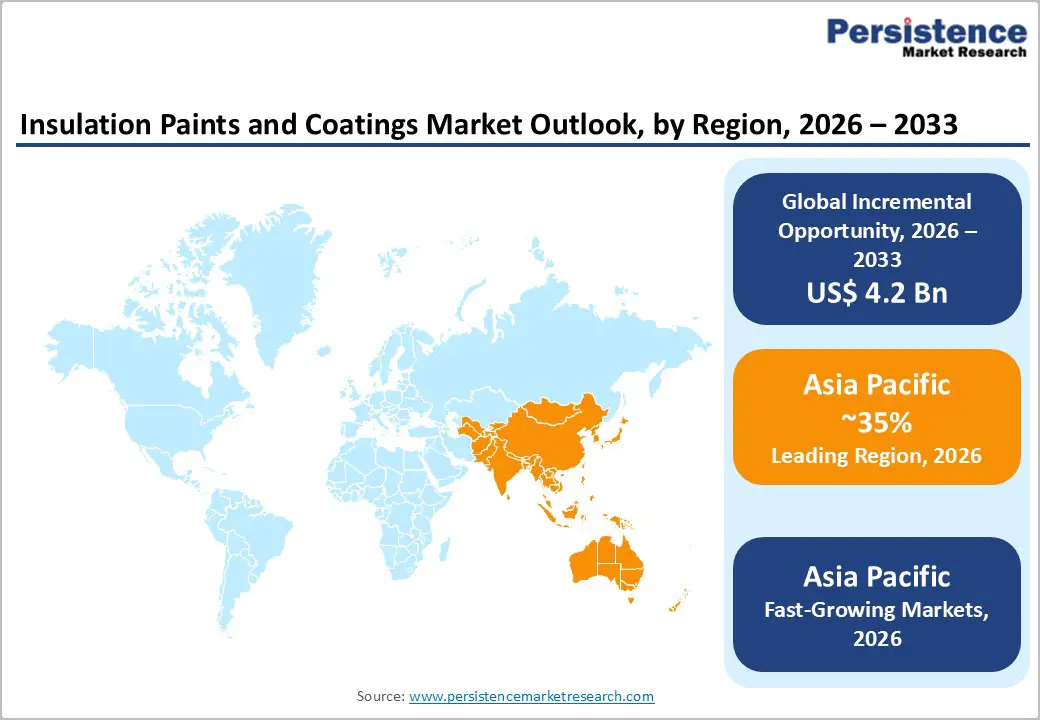

- Global Insulation Paints and Coatings Market Outlook: Region

- Key Highlights

- Historical Market Size (US$ Bn) and Volume (Tons) Analysis by Region, 2020-2025

- Current Market Size (US$ Bn) and Volume (Tons) Forecast, by Region, 2026-2033

- North America

- Europe

- East Asia

- South Asia & Oceania

- Latin America

- Middle East & Africa

- Market Attractiveness Analysis: Region

- North America Insulation Paints and Coatings Market Outlook: Historical (2020 - 2025) and Forecast (2026 - 2033)

- Key Highlights

- Pricing Analysis

- North America Market Size (US$ Bn) and Volume (Tons) Forecast, by Country, 2026-2033

- U.S.

- Canada

- North America Market Size (US$ Bn) and Volume (Tons) Forecast, by Product Type, 2026-2033

- Acrylic

- Epoxy

- Polyurethane

- Alkyd

- YSZ

- North America Market Size (US$ Bn) and Volume (Tons) Forecast, by Base Type, 2026-2033

- Water Based

- Solvent Based

- Powder Coating

- North America Market Size (US$ Bn) and Volume (Tons) Forecast, by End Use Industry, 2026-2033

- Manufacturing

- Buildings & Construction

- Oil & Gas

- Automotive

- Marine

- Aerospace

- Others

- Europe Insulation Paints and Coatings Market Outlook: Historical (2020 - 2025) and Forecast (2026 - 2033)

- Key Highlights

- Pricing Analysis

- Europe Market Size (US$ Bn) and Volume (Tons) Forecast, by Country, 2026-2033

- Germany

- Italy

- France

- U.K.

- Spain

- Russia

- Rest of Europe

- Europe Market Size (US$ Bn) and Volume (Tons) Forecast, by Product Type, 2026-2033

- Acrylic

- Epoxy

- Polyurethane

- Alkyd

- YSZ

- Europe Market Size (US$ Bn) and Volume (Tons) Forecast, by Base Type, 2026-2033

- Water Based

- Solvent Based

- Powder Coating

- Europe Market Size (US$ Bn) and Volume (Tons) Forecast, by End Use Industry, 2026-2033

- Manufacturing

- Buildings & Construction

- Oil & Gas

- Automotive

- Marine

- Aerospace

- Others

- East Asia Insulation Paints and Coatings Market Outlook: Historical (2020 - 2025) and Forecast (2026 - 2033)

- Key Highlights

- Pricing Analysis

- East Asia Market Size (US$ Bn) and Volume (Tons) Forecast, by Country, 2026-2033

- China

- Japan

- South Korea

- East Asia Market Size (US$ Bn) and Volume (Tons) Forecast, by Product Type, 2026-2033

- Acrylic

- Epoxy

- Polyurethane

- Alkyd

- YSZ

- East Asia Market Size (US$ Bn) and Volume (Tons) Forecast, by Base Type, 2026-2033

- Water Based

- Solvent Based

- Powder Coating

- East Asia Market Size (US$ Bn) and Volume (Tons) Forecast, by End Use Industry, 2026-2033

- Manufacturing

- Buildings & Construction

- Oil & Gas

- Automotive

- Marine

- Aerospace

- Others

- South Asia & Oceania Insulation Paints and Coatings Market Outlook: Historical (2020 - 2025) and Forecast (2026 - 2033)

- Key Highlights

- Pricing Analysis

- South Asia & Oceania Market Size (US$ Bn) and Volume (Tons) Forecast, by Country, 2026-2033

- India

- Southeast Asia

- ANZ

- Rest of SAO

- South Asia & Oceania Market Size (US$ Bn) and Volume (Tons) Forecast, by Product Type, 2026-2033

- Acrylic

- Epoxy

- Polyurethane

- Alkyd

- YSZ

- South Asia & Oceania Market Size (US$ Bn) and Volume (Tons) Forecast, by Base Type, 2026-2033

- Water Based

- Solvent Based

- Powder Coating

- South Asia & Oceania Market Size (US$ Bn) and Volume (Tons) Forecast, by End Use Industry, 2026-2033

- Manufacturing

- Buildings & Construction

- Oil & Gas

- Automotive

- Marine

- Aerospace

- Others

- Latin America Insulation Paints and Coatings Market Outlook: Historical (2020 - 2025) and Forecast (2026 - 2033)

- Key Highlights

- Pricing Analysis

- Latin America Market Size (US$ Bn) and Volume (Tons) Forecast, by Country, 2026-2033

- Brazil

- Mexico

- Rest of LATAM

- Latin America Market Size (US$ Bn) and Volume (Tons) Forecast, by Product Type, 2026-2033

- Acrylic

- Epoxy

- Polyurethane

- Alkyd

- YSZ

- Latin America Market Size (US$ Bn) and Volume (Tons) Forecast, by Base Type, 2026-2033

- Water Based

- Solvent Based

- Powder Coating

- Latin America Market Size (US$ Bn) and Volume (Tons) Forecast, by End Use Industry, 2026-2033

- Manufacturing

- Buildings & Construction

- Oil & Gas

- Automotive

- Marine

- Aerospace

- Others

- Middle East & Africa Insulation Paints and Coatings Market Outlook: Historical (2020 - 2025) and Forecast (2026 - 2033)

- Key Highlights

- Pricing Analysis

- Middle East & Africa Market Size (US$ Bn) and Volume (Tons) Forecast, by Country, 2026-2033

- GCC Countries

- South Africa

- Northern Africa

- Rest of MEA

- Middle East & Africa Market Size (US$ Bn) and Volume (Tons) Forecast, by Product Type, 2026-2033

- Acrylic

- Epoxy

- Polyurethane

- Alkyd

- YSZ

- Middle East & Africa Market Size (US$ Bn) and Volume (Tons) Forecast, by Base Type, 2026-2033

- Water Based

- Solvent Based

- Powder Coating

- Middle East & Africa Market Size (US$ Bn) and Volume (Tons) Forecast, by End Use Industry, 2026-2033

- Manufacturing

- Buildings & Construction

- Oil & Gas

- Automotive

- Marine

- Aerospace

- Others

- Competition Landscape

- Market Share Analysis, 2025

- Market Structure

- Competition Intensity Mapping

- Competition Dashboard

- Company Profiles

- Akzo Nobel

- Company Overview

- Product Portfolio/Offerings

- Key Financials

- SWOT Analysis

- Company Strategy and Key Developments

- Shewrin Williams

- PPG

- Hy-Tech Thermal Solutions

- Highland International

- Okitsumo Inc.

- NISSIN SANGYO CO., LTD.

- Industrial Nanotech, Inc.

- Insuladd Environmental Products Ltd

- Thermilate Roof and Wall Coatings Ltd.

- Kansai Paint Co. Ltd

- Nippon Paint Holdings Co., Ltd.

- Isonem Paint & Insulation Technologies

- Prolat S. Dimopoulos & Co. E.E.

- Thermilate Technologies Ltd.

- Akzo Nobel

- Appendix

- Research Methodology

- Research Assumptions

- Acronyms and Abbreviations

- Inks, Coatings, Adhesives & Sealants (ICAS)

- Insulation Paints and Coatings Market

Insulation Paints and Coatings Market Size, Share, and Growth Forecast 2026 - 2033

Insulation Paints and Coatings Market by Product Type (Acrylic, Epoxy, Polyurethane, Alkyd, and YSZ), Base Type (Water Based, Solvent Based, and Powder Coating), End Use Industry (Manufacturing, Buildings & Construction, Oil & Gas, Automotive, Marine, Aerospace, and Others), and Regional Analysis, 2026 - 2033

Key Industry Highlights:

- Leading Region: Asia Pacific maintains the strongest regional position with approximately 36.5% global market share, driven by rapid construction activity, manufacturing sector dominance, and extensive industrial infrastructure requiring thermal insulation solutions and energy efficiency compliance.

- Fastest Growing Country: India represents the fastest-growing region, expanding at approximately 7.1% CAGR, supported by rapid urbanization, manufacturing expansion, government energy efficiency initiatives, and substantial infrastructure development.

- Leading Product Type: Acrylic insulation coatings dominate the market with approximately 42% share, reflecting versatile application capabilities, cost-effectiveness, established manufacturing infrastructure, and broad compatibility with diverse industrial applications and operating environments.

- Growing Base Type: Water-based insulation coatings are the fastest-growing segment, with a 6.8% CAGR, driven by stringent VOC emissions regulations, growing consumer sustainability preferences, and regulatory mandates that promote the adoption of environmentally compliant coating systems globally.

- Key Market Opportunity: Aerospace thermal barrier coatings and multifunctional nano-coating technologies represent significant long-term market opportunities, with emerging applications in high-temperature industrial environments.

| Key Insights | Details |

|---|---|

| Insulation Paints and Coatings Market Size (2026E) | US$ 8.1 Bn |

| Market Value Forecast (2033F) | US$ 12.3 Bn |

| Projected Growth CAGR (2026 - 2033) | 6.2% |

| Historical Market Growth (2020 - 2025) | 5.7% |

Market Dynamics

Drivers - Rising Global Water Scarcity and Municipal Water Treatment Infrastructure Investment

The rising emphasis on energy efficiency and effective thermal management across residential, commercial, and industrial infrastructure is a key driver for the global Insulation Paints and Coatings Market. Governments, regulatory bodies, and industry stakeholders worldwide are increasingly prioritizing energy conservation to reduce carbon emissions, lower operating costs, and meet long-term sustainability targets. Insulation paints and coatings play a critical role in this transition by minimizing heat transfer through walls, roofs, pipelines, storage tanks, and industrial equipment, thereby enhancing overall energy performance without requiring major structural modifications.

The growing adoption of green building standards and energy-efficient building codes in the construction sector is increasing demand for advanced insulation coatings that reduce heating and cooling loads, improve indoor comfort, and extend building lifespan. Compared with conventional insulation materials, insulation paints and coatings offer advantages such as lightweight application, corrosion resistance, ease of maintenance, and suitability for complex geometries that are difficult to insulate with traditional materials. Rising energy prices and increasing awareness of lifecycle cost savings further strengthen their value proposition, as end users seek solutions that deliver long-term operational efficiency. Retrofitting and renovation activities in aging infrastructure are driving adoption, since insulation coatings can be applied directly to existing surfaces with minimal downtime.

Expanding Industrialization and Infrastructure Development in Emerging and Developed Economies

The accelerating pace of industrialization and large-scale infrastructure development across both emerging and developed economies is another significant driver for the global Insulation Paints and Coatings Market. Rapid growth in sectors such as oil & gas, power generation, petrochemicals, marine, and heavy manufacturing is creating sustained demand for advanced surface protection and thermal insulation solutions. Insulation paints and coatings are increasingly preferred in these industries for their ability to provide thermal control, prevent condensation, provide corrosion resistance, and enhance worker safety in a single application.

Infrastructure investments in transportation networks, including railways, ports, and airports, are also contributing to market growth, as insulation coatings are used to protect metal and concrete structures from temperature fluctuations, moisture ingress, and environmental degradation. In developed regions, modernization of aging industrial and public infrastructure is further driving demand, as insulation coatings offer a cost-effective alternative to complete material replacement or bulky insulation systems. As a result, expanding industrial capacity and ongoing infrastructure development remain powerful growth engines for the global insulation paints and coatings market.

Restraints - High Initial Cost and Limited Awareness Compared to Conventional Insulation Materials

The relatively high initial cost of advanced insulation coating technologies compared to conventional insulation materials such as mineral wool, fiberglass, or foam-based systems limits market growth. High-performance insulation paints often incorporate specialized ceramic microspheres, advanced polymers, or nanotechnology-based additives, which significantly increase raw material and formulation costs. For cost-sensitive end users, particularly in developing regions, these higher upfront costs can deter adoption despite the long-term energy savings offered by insulation coatings.

Limited awareness and understanding of performance benefits further constrain adoption. Many contractors, building owners, and industrial operators remain more familiar with traditional insulation solutions and may be skeptical about the thermal efficiency claims of insulation paints, especially when performance is influenced by factors such as surface preparation, application thickness, and operating conditions. Misconceptions regarding insulation coatings being “paint-only” solutions rather than functional thermal barriers also hinder wider acceptance. In some cases, the lack of standardized testing methods and region-specific performance benchmarks makes it difficult for buyers to accurately compare insulation coatings with conventional systems, thereby delaying purchasing decisions.

Performance Limitations and Regulatory Challenges Across Diverse Applications

Performance limitations under certain operating conditions, along with increasing regulatory complexity, is another key challenge to the insulation paints and coatings market. While insulation coatings are effective for reducing surface temperatures and controlling heat transfer, they may not always match the insulation efficiency of thick, conventional insulation systems in extremely high-temperature or cryogenic environments. This limits their suitability for certain heavy industrial applications, where regulatory standards mandate minimum insulation thickness or specific thermal resistance values that coatings alone may not achieve.

Performance consistency can vary with substrate type, application quality, climatic conditions, and long-term exposure to UV radiation, moisture, or chemicals. Regulatory challenges also pose barriers, as insulation paints and coatings must comply with evolving environmental, safety, and emissions regulations across different regions. Stringent rules related to volatile organic compound (VOC) emissions, chemical content, and workplace safety can increase compliance costs for manufacturers and delay product approvals. Smaller players may struggle to meet these regulatory requirements, reducing product availability and innovation in some markets.

Opportunity - Aerospace and High-Temperature Application Expansion with YSZ Thermal Barrier Coatings

Yttria-stabilized zirconia (YSZ) thermal barrier coatings represent a significant growth opportunity, driven by expanding aerospace applications and emerging high-temperature industrial uses. YSZ coatings demonstrate exceptional thermal insulation properties with thermal conductivity of approximately 2 W/m·K, enabling reduction of metal substrate temperatures by 150-200°C in gas turbine applications while maintaining mechanical integrity at operating temperatures exceeding 1200°C. The aerospace industry is increasingly adopting advanced multilayer YSZ coating systems using detonation spraying and atmospheric plasma spraying, thereby achieving enhanced thermal shock resistance and oxidation protection.

Composite YSZ ceramic thermal barrier coatings (TBCs) deliver superior thermal diffivity (0.340-0.46 mm²/s), balancing strength and thermal insulation properties essential for modern jet engine development and advanced propulsion systems. Emerging aerospace engine developments and hypersonic vehicle programs represent substantial growth opportunities for YSZ thermal barrier coating manufacturers. The global focus on fuel efficiency and extended component service life supports sustained investment in advanced thermal protection systems, positioning specialty ceramic insulation coatings as high-value growth segments.

Nano-Coating Technology and Multifunctional Coating Innovation Opportunities

Advanced nano-coating technologies incorporating nanotechnology principles represent significant innovation opportunities enabling the development of multifunctional insulation coatings combining thermal insulation with self-cleaning, antimicrobial, fire-resistance, and corrosion-protection properties. Research initiatives developing hollow glass microsphere-enhanced coatings, nano-silica particle integration, and advanced polymer matrices are enabling the development of ultra-thin coatings delivering thermal performance equivalent or superior to traditional insulation materials while minimizing application thickness and installation complexity.

Innovative nano-coating formulations are projected to transform market applications, enabling deployment in space-constrained industrial environments, equipment insulation scenarios requiring maintenance accessibility, and architectural applications demanding aesthetic integration with building design. Manufacturing facilities increasingly recognize the value of preventing corrosion under insulation (CUI) through insulation-coating technology, thereby removing equipment from intensive CUI inspection programs and mitigating lifetime corrosion-exposure risks. The convergence of advances in nanotechnology, integration of multifunctional properties, and emerging industrial applications positions the nano-coating segment for robust growth through 2033.

Category-wise Analysis

Product Type Insights

Acrylic insulation coatings constitute the leading product segment, commanding approximately 42% of the market, driven by their versatility, broad temperature-range compatibility, environmental advantages, and cost-effectiveness relative to specialty coating chemistries. Waterborne acrylic formulations, including Intertherm 3350 technology, demonstrate exceptional thin-film insulation performance suitable for substrates operating up to 177°C (350°F), combining superior thermal insulation characteristics with easy spray application, enabling on-site application to operating equipment.

Acrylic coatings offer significant advantages, including a seamless, adherent film that enables removal of affected equipment from CUI inspection protocols, minimization of facility corrosion exposure, and elimination of the complexity of handling and installing traditional insulation materials. The dominance of acrylic coating reflects established manufacturing infrastructure, proven performance across diverse industrial applications, and compatibility with both water-based and solvent-based formulation approaches, addressing diverse regulatory environments. Emerging acrylic nano-coating formulations incorporating hollow glass microspheres and nano-silica particles are expanding performance capabilities while maintaining cost-effectiveness advantages, sustaining market leadership through the forecast period.

Base Type Analysis

Water-based insulation coatings represent the fastest-growing segment, projected to expand at approximately 6.8% CAGR and capture more than 50% of global market share by 2033. The segment's rapid expansion reflects stringent environmental regulations that restrict volatile organic compound (VOC) emissions, growing consumer demand for sustainable products, and regulatory mandates that promote the adoption of low-VOC coating systems. Water-based formulations offer distinct advantages, including the ability to be applied to hot surfaces without an ignition hazard, enabling application to operating equipment; substantially lower VOC emissions than solvent-based alternatives; and improved environmental compliance, positioning manufacturers favorably in regulated markets.

Global regulatory emphasis on VOC reduction, combined with consumer preference for environmentally friendly products and industrial compliance requirements, positions water-based coatings as the dominant future segment. The segment benefits from continuous technological advancement in water-based resin systems, improved performance characteristics, and expanding infrastructure supporting water-based coating manufacturing and application across diverse industrial regions.

Industry Insights

The manufacturing sector is the dominant end-use industry, accounting for approximately 38% of insulation paint and coating demand, driven by extensive use in thermal management, corrosion prevention, and equipment protection across industrial operations. Manufacturing facilities use insulation coatings to control temperature on process equipment, conserve energy by reducing heat loss, and prevent corrosion under insulation (CUI) on piping, vessels, and critical infrastructure. Industrial applications emphasize thermal insulation performance, fire resistance properties, and corrosion protection, with manufacturers increasingly adopting insulation coating solutions addressing multiple performance requirements simultaneously.

China's manufacturing sector, which accounts for one-third of national GDP, drives substantial domestic demand for thermal insulation coatings that provide corrosion resistance and fire resistance, thereby enhancing industrial facility safety. The manufacturing sector's dominance reflects established adoption patterns, validated performance across diverse applications, and the integration of insulation coatings into standard industrial maintenance and energy conservation practices.

Regional Insights

North America Insulation Paints and Coatings Market Trends

North America accounts for approximately 28.6% of global insulation paints and coatings demand, with substantial market activity driven by stringent environmental regulations, mature commercial and industrial infrastructure, and significant investment in building renovation and modernization. The U.S. market leads regional demand, supported by federal energy efficiency initiatives including the Inflation Reduction Act, state-level energy conservation programs, and widespread adoption of LEED certification standards requiring advanced building envelope performance. Commercial building development and industrial facility modernization continue to drive demand for thermal management solutions that address energy efficiency objectives and reduce operational costs.

The energy-efficient buildings market in North America is expanding rapidly, with investments in green infrastructure and sustainable building technologies accelerating following federal policy implementation. The region's advanced industrial infrastructure, automotive sector expansion, and commercial real estate development generate sustained demand for insulation coatings that address energy-efficiency mandates and sustainability objectives. Strategic positioning by leading manufacturers, including Sherwin-Williams and PPG, with advanced insulation-coating portfolios supports continued regional market expansion.

Europe Insulation Paints and Coatings Market Trends

Europe is a major market with stringent environmental regulations and a strong focus on sustainability, driving adoption of advanced insulation coatings across the building and industrial sectors. The EU Energy Performance of Buildings Directive (EPBD), May 2024, establishes progressively stricter energy-efficiency requirements, mandating zero-emission buildings by 2030 and driving substantial investment in advanced building-envelope materials, including thermal-insulation coatings.

Germany, France, the United Kingdom, and Spain lead European market activity driven by regulatory harmonization, established supply chains, and commitment to climate neutrality. The European Union's focus on achieving carbon neutrality by 2050, combined with EPBD implementation, creates sustained regulatory drivers for the adoption of energy-efficient building materials. Manufacturers, including Akzo Nobel and Nippon Paint, maintain a significant European presence, supporting continued market expansion aligned with evolving regulatory requirements and sustainability initiatives.

Asia Pacific Insulation Paints and Coatings Trends

Asia Pacific represents the fastest-growing regional market, with East Asia accounting for 36.5% of the global market share, driven by substantial construction activity, manufacturing sector expansion, and emerging energy efficiency consciousness. India's emerging construction market and manufacturing sector expansion are creating increasing demand for thermal insulation coating,s supporting energy efficiency objectives.

Japan and South Korea focus on innovation and the adoption of advanced coating technologies, with climate challenges driving demand for weather-resistant and thermal management solutions. The region's manufacturing advantages, cost-effective production capabilities, and expanding construction activity position the Asia-Pacific region as the fastest-growing market, supporting global insulation coating market expansion through 2033.

Competitive Landscape

The insulation paints and coatings market exhibits moderate consolidation, with leading global manufacturers including Akzo Nobel, PPG Industries, Sherwin-Williams, Nippon Paint Holdings, and BASF SE capturing significant market share through vertically integrated production, extensive research and development infrastructure, and global distribution networks. The market combines established multinational companies with specialized regional manufacturers focusing on niche applications and geographic markets. Market leaders employ strategies emphasizing sustainability, advanced coating technologies including nano-coating and ceramic formulations, and application-specific product development supporting diverse industrial end-uses. Companies invest substantially in research and development targeting advanced thermal barrier coatings, multifunctional coating formulations, and environmentally compliant systems addressing evolving regulatory requirements.

Key Developments:

- In December 2024, PPG Industries Advances Sustainable Insulation Coating Portfolio - PPG Industries announced investment in advanced insulation coating formulations as part of sustainability strategy targeting 50% of sales from sustainably advantaged solutions by 2030, with focus on low-VOC and bio-based coating chemistry development.

- In September 2024, Akzo Nobel Expands YSZ Thermal Barrier Coating Production - Akzo Nobel announced expansion of advanced ceramic thermal barrier coating capacity for aerospace applications, including multilayer YSZ coating systems utilizing atmospheric plasma spraying technology for enhanced thermal performance.

- In June 2024, Nippon Paint Launches Nano-Enhanced Insulation Coating Technology - Nippon Paint Holdings Co. introduced advanced nano-silica particle-enhanced insulation coatings delivering superior thermal resistance and multifunctional properties, targeting manufacturing and industrial maintenance markets with innovative performance characteristics.

Companies Covered in Insulation Paints and Coatings Market

- Akzo Nobel

- Shewrin Williams

- PPG

- Hy-Tech Thermal Solutions

- Highland International

- Okitsumo Inc.

- NISSIN SANGYO CO., LTD.

- Industrial Nanotech, Inc.

- Insuladd Environmental Products Ltd

- Thermilate Roof and Wall Coatings Ltd.

- Kansai Paint Co. Ltd

- Nippon Paint Holdings Co., Ltd.

- Isonem Paint & Insulation Technologies

- Prolat S. Dimopoulos & Co. E.E.

- Thermilate Technologies Ltd.

Frequently Asked Questions

The global insulation paints and coatings market is projected to reach US$ 12.3 billion by 2033 from US$ 8.1 billion in 2026, representing a compound annual growth rate (CAGR) of 6.2% during the forecast period.

Primary demand drivers include stringent energy efficiency regulations including the EU Energy Performance of Buildings Directive (EPBD) mandating zero-emission buildings by 2030, substantial construction activity and infrastructure investment in emerging markets.

Water-based insulation coatings represent the fastest-growing product segment, expanding at approximately 6.8% CAGR, driven by stringent VOC emissions regulations, consumer preference for environmentally sustainable products, and regulatory mandates restricting solvent-based formulations.

Asia Pacific maintains the largest regional market share at approximately 36.5%, supported by rapid urbanization, manufacturing sector expansion, government energy efficiency initiatives, and substantial infrastructure development across emerging economies.

Primary opportunities include aerospace and high-temperature application expansion with advanced yttria-stabilized zirconia (YSZ) thermal barrier coatings achieving thermal insulation at temperatures exceeding 1200°C.

Key market players include Akzo Nobel N.V., PPG Industries Inc., The Sherwin-Williams Company, Nippon Paint Holdings Co., Ltd., Kansai Paint Co., Ltd., BASF SE, Jotun Group, Hy-Tech Thermal Solutions, and Okitsumo Inc.