- Pharmaceuticals

- Immune Checkpoint Inhibitors Market

Immune Checkpoint Inhibitors Market Size, Trends, Share, Growth, and Regional Forecast, 2025 to 2032

Immune Checkpoint Inhibitors Market by Drug Type (PD-1 Inhibitor, PD-L1 Inhibitor, and CTLA-4 Inhibitor), by Indication (Non-Small Cell Lung Cancer, Melanoma, Colorectal Cancer, and Others), by Distribution Channel (Hospital Pharmacies, Retail Pharmacies, and Online Pharmacies), and Regional Analysis from 2025 to 2032

Immune Checkpoint Inhibitors Market Share and Trends Analysis

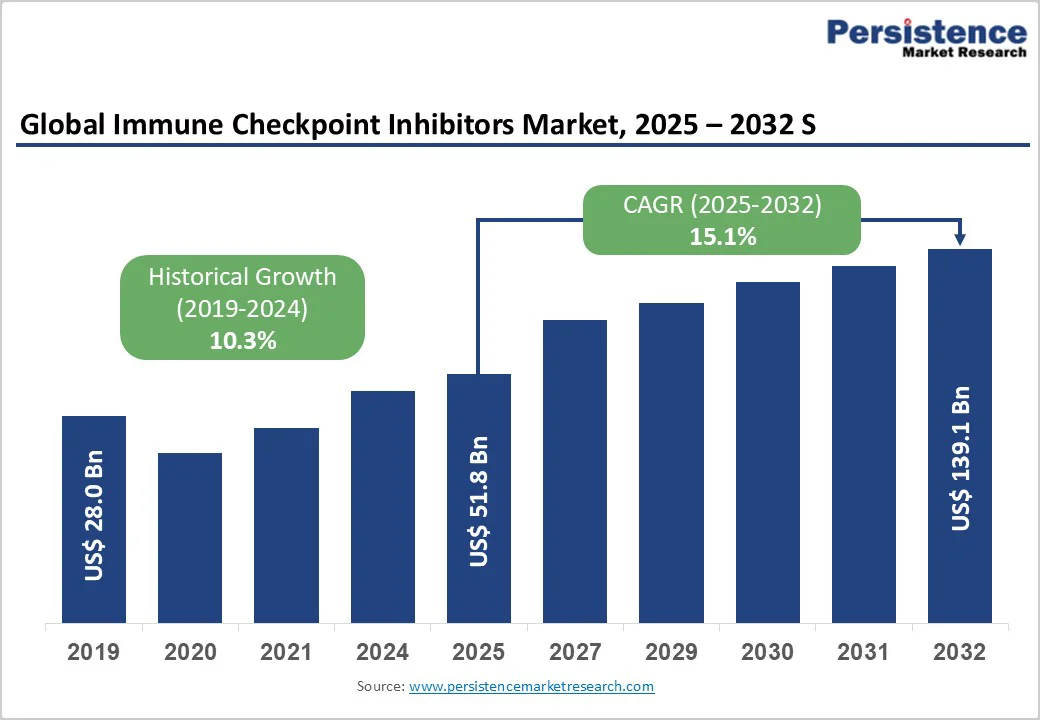

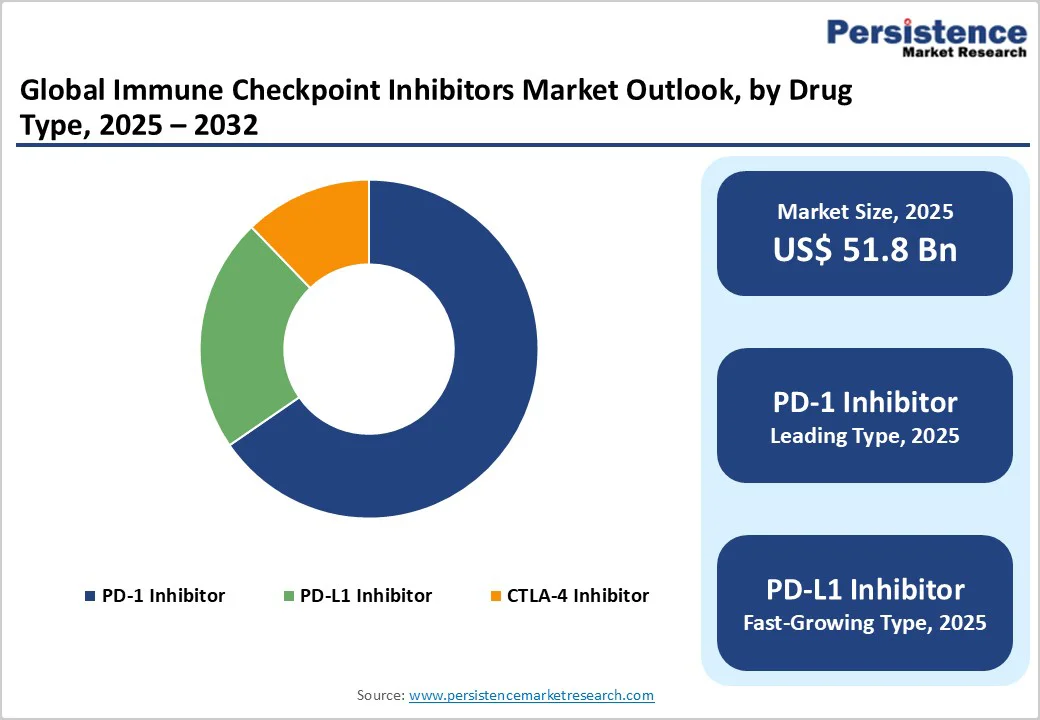

The global immune checkpoint inhibitors market size is valued at US$51.8 billion in 2025 and projected to reach US$139.1 billion by 2032, growing at a CAGR of 15.1% during the forecast period from 2025 to 2032.

Global demand for immune checkpoint inhibitors (ICIs) is increasing as awareness of advanced immunotherapy options and early cancer diagnosis grows across hospitals, oncology centers, and research institutions.

Rising emphasis on long-term survival outcomes, treatment precision, and the effectiveness of combination therapy is driving widespread adoption of ICIs across multiple cancer types. Moreover, expanding healthcare infrastructure, growing cancer incidence, and increasing government and private investments in oncology research and treatment access, especially in emerging markets, are further boosting market growth.

Key Industry Highlights

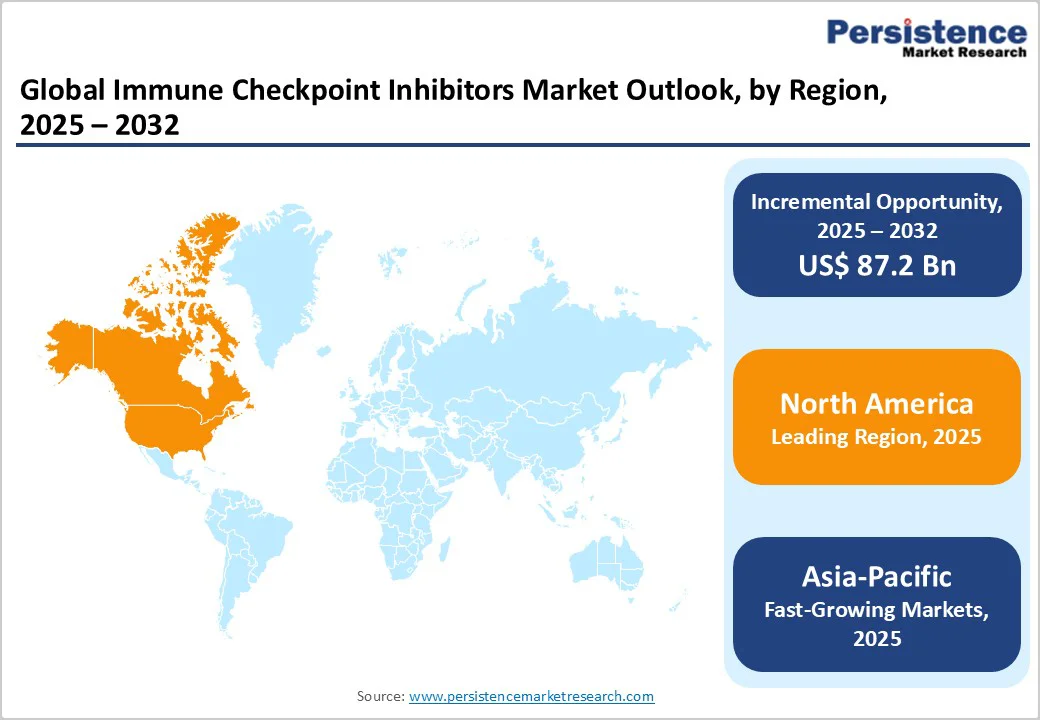

- Leading Region: North America leads globally with 39.5% share, driven by strong oncology research infrastructure, favorable reimbursement frameworks, and the presence of leading immuno-oncology players such as Merck & Co., Bristol Myers Squibb, and Pfizer.

- Fastest-Growing Region: Asia Pacific is the fastest-growing region, driven by rising cancer incidence, increased healthcare investments, and greater access to advanced immunotherapies across China, Japan, and India.

- Leading Type Category: The PD-1 inhibitors segment leads with a 65.4% share in 2025, supported by the clinical success and broad indications of drugs such as Keytruda (pembrolizumab) and Opdivo (nivolumab) across multiple tumor types.

- Fastest-Growing Type Category: PD-L1 inhibitors are the fastest-growing segment, driven by expanding regulatory approvals, new subcutaneous formulations, and increasing adoption in lung, bladder, and breast cancers.

- Leading Application Category: Non-small cell lung cancer (NSCLC) remains the leading application segment, accounting for 32.4% of global revenue, owing to its high disease burden and widespread use of ICIs as first-line and combination therapies.

- Fastest-Growing Application Category: The melanoma segment is the fastest-growing due to the strong clinical efficacy of immune checkpoint inhibitors (ICIs) in improving survival rates for advanced and metastatic cases.

- Increasing adoption of PD-1 and CTLA-4 inhibitors such as nivolumab, pembrolizumab, and ipilimumab, along with expanding adjuvant and combination therapy approvals, further supports segment growth.

| Global Market Attributes | Key Insights |

|---|---|

| Immune Checkpoint Inhibitors Market Size (2025E) | US 51.8 Bn |

| Market Value Forecast (2032F) | US$139.1 Bn |

| Projected Growth (CAGR 2025 to 2032) | 15.1% |

| Historical Market Growth (CAGR 2019 to 2024) | 10.3% |

Market Dynamics

Driver - Increasing Use of Combination Therapies and Rising Cancer Incidence Globally

The integration of immune checkpoint inhibitors (ICIs) with targeted therapies, chemotherapy, cancer vaccines, and radiotherapy is significantly improving treatment outcomes across multiple tumor types, which is driving market growth.

Additionally, biomarker-driven personalization using PD-L1 expression, microsatellite instability (MSI), and tumor mutational burden (TMB) enhances patient selection, optimizes therapeutic efficacy, and broadens the eligible patient population. This growing emphasis on tailored and combination immunotherapies is a major driver accelerating the global adoption of immune checkpoint inhibitors (ICIs).

For instance, an April 2024 study published in the International Journal of Radiation Oncology reported that the addition of radiotherapy (RT) to ICI and anti-angiogenic therapy markedly improved disease control rate (DCR) and survival outcomes in patients with advanced-stage hepatocellular carcinoma (HCC), while maintaining a satisfactory safety profile.

The increasing global prevalence of cancer remains a major factor driving the demand for immune checkpoint inhibitors (ICIs). For instance, according to the World Health Organization (WHO), over 35 billion new cancer cases are projected by 2050, representing a 77% increase from an estimated 20 billion cases in 2022.

This surge is primarily attributed to aging populations, lifestyle-related factors, and environmental exposures. The rising incidence of solid tumors such as lung, colorectal, and melanoma has intensified the need for effective and durable treatment options. ICIs have emerged as a preferred therapeutic class due to their potential to deliver long-term survival benefits and long-lasting immune responses across multiple cancer types.

Restraints - Immune-Related Adverse Events (irAEs) and Variability of Response

Despite their clinical success, immune checkpoint inhibitors (ICIs) are associated with a significant risk of immune-related adverse events (irAEs) such as colitis, pneumonitis, hepatitis, dermatitis, and endocrinopathies, which can range from mild to life-threatening. These toxicities often require immunosuppressive management, hospitalization, or discontinuation of therapy, increasing the overall treatment burden.

Furthermore, response rates to ICIs remain variable, with only a subset of patients achieving durable benefit, largely due to tumor heterogeneity, immune-evasion mechanisms, and the lack of predictive biomarkers. This variability in efficacy and safety profile limits broader clinical adoption and affects patient and physician confidence in immunotherapy.

Opportunity - Expanding Regulatory Approvals and Increasing Clinical Pipeline

Regulatory bodies worldwide are approving immune checkpoint inhibitors (ICIs) for an increasing number of cancer indications, expanding the overall patient base. Leading ICIs such as pembrolizumab, nivolumab, and atezolizumab have gained multiple label extensions across NSCLC, melanoma, urothelial, and head and neck cancers.

For instance, in September 2025, Merck received U.S. FDA approval for KEYTRUDA QLEX™ (pembrolizumab and berahyaluronidase alfa-pmph), a subcutaneous formulation for adults across 38 solid tumor indications previously approved for intravenous KEYTRUDA®.

Berahyaluronidase alfa, developed by Alteogen Inc., enables faster subcutaneous delivery, enhancing patient convenience and clinical efficiency. The launch of KEYTRUDA QLEX marks a significant innovation in immuno-oncology administration.

A large pipeline of ongoing clinical trials is evaluating immune checkpoint inhibitors (ICIs) across new tumor types and earlier stages of therapy, representing a significant growth opportunity. Numerous phase II and III studies are investigating their efficacy in cancers such as gastric, ovarian, prostate, and pancreatic cancers, as well as in adjuvant and neoadjuvant settings.

These trials aim to expand clinical indications, improve overall survival outcomes, and establish ICIs as part of standard treatment regimens. Successful trial outcomes are expected to accelerate regulatory approvals, enhance market adoption, and solidify ICIs’ position in next-generation cancer immunotherapy.

Category-wise Analysis

By Type, PD-1 Dominate Globally Due to their Broad Clinical Efficacy, Multiple Regulatory Approvals, and Strong Adoption across Diverse Cancer Indications

The PD-1segment is projected to lead the global immune checkpoint inhibitors market with 65.4% in 2025. The segment’s strong performance is driven by the broad clinical efficacy of PD-1 inhibitors across multiple tumor types, including non-small cell lung cancer (NSCLC), melanoma, renal cell carcinoma, and urothelial cancers, making them a preferred choice in oncology therapy.

PD-1 inhibitors also have a favorable safety profile compared to other checkpoint pathways, enhancing patient compliance and long-term treatment outcomes.

The availability of leading PD-1 drugs, such as pembrolizumab, nivolumab, and cemiplimab, which have received multiple regulatory approvals across major markets, including the U.S., Europe, and Asia-Pacific. Expanding indications for these drugs, supported by ongoing clinical trials demonstrating efficacy in additional cancer types and combination therapies, are fueling broader adoption.

By Application, Non-Small Cell Lung Cancer Dominates Due to High Global Prevalence, Established Use of Immune Checkpoint Inhibitors as First-Line Therapy

The non-small cell lung cancer segment is expected to dominate the global immune checkpoint inhibitors market in 2025 with a revenue share of 32.4%. This is due to its high prevalence of lung cancer, coupled with the proven clinical efficacy of ICIs such as pembrolizumab, nivolumab, and atezolizumab in both first-line and advanced NSCLC settings.

For instance, in 2023, according to the Lung Cancer Association, close to 238,000 people were diagnosed with lung cancer in the United States, with the rate of new cases varying by state. This rising disease burden underscores the growing demand for effective and durable treatment options, further boosting the adoption of immune checkpoint inhibitors (ICIs) in NSCLC management.

Additionally, early adoption of immunotherapy, favorable reimbursement policies, and ongoing label expansions for combination regimens.

By Distribution Channel, Hospital Pharmacies Segment Leads Due to Their Central Role in Administering Intravenous Immune Checkpoint Inhibitors, and Specialized Oncology Infrastructure

The hospital pharmacies segment is projected to account for 72.4% of the global immune checkpoint inhibitors market in 2025, owing to its central role in administering advanced oncology treatments and ensuring proper handling of high-cost biologics. Most ICIs, including pembrolizumab and nivolumab, require intravenous administration under medical supervision, making hospitals the primary point of care.

Additionally, the presence of specialized oncology units, trained healthcare professionals, and favorable reimbursement systems enhances treatment accessibility and patient safety. The growing number of hospital-based cancer centers and the increasing adoption of combination immunotherapy regimens further reinforce the segment’s market dominance.

Region-wise Insights

North America Immune Checkpoint Inhibitors Market Trends

The North America market is expected to dominate globally with a value share of 39.5% in the 2025, with the U.S. leading the region. This dominance is due to high cancer burden, particularly in lung, melanoma, renal cell, and urothelial cancers, which drives the demand for advanced immunotherapies.

The region benefits from a well-established healthcare infrastructure, favorable reimbursement policies, and widespread availability of immuno-oncology therapies across major hospitals and cancer centers.

Moreover, the early regulatory approvals by the U.S. FDA, such as for keytruda®, opdivo®, and tecentriq®, have accelerated clinical adoption. The active participation of biopharmaceutical companies such as Merck, Bristol Myers Squibb, and Regeneron in developing next-generation checkpoint inhibitors further drives growth in the region's immune checkpoint inhibitors market.

Europe Immune Checkpoint Inhibitors Market Trends

The European market is projected to experience steady growth, supported by rising cancer incidence, expanding access to innovative immunotherapies, and strong healthcare infrastructure across major countries such as Germany, the U.K., France, and Italy. Growing adoption of PD-1 and PD-L1 inhibitors in both first-line and combination therapies is driving regional market expansion.

Moreover, the European Medicines Agency (EMA) has accelerated approvals for multiple ICIs, including nivolumab, pembrolizumab, and durvalumab, across diverse cancer types. For instance, in May 2025, Bristol Myers Squibb received European Commission (EC) approval for a new subcutaneous formulation of Opdivo® (nivolumab).

This version, known as Opdivo SC, combines nivolumab with recombinant human hyaluronidase (rHuPH20) and is available as a 600 mg/vial solution for injection. It has been approved for use across multiple adult solid tumors, both as monotherapy and in combination regimens including maintenance therapy following intravenous nivolumab plus Yervoy® (ipilimumab) or alongside chemotherapy or cabozantinib.

This approval enhances patient convenience and broadens clinical accessibility of ICIs in Europe.

Asia and Pacific Immune Checkpoint Inhibitors Market Trends

The Asia Pacific market is expected to register a relatively higher CAGR of around 20.0% between 2025 and 2032, driven by the rising cancer prevalence, improving healthcare infrastructure, and growing adoption of advanced immunotherapies in countries such as China, Japan, India, and South Korea. Increasing government healthcare spending, expanding clinical trial activity, and accelerated regulatory approvals are further fueling regional growth.

Moreover, partnerships between global pharmaceutical companies and local biotech firms are enhancing drug accessibility and fostering innovation in immune-oncology therapeutics. The rising presence of biosimilar ICIs and favorable reimbursement reforms in emerging markets is also expected to boost long-term market expansion.

Competitive Landscape

The global immune checkpoint inhibitors market is highly competitive, with major players such as Sanofi, F. Hoffmann-La Roche Ltd., Merck & Co., Bristol-Myers Squibb Company, Regeneron Pharmaceuticals Inc., and AstraZeneca PLC dominating through continuous innovation, extensive clinical research, and strong regulatory and commercialization strategies.

Major companies are investing heavily in the development of next-generation ICIs and novel combinations with targeted therapies, radiotherapy, and cancer vaccines to enhance treatment efficacy. Strategic alliances, co-development agreements, and regional expansions are also key approaches used to strengthen their global footprint.

Key Industry Developments:

- In March 2025, Biond Biologics Ltd. announced it will regain full global rights to its novel immune checkpoint inhibitor BND-22 (also known as SAR444881) from Sanofi. BND-22 is a humanised IgG4 antibody targeting the ILT2 receptor and is being evaluated in solid tumour indications such as cholangiocarcinoma, non-small cell lung cancer, and colorectal cancer.

- In December 2024, the U.S. Food and Drug Administration (FDA) approved Cosibelimab-ipdl (Unloxcyt) developed by Checkpoint Therapeutics, Inc., as a programmed death ligand-1 (PD-L1) blocking antibody for adults with metastatic cutaneous squamous cell carcinoma (mCSCC) or locally advanced CSCC (laCSCC) who are not eligible for curative surgery or radiation therapy. This approval expands the therapeutic landscape for PD-L1 inhibitors in advanced skin cancers.

- In June 2024, RedHill Biopharma Ltd. announced that it received a Chinese patent notice of allowance for Opaganib in combination with immune checkpoint inhibitors (ICIs) as a novel method to induce an anti-cancer immune response. The patent, to be issued by the Chinese National Intellectual Property Administration (CNIPA), provides protection for Opaganib’s potential use alongside approved and investigational ICIs across multiple cancer indications through 2040.

Companies Covered in Immune Checkpoint Inhibitors Market

- Sanofi

- F. Hoffmann-La Roche Ltd.

- Merck & Co.

- Bristol-Myers Squibb Company

- Regeneron Pharmaceuticals Inc.

- AstraZeneca PLC

- Shanghai Jhunsi Biosciences Ltd

- Immutep.

- BeOne Medicines

- GSK plc.

- HCW Biologics, Inc.

- Novocure GmbH

- Biond Biologics

- Others

Frequently Asked Questions

The global immune checkpoint inhibitors market is projected to be valued at US$ 51.8 Bn in 2025.

Rising global cancer burden and growing adoption of immuno-oncology therapies offering durable survival benefits are driving immune checkpoint inhibitors market growth.

The global immune checkpoint inhibitors market is poised to witness a CAGR of 15.1% between 2025 and 2032.

Expanding approvals across new tumor types and earlier treatment lines, along with advancements in subcutaneous formulations and next-generation combination therapies. Increasing R&D investments and collaborations are creating significant opportunities in the market.

Sanofi, F. Hoffmann-La Roche Ltd., Merck & Co., Bristol-Myers Squibb Company, Regeneron Pharmaceuticals Inc., and AstraZeneca PLC are the key players in the market.