- Pharmaceuticals

- Erleada Market

Erleada Market Size, Share, and Growth Forecast 2026 - 2033

Erleada Market by Product Type (Branded, Generic), Indication (Metastatic Castration-Resistant Prostate Cancer, Non-Metastatic Castration-Resistant Prostate Cancer), Distribution Channel, End-user, and Regional Analysis, 2026 - 2033

Erleada Market Size and Trend Analysis

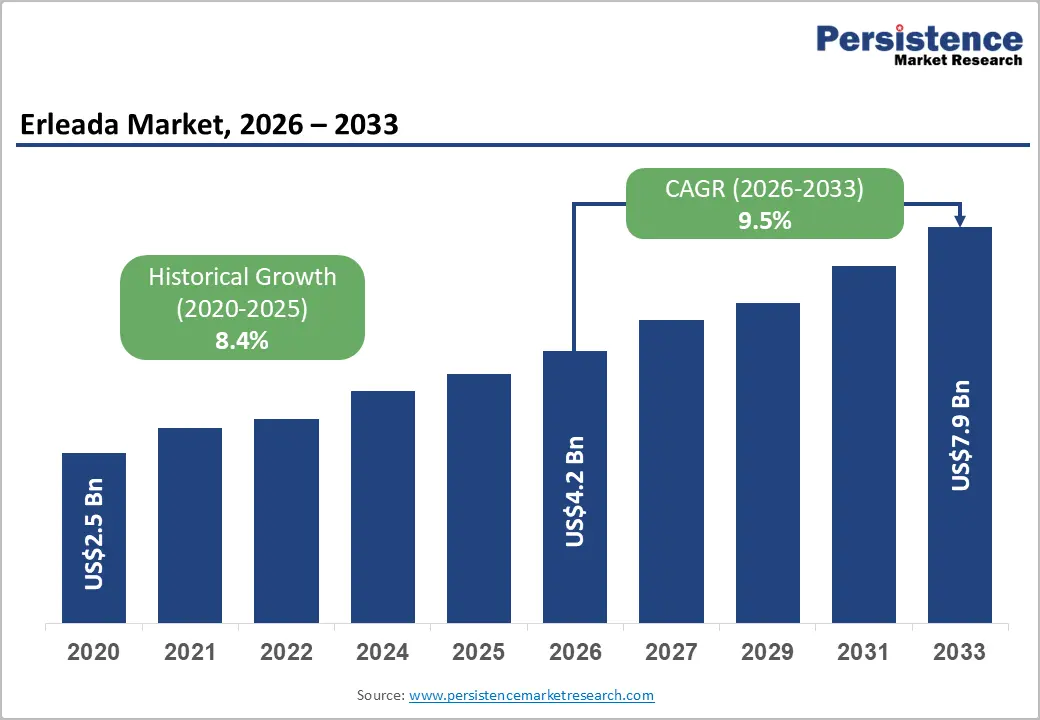

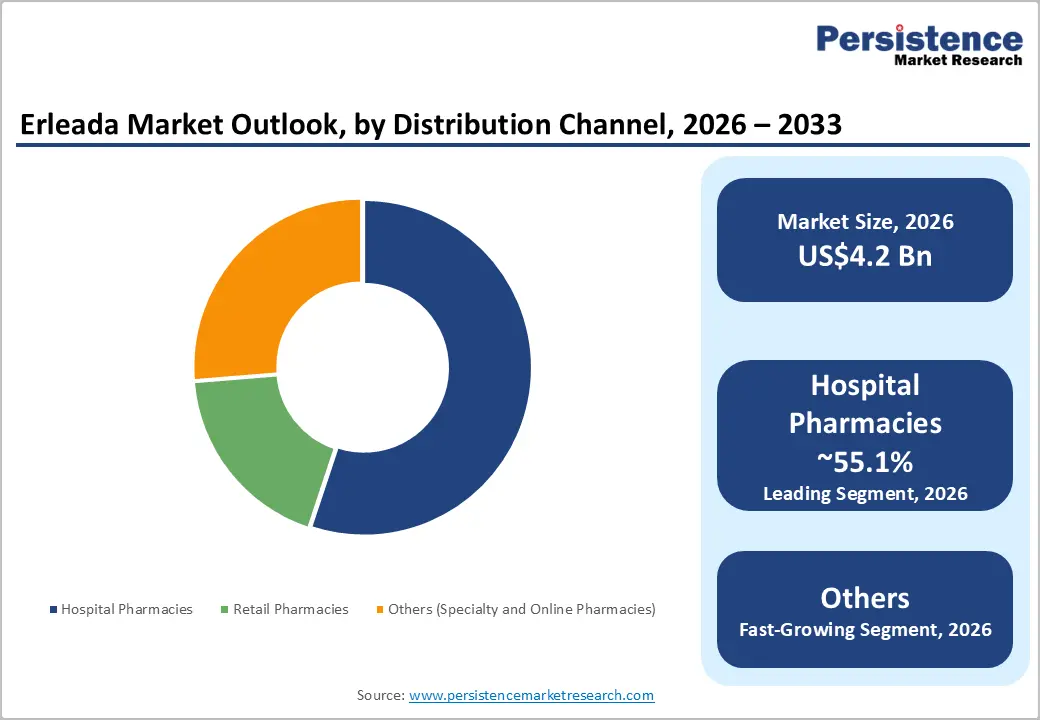

The global erleada market size is likely to be valued at US$4.2 billion in 2026 and is expected to reach US$7.9 billion by 2033, surging at a CAGR of 9.5% during the forecast period from 2026 to 2033, driven by the rising incidence of prostate cancer, increasing adoption of androgen receptor inhibitors in early stages of treatment, and strong clinical evidence supporting apalutamide-based therapies. Growth is further supported by surging awareness of advanced prostate cancer management.

Key Industry Highlights:

- Fast Track Approval: In March 2025, Zydus Lifesciences received final approval from the U.S. FDA to manufacture and market apalutamide tablets, 60 mg, which is a generic equivalent of Erleada, at its Special Economic Zone facility in Ahmedabad, India. However, the commercial launch remains subject to patent-related constraints surrounding Erleada.

- Leading Product Type: Branded products, approximately 94.4% share in 2026, owing to strong clinical validation from Phase III trials.

- Dominant Distribution Channel: Hospital pharmacies, nearly 55.1% in 2026, as prostate cancer therapies require close clinical supervision and regular monitoring.

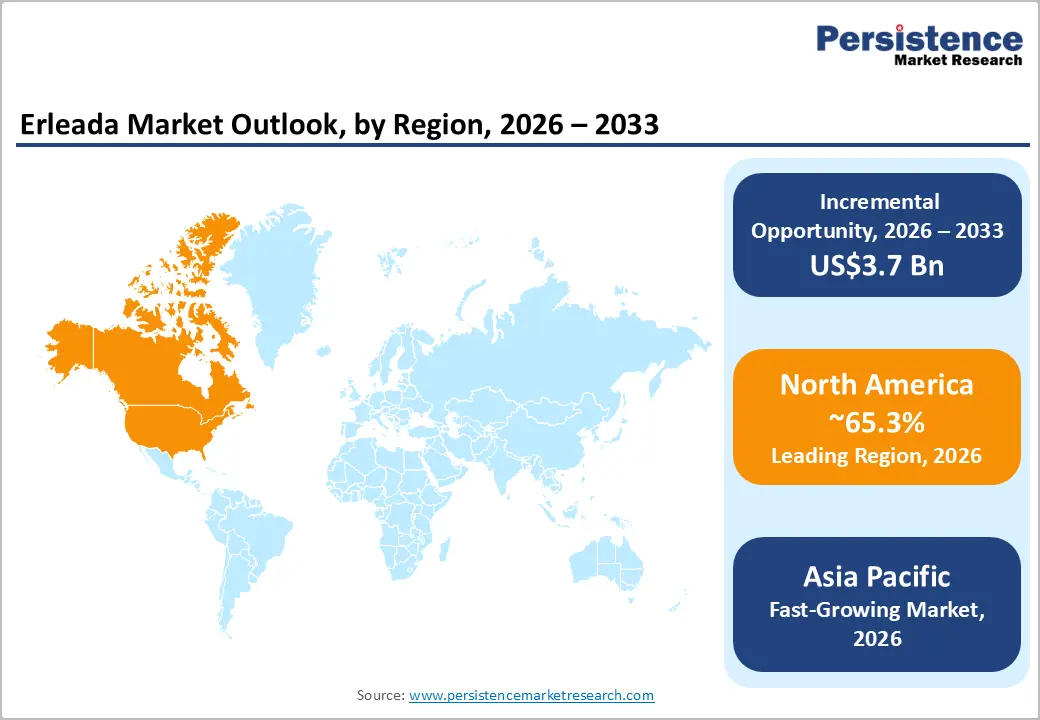

- Leading Region: North America, with about 65.3% share in 2026, spurred by high prostate cancer screening rates and early adoption of advanced androgen receptor inhibitors.

- Fast-growing Region: Asia Pacific, backed by rising prostate cancer incidence and surging access to oncology drugs.

DRO Analysis

Driver - Rising Prostate Cancer Diagnoses with Surging Old Male Population

Prostate cancer overwhelmingly affects older men, and the demographic math is working in Erleada's favor. Prostate cancer is most frequently diagnosed among men aged 65 to 74, with a median diagnosis age of 67. As this age group keeps rising globally, more patients will enter the treatment pipeline. Incidence of advanced prostate cancer is increasing rapidly in the U.S., a trend linked to both aging and wide Prostate-Specific Antigen (PSA)-based screening.

An estimated 299,010 new cases were projected for the U.S. in 2024 alone. Importantly, variations in prostate cancer incidence rates mainly reflect PSA screening use, which typically detects localized disease. Better screening translates to early diagnoses and long treatment windows. More eligible patients at early and treatable stages extend the pool directly addressable by Erleada.

Streamlined Payer Access to Support Fast Treatment Initiation

Reimbursement pathways for Erleada have matured considerably. United Healthcare, one of the largest U.S. insurers, has established a transparent prior authorization framework for Erleada, with approvals issued for 12-month durations across its indicated uses. This has helped in reducing the back-and-forth that typically delays specialty drug access. Johnson & Johnson has also published a dedicated reimbursement and access guide covering coding and payer-approval processes to support prescribers.

A case study by pharmacy benefit manager Prime Therapeutics demonstrated 90% faster payer response time through electronic prior authorization systems, a shift that benefits high-cost oral oncology drugs such as Erleada. National Comprehensive Cancer Network’s (NCCN) Category 1 designation for apalutamide in mCSPC further strengthens formulary placement, as payers routinely line up coverage criteria with NCCN guidance.

Restraint - Skeletal and Musculoskeletal Side Effects

Bone and muscle-related toxicities are a real clinical burden with Erleada, not just a label footnote. The SPARTAN trial showed approximately 12% of patients on apalutamide experienced fractures, compared to about 6% on placebo, a two-fold increase. The FDA prescribing information confirms that falls were significantly more common in elderly patients, occurring in 19% of patients aged 75 and above. This is a concerning figure given that it is precisely the demographic most likely to receive the drug.

Long-term therapy also carries a risk of osteoporosis, requiring additional monitoring and often bone-protective agents such as denosumab or zoledronic acid. This adds clinical complexity and treatment cost. The impact of combining ADT with ARPIs on bone quality remains unclear, and further research is required to understand the combined effects fully. Until clear bone-protective protocols are standardized, these risks can make oncologists more cautious with long treatment durations.

Opportunity - Role of Androgen Receptor Pathway Inhibitors Across Disease Stages

Androgen Receptor Pathway Inhibitors (ARPIs) are no longer reserved for late-stage disease, but they are moving earlier and broader. Over the last decade, ARPIs have been implemented progressively early in the natural history of prostate cancer, including in patients who have never received Androgen Deprivation Therapy (ADT) or are still responsive to it. Erleada is well-positioned in this shift.

The final TITAN analysis showed that apalutamide plus ADT reduced the risk of death by 35% versus ADT alone (HR 0.65; 95% CI, 0.53 to 0.79; P<0.0001), establishing superior OS data that support early prescribing. A 2026 real-world study also found a statistically significant 51% reduction in the risk of death for mCSPC patients initiated on Erleada versus darolutamide without docetaxel, strengthening its competitive edge. As the evidence base grows, Erleada stands to gain further uptake at early treatment lines.

Use of Combination Hormone Regimens in Advanced Prostate Cancer

The treatment paradigm has shifted firmly toward intensification. NCCN guidelines now recommend combination therapy as the standard of care for metastatic castration-sensitive prostate cancer, incorporating ADT with ARPIs and/or chemotherapy. Erleada is one of only four approved ARPIs supported in this framework. The updated NCCN guidelines (Version 1, 2026) recommend ADT in combination with apalutamide, abiraterone, enzalutamide, or darolutamide for patients with synchronous low-volume or oligometastatic disease.

There is also emerging interest in triplet therapy. High-risk or high-volume patients may benefit from triplet therapy combining ADT, an ARPI such as apalutamide, and docetaxel. As oncologists gradually move away from ADT monotherapy, Erleada's place in multi-drug regimens provides significant volume growth potential.

Category-wise Analysis

Product Type Insights

Branded products are predicted to lead with a share of approximately 94.4% in 2026, owing to strong clinical trust and long-term evidence. Oncologists rely on drugs that have proven survival benefits in large trials. Erleada gained acceptance after the SPARTAN and TITAN Phase III trials showed improvement in metastasis-free survival and overall survival. These studies were published in journals such as The New England Journal of Medicine, which increases physician confidence.

Approvals from the U.S. Food and Drug Administration (FDA) and European Medicines Agency (EMA) are based on strict data review. In cancer care, even small differences in outcomes matter, so doctors prefer sticking to the original branded drug with full safety data rather than switching early.

Generic products are estimated to be the fastest-growing segment in the forecast period, owing to cost pressure and fast regulatory approvals. Cancer treatment is expensive, and payers are pushing cost-effective alternatives. Governments are actively supporting generics. For example, the U.S. FDA accelerated approvals for oncology generics under its Drug Competition Action Plan. In 2025, Zydus Lifesciences received approval for generic apalutamide, which directly challenges branded therapies. In India, policies under the Central Drugs Standard Control Organization and schemes such as Jan Aushadhi promote low-cost medicines.

Distribution Channel Insights

Hospital pharmacies are anticipated to dominate with a share of nearly 55.1% in 2026, as prostate cancer treatment is closely managed in clinical settings. These drugs are not simple prescriptions. Patients require regular monitoring, PSA testing, and side-effect management. Most therapies are initiated in hospitals or cancer centers. Institutions associated with the National Cancer Institute highlight that novel prostate cancer treatment often follows multidisciplinary care models. This keeps drug dispensing within hospital systems.

The others segment is expected to remain in the second position in 2026. It includes specialty and online pharmacies. These are seeing steady growth, spurred by convenience and long-term therapy requirements. Patients with prostate cancer stay on therapy for years. Specialty pharmacies provide home delivery, adherence support, and counseling. Companies are building dedicated oncology distribution channels. For example, CVS Health and Walgreens Boots Alliance have extended specialty pharmacy services for oncology drugs. Online models also gained traction after COVID-19. Reports from the World Health Organization (WHO) showed increased digital health adoption globally.

Regional Insights

North America Erleada Market Trends

North America is expected to dominate in 2026 with a share of nearly 65.3%, backed by a high incidence of prostate cancer and a well-established healthcare infrastructure. The U.S. was Erleada's first approved market, giving it a multi-year head start in physician familiarity and prescribing culture. On top of that, Janssen's strong patent protection and established clinical reputation have allowed it to maintain leadership through targeted marketing and payer agreements, with formulation patents covering Erleada until 2038. This long runway keeps generic erosion at bay and sustains branded pricing power.

North America also benefits from a dense network of academic cancer centers, specialty pharmacies, and oncology practices where combination regimens are routinely initiated.

U.S. Erleada Market Trends

The U.S. market benefits from a rare combination, i.e., early FDA approval, dual-indication positioning, and superior guideline backing. Erleada's inclusion in major treatment guidelines has significantly spurred its adoption across both community and academic oncology settings. Its dual approval for nmCRPC and mCSPC is a key differentiator. It enables use at early disease stages, which means long treatment durations and broad patient eligibility. The 2024 NCCN Guidelines for Prostate Cancer were updated four times to integrate newly approved drugs and scientific data, keeping Erleada in active clinical conversation throughout the year.

Johnson & Johnson's patient support programs and reimbursement guides further reduce access friction for prescribers.

Asia Pacific Erleada Market Trends

Asia Pacific is anticipated to be the fastest-growing region in the forecast period, owing to aging demographics, rising screening rates, and improving drug access. The hormonal therapy segment's expansion in the region has been partly driven by the launch of Erleada in Japan. Japan, South Korea, and China are seeing steady adoption of next-generation androgen receptor inhibitors as their oncology infrastructure matures and Western treatment protocols become standard. Regulatory agencies across the region have also accelerated approvals for oncology drugs, reducing the lag time between U.S./EU launches and local availability.

Japan Erleada Market Trends

Japan's growth trajectory is associated with its demographic profile and a formal commitment to advancing prostate cancer treatment. The country has one of the fastest-growing elderly male populations in Asia Pacific, which is directly increasing demand for prostate cancer treatment. Erleada received approval from Japan's Ministry of Health, Labor and Welfare (MHLW) for the treatment of patients with metastatic prostate cancer. This MHLW approval, alongside those for enzalutamide and abiraterone, has helped establish ARPI-based regimens as the standard of care in Japan's mCSPC population.

India Erleada Market Trends

In India, the demand is rising, but affordability and access gaps are still holding back full uptake. Recent years have seen a shift toward proactive healthcare behavior, augmented by government health programs, NGO-led awareness campaigns, and private sector health initiatives. These are extending the pool of diagnosed patients who could be eligible for treatments such as Erleada. However, high treatment costs, limited accessibility in rural and semi-urban areas, and a lack of insurance penetration, as well as cancer-specific reimbursement support, continue to hinder widespread adoption.

Europe Erleada Market Trends

Europe’s growth is fueled by both regulatory approvals and rising clinical adoption. The European Commission granted marketing authorization for Erleada for use in metastatic hormone-sensitive prostate cancer in combination with ADT, building on its earlier approval for non-metastatic castration-resistant disease. The EMA has authorized Erleada for both castration-resistant disease at high risk of spreading and for hormone-sensitive metastatic prostate cancer, giving it a broad label that mirrors its U.S. positioning.

Germany Erleada Market Trends

Germany's market structure gives Erleada a favorable entry point but a complex long-term pricing environment. It is frequently the first market for new drug launches due to its initial free-pricing framework and automatic reimbursement upon product launch. Key oncologists have publicly endorsed the European approval of apalutamide as a significant step forward for patients with metastatic hormone-sensitive prostate cancer, reflecting strong clinician sentiment. A study using data from Germany's Robert Koch Institute projected the most pronounced increases in prostate cancer incidence among men aged 80 to 84 and 85+ by 2030. These age groups are most likely to receive ADT-based therapies such as Erleada.

U.K. Erleada Market Trends

In the U.K., Erleada faced initial pushback from the National Institute for Health and Care Excellence (NICE) due to pricing concerns, but the situation has since been resolved. NICE reversed its position after Janssen offered an improved discount, making Erleada an option for around 8,000 patients in England and Wales. It covered both hormone-relapsed non-metastatic and hormone-sensitive metastatic disease. NHS England has commissioned apalutamide as one of several innovative targeted prostate cancer therapies added in the past five years, alongside enzalutamide, darolutamide, and relugolix.

Competitive Landscape

The global Erleada market is highly consolidated, with Johnson & Johnson controlling the majority share through its Janssen Biotech unit. The company has built a superior competitive moat using long-term patent protection, broad oncology partnerships, and continuous label expansion in advanced prostate cancer treatment. Industry estimates suggest Janssen currently commands more than 80% of the branded Erleada landscape globally, making the segment heavily innovation-driven rather than price-driven.

Competition is centered around androgen receptor inhibitor therapies used in metastatic castration-sensitive prostate cancer (mCSPC) and non-metastatic castration-resistant prostate cancer (nmCRPC). The strongest rivals to Erleada include Xtandi from Astellas Pharma and Pfizer, Nubeqa from Bayer AG, and Zytiga, which is also marketed by Janssen. These therapies compete primarily on survival outcomes, safety profiles, combination therapy success, and physician familiarity rather than pricing alone.

Key Industry Developments:

- In May 2026, Johnson & Johnson announced that late-breaking Phase 3 PROTEUS data for Erleada (apalutamide) had been selected to open the ASCO Annual Meeting plenary session. It signals a potential paradigm shift for high-risk prostate cancer patients undergoing curative-intent radical prostatectomy.

- In January 2026, the REINFORCE trial (NCT07333066) was registered as a Phase 3 international, open-label, randomized study evaluating treatment intensification with docetaxel plus apalutamide in mHSPC patients who did not achieve a deep PSA response after initial treatment with apalutamide.

- In October 2025, Kairos Pharma presented interim safety and efficacy data from its Phase 2 trial of apalutamide and carotuximab at the European Society for Medical Oncology (ESMO) Congress in Berlin. The presentation was titled ‘Preliminary safety and clinical activity from a Phase 2 study of apalutamide and carotuximab in advanced, castration-resistant prostate cancer.’

Companies Covered in Erleada Market

- Zydus Lifesciences Limited

- Johnson & Johnson

- Pfizer Inc.

- Bayer AG

- Astellas Pharma Inc.

- Novartis AG

- AstraZeneca plc

- Merck & Co., Inc.

- Eli Lilly and Company

- Amgen Inc.

Frequently Asked Questions

The global Erleada market is projected to be valued at US$4.2 billion in 2026.

The Erleada market is expected to reach US$7.9 billion by 2033.

Key market trends include the expansion of Erleada into early treatment settings and rising competition from next-generation androgen receptor inhibitors.

Branded products are expected to be the leading product type with a share of nearly 94.4% in 2026, owing to continued trust among oncologists supported by approvals from the U.S. FDA.

The Erleada market is expected to grow at a CAGR of 9.5% from 2026 to 2033.

Zydus Lifesciences Limited, Johnson & Johnson, Pfizer Inc., and Bayer AG are a few key market players.