- Medical Devices

- Enteral Feeding Devices Market

Enteral Feeding Devices Market Size, Share and Growth Forecast, 2026 - 2033

Enteral Feeding Devices Market by Product Type (Enteral Feeding Pumps, Enteral Feeding Tubes, Others), Indication Type (Cancer Care, Neurological Disorders, Others), End-user (Hospitals, Others), and Regional Analysis for 2026 - 2033

Enteral Feeding Devices Market Share and Trends Analysis

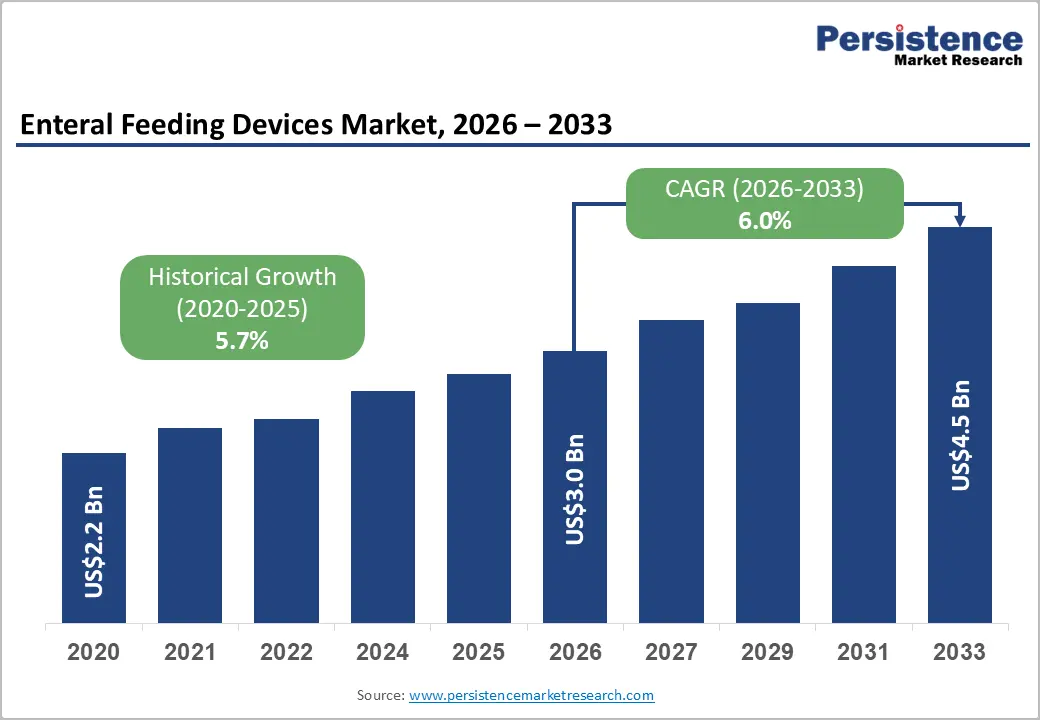

The global enteral feeding devices market size is likely to be valued at US$3.0 billion in 2026 and is projected to reach US$4.5 billion by 2033, growing at a CAGR of 6.0% during the forecast period from 2026 to 2033, driven by the rising prevalence of chronic diseases, the growing geriatric population, and the increasing demand for long-term nutritional support across hospitals and home care settings.

Demand for clinical nutrition device market solutions is increasing as healthcare providers prioritize patient recovery, ICU nutrition management, and post-surgical care. Technological advancements in the smart enteral feeding pump market, along with favorable reimbursement policies in developed economies, are accelerating adoption. In addition, expanding home healthcare infrastructure continues to strengthen growth across the home enteral nutrition market trends landscape.

Key Industry Highlights:

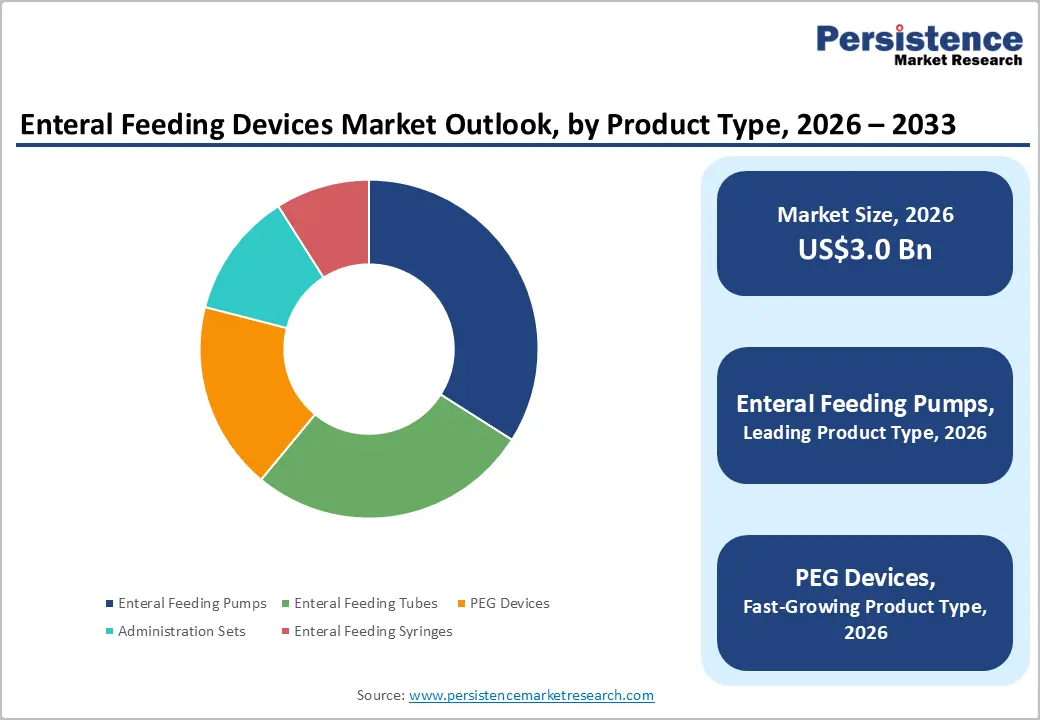

- Dominant Product Types: Enteral feeding pumps are set to account for nearly 34% of the market share in 2026, while PEG (Percutaneous Endoscopic Gastrostomy Devices) devices are projected to register the fastest growth through 2033, driven by rising long-term nutritional support demand.

- Leading Indications: Cancer care is expected to lead with approximately 31% share in 2026, while dysphagia is anticipated to witness the fastest growth through 2033 due to increasing neurological and age-related swallowing disorders.

- Dominant End-users: Hospitals are projected to dominate with nearly 46% revenue share in 2026, while home care settings are likely to record the fastest growth through 2033 amid rising home healthcare adoption.

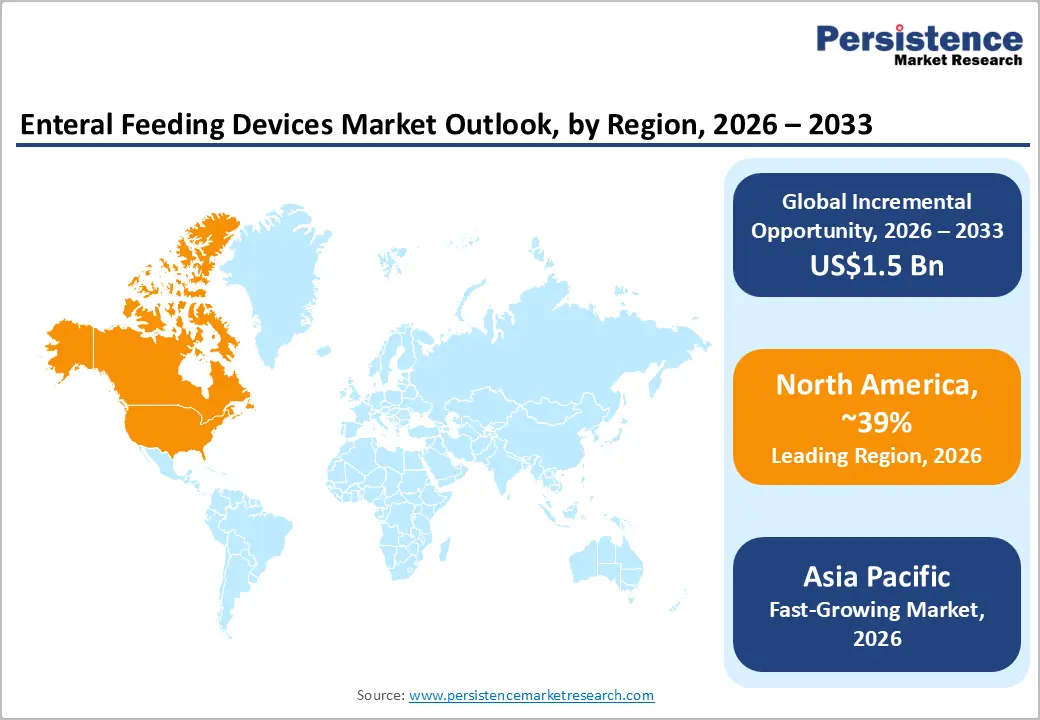

- Regional Leadership: North America is poised to lead with around 39% share in 2026, supported by advanced healthcare infrastructure, reimbursement support, and higher adoption of enteral nutrition technologies.

- Technology Trends: Smart monitoring systems, portable feeding devices, and automated dosage technologies are increasingly reshaping the smart enteral feeding pump market and broader enteral nutrition devices industry.

- Competitive Environment: Competitive activity is centered on product innovation, home healthcare expansion, strategic partnerships, and safety-focused enteral feeding system development.

DRO Analysis

Driver - Rising Prevalence of Chronic Diseases and an Aging Population Is Increasing Demand for Long-Term Nutritional Support

The growing incidence of cancer, neurological disorders, stroke-related complications, and gastrointestinal diseases is significantly increasing the requirement for enteral nutrition support globally. According to the World Health Organization (WHO), noncommunicable diseases account for nearly 74% of global deaths annually, while the global population aged 60 years and above is projected to reach 1.4 billion by 2030. Elderly patients are more vulnerable to dysphagia, malnutrition, and neurological impairments that require prolonged enteral feeding interventions.

In addition, the U.S. Centers for Disease Control and Prevention (CDC) reports that stroke remains a leading cause of long-term disability, driving demand for feeding support systems in rehabilitation and home care settings. These demographic and disease trends are directly strengthening the adoption of enteral feeding device market solutions across hospitals, rehabilitation centers, and long-term care facilities.

Restraint - High Device Costs and Risk of Feeding Complications Limit Adoption in Developing Economies

Despite strong demand, the market is constrained by high procurement and maintenance costs, along with the need for skilled clinical handling of enteral feeding systems. Advanced enteral feeding pumps and PEG devices require continuous monitoring, calibration, and trained staff, increasing operational burden for healthcare facilities.

According to the U.S. Food and Drug Administration (FDA), risks such as tube misconnection, infection, aspiration, and device malfunction necessitate strict compliance and monitoring. In low- and middle-income countries, limited reimbursement and budget constraints further restrict adoption, while raw material supply volatility continues to pressure the enteral nutrition devices industry.

Opportunity - Expansion of Home Healthcare and Remote Nutrition Management Creating Long-Term Growth Potential

The shift toward home-based care is creating strong opportunities in the home enteral nutrition market trends, supported by OECD-reported growth in long-term and home healthcare spending across developed economies. This is driving demand for portable, connected feeding systems with remote monitoring and automated control features in the smart enteral feeding pump market, while emerging economies continue expanding home care infrastructure.

In 2026, the U.S. FDA clearance of next-generation home-use enteral feeding systems and adoption of connector safety standards are improving safety and enabling wider deployment of enteral nutrition in non-hospital settings. These developments are accelerating the shift toward decentralized, digitally enabled enteral care delivery.

Category-wise Analysis

Product Type Insights

Enteral feeding pumps are expected to lead the market with nearly 34% share in 2026, driven by their critical role in ICU and acute care nutrition, where precision and safety are essential. These systems enable controlled, programmable feeding, reducing clinical errors and improving patient outcomes in high-dependency settings. Hospitals are increasingly adopting automated and connected solutions to enhance clinical efficiency and monitoring. This trend is supported by upgrades such as U.S. Veterans Health Administration ICU automation initiatives and Germany’s hospital digitalization programs integrating smart nutrition systems.

PEG devices are projected to be the fastest-growing segment through 2033, due to rising demand for long-term nutrition in patients with neurological disorders, cancer, and severe swallowing impairments. Their minimally invasive nature and improved safety profile are increasing acceptance for extended feeding support. Advancements in tube design and infection control are improving outcomes across clinical settings. Growth is reinforced by developments, including Japan’s expanded PEG adoption in geriatric care and NHS England’s community PEG programs, enabling earlier discharge.

Indication Type Insights

Cancer care is expected to dominate with approximately 31% share in 2026, driven by high nutritional needs in patients with head, neck, gastrointestinal, and esophageal cancers affecting swallowing function. Enteral feeding is widely used during chemotherapy and radiation therapy to maintain nutrition and improve treatment tolerance. Clinical guidelines strongly support early nutritional intervention in oncology care pathways. This is reinforced by initiatives such as the U.S. National Cancer Institute’s updated nutrition protocols and Europe’s expanded oncology nutrition support programs.

Dysphagia is projected to register the fastest CAGR through 2033, due to rising neurological conditions like stroke, Parkinson’s disease, and dementia affecting swallowing ability. Patients often require long-term enteral nutrition to prevent aspiration and malnutrition risks. Improved screening and early diagnosis are increasing intervention rates globally. This growth is supported by actions such as Australia’s mandatory dysphagia screening in stroke care and Japan’s updated rehabilitation guidelines promoting earlier feeding intervention.

End-user Insights

Hospitals are expected to lead with nearly 46% share in 2026, driven by ICU admissions, surgical recovery needs, and continuous nutritional monitoring in critical care. They remain the primary setting for enteral feeding due to advanced infrastructure and reimbursement support. Increasing automation in ICU nutrition systems is improving efficiency and patient outcomes. This dominance is reinforced by initiatives, including India’s ICU expansion under Ayushman Bharat and the U.K. NHS's standardized procurement of feeding systems.

Home care settings are projected to grow the fastest through 2033, as healthcare shifts toward decentralized, cost-effective care models. Patients increasingly prefer home recovery supported by portable feeding systems and caregiver assistance. Telehealth and remote monitoring are improving safety and continuity of care outside hospitals. This trend is strengthened by developments such as France’s expanded home nutrition reimbursement and South Korea’s remote monitoring-based home feeding programs.

Regional Insights

North America Enteral Feeding Devices Market Trends

North America is projected to account for around 39% of the global enteral feeding devices market in 2026, supported by advanced healthcare infrastructure, high chronic disease burden, and strong reimbursement systems. The region benefits from early adoption of enteral nutrition technologies across ICUs, rehabilitation, and home care settings. Rising demand for connected and automated feeding systems is strengthening the clinical nutrition devices market, while FDA oversight continues to drive safety-focused innovation.

U.S. Enteral Feeding Devices Market Trends

The U.S. is expected to hold nearly 35% share of the regional market in 2026, driven by high ICU admissions, rising cancer cases, and widespread use of enteral nutrition protocols in hospitals. Strong reimbursement support and advanced hospital systems enable large-scale deployment of feeding technologies. Federal hospital modernization efforts are expected to accelerate the adoption of smart feeding systems in ICUs. Increasing use of digital monitoring is improving patient safety and operational efficiency.

Canada Enteral Feeding Devices Market Trends

Canada is projected to account for around 15% of the regional market in 2026, supported by expanding elderly care programs and rising demand for home enteral nutrition services. Government-backed healthcare access is supporting a gradual shift toward home-based nutrition care. Provincial systems are increasingly focusing on long-term nutritional management for aging populations. This is driving steady adoption of portable enteral feeding systems.

Europe Enteral Feeding Devices Market Trends

Europe is estimated to hold approximately 27% of the global enteral feeding devices market in 2026, driven by aging populations, rising chronic disease prevalence, and strong EU MDR regulatory alignment. Demand is growing across hospitals and home care settings as long-term nutritional therapy gains importance. Adoption of standardized feeding systems is strengthening the hospital enteral feeding systems market, while cost pressures influence procurement strategies.

Germany Enteral Feeding Devices Market Trends

Germany is projected to account for nearly 30% of the Europe market in 2026, supported by advanced hospital infrastructure and high investment in critical care nutrition systems. Strong ICU networks ensure consistent demand for enteral feeding solutions. Hospital digitalization programs are integrating automated nutrition systems into care workflows. This reinforces Germany’s position in clinical nutrition innovation.

U.K. Enteral Feeding Devices Market Trends

U.K. is estimated to hold around 22% of the regional market, driven by NHS-supported home enteral nutrition programs and a shift toward outpatient care. Demand is rising for long-term nutrition support outside hospitals to ease system pressure. NHS care models are expanding structured home feeding support for chronic patients. This is accelerating the adoption of portable feeding technologies.

Asia Pacific Enteral Feeding Devices Market Trends

Asia Pacific is projected to be the fastest-growing region, accounting for around 24% of the global enteral feeding devices market in 2026, driven by healthcare infrastructure expansion and rising chronic disease burden. Increasing elderly population and ICU capacity growth remain key drivers. Adoption of cost-efficient feeding systems is rising across hospitals and home care. Growth is further supported by manufacturing advantages and localization initiatives.

China Enteral Feeding Devices Market Trends

China is expected to account for nearly 35% of the Asia Pacific market in 2026, driven by hospital modernization and expanding critical care infrastructure. Rising chronic disease burden is increasing demand for advanced enteral nutrition systems. Government investments are improving access to critical care nutrition in hospitals. This reinforces China’s leadership in high-volume adoption.

India Enteral Feeding Devices Market Trends

India is projected to hold around 18% of the regional market in 2026, supported by rising hospital admissions, ICU expansion, and growing clinical nutrition awareness. Demand is increasing across both public and private healthcare systems. Infrastructure improvements are expanding access in tier-2 and tier-3 cities. This is accelerating the adoption of cost-effective enteral feeding solutions.

Competitive Landscape

The global enteral feeding devices market is moderately consolidated, with key players such as Cardinal Health, Fresenius Kabi, BD, Avanos Medical, and Moog accounting for a major share of revenues. These companies leverage strong hospital relationships, broad product portfolios, and integrated nutrition delivery systems. Continuous investment in safer, more precise feeding technologies and connected solutions is strengthening competitiveness in the enteral nutrition devices industry. Expansion into home healthcare and digital monitoring is further driving differentiation.

Regional and niche players such as Nestlé Health Science, Danone Nutricia, B. Braun, and Cook Medical focus on specialized segments like medical nutrition and PEG systems. High regulatory barriers, clinical validation requirements, and complex hospital integration limit new entrants. However, rising demand for portable and home-based feeding solutions is creating opportunities for mid-sized innovators. The market is expected to consolidate further through acquisitions and strategic partnerships.

Key Industry Developments:

- In March 2025, Fresenius Kabi announced expanded investment in clinical nutrition and infusion technologies across Europe and Asia Pacific, supporting increased manufacturing capacity for enteral feeding systems and home nutrition products. The expansion aligned with rising regional demand for long-term nutritional care.

- In February 2025, Cardinal Health launched the Kangaroo OMNI™ enteral feeding pump in Europe, Australia, and New Zealand. Designed for use with blended and thickened formulas, the pump features a night mode display, 30-day feeding history, and a portable, water-resistant design ideal for both clinical and home enteral nutrition settings.

Companies Covered in Enteral Feeding Devices Market

- Cardinal Health

- Becton, Dickinson and Company

- Fresenius Kabi AG

- Avanos Medical, Inc.

- Moog Inc.

- Abbott Laboratories

- B. Braun SE

- Boston Scientific Corporation

- CONMED Corporation

- Vygon SA

- Cook Medical

- Applied Medical Technology, Inc.

- Medela AG

Frequently Asked Questions

The global enteral feeding devices market is projected to reach US$3.0 billion in 2026.

Rising chronic disease prevalence, aging population, and growing demand for clinical nutrition drive the market.

The enteral feeding devices market is expected to grow at a CAGR of 6.0% from 2026 to 2033.

Expansion of home healthcare, adoption of smart feeding systems, and rising demand in emerging economies create growth opportunities.

Key players include Cardinal Health, Fresenius Kabi, BD (Becton Dickinson), Avanos Medical, and Moog Inc.