- Pharmaceuticals

- Cancer Care Supportive Products Market

Cancer Care Supportive Products Market Size, Share, Trends, Growth, and Regional Forecast, 2025 to 2032

Cancer Care Supportive Products Market by Drug Class (Granulocyte Colony Stimulating Factor, Nonsteroidal Anti-inflammatory Drugs, Monoclonal Antibodies, Erythropoietin Stimulating Agents, Opioid Analgesics, Others), Indication, Distribution Channel and Regional Analysis from 2025 to 2032

Cancer Care Supportive Products Market Share and Trends Analysis

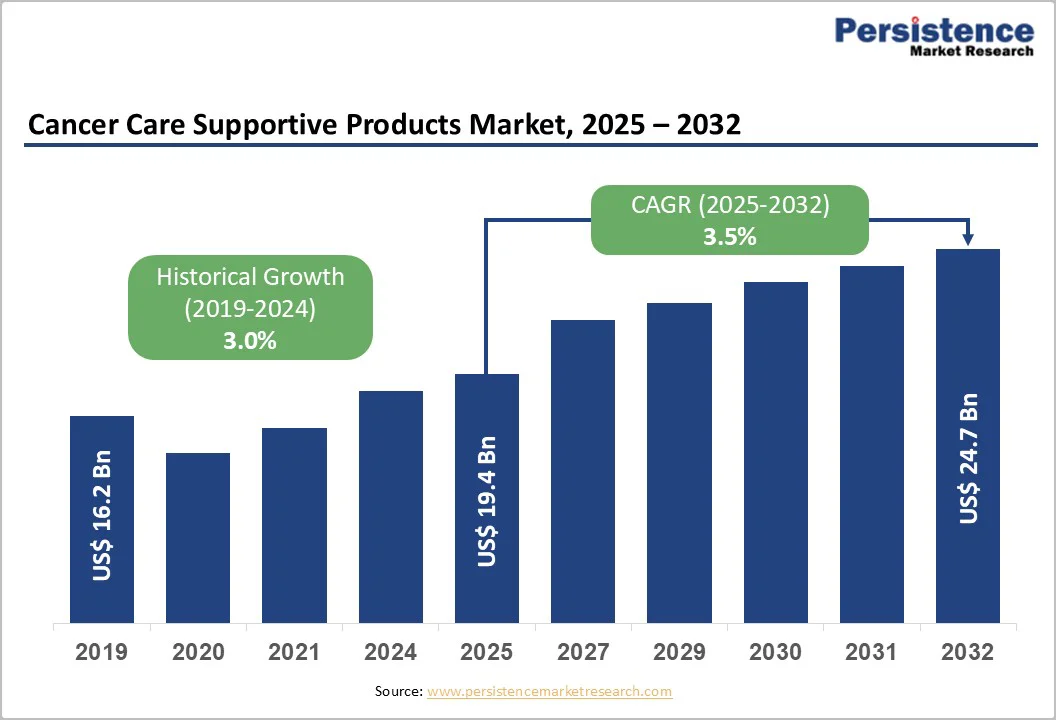

The global cancer care supportive products market size is valued at US$ 19.4 billion in 2025 and is projected to reach US$ 24.7 billion by 2032, growing at a CAGR of 3.5% between 2025 and 2032.

As cancer incidence continues to rise, it has intensified the need for therapies that manage treatment-related complications. With patients undergoing increasingly complex regimens-ranging from cytotoxic chemotherapy to targeted and immuno-oncology therapies-the demand for products that reduce toxicity, improve tolerance, and maintain treatment continuity is accelerating.

As cancer prevalence grows across regions, more healthcare organizations and pharmaceutical players are strengthening their presence in this space, driving rapid uptake of supportive care solutions that enhance patient outcomes and overall quality of life during cancer treatment.

Key Industry Highlights

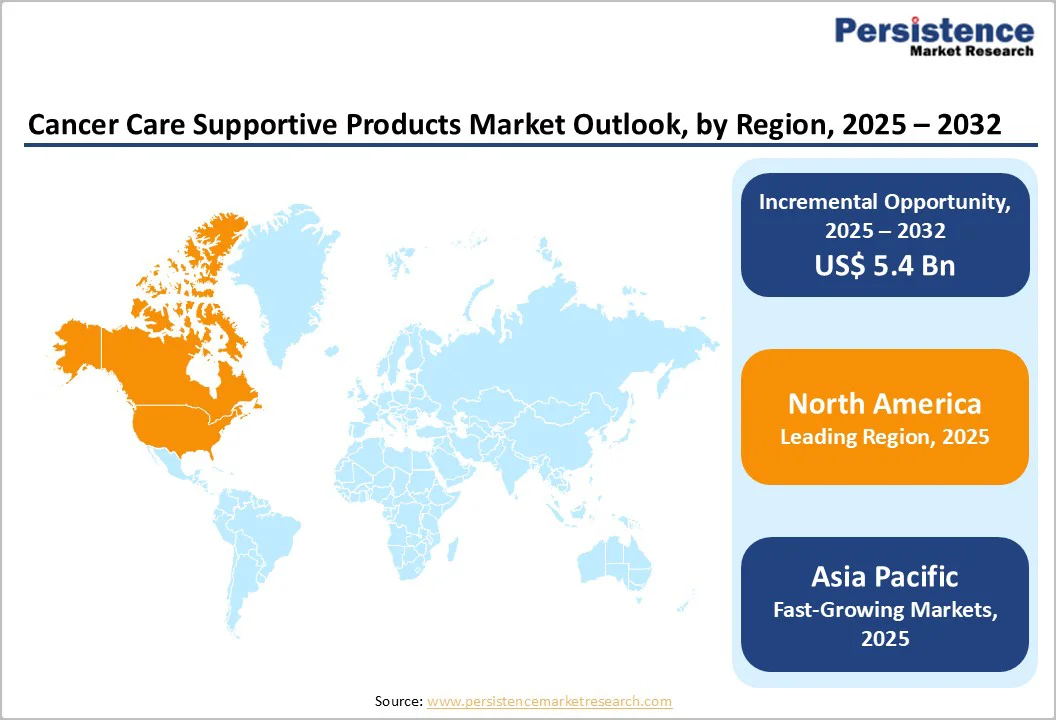

- Leading Region: North America dominates the global market with 46.2%, driven by advanced oncology infrastructure, strong reimbursement systems, and high adoption of innovative supportive care therapies.

- Fastest-Growing Region: The Asia Pacific market is expected to grow rapidly with a CAGR of 4.4% in forecast period, fueled by rising cancer burden, expanding healthcare access, and increasing availability of cost-effective supportive care products.

- Leading Service: Granulocyte colony stimulating factor lead with 25.5% share, supported by its central role in preventing chemotherapy-induced neutropenia across multiple high-volume cancer treatments.

- Leading Indication: Lung cancer dominates with 15.2%, driven by its high global incidence and frequent need for toxicity-management therapies during aggressive treatment regimens.

- Leading Distribution Channel: Hospital pharmacies dominate with 51.8%, driven by specialized dispensing controls, oncology-linked oversight, and high utilization of supervised injectable supportive therapies.

- Rising Biologic Adoption: Growing use of biologic and targeted therapies increases supportive care needs due to evolving toxicity profiles requiring specialized management.

- Regulatory Alignment: Harmonized global regulatory frameworks for supportive therapies speed approvals and encourage multinational product rollouts.

- Increased Institutional Investment: Hospitals and cancer centers are expanding supportive oncology units, boosting procurement of advanced supportive products across specialties.

| Key Insights | Details |

|---|---|

| Global Cancer Care Supportive Products market Size (2025E) | US$ 19.4 Billion |

| Market Value Forecast (2032F) | US$ 24.7 Billion |

| Projected Growth (CAGR 2025 to 2032) | 3.5% |

| Historical Market Growth (CAGR 2019 to 2024) | 3.0% |

Market Dynamics

Driver - Rising Cancer Burden and Advancing Therapies Propel Demand for Supportive Products by Expanding Treatment Volumes and Complexity

The global cancer supportive care products market continues to grow, supported not only by rising cancer prevalence but also by demographic, economic, and technological shifts. The World Health Organization (2024) projected over 35 million new cancer cases by 2050, reinforcing long-term demand.

An ageing global population, greater effectiveness of anti-cancer therapies, and rising purchasing power in emerging economies further strengthened the adoption of supportive care solutions. Innovation also played a pivotal role, with companies advancing diagnostics, targeted therapies, and access programs.

Pediatric cancer care remained a major unmet area. Each year, 400,000 children develop cancer worldwide, yet survival varies dramatically-over 80% cured in high-income countries versus 90% mortality in sub-Saharan Africa.

In response, companies such as Teva Pharmaceuticals expanded its access program-initially launched in Malawi-to Uganda, Botswana, Tanzania, and Rwanda, with plans for eight global programs by 2025 to deliver medicines to underserved communities.

Advances in precision oncology also supported market growth. In April 2023, Foundation Medicine expanded its collaboration with Bristol Myers Squibb to advance the FoundationOne®CDx diagnostic as a companion test for the investigational TKI repotrectinib in the TRIDENT-1 Phase 1/2 trial, reinforcing precision oncology adoption.

Meanwhile, in October 2025, Scottish biotech Trogenix secured £70 million in Series A funding-supported by Eli Lilly and leading venture firms-to accelerate its viral immunotherapy program for glioblastoma. Together, these scientific, demographic, and access-driven factors continued to strengthen global demand for cancer supportive care products.

Restraints - High R&D Costs and Biosimilar Competition Hinder Growth by Increasing Development Risk and Compressing Commercial Margins

Despite strong growth drivers, several structural barriers continue to restrain the global cancer supportive care products market. One of the most significant challenges is the accelerating entry of biosimilars, which has intensified price competition and reduced revenue potential for originator therapies.

As patents expired across major oncology and supportive care drug classes, manufacturers faced shrinking margins, forcing companies to reassess investment priorities and commercialization strategies.

At the same time, the extremely high cost of research and development-often requiring more than a decade of discovery, clinical testing, and validation-remained a major limitation. Oncology-related R&D is particularly complex, with rising failure rates in late-stage trials and growing demand for biomarker-driven studies. These escalating costs deterred smaller companies and slowed the introduction of truly novel supportive care therapies.

Regulatory hurdles also weighed heavily on market expansion. Global agencies such as the U.S. FDA, Europe Medicines Agency (EMA), and emerging regulators in Asia enforced increasingly stringent clinical, safety, and manufacturing standards, lengthening approval timelines and increasing compliance costs. Companion diagnostics, real-world evidence requirements, and post-marketing surveillance frameworks further added to regulatory complexity.

Collectively, these pressures-biosimilar competition, costly R&D pathways, and evolving regulatory barriers-continued to limit market acceleration and challenge the timely delivery of innovative supportive care solutions worldwide.

Opportunity - Expanding Access Programs and Precision Diagnostics Create New Growth Avenues by Improving Early Detection and Treatment Reach

The global cancer supportive care products market is poised for significant opportunity as vendors expand into highly populated emerging economies and increase investment in next-generation R&D. Rapidly growing cancer incidence globally creates a substantial unmet need, positioning the region as a priority market where wider access, rising purchasing power, and ongoing healthcare modernization can accelerate adoption.

Innovation-driven approvals are further opening avenues for supportive care integration. In August 2024, Johnson & Johnson received FDA approval for the first-line, chemotherapy-free, multitargeted regimen RYBREVANT® + LAZCLUZE™ for EGFR-mutated non-small cell lung cancer (NSCLC)-raising demand for adjunctive supportive products.

Shortly after, in September 2024, Takeda secured Japanese approval for FRUZAQLA, supported by the FRESCO-2 global Phase 3 trial, which demonstrated consistent benefits for previously treated metastatic colorectal cancer patients.

In May 2025, AbbVie’s EMRELIS™ earned accelerated FDA approval for high c-Met overexpressing NSCLC, marking a breakthrough in antibody drug conjugate (ADC)-based precision oncology and expanding opportunities for supportive interventions that accompany advanced therapies.

Complementary ecosystem investments also fuel market growth. Heron Therapeutics continues to fund Investigator-Initiated Trials (IITs) and medical education to advance non-opioid post-operative cancer pain management, while Helsinn Healthcare’s global Early Access Programs (EAPs) broaden compassionate-use availability of investigational therapies.

Collectively, expanding R&D, rising access initiatives, and strong oncology pipelines position global vendors to capture substantial new growth opportunities.

Category-wise Analysis

By Service Insights: Granulocyte Colony Stimulating Factor Dominates Owing to Expanding Use Despite Shifts in Chemotherapy Demand

Granulocyte colony-stimulating factor is projected to secure a 25.5% share of the global cancer supportive care products market by 2025. Its widespread adoption is driven by its role in preventing chemotherapy-induced neutropenia across several high-incidence cancers, making it a routine component of supportive care protocols.

However, the rapid uptake of immuno-oncology therapies-especially anti-PD-1/L1 agents that reduce reliance on myelosuppressive chemotherapy-is steadily softening the demand trajectory for G-CSF. This shift is creating a more balanced growth landscape, where clinical relevance remains strong but expansion is increasingly moderated by evolving treatment paradigms.

By Indication Insights: Lung Cancer Lead Due to Rising Global Incidence and Intensive Treatment Needs

Lung cancer is projected to command almost 15.2% of the global cancer supportive care products market in 2025. Its leadership is driven by persistently high incidence, late-stage diagnosis rates, and intensive reliance on supportive care to manage chemotherapy-induced toxicities, respiratory complications, and overall treatment burden.

As systemic therapies expand and survival improves, demand for adjunct supportive care continues to strengthen across both non-small cell and small cell lung cancer populations.

By Distribution Channel Insights: Hospital Pharmacies to Dominated Due to Their Clinical Oversight and High-Volume Oncology Dispensing

Hospital pharmacies are projected to capture 51.8% of the global market in 2025, driven by their specialized role in dispensing high-acuity oncology supportive care products. Their structured inventory systems, stringent safety protocols, and closer coordination with oncology departments enable reliable, clinically supervised access to injectables, biologics, and other regulated therapies.

Additionally, hospital pharmacies manage a higher volume of chemotherapy-related prescriptions and treatment add-ons, making them the preferred distribution point for products that require expert handling, cold-chain integrity, and on-site clinical oversight.

Regional Insights

North America Cancer Care Supportive Products Market Trends

By 2025, North America was projected to account for 46.2% of the global cancer supportive care products market, anchored by a consistently high cancer burden and rapid therapeutic innovation. The region’s need for supportive care expanded as the National Cancer Institute estimated 2,001,140 new cancer cases and 611,720 deaths in the U.S. by the end of 2024, while historic incidence remained high, with over 1.5 million new cases reported in 2017.

Rising recurrence risk in early-diagnosed breast cancer further sustained long-term supportive therapy demand; despite 90% of U.S. cases being detected at stages I-III, recurrence-often as metastatic and incurable disease-remained a persistent concern, with about 10% of high-risk N0 patients experiencing relapse within three years.

The FDA granted Breakthrough Therapy Designation to GSK’s Jemperli in December 2024, followed by Fast Track status in January 2023. Approvals continued into October 2025 with Blenrep for relapsed/refractory multiple myeloma, and September 2025 data from Lilly’s Jaypirca strengthened first-line potential in blood cancers.

Additionally, in January 2025, Health Canada authorized FRUZAQLA and expanded access to advanced colorectal cancer treatment. Collectively, the rising disease burden and continuous treatment innovation solidified North America’s leadership in supportive care demand.

Europe Cancer Care Supportive Products Market Trends

By 2025, Europe was projected to hold 24.3% of the global cancer supportive care products market, supported by a rising disease burden and strong healthcare engagement. Cancer prevalence had increased by 24% over the past decade, and in many European countries, one in three individuals faced a high likelihood of diagnosis by age 75.

Throughout 2024, multiple regional initiatives highlighted Europe’s emphasis on patient-centred care. Daiichi Sankyo Germany partnered with dasBUUSENKOLLEKTIV to promote open cancer dialogue and hosted a 2024 “Let Your Scars Shine” empowerment event in Munich, spotlighting challenges after mastectomy.

The same year, Daiichi Sankyo UK collaborated with Breast Cancer Now to support a national metastatic breast cancer audit, which later received government funding. Daiichi Sankyo Europe also worked with The Economist Impact to propose a more women-centric framework for breast cancer care.

Regulatory advancements further strengthened demand for supportive therapies. Lynparza was accepted by NHS Scotland in February 2025, Blenrep regained U.K. approval in October 2025, and Ireland approved Abemaciclib in May 2024, with availability from June 1, 2024. Collectively, these initiatives and approvals continued to strengthen Europe’s push toward more equitable, patient-centred cancer care across the region.

Asia Pacific Cancer Care Supportive Products Market Trends

Asia Pacific cancer supportive care products market has been expanding rapidly and was projected to grow at a 4.4% CAGR over the forecast period, driven by rising cancer incidence, accelerating approvals, and strong regional R&D activity.

Breast cancer remained the most common cancer among women in Japan, with 92,000 cases and 17,600 deaths recorded in 2022, and approximately 70% classified as HR-positive, HER2-negative disease. This high burden supported demand for advanced supportive and therapeutic options.

In August 2025, Japan approved Daiichi Sankyo’s Enhertu as the first HER2-directed therapy for HR-positive, HER2-low or ultralow metastatic breast cancer-shortly after the FDA granted the drug U.S. approval in January 2025 and featured it on World Cancer Day (Feb 4, 2025).

Daiichi Sankyo also received FDA Breakthrough Therapy Designation for ifinatamab deruxtecan for extensive-stage small cell lung cancer (August 2025). Moreover, recent studies highlighted India’s rising gynecological cancer burden which intensified supportive care needs, with endometrial and ovarian cancer incidence projected to rise 78% and 69% by 2045. In August 2025, GSK introduced Jemperli and Zejula in India to address these gaps.

China advanced regional innovation through major partnerships-HUTCHMED’s January 2023 global licensing deal with Takeda for fruquintinib, and Takeda’s October 2025 $11B collaboration with Innovent. Australia added to the ecosystem with a March 2022 MSD-Imugene trial evaluating HER-Vaxx with Keytruda. Collectively, these developments strengthened Asia Pacific’s momentum in supportive oncology care.

Competitive Landscape

The competitive landscape is shaped by rapid advancements in targeted therapies, antibody-drug conjugates, and immuno-oncology candidates, supported by frequent strategic alliances, global licensing deals, and accelerated regulatory designations. Expanding late-stage pipelines, breakthrough approvals, and cross-border development partnerships continue to intensify competition across solid tumors and hematologic malignancies.

Key Industry Developments:

- In October 2025, AstraZeneca and Daiichi Sankyo’s Datroway showed a 43% reduction in risk of progression or death in the TROPION-Breast02 Phase III trial, becoming the first therapy to significantly improve both overall and progression-free survival versus chemotherapy in first-line metastatic TNBC without immunotherapy options.

- In October 2025, Takeda entered a global partnership with Innovent Biologics to develop, manufacture, and commercialize late-stage oncology candidates IBI363 and IBI343 outside Greater China, targeting lung, colorectal, gastric, and pancreatic cancers.

- In October 2025, Moffitt Cancer Center and AbbVie formed a five-year strategic alliance to accelerate oncology innovation, combining AbbVie’s research strength with Moffitt’s clinical expertise to advance early-stage programs, translational research, and real-world evidence generation.

- In September 2025, the IDeate-Lung01 Phase 2 trial showed ifinatamab deruxtecan delivering clinically meaningful responses in previously treated ES-SCLC, following its August 2025 FDA Breakthrough Therapy Designation as a potential first-in-class B7-H3-directed antibody-drug conjugate.

Companies Covered in Cancer Care Supportive Products Market

- Amgen Inc.

- Johnson & Johnson.

- Novartis AG

- Baxter

- Fagron

- Teva Pharmaceutical Industries Ltd.

- F. Hoffmann-La Roche Ltd

- APR

- Acacia Pharma Ltd.

- Kyowa Kirin Co., Ltd.

- Daiichi Sankyo, Inc.

- GSK plc

- Heron Therapeutics, Inc.

- Helsinn Healthcare SA

- Bristol-Myers Squibb Company

- Eli Lilly and Company

- Takeda Pharmaceutical Company Limited

- Sanofi

- AbbVie Inc.

- AstraZeneca

- Kura Oncology, Inc.

Frequently Asked Questions

The global cancer care supportive products market is valued at US$ 19.4 Billion in 2025.

Rising cancer incidence, expanding treatment complexity, and growing adoption of advanced supportive therapies drive global market growth.

The global market is poised to witness a CAGR of 3.5% between 2025 and 2032.

Emerging markets, R&D expansion, and next-generation supportive innovations create significant new growth opportunities.

Major players in the global are Novartis AG, GSK, Amgen, Eli Lilly and Company, Sanofi and others.