- Healthcare IT

- ICD-10 Market

ICD-10 Market Size, Share, and Growth Forecast 2026 - 2033

ICD-10 Market by Product Type (ICD-10-CM, ICD-10-PCS), by Deployment Mode (Cloud-Based, On-Premise, Hybrid, Mobile-Based), by Application (Clinical Documentation, Medical Billing & Reimbursement, Reporting & Compliance, Healthcare Analytics), End-User, and Regional Analysis, 2026 - 2033

ICD-10 Market Size and Trend Analysis

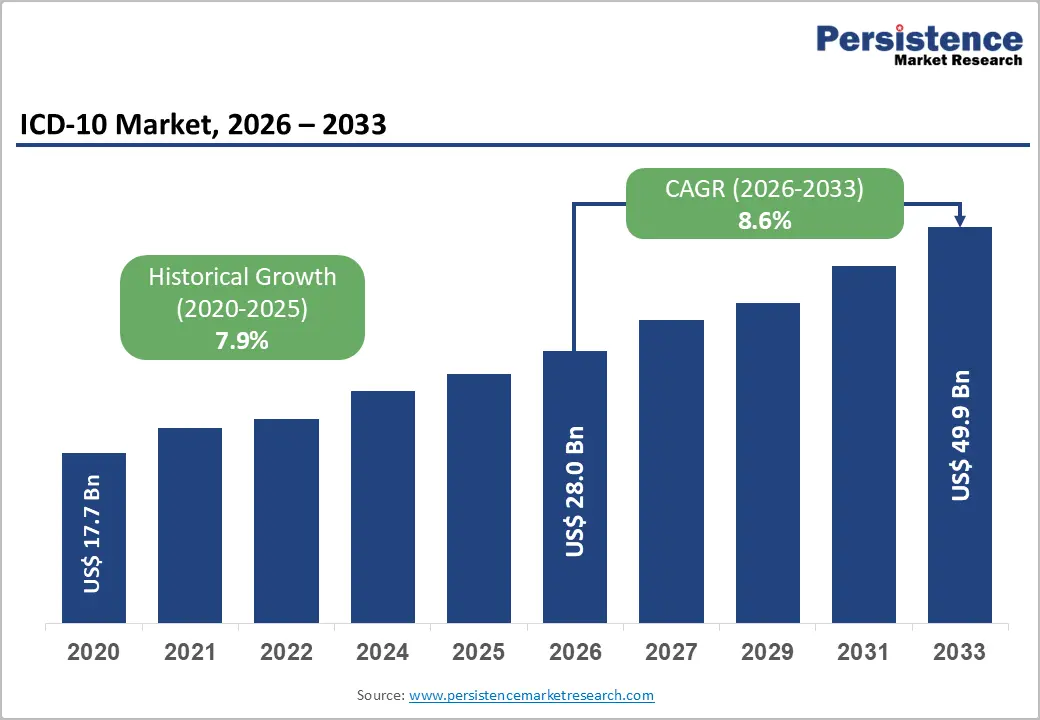

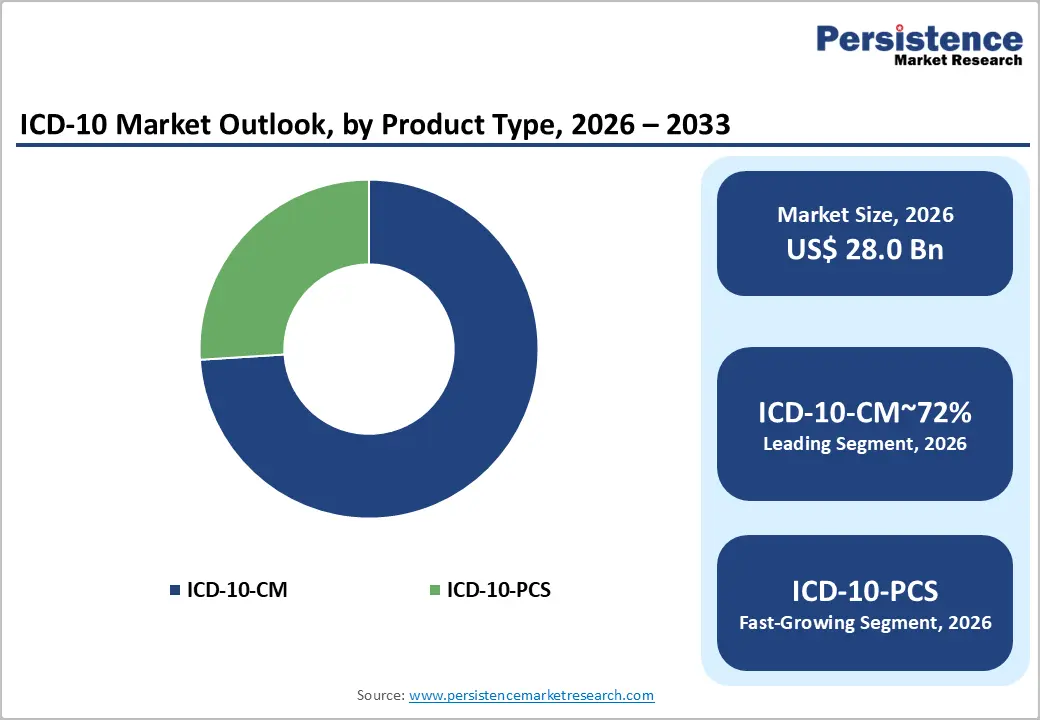

The global ICD-10 market size is likely to reach US$ 28.0 billion in 2026 and is expected to reach US$ 49.9 billion by 2033, growing at a CAGR of 8.6% during the forecast period from 2026 to 2033.

The ICD-10 market is on a robust and accelerating growth trajectory, driven by global healthcare digitalization mandates, the universal adoption of ICD-10 coding standards for clinical documentation and medical billing, and the expanding role of ICD-10 coded data in population health management, healthcare analytics, and value-based care reimbursement models.

Key Industry Highlights:

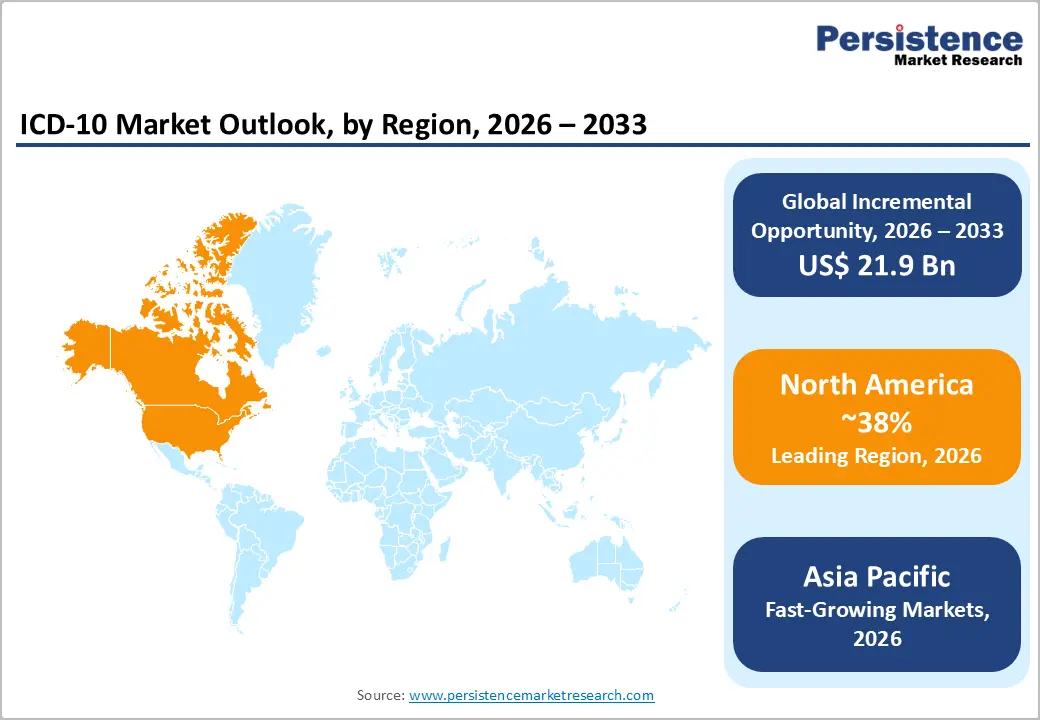

- Leading Region: North America dominates the ICD-10 market, accounting for 39% share, anchored by the U.S.’s mandatory federal ICD-10-CM/PCS compliance for Medicare and Medicaid claims, a 6,000+ hospital and 900,000+ physician market, and a world-leading health IT innovation ecosystem driving global ICD-10 solution standards.

- Fastest Growing Region: Asia Pacific is the fastest growing region with a rising CAGR of 9.8%, driven by India’s Ayushman Bharat Digital Mission, China’s Healthy China 2030 hospital digitalization, Australia’s mature ICD-10-AM system, and ASEAN nations progressively implementing national ICD-10 coding standards with WHO support.

- Dominant Segment: ICD-10-CM leads the By Product Type category with approximately 72% market share, as the universal diagnostic coding system used across all clinical settings, driven by annual CMS code updates and mandatory compliance requirements for every U.S. Medicare and Medicaid claim.

- Fastest Growing Segment: Cloud-Based deployment is the fastest growing segment within the By Deployment Mode category, driven by automatic annual code set updates, HIPAA-compliant cloud health IT platforms from AWS, Microsoft Azure, and Google Cloud, and FHIR interoperability mandate compliance requirements.

- Key Opportunity: AI-powered Computer-Assisted Coding (CAC) delivering 30-50% productivity improvement amid chronic medical coder shortages, and emerging market ICD-10 adoption supported by India’s ABDM and China’s Healthy China 2030, represent the highest-value growth opportunities through 2033.

Market Dynamics

Drivers - Mandatory Healthcare Digitalization and ICD-10 Compliance Regulations

Government-mandated healthcare digitalization programs and ICD-10 compliance requirements constitute the most powerful and consistent demand driver in this market. In the United States, the Centers for Medicare & Medicaid Services (CMS) made ICD-10-CM/PCS the mandatory coding standard for all Medicare and Medicaid claims from October 1, 2015, with ongoing annual code updates creating continuous upgrade demand.

The 21st Century Cures Act and the CMS Interoperability and Patient Access Final Rule are compelling broader adoption of standardized clinical data exchange, including ICD-10-coded diagnoses. Internationally, the WHO’s ICD-11 implementation timeline is driving countries currently on ICD-10 to upgrade their coding infrastructure. Over 100 countries have adopted ICD-10 as their national clinical coding standard per WHO records, with many now migrating systems to accommodate ICD-11 compatibility, generating sustained software investment cycles globally.

Value-Based Care and Healthcare Analytics Driving ICD-10 Data Utilization

The global transition from fee-for-service to value-based care reimbursement models is fundamentally expanding the strategic importance and commercial value of ICD-10-coded clinical data. Accurate, granular ICD-10 coding enables risk stratification for population health programs, supports quality measure reporting under CMS’ Merit-based Incentive Payment System (MIPS) and Alternative Payment Models (APMs), and underpins predictive analytics for chronic disease management.

The American Academy of Professional Coders (AAPC) reports that healthcare organizations with optimized ICD-10 coding accuracy achieve improvements of 15-20% in claim reimbursement rates and significant reductions in claim denial rates. This direct revenue impact is compelling healthcare providers to invest in advanced ICD-10 software, AI-assisted coding tools, and professional coding education programs, accelerating demand across the full ICD-10 solutions ecosystem.

Restraints - High Implementation Costs and Complexity for Smaller Healthcare Providers

Implementing comprehensive ICD-10 coding systems requires significant upfront investment in software licensing, infrastructure upgrades, workflow redesign, and staff training, creating financial barriers for small and rural healthcare providers.

The American Medical Association (AMA) estimated that initial ICD-10 implementation costs for small physician practices ranged from US$3,000 to over US$226,000, depending on practice size and EHR system readiness. For developing countries attempting national ICD-10 adoption, the investment in health information infrastructure, coder training programs, and software localization represents a substantial burden relative to available public health budgets.

Coding Complexity and Workforce Shortage of Certified Medical Coders

ICD-10, particularly the procedural coding system (ICD-10-PCS), represents a substantial increase in coding complexity over its predecessor, with ICD-10-CM containing over 70,000 diagnosis codes and ICD-10-PCS over 87,000 procedure codes versus approximately 13,000 codes in ICD-9-CM. The AAPC and American Health Information Management Association (AHIMA) both report persistent shortages of certified medical coders, with demand significantly outpacing supply. This workforce constraint elevates coding error rates, delays claim submission, and increases reliance on outsourced coding services, adding cost and complexity for healthcare providers.

Opportunities - AI-Assisted Computer-Assisted Coding (CAC) Technology Adoption

Artificial intelligence and natural language processing (NLP) technologies are transforming ICD-10 coding through Computer-Assisted Coding (CAC) systems that automatically suggest ICD-10 codes from clinical documentation, dramatically reducing manual coding time and error rates. The Office of the National Coordinator for Health Information Technology (ONC) in the U.S. has actively promoted NLP-driven clinical documentation improvement as a strategic healthcare IT priority.

Leading CAC platform providers, including 3M Company’s 360 Encompass™ system, Nuance Communications’ Dragon Medical One, and Optum’s Optum360, are demonstrating productivity improvements of 30-50% in coding throughput, with simultaneous increases in accuracy. As healthcare organizations face growing coding volumes, workforce shortages, and annual ICD-10 code updates, the ROI case for AI-assisted coding technology is immediate and compelling, positioning CAC as the fastest-growing ICD-10 technology segment with substantial revenue expansion opportunities for vendors.

Emerging Market Healthcare Infrastructure Development and ICD-10 Adoption

Asia Pacific, Latin America, and the Middle East represent high-growth regions, as governments and healthcare systems in these markets invest in digital health infrastructure and transition to ICD-10 as their national clinical coding standard. India’s National Digital Health Mission (Ayushman Bharat Digital Mission) is building a nationwide health data exchange infrastructure that mandates standardized diagnostic coding aligned with ICD-10 across all participating facilities.

China’s Healthy China 2030 plan is driving hospital information system modernization, incorporating ICD-10 as the clinical coding backbone. The WHO’s Collaborating Center for Classification of Diseases actively supports ICD-10 adoption in member states, with ongoing technical assistance programs expanding the global ICD-10 software and services market into previously underpenetrated healthcare systems across Africa, Southeast Asia, and Latin America.

Category-wise Analysis

By Product Type Insights

ICD-10-CM (Clinical Modification) is the dominant product type segment, commanding approximately 72% of total market share. ICD-10-CM is the universal diagnostic coding system used across all outpatient, inpatient, emergency, and home health clinical documentation in the United States and adapted versions are similarly the standard in healthcare systems globally.

With over 70,000 diagnosis codes covering the complete spectrum of diseases, injuries, and health conditions, ICD-10-CM software is required by every healthcare provider, insurance company, and government health program involved in clinical documentation and claims processing. Annual code updates released by the National Center for Health Statistics (NCHS) and CMS each October drive recurring software upgrade and training investment cycles that sustain ICD-10-CM solution demand as a baseline, non-discretionary expenditure for the U.S. healthcare system and analogous systems globally.

By Deployment Mode Insights

Cloud-Based deployment leads the deployment mode segment, representing approximately 51% of total market share. Cloud-deployed ICD-10 coding solutions offer healthcare organizations compelling advantages, including automatic code set updates aligned with annual ICD-10 releases, scalable user access for distributed coding teams, lower upfront infrastructure investment, and seamless integration with cloud-hosted EHR and revenue cycle management platforms.

Major cloud platforms, including Amazon Web Services (AWS) for Health, Microsoft Azure Healthcare APIs, and Google Cloud Healthcare API, have developed HIPAA-compliant cloud infrastructure specifically designed for healthcare data workloads, including ICD-10 coded clinical data. The ONC’s Interoperability Standards Advisory and FHIR-based data exchange mandates are further accelerating cloud adoption by requiring accessible, standardized data exchange that cloud platforms best support.

By Application Insights

Medical Billing & Reimbursement is the leading application segment, accounting for approximately 39% of the market. The direct and immediate revenue impact of ICD-10 coding accuracy on healthcare provider reimbursement makes medical billing and revenue cycle management the highest-priority application for ICD-10 software investment.

Incorrect or unspecific ICD-10 diagnosis coding is the leading cause of medical claim denials, with the American Association of Healthcare Administrative Management (AAHAM) estimating that claim denials cost U.S. healthcare providers over US$ 262 billion annually. ICD-10 billing solutions that integrate real-time code validation, payer-specific coding edits, and AI-assisted coding suggestions deliver measurable, quantifiable ROI by reducing denial rates and accelerating reimbursement cycles. The segment’s commercial importance ensures it receives the majority of investment in healthcare revenue cycle management technology.

By End-user Insights

Healthcare Providers are the dominant end-user segment, representing approximately 47% of total market share. Hospitals, physician practices, outpatient clinics, ambulatory surgical centers, and home health agencies constitute the largest and most diverse buyer constituency for ICD-10 coding solutions, requiring software for inpatient and outpatient clinical documentation, electronic health record integration, and claims submission.

The American Hospital Association (AHA) reports that there are over 6,000 hospitals in the United States alone, each requiring comprehensive ICD-10 software deployment, annual code updates, and ongoing coder training. Internationally, healthcare provider adoption of ICD-10 is expanding rapidly as national eHealth strategies mandate standardized coding across public and private healthcare facilities, ensuring sustained and growing global demand from this end-user segment.

Regional Insights

North America ICD-10 Market Insights

North America is the dominant ICD-10 market, anchored by the United States’ mandatory federal ICD-10-CM/PCS adoption for all Medicare, Medicaid, and CHIP claims, which has created the world’s largest and most commercially developed ICD-10 software and services ecosystem. The CMS’ annual ICD-10 code set update cycle, adding hundreds of new codes each October, generates recurring upgrade and retraining demand. The U.S. healthcare information technology market’s scale, with over 6,000 hospitals and 900,000+ physicians requiring ICD-10 compliant systems, sustains a vast addressable market.

The 21st Century Cures Act’s information blocking provisions and the CMS Interoperability Final Rule mandating FHIR-based data exchange are compelling healthcare organizations to upgrade their ICD-10 systems to support structured, standardized data sharing. Canada’s ICD-10-CA system and ongoing eHealth Canada initiatives also contribute to regional demand. The U.S. innovation ecosystem, with companies including 3M, Optum, Nuance Communications, Cerner (Oracle Health), and Athenahealth, continuously develops next-generation AI-assisted coding and clinical documentation improvement technologies that define global ICD-10 solution standards.

Europe ICD-10 Market Insights

Europe is a significant and growing ICD-10 market, with most member states using national adaptations of ICD-10 for clinical and administrative coding within their healthcare systems. Germany uses ICD-10-GM (German Modification), which serves as the basis for DRG-based hospital reimbursement, governed by the Institut für das Entgeltsystem im Krankenhaus (InEK). Annual German ICD-10-GM updates drive continuous software upgrade investment across the country’s healthcare facilities. The United Kingdom’s NHS uses ICD-10 for clinical coding within its Secondary Uses Service (SUS) data infrastructure, with the NHS Digital (now NHS England) driving national clinical coding standards.

France employs the CIM-10 (Classification Internationale des Maladies) adaptation for hospital activity reporting under the PMSI (Program de Médicalisation des Systèmes d’Information) framework. The EU’s European Health Data Space (EHDS) regulation, proposed in 2022 and advancing through the legislative process, mandates standardized health data sharing across member states, with ICD-10-coded data as a core component, creating new regulatory demand for system upgrades. Spain and Central/Eastern European nations are modernizing hospital information systems with ICD-10 capabilities under EU digital health transformation programs, expanding the European ICD-10 addressable market.

Asia Pacific ICD-10 Market Trends

Asia Pacific is the fastest-growing ICD-10 market, driven by national digital health initiatives, expanding healthcare IT investment, and government mandates for standardized clinical coding across China, India, Japan, Australia, and ASEAN nations. Australia has been an ICD-10 early adopter, using ICD-10-AM (Australian Modification) since 1998, with the Australian Consortium for Classification Development (ACCD) managing ongoing updates. Japan uses ICD-10 for mortality statistics and is expanding its clinical coding infrastructure under national eHealth mandates.

India’s Ayushman Bharat Digital Mission (ABDM) is building a nationwide health data exchange framework incorporating ICD-10-coded diagnoses across enrolled facilities, generating significant demand for software, training, and implementation services. China’s hospital information system modernization under Healthy China 2030 is driving ICD-10 clinical coding adoption across its vast network of tier-2 and tier-3 hospitals. ASEAN health ministries, including Thailand, Vietnam, Malaysia, and Indonesia, are progressively implementing national ICD-10 coding standards, supported by WHO technical assistance, creating a rapidly expanding regional market for ICD-10 solutions and clinical coding education.

Competitive Landscape

The global ICD-10 market is moderately consolidated, with a mix of large health IT conglomerates and specialized clinical coding solution providers competing across software, services, and education segments. Companies such as 3M Company, Optum (UnitedHealth Group), Nuance Communications (Microsoft), Oracle Health (Cerner), and Wolters Kluwer hold strong market positions through comprehensive clinical documentation, CAC, and revenue cycle management platforms integrated with ICD-10 coding engines.

Key differentiators include AI-assisted coding accuracy, EHR integration depth, payer-specific editing rules, annual code update reliability, and clinical documentation improvement program support. Emerging trends include generative AI-powered autonomous coding, real-time clinical documentation improvement, mobile coding applications for remote coders, and outsourced coding-as-a-service subscription models targeting resource-constrained healthcare providers.

Key Developments:

- March 2025: Nuance Communications (Microsoft) launched an enhanced generative AI-powered clinical documentation intelligence module for Dragon Medical One, featuring automated ICD-10-CM code suggestion from ambient clinical documentation with real-time accuracy validation.

- October 2024: 3M Company released its updated 360 Encompass™ CAC platform with FY2025 ICD-10-CM/PCS code updates, incorporating enhanced AI logic for specificity improvement in diagnosis coding aligned with the annual CMS code set update effective October 1, 2024.

- June 2024: Optum, Inc. expanded its Optum360® coding solutions with a new mobile-based ICD-10 coding application for remote medical coders, enabling secure HIPAA-compliant coding workflow access from any device with integrated real-time code validation.

ICD-10 Market Report -Key Insights & Scope

| Key Insights | Details |

|---|---|

| Historical Market Value (2020) | US$ 17.7 Bn |

| Current Market Value (2026) | US$ 28.0 Bn |

| Projected Market Value (2033) | US$ 49.9 Bn |

| CAGR (2026-2033) | 8.6% |

| Leading Region | North America, 39% share |

| Dominant Product Type | ICD-10-CM, 72% share |

| Top-ranking deployment mode | Cloud-Based, 51% |

| Incremental Opportunity | US$ 21.9 Bn |

Companies Covered in ICD-10 Market

- 3M Company

- Wolters Kluwer N.V.

- Optum, Inc.

- QuadraMed Corporation

- Change Healthcare Holdings, Inc.

- Dolbey Systems, Inc.

- MRS Systems

- Intelligent Medical Objects, Inc.

- TELUS Health Solutions

- e-MDs, Inc.

- Nuance Communications, Inc.

- Oracle Corporation

- Cerner Corporation

- Athenahealth, Inc.

- Aviacode Inc.

- nThrive

- Coding Clarity

Frequently Asked Questions

The global ICD-10 Market is projected to reach US$ 49.9 Billion by 2033, growing from US$ 28.0 Billion in 2026 at a CAGR of 8.6% during the 2026-2033 forecast period. This is driven by mandatory digital health compliance, AI-assisted coding adoption, and global ICD-10 implementation expansion.

The primary drivers are CMS-mandated ICD-10-CM/PCS compliance for all Medicare and Medicaid claims in the U.S., with annual code set updates generating recurring upgrade demand, and the transition to value-based care reimbursement under MIPS and APMs, where AAPC documents 15-20% reimbursement improvement from optimized ICD-10 coding accuracy driving healthcare provider investment.

ICD-10-CM leads the By Product Type category with approximately 72% market share. As the universal diagnostic coding system mandated for all clinical settings in the U.S. and adopted globally, ICD-10-CM generates non-discretionary recurring software investment through annual code updates managed by NCHS and CMS, covering over 70,000 diagnosis codes across all disease categories.

North America dominates the global ICD-10 Market, led by the United States’ federal mandated ICD-10-CM/PCS compliance for CMS programs, a 6,000+ hospital and 900,000+ physician addressable market, annual code update investment cycles, and the presence of global ICD-10 solution leaders including 3M, Optum, Nuance (Microsoft), and Oracle Health.

The highest-value opportunities are AI-powered Computer-Assisted Coding (CAC) systems delivering documented 30-50% productivity improvement to address chronic coder shortages, and emerging market ICD-10 digital health infrastructure expansion, including India’s Ayushman Bharat Digital Mission and China’s Healthy China 2030, creating vast new addressable markets for ICD-10 software and services globally.

The key market participants include 3M Company, Wolters Kluwer N.V., Optum Inc. (UnitedHealth Group), QuadraMed Corporation, Change Healthcare Holdings Inc., Dolbey Systems Inc., Intelligent Medical Objects Inc., TELUS Health Solutions, Nuance Communications Inc. (Microsoft), Oracle Corporation (Oracle Health), Cerner Corporation, Athenahealth Inc., and Aviacode Inc.