- Home Care & Utilities

- Wine Packaging Market

Wine Packaging Market Size, Share, and Growth Forecast 2026 – 2033

Wine Packaging Market by Product Type (Glass Bottles, Plastic Bottles), Wine Type (Still Wine, Sparkling Wine), Closure Type (Natural Cork, Technical/Synthetic Cork), Capacity (Less than 375 ml, 375-750 ml), and Regional Analysis, 2026 – 2033

Wine Packaging Market Size and Trend Analysis

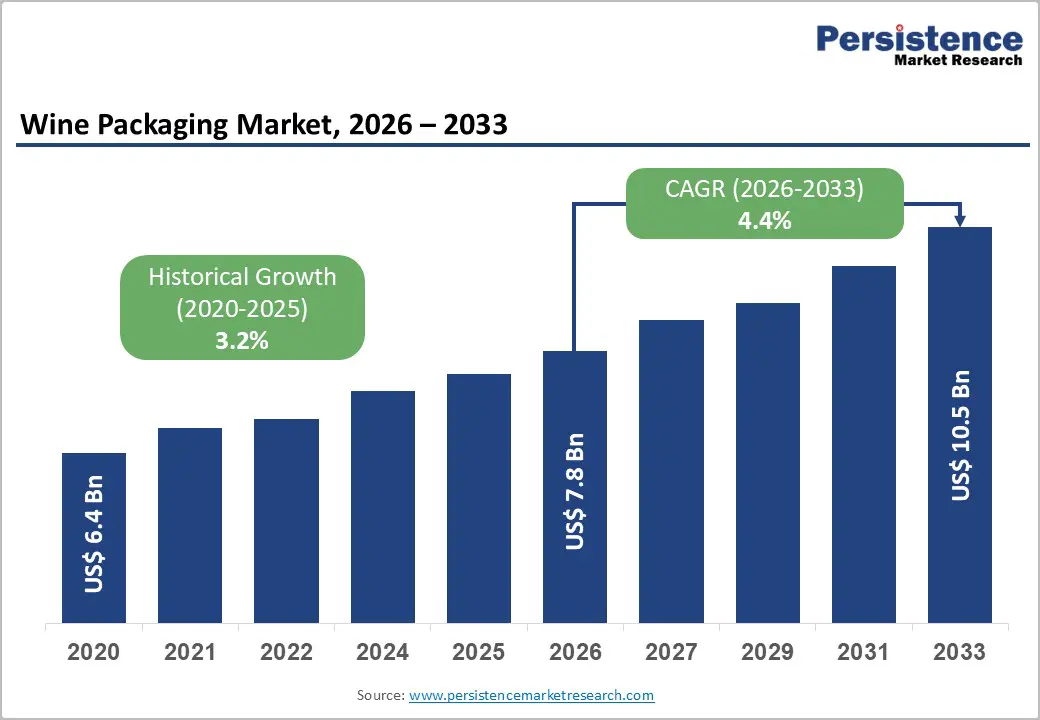

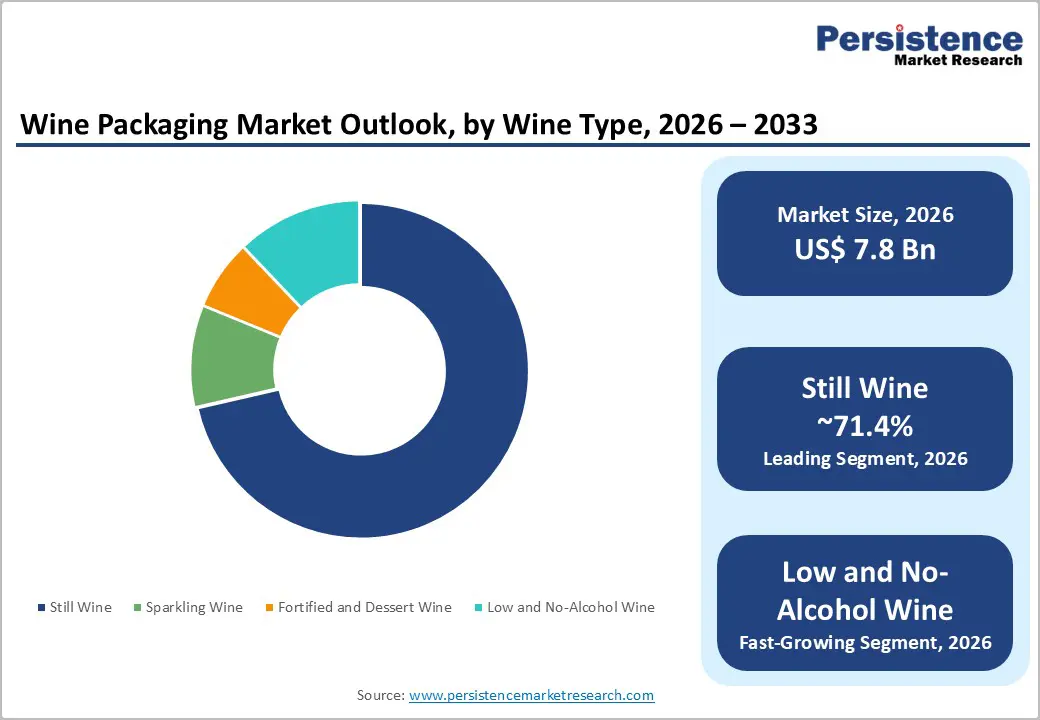

The global wine packaging market size is likely to be valued at US$7.8 billion in 2026 and is expected to reach US$10.5 billion by 2033, growing at a CAGR of 4.4% during the forecast period from 2026 to 2033, driven by a rising shift toward sustainable and lightweight packaging formats, including recycled glass and paper-based bottles. Increasing adoption of alternative formats such as bag-in-box and cans for convenience and cost efficiency is further supporting demand.

Key Industry Highlights:

- Leading Product Type: Glass bottles, approximately 69.2% share in 2026, as they are chemically inert and preserve wine quality without altering taste or aroma over time.

- Dominant Wine Type: Still wine, with a nearly 71.4% share in 2026, as they are easy to produce and compatible with multiple packaging formats.

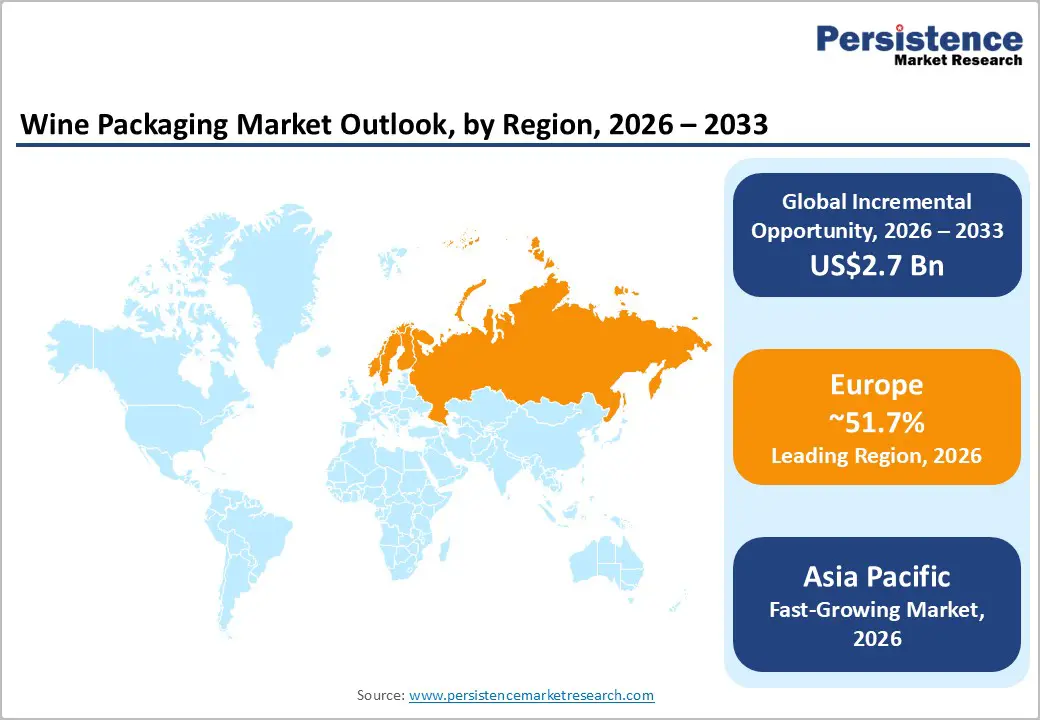

- Leading Region: Europe, with about a 51.7% share in 2026, backed by its dominant wine production and export base.

- Fast-growing Region: Asia Pacific, owing to increasing wine adoption with rising disposable income and urban lifestyles.

- Latest Product: In November 2025, Verallia launched the Burgundy Air 300G, described as the world's lightest Burgundy wine bottle. The new bottle weighs only 300 grams while maintaining the traditional Burgundy shape. It would help in reducing raw material consumption and production-related CO2 emissions by approximately 33% compared with conventional Burgundy bottles.

DRO Analysis

Driver- Climate-Friendly Formats to See High Demand in the Nordic Region

State-controlled alcohol monopolies in the Nordic countries are actively pushing Bag-In-Box (BIB) wine as a preferred format. Sweden's Systembolaget introduced strict maximum bottle weight limits effective March 2024, as part of its goal to cut environmental impact by 50% by 2030. The retailer also displays CO2 emissions for individual packaging types on its e-commerce site and provides alternative formats such as bag-in-box, pouches, and cans.

Norway's Vinmonopolet is following the same direction. Both monopolies are centering their 2025 procurement tenders around climate-friendly formats such as bag-in-box, PET bottles, pouches, and lightweight glass. This policy-led push has structural advantages. Nordic alcohol monopolies are generally regarded as ambitious in sustainability, and their monopoly position helps since consumers have limited options to buy elsewhere. This creates a reliable volume channel for BIB producers that no other region can replicate easily.

Increasing Demand for Canned and PET Single-Serve Wines in Oceania

Australia's deeply outdoor-oriented lifestyle is a natural fit for portable wine formats. Ian Batt, founder of Australia's Small Things Wine, explains that Australians spend much of their lives outdoors, at the beach, hiking, camping, or at picnics, and glass wine bottles are heavy and inconvenient once opened. This has pushed wineries to embrace canned formats. Leading players are already in the game.

Industry executives from Pernod Ricard Pacific noted in 2024 that casual social occasions are pushing consumers toward sessionable formats, and small formats such as canned wine are well-suited to those settings. New Zealand is also seeing similar signals. New Zealand Winegrowers highlighted that premiumization, provenance, and sustainability are the key drivers influencing wine packaging decisions in the year ahead. Collectively, these trends are accelerating demand for single-serve, break-resistant, and easily chillable formats across the Oceania region.

Restraint- Soda Ash Price Hikes to Push Up the Cost of Glass Bottles

Soda ash is one of the primary raw materials used to make glass wine bottles. When its price moves sharply, glassmakers feel it fast. Soda ash prices dropped by 23% in the second quarter of 2024 due to oversupply, but supply chain disruptions, rising logistics costs, and geopolitical tensions have created a challenging marketplace for sourcing the material. Energy costs have compounded the issue. In 2024, the average price of glass wine bottles rose by 4%, boosted by rising energy costs, as reported by Independent Commodity Intelligence Services (ICIS).

Wineries have been left with little choice but to pass costs on. Wineries across the U.S. implemented broad price adjustments in late 2024 and throughout 2025 to offset inflation in labor, glass, logistics, and energy, with those increases set to be fully reflected in 2026. Key challenges for the glass bottle market include volatility in energy and soda ash costs, along with freight constraints and rising pressure from alternative formats such as cans and cartons in entry-price tiers.

Opportunity - Sustainability Certifications at Vineyards Open the Door to Bio-Based Closures

As more vineyards pursue formal sustainability certifications, the pressure to comply with green credentials in packaging, including closures, is intensifying. Programs such as Napa Green focus on climate action, regenerative agriculture, and carbon neutrality, while SIP Certified covers over 43,000 acres and requires strict environmental compliance, renewed annually. Closure manufacturers are responding.

Nomacorc launched its Select Bio Series closure, made from renewable polymers derived from sugarcane and marketed as 100% recyclable with a net-zero carbon footprint. It has immediately drawn interest from certified sustainable wineries such as Bodegas Castro Martin in Spain. Italy-based Tapì has gone further, gaining ISCC PLUS certification for chemically recycling plastic closures, a process that produces plastic of the same quality as virgin material. As certification adoption spreads, bio-based and technically certified closures will likely move from a niche preference to a procurement standard.

China's Appetite for Premium Wines to Spur Demand for Unique Bottle Designs

China's wine drinkers are not just buying wine, but they are buying into a presentation. Affluent middle and upper-middle-class consumers in the country often associate wine with social status and are willing to pay a premium for high-quality imports, especially from regions such as Bordeaux, Burgundy, and Napa Valley. This buying behavior influences packaging expectations. Drinking occasions have evolved into a concept of gift-giving and personal tasting, with local wine enthusiasts moving toward a luxury-oriented lifestyle.

China's market is surging rapidly, with producers investing in innovative packaging solutions that improve product appeal and convenience as wine consumption rises among younger consumers and a surging middle class. Domestic bottle manufacturers are already catering to this shift. Premium bottle makers now provide intricate embossed patterns, engraved logos, and unique shapes specifically to help wineries build a high-end brand image in the premium wine segment.

Category-wise Analysis

Product Type Insights

Glass bottles are predicted to lead with a share of approximately 69.2% in 2026, as they are chemically inert. They do not react with wine, even over long storage periods. This is important for premium wines that are aged for years. According to studies cited by the International Organization of Vine and Wine, even minor packaging interactions can alter aroma compounds, which is why glass is still the reference material for quality preservation.

Bag-in-box segment is estimated to be the fastest-growing segment over the forecast period, as it solves wastage and convenience issues. Once opened, the wine inside the bag does not come in contact with air. It can stay fresh for weeks. This is a key advantage over bottles, where oxidation starts within days. The Australian Government Wine Australia has highlighted that bag-in-box reduces spoilage in household consumption settings.

Wine Type Insights

Still wines are anticipated to dominate with a share of nearly 71.4% in 2026, as they are simple to produce and package. They do not require secondary fermentation like sparkling wines. This reduces production complexity and packaging pressure requirements. As noted by the Food and Agriculture Organization (FAO), still wines account for the majority of global wine output due to low processing requirements.

Low- and no-alcohol wines are expected to remain in the second position in 2026 owing to health-driven consumer shifts. Several consumers are reducing alcohol intake but do not want to leave the wine category. Packaging is evolving alongside this trend. These wines are often sold in small bottles and cans, supporting moderation. Brands are also using modern, minimal designs to differentiate from traditional wine. This creates a new identity rather than imitating conventional products.

Regional Insights

Europe Wine Packaging Market Trends

Europe will likely dominate globally over the forecast period with a share of nearly 51.7% in 2026, as it is the world's largest wine-producing and wine-exporting region. According to the European Commission, the European Union accounts for more than 60% of global wine production and nearly half of global wine consumption. The region is home to leading wine-producing countries such as France, Italy, and Spain, creating sustained demand for glass bottles, closures, labels, cartons, and premium packaging solutions.

Italy Wine Packaging Market Trends

Italy will likely register a substantial share of approximately 54.3% in 2026, as it remains the world's largest wine producer and continues to strengthen its export presence. According to data presented during Vinitaly 2026, the country produced nearly 47.3 million hectoliters of wine in 2025 and maintained its position as the leading global producer. The country is also investing heavily in premiumization. Local wineries are constantly using premium glass bottles, embossed labels, and sustainable packaging to differentiate products in export markets. Demand is particularly high for wines carrying DOC and DOCG certifications, which require premium presentation and branding.

France Wine Packaging Market Trends

A share of around 24.4% is predicted to be held by France in 2026, owing to its superior premium wine culture and global reputation. Many of the world's most recognized wine regions, including Bordeaux and Burgundy, rely heavily on premium packaging to strengthen brand identity. Local wineries are now adopting lightweight bottles to reduce emissions while maintaining luxury appeal. Packaging suppliers are responding with unique glass solutions that lower carbon footprints without compromising aesthetics. The country's export-oriented wine market also supports consistent packaging demand.

Asia Pacific Wine Packaging Market Trends

Asia Pacific is anticipated to be the fastest-growing market in 2026 with a share of nearly 23.6%, as wine consumption is broadening from a relatively low base. Rising disposable income, urbanization, and exposure to Western lifestyles are encouraging wine adoption across several countries. The region is also witnessing steady growth in alternative wine categories. Low- and no-alcohol wines, sparkling wines, and ready-to-drink wine formats are gaining popularity among younger consumers. These trends are creating demand for innovative packaging formats such as cans, bag-in-box solutions, and small bottle sizes.

China Wine Packaging Market Trends

China will likely lead in Asia Pacific in 2026 with a share of around 40.8%, as it remains one of the largest wine-consuming markets in Asia Pacific despite recent market fluctuations. A rising middle class continues to view wine as a premium and sophisticated beverage, mainly in urban areas. Packaging innovation is playing an important role. Several domestic and international brands are introducing premium bottles, gift packaging, and digitally enabled labels featuring QR codes for product authentication. These features are especially valuable in China, where brand trust and authenticity are important purchasing factors.

Australia Wine Packaging Market Trends

In 2026, Australia is projected to account for a share of approximately 29.8%. The country remains one of the world's leading wine producers and exporters, supporting significant demand for wine packaging. The country is also emerging as a leader in sustainable packaging. In 2025, several local wineries partnered with SIG to launch the country's first recycle-ready bag-in-box wine packaging. This reflects rising interest in low-carbon packaging solutions. However, Australia-based producers face challenges from declining global wine consumption and weak export demand in some markets. Hence, few wineries are focusing on innovation, light packaging formats, canned wines, and low-alcohol products to attract consumers.

North America Wine Packaging Market Trends

North America is predicted to showcase steady growth in 2026 with a share of approximately 17.9%, as consumers continue to shift toward premium and sustainable wine products. Various wineries are investing in packaging upgrades, including lightweight glass bottles, recyclable materials, and premium labeling solutions. The region is also experiencing growth in alternative packaging formats. Bag-in-box wines, canned wines, and single-serve packaging are becoming more common, especially among Gen Z and millennial consumers seeking convenience and portability.

U.S. Wine Packaging Market Trends

A share of nearly 56.3% is expected to be held by the U.S. in 2026, as it remains one of the largest wine markets globally and continues to support substantial demand for bottles, closures, labels, and shipping packaging. Future growth is likely to come from premiumization rather than volume expansion. Several wineries are investing in luxury bottle designs, sustainable materials, and smart packaging technologies that improve traceability and consumer engagement.

Competitive Landscape

The global wine packaging market is moderately fragmented with the presence of large multinational packaging companies and several regional glass bottle, closure, carton, and flexible packaging manufacturers. Traditional suppliers such as Amcor, Ardagh Group, O-I Glass, Ball Corporation, Verallia, and Vidrala are investing heavily in reducing packaging weight, increasing recycled content, and lowering carbon emissions.

A few wine producers are increasingly adopting aluminum cans, bag-in-box solutions, paper bottles, and aseptic cartons to reduce transportation costs and environmental impact. This has opened opportunities for companies specializing in flexible and paper-based packaging. Strategic partnerships and product innovation have also become key competitive tools.

Key Industry Developments

- In January 2026, premium boxed wine producer Gratsi announced a key retail expansion across the U.S. after steady growth in its bag-in-box wine business during 2025. This expansion shows increasing consumer acceptance of boxed wine packaging and surging retailer support for alternative wine packaging formats.

- In January 2026, Chateau Ste. Michelle launched a unique packaging redesign following its acquisition by The Wyckoff Family. The company introduced updated bottle and label packaging featuring embossed elements, textured paper, and premium visual cues aimed at strengthening the brand's premium positioning in the wine market.

- In January 2026, Avantium entered into a capacity reservation agreement with Packamama to support the development of plant-based and recyclable PEF materials for wine packaging. The companies indicated that the collaboration would facilitate the future production of lightweight wine bottles with a lower carbon footprint using Avantium's Releaf polymer technology.

Companies Covered in Wine Packaging Market

- Owens-Illinois Inc. (O-I)

- Verallia SA

- Ardagh Group SA

- Saverglass SAS

- Vetropack Holding AG

- BA Glass Group

- Consol Glass Pty Ltd

- Guala Closures Group

- Amorim Cork, S.A.

- Vinventions LLC (Nomacorc)

- Amcor plc

- Ball Corporation

- TricorBraun Inc.

- Tetra Laval International SA

- SIG Combibloc Group AG

- Scholle IPN (Sealed Air)

- Liqui-Box (Sealed Air)

- International Paper Company

- G3 Enterprises Inc.

- Maverick Enterprises Inc.

- Encore Glass Inc.

- Smurfit WestRock

- Crown Holdings, Inc.

- Others

Frequently Asked Questions

The global wine packaging market is projected to be valued at US$7.8 billion in 2026.

The market is expected to reach US$10.5 billion by 2033.

Key market trends include the shift toward sustainable packaging and increasing focus on premium packaging designs.

Glass bottles are expected to be the leading product type with a share of nearly 69.2% in 2026, as they are recyclable, making them suitable for both luxury positioning and sustainability goals.

The market is expected to grow at a CAGR of 4.4% from 2026 to 2033.

Owens-Illinois Inc. (O-I), Verallia SA, and Ardagh Group SA are a few key market players.