- Inks, Coatings, Adhesives & Sealants (ICAS)

- Wind Turbine Coatings Market

Wind Turbine Coatings Market Size, Share, and Growth Forecast 2026 - 2033

Wind Turbine Coatings Market by Material Type (Epoxy, Polyurethane, Acrylic, Fluoropolymer, Silicone, Others), Layer Type (Primer Coatings, Topcoat Coatings, Repair Coatings), Application Method (Spray Coating, Roller Coating, Brush Coating, Powder Coating), Application Stage (OEM, Maintenance & Repair), End-user (Onshore Wind Turbines, Offshore Wind Turbines), Regional Analysis, 2026 - 2033

Wind Turbine Coatings Market Size and Trend Analysis

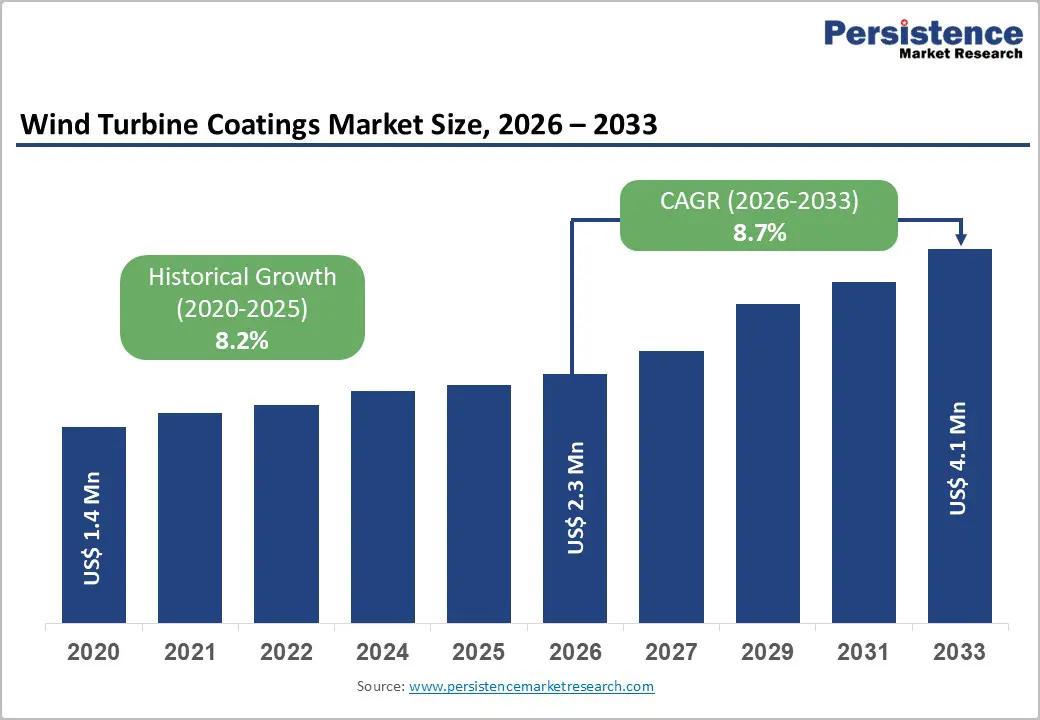

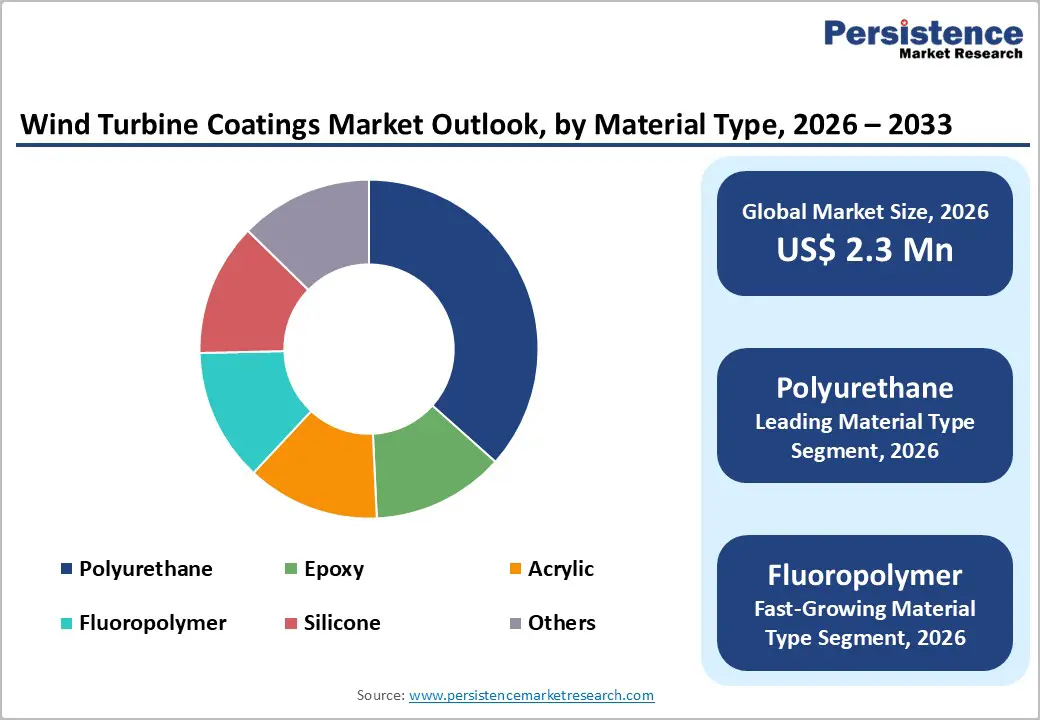

The global wind turbine coatings market size is expected to be valued at US$ 2.3 billion in 2026 and projected to reach US$ 4.1 billion by 2033, growing at a CAGR of 8.7% between 2026 and 2033.

This robust growth is driven by a convergence of record-setting global wind energy installations, the rapid scale-up of offshore wind capacity, and tightening performance requirements for turbine protection coatings in increasingly harsh operating environments. According to the Global Wind Energy Council (GWEC), the world installed a record 117 GW of new wind capacity in 2024, bringing cumulative global wind capacity to 1,136 GW across 55 countries. GWEC forecasts an additional 981 GW of new capacity by 2030 at a compound annual growth rate of 8.8% for the wind industry, a trajectory that will require tens of thousands of turbines to be coated at OEM stage and maintained across multi-decade operational lifespans, consistently expanding the addressable market for high-performance wind turbine coatings through 2033.

Key Industry Highlights

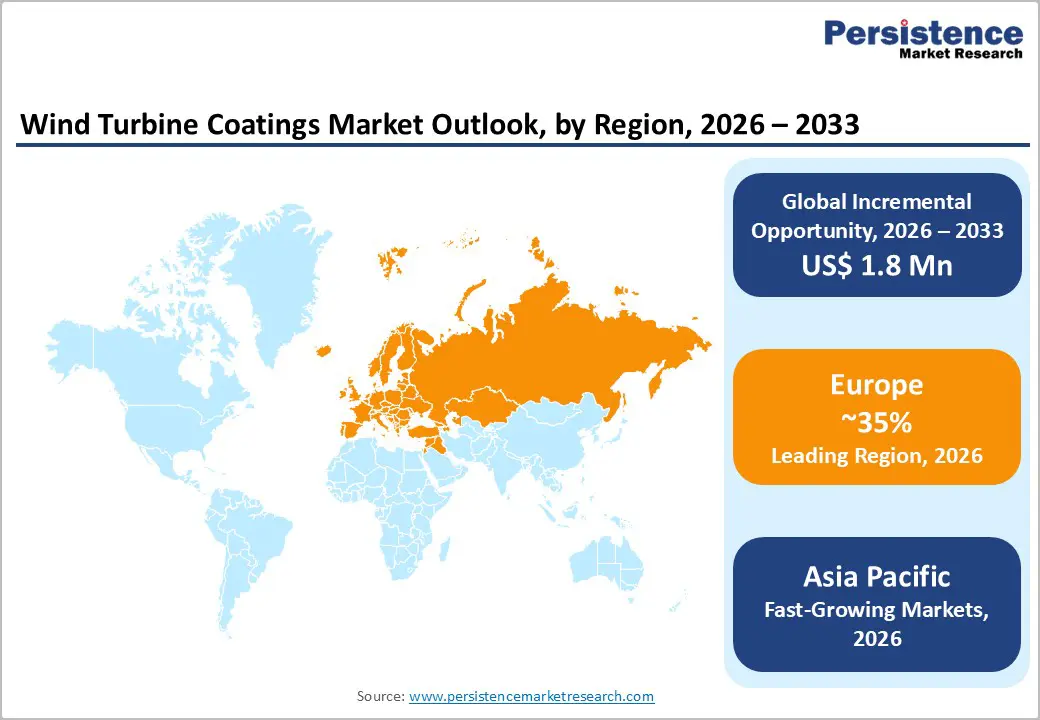

- Leading Region: Europe leads the global Wind Turbine Coatings market with approximately 35% share in 2025, driven by the world's largest offshore wind fleet, record 23.2 GW of offshore auction awards in 2024, and a concentration of major coating OEMs including Hempel, Jotun, and AkzoNobel.

- Fastest Growing Region: Asia Pacific is the fastest-growing region through 2033, anchored by China's record 86.9 GW of new wind installations in 2024, 72% of global additions, India's 140 GW wind target by 2030, and rapidly expanding offshore wind programmes across South Korea and Taiwan.

- Dominant Segment: Polyurethane coatings lead with approximately 38% market share in 2025, valued for superior UV durability, flexibility, and erosion resistance in turbine topcoat and leading edge protection applications, PPG's polyurethane series reduced reapplication intervals by 30% in 2024.

- Fastest Growing Segment: Offshore Wind Turbines is the fastest-growing end-use segment, with GWEC forecasting an 8-fold increase in annual offshore installations by 2034, driving premium anti-corrosion coating demand at per-turbine values significantly exceeding onshore applications.

- Key Market Opportunity: Approximately 25,000 European wind turbines will reach design-life milestones by 2030 per IRENA, creating a structurally growing MRO coating market. Companies offering blade LEP repair systems and long-term coating lifecycle service agreements are well positioned for recurring revenue.

| Key Insights | Details |

|---|---|

| Wind Turbine Coatings Market Size (2026E) | US$ 2.3 Billion |

| Market Value Forecast (2033F) | US$ 4.1 Billion |

| Projected Growth CAGR (2026 - 2033) | 8.7% |

| Historical Market Growth (2020 - 2025) | 8.2% |

DRO Analysis

Drivers - Record Global Wind Energy Installations Fuelling Coating Demand at Scale

The most fundamental driver of the Wind Turbine Coatings market is the unprecedented and accelerating pace of global wind energy deployment. According to the Global Wind Energy Council (GWEC)'s Global Wind Report 2025, the world installed a record 117 GW of wind capacity in 2024, comprising 109 GW of onshore and 8 GW of offshore wind, with a cumulative installed base now reaching 1,136 GW. GWEC projects consecutive record installation years through 2030, with 138 GW in 2025, 140 GW in 2026, escalating to 194 GW by 2030.

Each turbine installed requires multiple layers of protective coatings across blades, towers, nacelles, and foundations, representing a direct and compounding coating consumption volume. In 2024 alone, 23,098 wind turbines were installed globally by 29 manufacturers. As the average turbine rated capacity reaches nearly 5,500 kW in 2024, up 9% year-on-year, larger turbines carry greater surface area per unit and higher coating material requirements per installation, amplifying per-turbine coating demand growth.

Offshore Wind Expansion Driving Premium Anti-Corrosion Coating Specification

Offshore wind turbines represent the most coating-intensive application in the market, demanding advanced anti-corrosion, anti-fouling, and leading-edge erosion protection systems engineered to withstand prolonged marine salt spray, UV irradiation, high humidity, and wave splash zone exposure. According to the GWEC Global Offshore Wind Report, global offshore wind cumulative capacity reached 83 GW by the end of 2024, with 48 GW currently under construction worldwide and auctions of 56.3 GW awarded in 2024 alone, the highest single-year auction volume ever recorded.

GWEC forecasts an 8-fold increase in annual offshore installations from 2025 to 2034, from 16 GW to 55 GW per annum, creating sustained and rapidly growing demand for the highest-performance coating systems. Offshore wind towers, monopile foundations, and transition pieces are exposed to splash zone corrosion that can degrade unprotected steel within months, making robust multi-layer coating systems, including marine-grade epoxy primers, polyurethane topcoats, and cathodic protection integration, a non-negotiable operational requirement throughout the asset life.

Restraints - High Application Complexity and Offshore MRO Access Challenges

Wind turbine coatings, particularly for offshore assets, present significant logistical and technical challenges that constrain seamless market adoption. Offshore turbine maintenance and recoating operations require specialized access equipment (rope access, suspended platforms, or jack-up vessels), favourable weather windows, and highly trained coating applicators certified to marine and industrial standards including NACE/AMPP and SSPC (Society for Protective Coatings).

Approximately 47% of offshore coating maintenance programmes are delayed due to labour availability and equipment scheduling constraints. For rotating blade components, leading edge protection (LEP) repairs at height in dynamic marine conditions demand formulations compatible with minimum application temperature ranges and short recoat windows, complicating in-situ repair delivery and increasing maintenance cycle costs for wind farm operators.

Volatile Raw Material Costs and Environmental Reformulation Pressure

Wind turbine coating formulators face persistent cost pressure from raw material volatility, particularly in isocyanates, epoxy resins, and fluoropolymer intermediates, whose pricing is directly linked to petrochemical supply chains and subject to disruption from energy market cycles and OPEC+ production decisions. Simultaneously, tightening environmental regulations are mandating reformulation toward lower-VOC and waterborne technologies: the European Union's Industrial Emissions Directive (IED) and REACH framework are progressively restricting solvent-based coating chemistries.

In the United States, the U.S. Environmental Protection Agency (EPA) has expanded VOC emission limits applicable to industrial coating operations. While waterborne and powder technologies are commercially available, performance parity with established solvent-borne systems in extreme-environment wind applications has not yet been fully demonstrated, creating a technical and cost transition burden for manufacturers.

Opportunities - Leading Edge Erosion Protection Coatings for Mega-Turbine Blades

The rapid scale-up in wind turbine blade length presents an acute and commercially significant opportunity for advanced leading edge protection (LEP) coating systems. As turbine rotor diameters expand, rotors larger than 180 metres now represent 58.6% of global installations in 2024, up from 42.9% in 2023 (GWEC), blade tip speeds at the outer section regularly exceed 90-100 metres per second, creating severe rain and particle erosion at leading edges that can reduce annual energy yield by up to 5% within the first three years of operation if unprotected.

In 2024, PPG Industries launched a new highly durable anti-corrosion and erosion-resistant coating series specifically designed for offshore wind turbines, while AkzoNobel developed an edge-retentive coating that decreased annual coating failures by approximately 24% across European offshore installations. The offshore segment, where a single unplanned shutdown can cost €20,000-€50,000 per turbine per day, creates strong willingness-to-pay for premium LEP solutions with extended service intervals.

MRO Coating Market Expansion Across Aging Onshore Wind Fleet

A structurally growing opportunity exists in the maintenance, repair, and overhaul (MRO) coating segment as the global installed wind fleet ages. According to IRENA (International Renewable Energy Agency), approximately 25,000 wind turbines will reach end-of-design-life in Europe by 2030, with a significant portion requiring either repowering with coating-intensive new turbines or life-extension programmes involving comprehensive recoating of blades, towers, and structural elements. The MRO segment is the fastest-growing application stage category, as coatings on onshore turbines typically require partial or full recoating at 10-15 year intervals.

In October 2024, Hempel A/S entered a strategic partnership with a leading wind turbine OEM to co-develop a customized integrated coating solution, reflecting the growing commercial value of long-term OEM-and operator-coating service agreements. Companies offering combined OEM supply, field application services, and digital coating lifecycle monitoring are positioned to capture significant recurring revenue from the MRO segment through 2033.

Category-wise Analysis

Material Type Insights

Polyurethane is the leading material type in the Wind Turbine Coatings market, commanding approximately 38% of global market share in 2025. Polyurethane-based coatings dominate the wind turbine topcoat and leading edge protection categories owing to their superior combination of flexibility, abrasion resistance, UV durability, and resistance to moisture-driven hydrolysis, critical properties for components operating in outdoor and offshore environments. Blade-tip and nacelle components that experience high mechanical and UV stress particularly benefit from polyurethane's elastomeric properties, which allow coatings to flex with substrate movement without cracking.

In 2024, PPG Industries launched an advanced polyurethane-based coating series that reduced reapplication intervals by up to 30% and was adopted by over 22% of wind farms in coastal regions for nacelle and tower protection. The fastest-growing material type is Fluoropolymer coatings, driven by growing deployment in ultra-harsh offshore environments where their exceptional chemical resistance, low surface energy (ice-phobic properties), and multi-decade service life justify their premium cost.

Layer Type Insights

Topcoat Coatings represent the leading layer type segment, accounting for approximately 46% of global wind turbine coatings revenue in 2025. Topcoats constitute the primary protective interface between turbine surfaces and the operating environment, providing UV resistance, colour stability, anti-erosion performance, and resistance to salt spray, rain, and industrial pollutants. As the most visible and performance-critical coating layer, and the one most frequently requiring in-situ maintenance, spot repair, or full overhaul across turbine operational lifespans, topcoat consumption volumes are substantial and recurring.

Waterborne coatings already dominate the topcoat category, accounting for over 50% of global wind energy coating revenue in 2025 by value, driven by low-VOC regulatory compliance. The fastest-growing layer type is Repair Coatings, including field-applied leading-edge protection systems and patch repair kits, reflecting the expanding MRO market across the ageing global onshore fleet.

Application Method Insights

Spray Coating is the dominant application method in the wind turbine coatings market, holding approximately 58% of global market share in 2025. Spray application, encompassing airless spray, air-assisted airless, and electrostatic spray techniques, delivers the consistent film build, uniform thickness, and high transfer efficiency required for large-surface-area turbine components such as tower sections, nacelle shells, and blade bodies. At OEM facilities, automated spray lines enable high-throughput, quality-controlled coating of standardized blade and tower components with minimal material waste.

In the field, rope-access spray applicators and remotely operated spray systems are increasingly employed for turbine blade re-coating and LEP repairs. SSPC (Society for Protective Coatings) certification requirements for spray application operators have driven industry-wide quality standardization. The fastest-growing method is Powder Coating, driven by near-zero VOC emissions, high transfer efficiency, and superior corrosion resistance, particularly for steel turbine tower segments and structural components.

Application Stage Insights

OEM (Original Equipment Manufacturer) application is the leading application stage, representing approximately 61% of global wind turbine coatings revenue in 2025. OEM-stage coating is performed in controlled factory environments on newly manufactured turbine components, including tower sections, nacelle housings, generator components, and blades, where temperature, humidity, surface preparation, and coating application parameters can be precisely controlled to achieve specified film thicknesses and performance characteristics.

In 2024, a record 23,098 wind turbines were mechanically installed worldwide (GWEC), each requiring comprehensive multi-layer OEM coating across all structural and rotating components. Factory-applied coatings offer superior adhesion and quality consistency versus field application, making OEM the preferred and highest-volume stage. The fastest-growing application stage is Maintenance & Repair (MRO), expanding at the highest CAGR, driven by the aging global turbine fleet, LEP maintenance cycles, and life-extension programmes for turbines approaching design-life milestones.

End-user Insights

Onshore Wind Turbines constitute the leading end-use segment, accounting for approximately 72% of global wind turbine coatings market share in 2025. This dominance directly reflects the compositional structure of the global wind fleet, according to GWEC, onshore wind represented 109 GW of the 117 GW installed in 2024 (approximately 93% of annual installations), with the global cumulative onshore base far exceeding offshore in absolute installed capacity. In 2024, China alone added 79.8 GW of onshore wind capacity, a volume requiring enormous OEM coating consumption across blades, nacelles, and towers. However, the fastest-growing end-use segment is Offshore Wind Turbines, registering the highest revenue CAGR through 2033. GWEC forecasts offshore annual installations to increase from 16 GW in 2025 to 55 GW by 2034, an 8-fold increase, with premium anti-corrosion and LEP coatings required across offshore assets driving significantly higher per-turbine coating revenue compared to onshore applications.

Regional Insights

Europe Wind Turbine Coatings Market Trends and Insights

Europe is the leading region in the global Wind Turbine Coatings market, commanding approximately 35% of global revenue share in 2025. This dominance is underpinned by the region's status as the world leader in offshore wind development, home to the majority of global operational offshore capacity, and by the highest concentration of coating OEMs serving wind turbine manufacturers. The GWEC Global Offshore Wind Report confirms that Europe awarded 23.2 GW of offshore wind capacity in 2024 auctions alone, more than any other region, with Germany awarding a record 11 GW of onshore wind in procurement mechanisms, 72% higher than 2023. Jotun secured a major contract to supply coatings for a large European offshore wind farm in October 2024, while AkzoNobel reported strong growth in its wind energy coatings segment driven by European demand in March 2024.

The United Kingdom, home to the world's largest operational offshore wind fleet, and Germany continue to drive premium anti-corrosion coating demand. The UK's Contracts for Difference (CfD) Allocation Round 6 is expected to support significant new offshore capacity, sustaining coating demand across the project pipeline. European coating companies including Hempel A/S, Jotun, AkzoNobel, and Teknos Group are investing in low-VOC, waterborne wind turbine coating technologies to meet the EU Industrial Emissions Directive (IED) and REACH framework requirements, while concurrently developing enhanced performance systems for deep-water floating wind turbine applications.

Asia Pacific Wind Turbine Coatings Market Trends and Insights

Asia Pacific is the fastest-growing regional market through 2033, registering the highest CAGR in the global Wind Turbine Coatings market, driven predominantly by China, India, and expanding Southeast Asian wind energy programmes. According to the World Wind Energy Association (WWEA), China passed the 500,000 MW (500 GW) installed wind capacity milestone in 2024, adding 86,892 MW of new capacity in 2024 alone, accounting for 72% of total global new wind installations. This extraordinary installation pace translates into an unprecedented demand for OEM turbine coatings from Chinese and global coating suppliers. China led global offshore wind installations for the seventh consecutive year in 2024 according to GWEC, with 4 GW of new offshore capacity added.

India is the region's fastest-growing sub-market: the World Wind Energy Association (WWEA) recorded India adding 3,420 MW of new wind capacity in 2024, ranked fourth globally, with the country's wind energy target of 140 GW by 2030 under the National Electricity Plan creating a long-term pipeline for turbine coatings demand. In 2024, Asia-Pacific as a whole experienced 7% year-on-year growth in new wind installations (GWEC). Nippon Paint (Singapore) Co. Pte Ltd has expanded its wind energy coatings portfolio specifically for Asian markets, while Sherwin-Williams and PPG have strengthened distribution networks in the region to capture growing OEM and MRO coating demand.

North America Wind Turbine Coatings Market Trends and Insights

North America represents the third-largest regional market, with the United States accounting for approximately 73% of regional revenue in 2025. The U.S. added 4,058 MW of wind capacity in 2024, ranking second globally in new installations per GWEC, though the World Wind Energy Association noted this represented the U.S. wind market's slowest growth in over a decade (4.2 GW total for 2024) as policy uncertainty moderated near-term development. The U.S. cumulative installed capacity reached 155 GW at end-2024 (WWEA), creating a substantial base for MRO coating demand. The Inflation Reduction Act (IRA) extended Production Tax Credits (PTCs) and Investment Tax Credits (ITCs) for wind energy through 2032, supporting long-term project development and sustaining coating consumption.

The offshore wind sector presents the region's most significant near-term coating growth opportunity: 56.3 GW of offshore capacity was awarded globally in auctions in 2024 (GWEC), with North American developers part of this pipeline. 3M, headquartered in the U.S., is a leading supplier of wind turbine blade protection tape and repair films, while PPG Industries and Sherwin-Williams serve the North American wind turbine market through specialized product lines compliant with NACE/AMPP MR0175 and SSPC coating standards. Brazil, ranked the world's second-largest market for new wind turbines in 2024 with 5.4 GW installed per WWEA, represents Latin America's dominant and fastest-growing wind coating market.

Competitive Landscape

The global wind turbine coatings market is moderately consolidated, with a limited number of large multinational suppliers accounting for a significant share of revenue, supported by regional and niche players. The market structure is defined by high technical requirements, strict environmental regulations, and strong integration with turbine OEMs, creating entry barriers and reinforcing the position of established manufacturers.

Key business strategies focus on developing application-specific coating systems, including anti-corrosion solutions for offshore environments and advanced, leading-edge protection for blades. Companies are investing in low-VOC and waterborne formulations to meet evolving regulatory standards, while expanding digital capabilities for coating performance monitoring and lifecycle management. Strategic partnerships with turbine manufacturers and service providers are critical for securing long-term contracts.

Key Developments:

- March 2026: AkzoNobel (International brand) launched RELEST Wind EP Process Coat, a solvent-free epoxy in-mould coating designed for wind blade production, enabling faster curing, reduced application time, and improved efficiency under higher mould temperature conditions.

- October 2024: Hempel A/S entered a strategic partnership with a leading global wind turbine manufacturer to co-develop a customized integrated coating solution for next-generation multi-megawatt offshore turbines, targeting the growing offshore MRO segment.

- January 2024: PPG Industries launched a new, highly durable anti-corrosion coating specifically designed for offshore wind turbines, emphasizing long-term performance in marine environments and reducing reapplication intervals by up to 30% across nacelle and tower applications.

Companies Covered in Wind Turbine Coatings Market

- AkzoNobel

- PPG Industries

- Sherwin-Williams

- Axalta Coating Systems

- Teknos Group

- Hempel A/S

- Jotun

- Sika AG

- 3M

- Bergolin GmbH & Co. KG

- Nippon Paint (Singapore) Co. Pte Ltd

- Huisins Coatings

- Mankiewicz Gebr. & Co.

- BASF SE

- Duromar, Inc.

- MEGA P&C (Protective Coatings)

- Belzona Polymerics Ltd.

- Feilu Coatings

- Covestro AG

Frequently Asked Questions

The global Wind Turbine Coatings market is valued at US$ 2.3 billion in 2026 and is projected to reach US$ 4.1 billion by 2033 at a CAGR of 8.7%.

Demand is driven by rising wind energy installations, offshore wind expansion, and increasing maintenance and repair of aging turbines.

Europe leads the market with around 35% share due to strong offshore wind capacity and presence of major coating manufacturers.

Key opportunities lie in advanced leading edge protection coatings and the expanding MRO segment for aging wind turbines.

Key players include Hempel, AkzoNobel, PPG Industries, Jotun, Sherwin-Williams, Teknos, 3M, Sika, Axalta, Bergolin, and Nippon Paint.