- Non-food Packaging

- Western Europe Steel Drums Market

Western Europe Steel Drums Market Size, Share, and Growth Forecast 2026 - 2033

Western Europe Steel Drums Market by Material (Carbon Steel, Stainless Steel), Capacity (Up to 10 Gallons, 10-30 Gallons, 31-50 Gallons), by Product Type (Tight Head, Open Head), by End-use Industry, and Country Analysis, 2026 - 2033

Western Europe Steel Drums Market Size and Trends Analysis

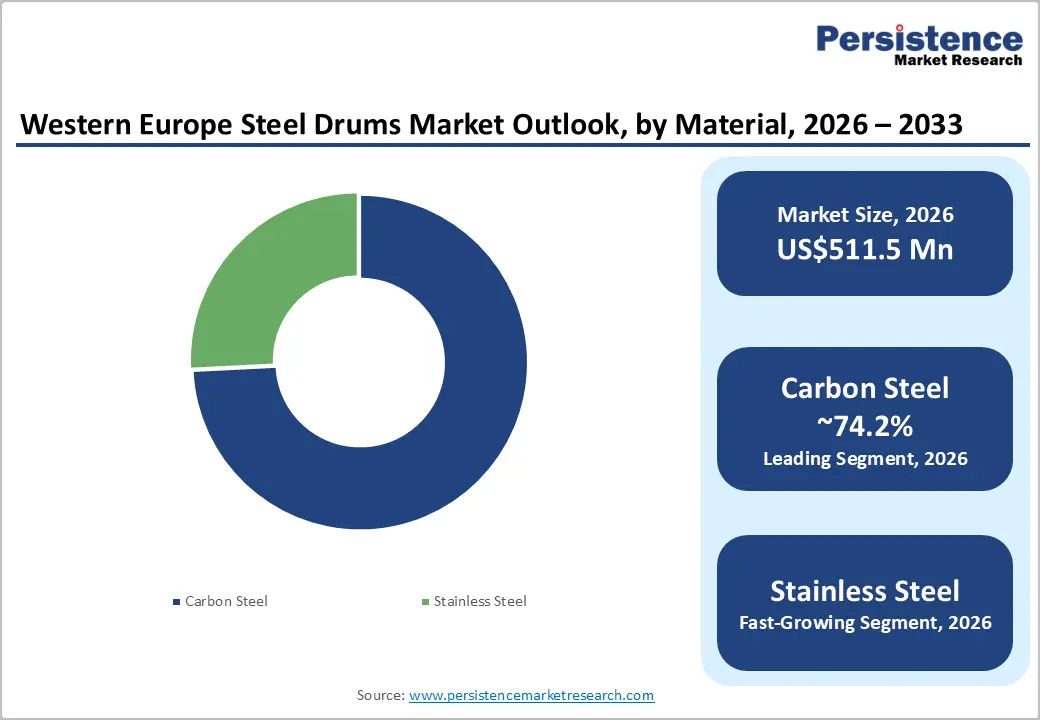

The Western Europe steel drums market size is likely to be valued at US$511.5 million in 2026 and is predicted to reach US$710.1 million by 2033, growing at a CAGR of 4.8% during the forecast period from 2026 to 2033, driven by the rising demand from the chemical and petrochemical industries for safe and durable bulk packaging solutions.

Growth is further fostered by increasing adoption of reconditioned and recyclable steel drums to comply with circular economy regulations across Western Europe.

Key Industry Highlights:

- Latest Product: In September 2025, Greif launched its EcoBalance Low Carbon Emission Steel Drums in partnership with ArcelorMittal. The new drums are manufactured using ArcelorMittal’s XCarb recycled and renewably produced steel. These are reported to reduce cradle-to-gate carbon emissions by approximately 60% compared with conventional steel drums.

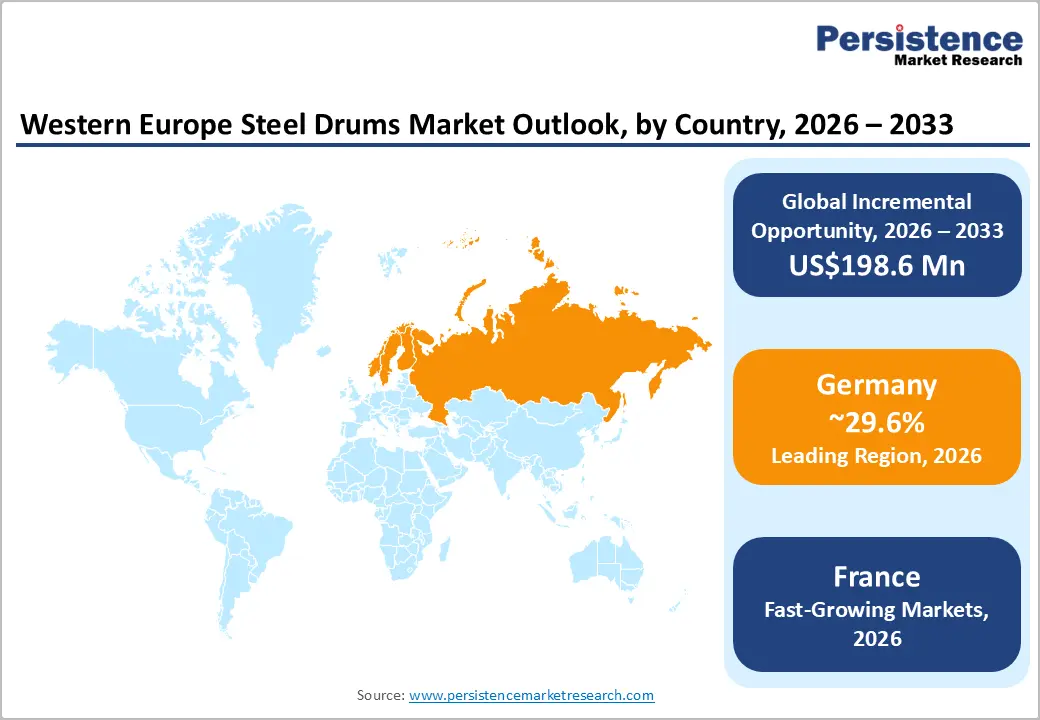

- Leading Country: Germany, with about a 29.6% share in 2026, spurred by its superior chemical manufacturing base and presence of leading industrial packaging producers.

- Fast-growing Country: France, backed by increasing investments in specialty chemicals and strict environmental regulations.

- Leading Material: Carbon steel, approximately 74.2% share in 2026, as its high recyclability complies with policies from the European Commission.

- Dominant Product Type: Open head, nearly 55.6% in 2026, backed by their ease of filling, cleaning, and reuse, making them ideal for handling solids, semi-solids, and hazardous waste.

DRO Analysis

Driver - Strict Environmental Norms and Shift toward Circular Economy

Western Europe is enforcing some of the world’s strictest environmental rules, especially through the European Union’s Circular Economy Action Plan and related 2024 to 2025 policy updates. These rules heavily penalize single-use plastics as well as push industries to adopt reusable and recyclable packaging solutions. Steel drums stand out as they can be reused dozens of times, have a service life multiple times longer than plastic containers, and can be recycled at rates exceeding 90% without losing quality.

This makes them far more compliant with EU sustainability targets than disposable alternatives. For example, the EU’s push to reduce plastic waste in the chemical and industrial sectors has boosted demand for steel drums. These qualify as infinite-cycle packaging under EU recycling frameworks. Companies in Germany, France, and the Netherlands are speedily replacing plastic pails and fiber drums with steel drums to meet corporate ESG goals and avoid plastic-related taxes.

Rising Demand for Superior Safety Performance for Hazardous Goods

Steel drums remain the gold standard for transporting and storing hazardous goods due to their unmatched rigidity, leak-proof construction, and resistance to tearing, puncturing, or collapsing under pressure. This is important in Western Europe, where strict UN-certified transport regulations govern the movement of toxic chemicals, solvents, flammable liquids, and petrochemicals. Unlike plastic or composite containers, steel drums maintain structural integrity even in extreme temperatures or during rough handling, further reducing the risk of spills, contamination, or accidents.

Regulatory bodies such as the European Chemicals Agency (ECHA) and national transport safety agencies consistently recommend or mandate steel drums for Class 3 (flammable liquids), Class 6 (toxic substances), and Class 8 (corrosives) materials. Prominent chemical manufacturers in the U.K., Belgium, and Italy rely on steel drums to comply with these safety standards, ensuring their supply chains remain audit-ready and accident-free.

Restraint - High Logistics Costs Bolstered by Heavy Tare Weight

One of the key challenges for Western Europe's steel drums market is the high weight of empty drums, which significantly increases freight and handling expenses. Steel drums have a much higher tare weight, i.e., the weight of the empty container, compared to plastic, fiber, or composite alternatives. This means more fuel is consumed during transportation, and trucks reach weight limits before maximizing volumetric capacity.

Logistics providers across the continent report that transporting empty steel drums is inherently inefficient, leading to higher per-ton handling fees and increased carbon emissions per shipment. For small and mid-sized chemical firms operating on tight margins, these added logistics costs can make steel drums less attractive despite their superior safety and sustainability benefits. This restraint is acute in landlocked regions such as southern Germany and Austria, where transport distances are longer, and freight costs are more sensitive to weight.

Opportunity - Adoption of Solvent-Free and Low-VOC Coatings

Pushed by the EU’s strict limits on Volatile Organic Compound (VOC) emissions, steel drum manufacturers in Germany, Italy, and the U.K. are swiftly transitioning to solvent-free internal and external coatings. Traditional drum linings often used solvent-based epoxies or phenolics that released harmful VOCs during curing and application. New water-based and 100% solid coatings eliminate these emissions while maintaining excellent chemical resistance and food-contact safety.

This shift is associated with the EU regulations such as the Industrial Emissions Directive and the proposed ban on bisphenol A (BPA) in food-contact materials, which took shape between 2024 and 2025. Over 7.5 million drums produced in Europe in recent years already use low-carbon steel and solvent-free coatings, pointing to a significant industry-wide transformation. Companies that adopt these coatings early gain a competitive edge by providing eco-labeled drums that meet both environmental and regulatory requirements for chemical, pharmaceutical, and food-grade applications.

Integration of Digital Traceability and Automated Quality Systems

Leading steel drum producers are now embedding digital traceability into their products through automated quality testing and unique identification markings such as data-matrix codes, RFID tags, or IoT-enabled sensors. A key example is Greif’s April 2026 launch of its Track & Trace system in Europe, which places a scannable data-matrix code on every large steel drum, giving it a unique digital identity from production to end-of-life. This allows customers to instantly verify batch numbers, manufacturing dates, UN certification status, and repair history using a smartphone or scanner.

Such systems improve compliance with UN transport regulations for hazardous goods, reduce counterfeiting, minimize errors in inventory management, and support circular economy goals by enabling precise drum lifecycle tracking. As Western Europe’s chemical and pharmaceutical industries face increasing pressure to digitize supply chains and prove regulatory compliance, steel drums with built-in traceability are becoming a preferred choice for risk-averse and efficiency-driven firms.

Category-wise Analysis

Material Insights

The carbon steel segment is predicted to lead with a share of approximately 74.2% in 2026 in Western Europe steel drums market, as it provides a smooth balance of cost, strength, and recyclability. Carbon steel drums are widely used in chemicals, paints, and petroleum as they are stronger and cheaper than stainless steel. Their high mechanical strength allows safe transport of hazardous goods over long distances. A key reason for dominance is recyclability. According to the European Commission, steel packaging achieves recycling rates above 80% in Europe under circular economy policies. This makes carbon steel drums attractive for companies trying to meet sustainability targets.

The stainless steel segment is estimated to be the fastest-growing segment over the forecast period, as industries are shifting toward high-purity and corrosion-resistant storage. Stainless steel drums are witnessing demand in pharmaceuticals, food, and specialty chemicals where contamination must be avoided. These drums resist corrosion, oxidation, and chemical reactions better than carbon steel. For example, guidance from the European Medicines Agency highlights the requirement for inert and non-reactive storage materials in drug manufacturing. This has increased the use of stainless steel drums for active pharmaceutical ingredients.

Product Type Insights

The open head segment is anticipated to dominate with a share of nearly 55.6% in 2026, as it provides flexibility for handling solid and semi-solid materials. Open head drums have removable lids, which makes them easy to fill, empty, and clean. This is important for industries dealing with powders, pastes, and viscous chemicals. Sectors such as food processing, construction chemicals, and waste management prefer this design because workers can access the entire drum interior. According to guidelines from the U.K. Health and Safety Executive, containers that allow easy inspection and cleaning reduce contamination risks in industrial handling.

The tight head segment is expected to remain in the second position in 2026, owing to rising demand for safe transport of liquids and hazardous chemicals. Tight head drums are sealed and designed for liquids, including chemicals, oils, and fuels. Growth is pushed by strict safety and leakage regulations in Europe. For example, ADR regulations under the United Nations Economic Commission for Europe (UNECE) require secure and leak-proof packaging for transporting dangerous liquids across borders.

Tight head drums meet these requirements with features such as sealed tops and controlled dispensing systems. These drums also work better with automated filling and dispensing systems used in large chemical plants.

Country Insights

Germany Steel Drums Market Trends

Germany is anticipated to dominate in 2026 with a share of nearly 29.6%, backed by the presence of a well-established chemical industry. The country is home to over 1,700 chemical companies, including global giants such as BASF, Bayer, and Dow Germany, all of which rely heavily on steel drums for storing and transporting hazardous materials. Its law strictly enforces UN-certified packaging for dangerous goods, and steel drums are the most compliant option. The Federal Institute for Materials Research and Testing (BAM) regularly audits chemical firms, and non-compliant packaging leads to heavy fines.

France Steel Drums Market Trends

In 2026, France will likely showcase the fastest growth and account for approximately 18.4% of the share in Western Europe steel drums market. Growth is attributed to the ongoing expansion of the pharmaceutical and agrochemical sectors. The French National Agency for Medicines and Health Products Safety (ANSM) now requires strict packaging traceability for drugs and plant-protection products, propelling demand for steel drums with unique identifiers. France also launched its Industry 2030 plan in 2024, which invests nearly US$1.75 Bn to modernize chemical and packaging facilities. This has led to new production lines for solvent-free coated steel drums in regions such as Rhône-Alpes and Alsace.

U.K. Steel Drums Market Trends

A share of nearly 13.8% is expected to be recorded by the U.K. in 2026 in Western Europe steel drums market. Growth is fueled by its well-established chemical and food-processing industries, despite post-Brexit trade challenges. The Health and Safety Executive (HSE) enforces strict UN transport regulations for hazardous materials, and steel drums remain the only packaging that consistently passes HSE audits for Class 3 and Class 8 chemicals. The U.K. also has a superior recycling infrastructure, with the Waste and Resources Action Program (WRAP) reporting that 92% of steel drums are recovered and recycled.

The Netherlands Steel Drums Market Trends

The Netherlands is predicted to account for a share of nearly 9.1% in 2026, as it serves as Europe’s largest chemical logistics hub. The Port of Rotterdam handles over 470 million tons of cargo annually, including massive volumes of chemicals, solvents, and petrochemicals that require steel drum packaging. The Dutch Ministry of Infrastructure and Water Management mandates UN-certified packaging for all hazardous cargo passing through Rotterdam, and steel drums are the most cost-effective certified option.

Spain Steel Drums Market Trends

Spain is estimated to hold a share of approximately 7.2% in 2026 in Western Europe steel drums market, spurred by its booming food, beverage, and olive oil export industries. Locally made steel drums are extensively used for packaging edible oils, wine, and agricultural chemicals. The Spanish Agency for Food Safety and Nutrition (AESAN) enforces strict food-contact material rules, and steel drums with BPA-free linings are now the standard for edible oil exports. The country’s chemical sector is smaller than Germany’s or France’s, but it is expanding in the renewable chemicals segment, supported by the Spain 2030 Industrial Strategy.

Belgium Steel Drums Market Trends

Belgium is anticipated to be one of the key countries in Western Europe steel drums market, with a share of approximately 6.4% in 2026. Prominent chemical firms such as Solvay, BASF Antwerp, and Dow Belgium rely heavily on steel drums for intermediates and final products. The country also leads in sustainability innovation. The Flemish Circular Economy Roadmap 2025 prioritizes reusable steel packaging. Belgium has several steel drum converters, including Mauser Belgium and Schoeller Allibert, which supply UN-rated drums to the entire Benelux region. Growth is expected to be supported by chemical industry expansion and strict EU packaging regulations.

Competitive Landscape

The Western Europe steel drums market is highly fragmented with the presence of multinational packaging companies and various regional manufacturers. Competition is led by leading industrial packaging companies such as Greif, Mauser Packaging Solutions, and SCHÜTZ GmbH & Co. KGaA. These companies have strengthened their positions through extensive manufacturing networks, drum reconditioning services, and closed-loop packaging solutions.

A prominent competitive trend is the rising emphasis on the circular economy and sustainability. Steel drum suppliers are now delivering reconditioning, recycling, and reuse programs to help chemical and lubricant manufacturers meet environmental targets. Companies with integrated lifecycle services have gained a competitive advantage as customers are seeking lower packaging waste and reduced carbon footprints.

Key Industry Developments

- In February 2026, ArcelorMittal highlighted the rising importance of Europe’s Carbon Border Adjustment Mechanism (CBAM) and improved trade measures in supporting low-carbon steel production. These policy developments are anticipated to encourage wide adoption of low-emission steel products, including sustainable industrial packaging such as steel drums.

- In November 2025, Mauser Packaging Solutions completed a major debt refinancing initiative by exchanging existing notes for new securities maturing in 2030. The move strengthened the company’s financial flexibility and supports ongoing investments in industrial packaging, including steel drum manufacturing and reconditioning operations across Europe.

- In March 2025, SCHÜTZ broadened commercialization efforts for its Combi Steel Drum following the start of production at its Selters, Germany, facility. The drum was designed to address rising demand from chemical manufacturers for packaging that combines the strength of steel with the chemical resistance of plastic.

Companies Covered in Western Europe Steel Drums Market

- Mauser Packaging Solutions

- Greif, Inc.

- SCHÜTZ GmbH & Co. KGaA

- B & B GmbH & Co. KG

- Grupo Armando Alvarez

- Müller Group

- The Metal Drum Company

- Carrick Packaging

- Nexus Packaging

- SL Packaging GmbH

- Hanningfield

- Ramsden Steel Drums Limited

- Innopack Suzhou Co., Ltd.

- MBL

- A W Stokes & Son (Drums) Ltd.

- Others

Frequently Asked Questions

The Western Europe steel drums market is projected to be valued at US$511.5 million in 2026.

The Western Europe steel drums market is expected to reach US$710.1 million by 2033.

Key market trends include a rising focus of leading manufacturers on circular economy models and surging adoption of low-carbon steel production.

Carbon steel is expected to be the leading material with a share of nearly 74.2% in 2026, as it provides high strength at a low cost, making it suitable for large-scale use in chemicals and petroleum industries.

The Western Europe steel drums market is expected to grow at a CAGR of 4.8% from 2026 to 2033.

Mauser Packaging Solutions, Greif, Inc., SCHÜTZ GmbH & Co. KGaA, and B & B GmbH & Co. KG are a few key market players.