- Non-food Packaging

- Vials Packaging Market

Vials Packaging Market Size, Share, and Growth Forecast, 2026 - 2033

Vials Packaging Market by Material (Glass, Plastic, Others), Capacity (Up to 10 ml, 11-50 ml, Others), Application, and Regional Analysis for 2026 - 2033

Vials Packaging Market Size and Trends Analysis

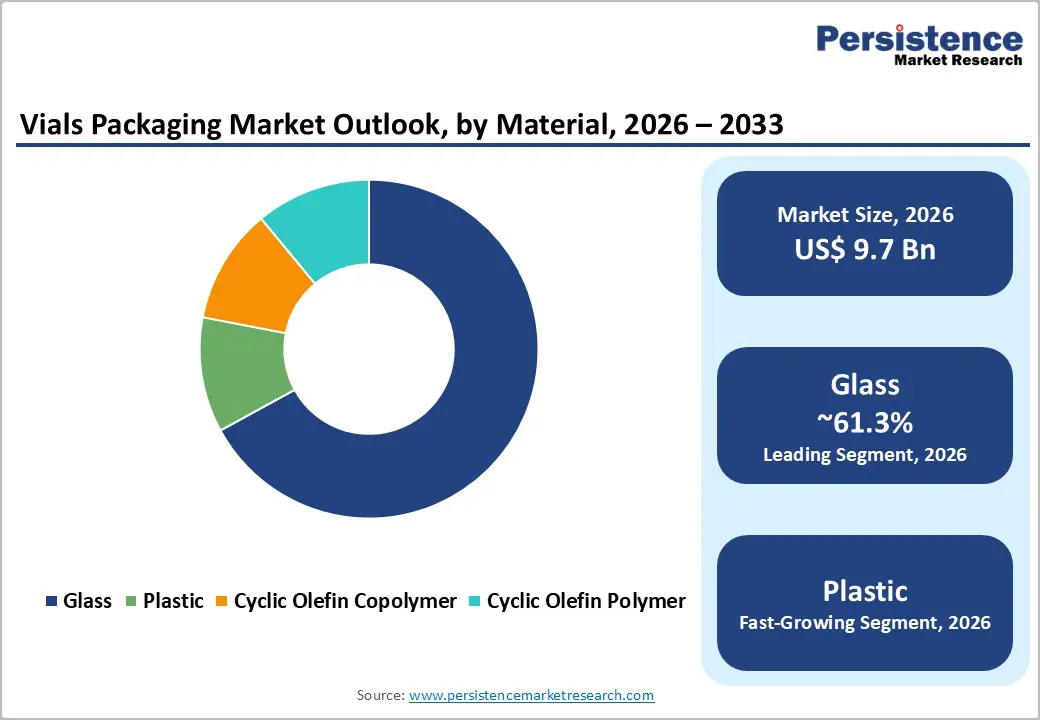

The global vials packaging market size is likely to be valued at US$9.7 billion in 2026 and is expected to reach US$13.1 billion by 2033, growing at a CAGR of 4.4% between 2026 and 2033, driven by the expansion of biologics, vaccines, and sterile injectables, while regulators continue to tighten expectations for container closure integrity, particulate control, and sterilization documentation.

Manufacturers are also shifting toward ready-to-use (RTU) and high-performance vial platforms to reduce contamination risk and improve fill-finish efficiency. The market is transitioning from commodity glass formats toward quality-driven, application-specific primary packaging, particularly for sensitive injectables, light-sensitive formulations, and high-throughput sterile operations. Uneven global vaccination coverage continues to sustain long-term demand for vials, while evolving regulatory standards reinforce the need for validated, high-performance primary containers. Industry innovation is increasingly concentrated in RTU vials, coated glass technologies, and advanced polymer alternatives.

Key Industry Highlights:

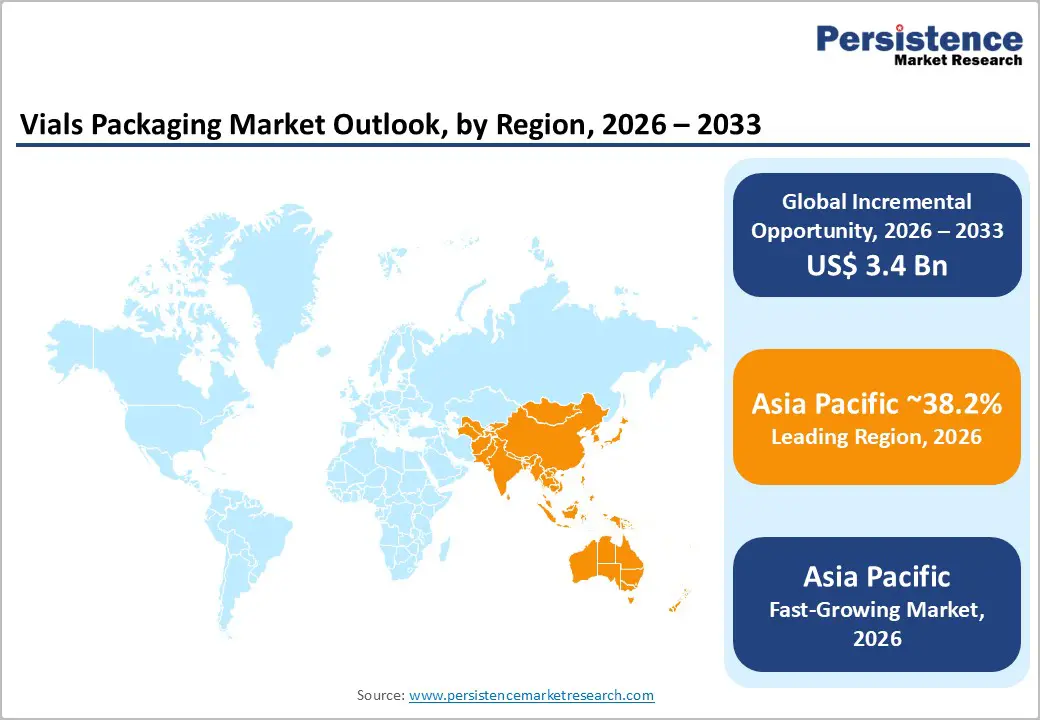

- Leading Region: Asia Pacific is projected to account for approximately 38.2% of the market share, driven by large-scale pharmaceutical manufacturing and strong vaccine production capabilities.

- Fastest-growing Region: Asia Pacific is also the fastest-growing region, supported by increasing healthcare demand, expanding biologics production, and ongoing investments in local manufacturing infrastructure across China, India, and ASEAN countries.

- Investment Plans: The market is witnessing strong investments in ready-to-use (RTU) vial systems, advanced glass technologies, and regional manufacturing expansion, particularly in Asia Pacific and Europe, to enhance supply chain resilience and meet rising demand for high-performance packaging.

- Dominant Material: Glass is anticipated to hold approximately 61.3% of the market share, due to its superior chemical resistance and suitability for sterile pharmaceutical applications.

- Leading Capacity: The up to 10 ml capacity segment leads the market with an estimated 49.4% share, driven by its extensive use in vaccines, single-dose biologics, and high-value injectable therapies.

| Key Insights | Details |

|---|---|

| Vials Packaging Market Size (2026E) | US$9.7 Bn |

| Market Value Forecast (2033F) | US$13.1 Bn |

| Projected Growth (CAGR 2026 to 2033) | 4.4% |

| Historical Market Growth (CAGR 2020 to 2025) | 5.2% |

Market Factors - Growth, Barriers, and Opportunity Analysis

Growth Analysis - Growth in Injectable Therapeutics and Biologics

The expansion of injectable therapies, particularly biologics and advanced treatment modalities, is a primary driver of the vials packaging market. Biologics require highly controlled packaging environments due to their sensitivity to contamination, temperature fluctuations, and chemical interactions. These therapies require packaging solutions with high container-closure integrity, minimal particulate generation, and compatibility with cold-chain and lyophilization processes. As oncology, immunology, and specialty therapeutics continue to shift toward injectable delivery formats, demand for small-volume, high-specification vials is increasing. This trend is reshaping procurement strategies, with pharmaceutical manufacturers prioritizing performance, reliability, and regulatory compliance over cost considerations.

Vaccination Programs and Public Health Demand

Vaccination programs remain a critical demand driver, as most vaccines are distributed in single- or multi-dose vials. Despite improvements in global immunization coverage, significant segments of the population remain unvaccinated, sustaining long-term demand for vaccine packaging. National immunization initiatives, global health programs, and pandemic preparedness strategies continue to require large-scale vial production capacity. Manufacturers are responding by scaling up production of small-capacity vials that support high-volume fill-finish operations and global distribution networks. This sustained demand reinforces the importance of reliable, high-quality vial supply chains for public health systems.

Regulatory Tightening and Quality Standards

Increasing regulatory scrutiny around sterility, particulate contamination, and container closure integrity is significantly influencing the market. Regulatory agencies require strict validation of primary packaging systems to ensure product safety and stability. Guidelines addressing issues such as glass delamination, visible particulates, and sterilization processes have elevated the importance of high-performance vial materials and manufacturing practices. As a result, pharmaceutical companies are adopting advanced packaging solutions such as coated glass, RTU formats, and specialized polymers. This shift is driving demand for technologically advanced vials and strengthening the competitive position of suppliers with proven compliance capabilities.

Barrier Analysis - High Production and Compliance Costs

The vials packaging market is characterized by high capital intensity due to the need for cleanroom environments, sterilization systems, and stringent quality control processes. Compliance with international standards requires significant investment in infrastructure, validation, and testing capabilities. These factors increase production costs and limit the speed of capacity expansion. Smaller manufacturers may face challenges in meeting these requirements, while pharmaceutical companies may delay transitioning to premium vial solutions due to budget constraints, particularly in cost-sensitive markets.

Supply Chain Volatility and Demand Fluctuations

The market is also affected by supply chain disruptions and cyclical demand patterns. Inventory corrections following periods of high demand, such as during global health crises, can lead to temporary declines in orders. Additionally, geopolitical factors, trade barriers, and regional manufacturing challenges can impact supply stability and pricing. These fluctuations create uncertainty for manufacturers and suppliers, particularly those with limited geographic diversification or production flexibility.

Opportunity Analysis - Expansion of Ready-To-Use (RTU) Vial Systems

RTU vials represent a significant growth opportunity, as they can streamline pharmaceutical manufacturing processes and reduce operational complexity. These pre-sterilized, ready-to-fill formats eliminate multiple preparation steps such as washing, depyrogenation, and sterilization, which significantly lowers contamination risk and minimizes human intervention. This directly improves efficiency in high-speed fill-finish lines and reduces downtime associated with quality deviations. As pharmaceutical companies increasingly prioritize faster time-to-market and lower total cost of ownership, RTU adoption is accelerating, particularly among contract manufacturing organizations (CMOs) and biologics producers. The trend is especially relevant for high-value injectables, including monoclonal antibodies and cell and gene therapies, where packaging reliability is critical to maintaining product integrity and meeting stringent regulatory standards.

Localization of Manufacturing in the Asia Pacific

The expansion of pharmaceutical manufacturing in Asia Pacific presents substantial opportunities for vial packaging suppliers, as the region continues to evolve into a global production hub. Governments and private stakeholders in countries such as China, India, and Japan are actively investing in pharmaceutical infrastructure, including sterile manufacturing and packaging facilities. This shift aims to reduce reliance on imports, improve supply chain resilience, and ensure uninterrupted access to critical healthcare products. Localization also enables faster delivery timelines, cost efficiencies, and better alignment with regional regulatory frameworks. In addition, the growth of domestic pharmaceutical companies and contract manufacturing services in the region is increasing demand for both standard glass vials and advanced packaging solutions such as RTU systems. As a result, Asia Pacific is becoming a focal point for capacity expansion, joint ventures, and technology transfer initiatives.

Development of Advanced Materials and Sustainable Solutions

Ongoing innovation in materials science is creating new opportunities in the vials packaging market, particularly in addressing performance and sustainability challenges. Advanced materials such as coated glass, hybrid glass-polymer systems, and high-performance polymers are being developed to improve durability, reduce breakage, and enhance compatibility with sensitive drug formulations. These materials are particularly valuable in applications involving biologics, cold-chain logistics, and high-stress transportation conditions. At the same time, sustainability is becoming an increasingly important consideration, with manufacturers exploring energy-efficient production methods, lightweight designs, and recyclable materials. Efforts to reduce carbon emissions and minimize packaging waste are influencing both product development and procurement strategies. This convergence of performance and sustainability is expected to drive innovation and create new opportunities for packaging suppliers to differentiate in the coming years.

Category-wise Analysis

Material Insights

Glass is anticipated to account for approximately 61.3% of the market share in 2026, maintaining its position as the dominant material in the vials packaging market. Its widespread use is driven by superior chemical inertness, strong resistance to temperature variations, and high compatibility with a broad range of pharmaceutical formulations. Glass vials are particularly critical for injectable drugs, vaccines, and lyophilized products, where maintaining product stability, sterility, and preventing contamination are essential.

Regulatory frameworks strongly favor high-quality glass, especially Type I borosilicate, due to its proven performance in sterile environments. For instance, vaccine manufacturers and biologics producers commonly rely on borosilicate glass vials to ensure long-term storage stability and compatibility with sensitive formulations, reinforcing its continued dominance.

Plastic is the fastest-growing material segment, driven by increasing demand for lightweight, durable, and flexible packaging solutions. Advanced polymers such as Cyclic Olefin Copolymer (COC) and Cyclic Olefin Polymer (COP) are gaining traction due to their low extractables, high transparency, and suitability for sensitive biologics and specialty injectables. These materials are increasingly adopted in applications where breakage risk, transportation efficiency, and patient safety are critical, such as prefilled systems and emergency-use injectables.

For example, polymer-based vials are being used in certain biologic drug delivery systems and cold-chain applications where glass fragility poses operational challenges. While glass will continue to dominate overall demand, plastics are expected to capture a growing share in high-value, niche applications where performance advantages outweigh traditional material preferences.

Capacity Insights

The up to 10 ml segment is anticipated to account for approximately 49.4% of the market share in 2026, making it the leading capacity category in the vials packaging market. This dominance is driven by the extensive use of small-capacity vials in vaccines, single-dose biologics, and high-value injectable therapies. These vials play a critical role in ensuring accurate dosing, reducing drug wastage, and enabling efficient large-scale immunization programs. Their compatibility with high-speed fill-finish lines and stringent regulatory requirements further strengthens their position.

For example, most routine vaccines and mRNA-based therapies are packaged in 2-10 ml vials, highlighting the importance of this segment in both public health and commercial pharmaceutical applications.

The 11-50 ml segment is the fastest-growing category, supported by its versatility across a wide range of pharmaceutical applications. These vials are commonly used for biologics, hospital-administered injectables, and reconstitution processes, where flexibility in dosing and storage is required. Growth in this segment is driven by increasing demand for complex therapies, including monoclonal antibodies and specialty drugs that require larger volumes or multi-dose formats.

For instance, hospitals frequently use 20 ml and 50 ml vials for injectable antibiotics and infusion-based treatments. While larger-capacity segments, such as 51-100 ml and above 100 ml, remain relatively niche, they serve specific use cases, such as intravenous infusions and bulk pharmaceutical preparations, contributing to overall market diversification.

Regional Market Insights

North America Vials Packaging Market Trends - Biologics-Driven Innovation & High-Performance Vial Solutions

North America is a key market for vial packaging, supported by a strong pharmaceutical industry, advanced healthcare infrastructure, and a robust regulatory framework. The U.S. leads the region, driven by high demand for biologics, vaccines, and injectable therapies. Regulatory requirements emphasize quality, safety, and compliance, encouraging the adoption of high-performance packaging solutions. The presence of leading pharmaceutical and packaging companies such as Corning Incorporated, West Pharmaceutical Services, and AptarGroup further strengthens the region’s market position. For instance, Corning’s development and commercialization of Valor glass vials has significantly improved resistance to breakage and delamination, directly addressing critical manufacturing challenges in sterile injectables.

Innovation remains a major growth driver in North America, with ongoing investments in advanced materials, RTU systems, and automation technologies. Companies are focusing on improving fill-finish efficiency, reducing contamination risks, and enhancing product integrity. West Pharmaceutical Services has expanded its containment and delivery solutions to support high-value biologics, while partnerships between pharmaceutical manufacturers and packaging providers are accelerating the adoption of ready-to-use vial systems. The region also benefits from a well-established supply chain and strong R&D capabilities, supported by regulatory oversight that encourages continuous improvement. These developments position North America as a hub for premium, technology-driven vial packaging solutions, particularly for complex biologics and specialty injectables.

Europe Vials Packaging Market Trends - Regulatory Excellence & Advanced Glass Packaging Leadership

Europe is a mature and technologically advanced market, characterized by strong regulatory standards and a high level of innovation. Countries such as Germany, the U.K., France, and Spain play a significant role in driving market growth. The region is home to several leading packaging manufacturers, including Gerresheimer AG, SCHOTT Pharma, and Stevanato Group, which are known for their expertise in high-quality glass production and advanced pharmaceutical packaging solutions. These companies have established strong relationships with global pharmaceutical firms, enabling consistent demand for premium vial products.

Regulatory harmonization across Europe ensures consistent quality standards, supporting the adoption of advanced packaging technologies such as RTU vials and coated glass systems. At the same time, the region faces challenges related to energy costs and supply chain disruptions, prompting companies to invest in efficiency and localization strategies. For example, SCHOTT Pharma’s expansion of production capacity in Eastern Europe has improved supply chain resilience and reduced dependence on higher-cost manufacturing locations.

Similarly, Gerresheimer has expanded its ready-to-fill vial capabilities in Germany to meet growing demand for sterile, high-performance packaging. These developments highlight a strategic shift toward high-value, specialized packaging solutions, reinforcing Europe’s position as a leader in innovation and quality within the global vials packaging market.

Asia Pacific Vials Packaging Market Trends - High-Volume Growth & Cost-Efficient Manufacturing Expansion

Asia Pacific is the largest and fastest-growing region in the vials packaging market, accounting for 38.2% of market share. The region’s growth is driven by expanding pharmaceutical manufacturing, rising healthcare demand, and production cost advantages. Countries such as China, India, and Japan are leading contributors, supported by strong domestic markets and export capabilities. Major players such as Nipro Corporation, along with global companies expanding their footprint in the region, are strengthening local production ecosystems. For example, India has emerged as a key hub for vaccine manufacturing, thereby increasing demand for small-capacity glass vials used in immunization programs.

Investment in manufacturing infrastructure and supply chain localization is accelerating market growth across the region. Strategic developments such as joint ventures between global packaging companies and local manufacturers are enhancing access to advanced vial technologies. For instance, collaborations to expand high-quality glass vial production in India are improving regional self-sufficiency and reducing reliance on imports. In China, ongoing investments in pharmaceutical packaging facilities are supporting the country’s large-scale biologics and generics production.

Meanwhile, Japan continues to contribute through high-precision manufacturing and innovation in advanced materials. These combined factors enable Asia Pacific to offer both cost-efficient volume production and increasing technological sophistication, making it a central focus for global expansion strategies in the vials packaging market.

Competitive Landscape

The global vials packaging market is moderately consolidated, with a few major players holding significant market share, while numerous smaller companies operate at regional levels. Leading companies dominate through their technical expertise, global presence, and ability to meet stringent regulatory requirements. Competition is driven by innovation, product quality, and supply chain reliability rather than price alone.

Key strategies include innovation, geographic expansion, and portfolio diversification. Companies are investing in advanced materials, RTU technologies, and localized manufacturing to enhance competitiveness. Strategic partnerships and acquisitions are also being used to strengthen market position and expand product offerings.

Key Industry Developments

- In June 2025, ten23 health joined the RTU alliance initiated by Stevanato Group, Gerresheimer, and SCHOTT Pharma, strengthening collaboration to advance sterile fill-finish processes and standardize ready-to-use vial technologies across the pharmaceutical industry.

Companies Covered in Vials Packaging Market

- Gerresheimer AG

- SCHOTT Pharma AG & Co. KGaA

- Stevanato Group

- Corning Incorporated

- West Pharmaceutical Services

- SGD Pharma

- Nipro Corporation

- Bormioli Pharma

- DWK Life Sciences

- AptarGroup Inc.

- Daikyo Seiko Ltd.

- SiO2 Material Science

- Shandong Pharmaceutical Glass Co., Ltd.

- Ardagh Group

- Piramel Glass Pvt. Ltd.

- Amcor plc

Frequently Asked Questions

The global vials packaging market is estimated to be valued at US$9.7 billion in 2026.

The vials packaging market is projected to reach US$13.1 billion by 2033, driven by sustained demand for injectable drugs and vaccines.

Key trends include the growing adoption of ready-to-use (RTU) vials, increasing demand for high-performance glass and polymer materials, rising focus on sterility and regulatory compliance, and expanding use of vials in biologics and vaccine applications.

The glass material segment is the leading segment, accounting for approximately 61.3% of the market share, due to its superior chemical resistance and compatibility with pharmaceutical applications.

The vials packaging market is expected to grow at a CAGR of 4.4% from 2026 to 2033.

Some of the major players include Gerresheimer AG, SCHOTT Pharma AG & Co. KGaA, Stevanato Group, Corning Incorporated, and West Pharmaceutical Services.