- Beverages

- U.S. Functional Beverage Market

U.S. Functional Beverage Market Size, Share, Growth, and Regional Forecast, 2026 to 2033

U.S. Functional Beverage Market is segmented by Product Type (Functional Waters, Dairy alternative beverages, Functional juices, Functional RTD coffees and teas), Packaging Type (Cans, PET/Plastic Bottles, Glass Bottles), Sales Channel (Supermarket/Hypermarket, Convenience Stores, Specialty Stores, Online Stores), 2026 - 2033

U.S. Functional Beverage Market Share and Trends Analysis

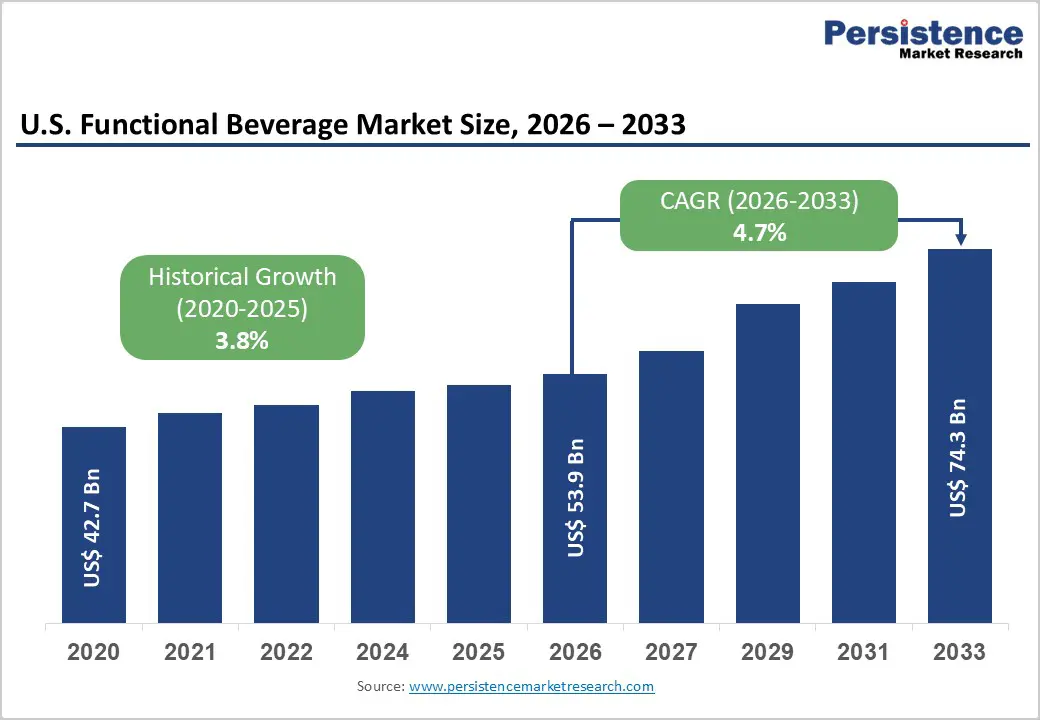

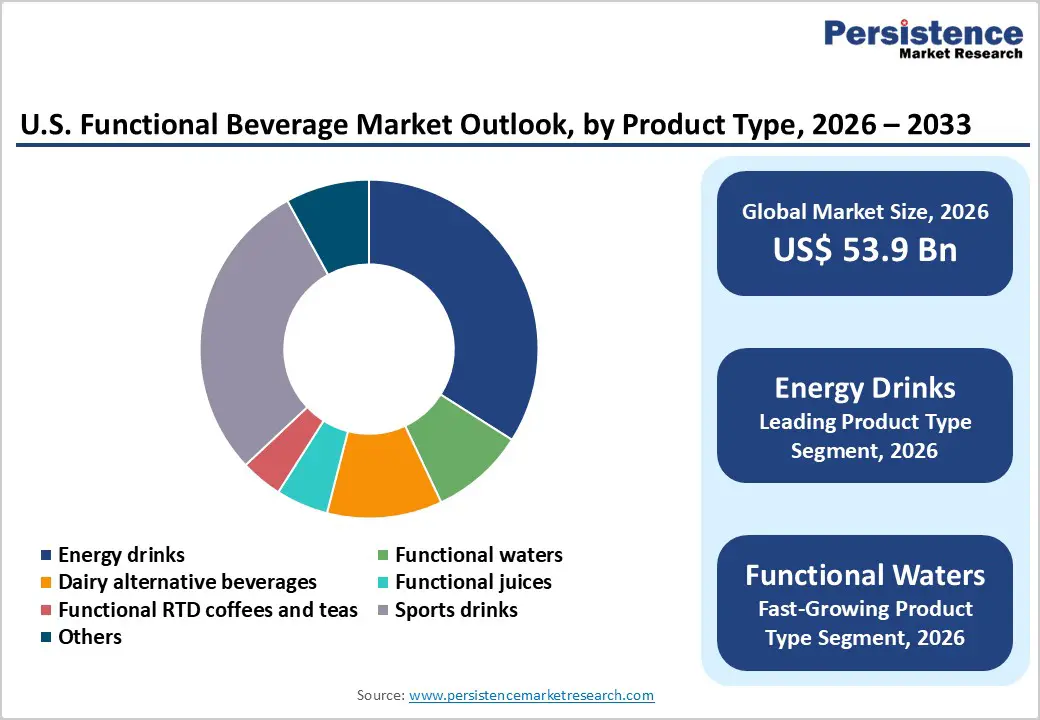

The U.S. functional beverage market size is expected to be valued at US$ 53.9 billion in 2026 and projected to reach US$ 74.3 billion by 2033, growing at a CAGR of 4.7% between 2026 and 2033.

It is witnessing steady growth, driven by a strong shift toward health-focused and better-for-you drink alternatives. Consumers are increasingly replacing sugary beverages with products offering hydration, energy, and nutritional benefits. Innovation in ingredients, packaging, and targeted wellness solutions especially for women is shaping market evolution.

Key Industry Highlights:

- Leading Product Type Segment: Energy Drinks, accounting for about 34% market share in 2025, supported by strong demand for convenient energy, mental focus, and performance-oriented beverages among students, professionals, and fitness enthusiasts.

- Fastest-Growing Packaging Type Segment: Pouches & Sachets, driven by increasing demand for portable drink mixes, personalized nutrition powders, and lightweight packaging suited for on-the-go lifestyles and e-commerce distribution.

- Growth Indicators: Consumers shifting from sugary sodas toward better-for-you beverages enriched with vitamins, electrolytes, plant proteins, and botanical ingredients that support hydration, immunity, and sustained energy.

- Challenges: Premium pricing of functional beverages containing specialty ingredients such as adaptogens, plant proteins, and clinically backed nutrients limits adoption among price-sensitive mainstream consumers.

- Opportunities: Women-focused functional beverage innovation addressing hormonal balance, beauty nutrition, and wellness needs through targeted formulations featuring collagen, probiotics, and botanical extracts.

- Key Developments: In March 2026, Elmhurst 1925 launched Clean Protein, a ready-to-drink plant-based beverage delivering 27g of complete protein. In March 2026, PolkaDot refreshed its adaptogenic mushroom drink line with updated formulations and branding.

| Key Insights | Details |

|---|---|

| U.S. Functional Beverage Market Size (2026E) | US$ 53.9 Bn |

| Market Value Forecast (2033F) | US$ 74.3 Bn |

| Projected Growth (CAGR 2026 to 2033) | 4.7% |

| Historical Market Growth (CAGR 2020 to 2025) | 3.8% |

Market Dynamics

Driver - Consumers shifting from sugary sodas to better-for-you beverages

The American beverage aisle is undergoing a visible transformation as consumers increasingly move away from traditional sugary sodas toward drinks positioned around wellness and everyday functionality. Growing awareness of sugar-related health concerns, including obesity and metabolic disorders, is prompting shoppers to reevaluate long-standing beverage habits. Many consumers now seek hydration options that contribute to energy balance, immunity, or digestive health rather than empty calories. This shift has expanded interest in beverages formulated with vitamins, electrolytes, botanical extracts, probiotics, and natural fruit ingredients. Functional drinks are increasingly perceived as practical daily nutrition tools that align with modern health goals.

Younger demographics and health-conscious households are especially influential in accelerating this transition. Convenience stores, supermarkets, and online grocery platforms are expanding shelf space for kombucha, electrolyte waters, protein beverages, and adaptogenic drinks. Product innovation focusing on reduced sugar formulations and natural sweeteners further strengthens consumer confidence. As beverage preferences evolve toward wellness-oriented choices, functional beverages are steadily capturing share from traditional carbonated soft drinks.

Restraints - Premium pricing limiting mass-market penetration

Premium functional beverages promise enhanced nutrition, clean-label formulations, and targeted health benefits, yet their elevated price points create a barrier for widespread adoption. Many products incorporate specialty ingredients such as adaptogenic mushrooms, botanical extracts, plant proteins, and clinically studied vitamins, which increase production costs and retail pricing. In price-sensitive retail environments, consumers frequently compare these beverages with traditional soft drinks, bottled water, or standard juices that are significantly cheaper. This pricing gap restricts consistent purchasing among middle-income households and limits the category’s reach beyond health-focused urban consumers. Retailers often allocate premium shelf space to higher-margin products, which can further raise final prices. As a result, despite strong interest in wellness-oriented drinks, premium pricing continues to constrain the transition of functional beverages from niche health products into a truly mass-market everyday beverage choice.

Opportunity - Women-focused functional beverage innovation

A new wave of product development is emerging as beverage companies increasingly design functional drinks tailored specifically for women’s health needs. Formulations are being crafted to support hormonal balance, bone health, skin vitality, and energy management, using ingredients such as collagen peptides, magnesium, plant proteins, and botanical adaptogens. Brands are recognizing that female consumers actively seek convenient wellness solutions that align with busy lifestyles, which creates strong demand for ready-to-drink formats offering targeted nutritional benefits. This shift encourages companies to move beyond generic energy or hydration positioning toward beverages designed around life stages, including active lifestyles, prenatal nutrition, and healthy aging.

Innovation opportunities extend further through personalized nutrition and lifestyle positioning. Functional beverages are increasingly marketed around wellness themes such as stress management, beauty support, and metabolic balance. Ingredients like biotin, hyaluronic acid, probiotics, and herbal extracts are gaining attention in formulations aimed at skin health and digestive comfort. Companies are also experimenting with low-sugar profiles, plant-based bases, and clean-label ingredient lists that appeal to health-conscious female consumers. Packaging and branding strategies are evolving as well, with sleek single-serve cans and subscription-based online sales designed to build long-term consumer engagement and brand loyalty.

Category-wise Analysis

Product Type Insights

Energy drinks hold approx. 34% share as of 2025, reflecting their strong integration into the daily routines of U.S. consumers seeking quick mental and physical stimulation. These beverages are widely consumed by students, professionals, gamers, and athletes who rely on caffeine, taurine, and B-vitamins to maintain alertness and endurance during demanding schedules. The convenience of ready-to-drink formats, aggressive branding, and constant flavor innovation have strengthened their position across supermarkets, gyms, and convenience stores. Energy drinks also benefit from strong marketing around performance, focus, and lifestyle identity, which resonates with younger demographics and fitness-focused consumers.

Functional Waters are gaining popularity as hydration-focused beverages enriched with vitamins, electrolytes, and botanical extracts for everyday wellness. Dairy alternative beverages appeal to plant-based consumers seeking protein, calcium, and lactose-free nutrition. Functional juices deliver antioxidant and immunity benefits through fruit concentrates and herbal blends. Functional RTD coffees and teas provide natural caffeine and adaptogenic ingredients, attracting consumers seeking sustained energy with familiar beverage formats.

Packaging Type Insights

Pouches & Sachets is expected to achieve a CAGR of 7.7% during the forecast period, supported by their portability and compatibility with modern on-the-go consumption habits. Consumers increasingly favor lightweight packaging that can be easily carried in gym bags, office drawers, or travel kits without the bulk associated with cans or bottles. These compact formats are especially suitable for powdered functional beverages, concentrated drink mixes, and single-serve nutrition blends designed for quick preparation. Manufacturers are also attracted to pouches and sachets because they require less packaging material, reduce transportation weight, and offer longer shelf stability for powdered formulations.

Innovation in flexible packaging technology has improved barrier protection, preserving sensitive ingredients such as probiotics, vitamins, and plant extracts. Functional beverage startups are leveraging this format to launch personalized nutrition drink mixes, collagen blends, and electrolyte powders targeting fitness enthusiasts and wellness consumers. Attractive graphics, resealable designs, and portion-controlled servings strengthen consumer appeal. As subscription-based e-commerce and direct-to-consumer beverage brands expand in the U.S., lightweight pouch packaging continues to offer logistical advantages for shipping efficiency and cost optimization.

Competitive Landscape

The U.S. functional beverage market presents a moderately fragmented competitive landscape where global beverage corporations and emerging wellness startups compete across energy, hydration, and nutrition categories. Leading companies continuously expand product portfolios through flavor innovation, functional ingredient blends, and health-focused positioning to capture evolving consumer demand. Many brands emphasize clean label formulations using botanical extracts, plant proteins, probiotics, and vitamins while replacing refined sugars with natural sweeteners such as stevia or monk fruit. This ingredient transparency strengthens consumer trust among health-conscious buyers seeking functional beverages that align with wellness lifestyles.

Brand visibility is increasingly driven through celebrity partnerships and sports players serving as brand ambassadors, which strengthens cultural relevance and consumer engagement. Companies are investing in recyclable cans, lightweight bottles, and eco-friendly packaging formats while highlighting certifications related to organic or non-GMO ingredients. Direct-to-consumer channels are expanding through subscription models, enabling beverage brands to build loyal digital communities and gather real-time consumer insights.

Key Developments:

- In March 2026, Elmhurst 1925 introduced Clean Protein, a ready-to-drink plant-based protein beverage delivering 27g of complete protein and 190 calories, formulated without gums, seed oils, or artificial sweeteners.

- In March 2026, PolkaDot refreshed its adaptogenic mushroom drink line, introducing updated formulations and branding to strengthen its position in the functional beverage segment.

- In January 2026, BLU Energy Drink officially launched its complete product lineup in the United States, expanding its global presence across more than 40 countries.

Companies Covered in U.S. Functional Beverage Market

- The Coca-Cola Company

- PepsiCo, Inc.

- Monster Beverage Corp.

- Keurig Dr Pepper

- Celsius Holdings

- Vita Coco Company

- National Beverage Corp.

- Tilray Brands

- Red Bull GmbH

- PRIME Hydration LLC

- Chobani LLC

- Others

Frequently Asked Questions

The U.S. Functional Beverage market is projected to be valued at US$ 53.9 Bn in 2026.

Consumers shifting from sugary sodas to better-for-you beverages is a major factor driving the U.S. Functional Beverage market.

The U.S. Functional Beverage market is poised to witness a CAGR of 4.7% between 2026 and 2033.

Women-focused functional beverage innovation is a significant opportunity in the functional beverages market.

Major players in the U.S. Functional Beverage market include The Coca-Cola Company, PepsiCo, Inc., Monster Beverage Corp., Keurig Dr Pepper, Celsius Holdings, National Beverage Corp., Red Bull GmbH, and others.