- Executive Summary

- U.S. Data Center Construction Market Snapshot 2026 and 2033

- Market Opportunity Assessment, 2026-2033, US$ Mn

- Key Market Trends

- Industry Developments and Key Market Events

- Demand Side and Supply Side Analysis

- PMR Analysis and Recommendations

- Market Overview

- Market Scope and Definitions

- Value Chain Analysis

- Macro-Economic Factors

- GDP Outlook

- Digital Transformation and ICT Penetration

- Labor Market Tightness & Wage Growth

- Cloud Computing Growth

- Telecommunications Infrastructure Upgrade

- Forecast Factors – Relevance and Impact

- COVID-19 Impact Assessment

- PESTLE Analysis

- Porter's Five Forces Analysis

- Geopolitical Tensions: Market Impact

- Regulatory and Tier Landscape

- Market Dynamics

- Drivers

- Restraints

- Opportunities

- Trends

- Price Trend Analysis

- Price by Infrastructure

- Price Impact Factors

- U.S. Data Center Construction Market Outlook: Historical (2020 – 2025) and Forecast (2026 – 2033)

- Key Highlights

- U.S. Data Center Construction Market Outlook: Infrastructure

- Introduction/Key Findings

- Historical Market Size (US$ Mn) Analysis by Infrastructure, 2020-2024

- Current Market Size (US$ Mn) Forecast, by Infrastructure, 2025-2033

- IT Infrastructure

- Power & Cooling Infrastructure

- General Construction & Building Support

- Others

- Market Attractiveness Analysis: Infrastructure

- U.S. Data Center Construction Market Outlook: Tier

- Introduction/Key Findings

- Historical Market Size (US$ Mn) Analysis by Tier, 2020-2024

- Current Market Size (US$ Mn) Forecast, by Tier, 2025-2033

- Tier 1

- Tier 2

- Tier 3

- Tier 4

- Market Attractiveness Analysis: Tier

- U.S. Data Center Construction Market Outlook: Data Center Size

- Introduction/Key Findings

- Historical Market Size (US$ Mn) Analysis by Data Center Size, 2020-2024

- Current Market Size (US$ Mn) Forecast, by Data Center Size, 2025-2033

- Small and Medium-sized Data Centers

- Large Data Centers

- Market Attractiveness Analysis: Data Center Size

- U.S. Data Center Construction Market Outlook: Vertical

- Introduction/Key Findings

- Historical Market Size (US$ Mn) Analysis by Vertical, 2020-2024

- Current Market Size (US$ Mn) Forecast, by Vertical, 2025-2033

- IT and Telecom

- BFSI

- Government and Defense

- Healthcare

- Energy & Utilities

- Media & Entertainment

- Others

- Market Attractiveness Analysis: Vertical

- Competition Landscape

- Market Share Analysis, 2025

- Market Structure

- Competition Intensity Mapping

- Competition Dashboard

- Company Profiles

- AECOM

- Company Overview

- Solution Portfolio/Offerings

- Key Financials

- SWOT Analysis

- Company Strategy and Key Developments

- Vertiv Group Corp.

- Equinix, Inc.

- Gensler

- Turner Construction Company

- Jacobs Solutions Inc.

- Cisco Systems, Inc.

- IPXON Networks

- HITT Contracting Inc.

- Fluor Corporation

- HostDime Global Corp.

- ABB

- Others

- AECOM

- Appendix

- Research Methodology

- Research Assumptions

- Acronyms and Abbreviations

- Technology

- U.S. Data Center Construction Market

U.S. Data Center Construction Market Size, Share, and Growth Forecast, 2026 - 2033

U.S. Data Center Construction Market by Infrastructure (IT Infrastructure, Power & Cooling Infrastructure, General Construction & Building Support, Others), Tier (Tier 1, Tier 2, Tier 3, Tier 4), Data Center Size (Small and Medium-sized Data Centers, Large Data Centers), Vertical (IT and Telecom, BFSI, Government and Defense, Healthcare, Energy & Utilities, Media & Entertainment, Others) Analysis for 2026 - 2033

U.S. Data Center Construction Market Size and Trends Analysis

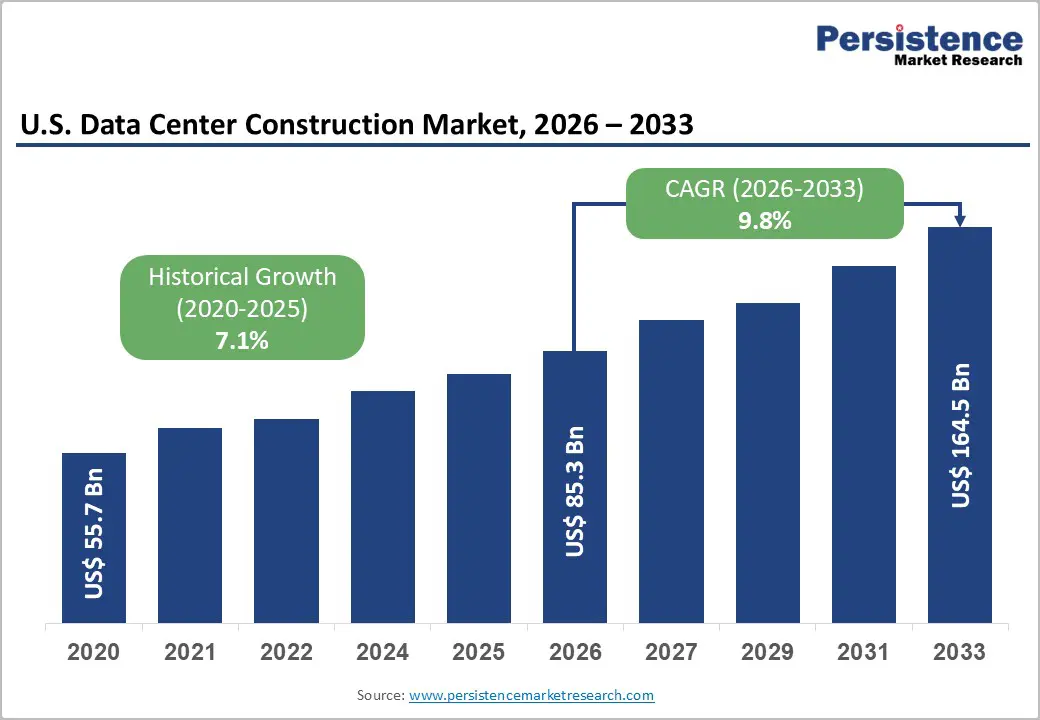

The U.S. Data Center Construction Market size is projected to rise from US$ 85.3 billion in 2026 to US$ 164.5 billion by 2033. It is anticipated to witness a CAGR of 9.8% during the forecast period from 2026 to 2033, driven by the rapid expansion of hyperscale and colocation facilities to support cloud computing, AI workloads, and edge computing, which is fundamentally reshaping construction demand across primary and secondary U.S. markets. This surge is reinforced by large-scale investment plans from hyperscalers and technology majors, generous state-level tax incentives, and fast-growing data intensity across sectors, which together are driving sustained multi-year construction pipelines.

Key Industry Highlights:

- Leading Infrastructure: IT infrastructure captures over 38% market share in 2026, valued at more than US$ 32.4 Bn, driven by enterprise demand for high-performance computing, scalable server racks, advanced networking, and storage to support AI, cloud, and big data workloads. Power and cooling infrastructure exhibits the highest growth, addressing the rising energy demands of hyperscale and AI-optimized data centers.

- Leading Tier Type: Tier 3 data centers hold over 45% market share in 2026, valued at more than US$ 38.4 Bn, balancing high reliability ~99.982% uptime with cost efficiency, meeting enterprise and cloud provider needs. Tier 4 is projected to grow at a CAGR of 12.7%, offering fully redundant systems with zero single points of failure, catering to cloud, financial, and critical government operations requiring maximum uptime.

- Leading Data Center Size: Large data centers command over 63% market share in 2026, valued at more than US$ 53.8 Bn, supporting hyperscale workloads, AI computing, robust interconnectivity, and disaster recovery with centralized, high-capacity infrastructure. Small and medium-sized facilities are growing rapidly, driven by edge computing, hybrid IT strategies, and demand for low-latency, scalable, and localized deployments.

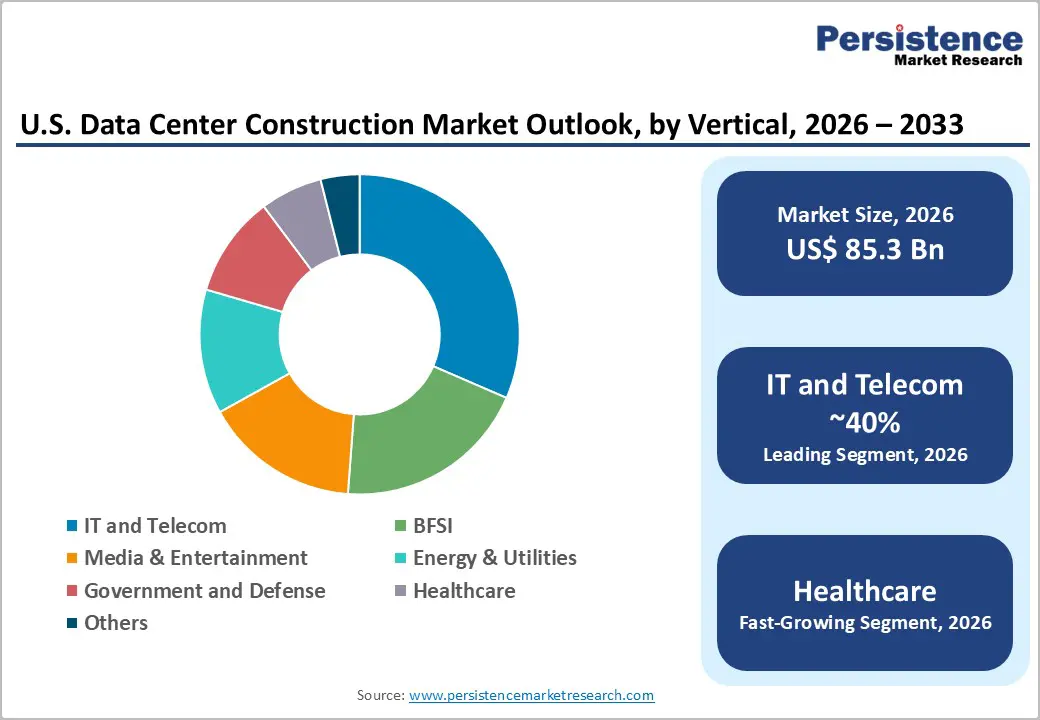

- Leading Vertical: IT & Telecom dominate with over 40% market share in 2026, valued at more than US$ 34.1 Bn, fueled by cloud adoption, 5G rollout, high-speed connectivity, and low-latency requirements. Healthcare is witnessing rapid expansion due to digital patient records, telemedicine, AI-driven analytics, IoT devices, and regulatory compliance needs, increasing demand for secure and high-performance infrastructure.

| Key Insights | Details |

|---|---|

|

U.S. Data Center Construction Market Size (2026E) |

US$85.3 Bn |

|

Market Value Forecast (2033F) |

US$164.5 Bn |

|

Projected Growth (CAGR 2026 to 2033) |

9.8% |

|

Historical Market Growth (CAGR 2020 to 2025) |

7.1% |

Market Dynamics

Driver - Surging AI, Cloud, and Data Intensity Across Verticals

Unprecedented growth in AI, cloud computing, and data-rich applications across IT & telecom, BFSI, healthcare, and media & entertainment is driving demand for U.S. data center construction. Hyperscalers and cloud providers have announced expansion programs worth tens of billions of US$ to add campus-scale capacity and GPU-dense halls capable of handling AI workloads that consume up to 160% more power than conventional applications, significantly raising infrastructure complexity and construction scope. In 2024, major players such as Microsoft, Amazon Web Services (AWS), and Google reportedly committed over US$ 40 Bn in U.S. data center infrastructure expansions, triggering multi-phase projects in hubs like Northern Virginia, Texas, and Arizona, thereby structurally lifting demand for specialized power, cooling, and building systems.

Tax Incentives, Renewable Energy Push, and Edge Expansion

State and local governments across the U.S. are competing to attract data center investments via tax exemptions, sales/use tax abatements, and streamlined permitting for mission-critical infrastructure, which strongly supports new greenfield and brownfield construction. Numerous states offer multi-year breaks on equipment and power purchases for qualifying data center projects, encouraging long-term campus development and on-site renewable integration that lowers the total cost of ownership for operators. The shift toward renewable-powered and low-latency edge facilities, particularly around 5G rollouts by operators like AT&T and T-Mobile, is accelerating build-outs of smaller edge nodes as well as regional campuses, strengthening the overall U.S. data center construction pipeline without necessarily concentrating all activity in a few legacy hubs.

Restraint - Power Availability Constraints and Grid Congestion

Limited availability of high-capacity, reliable power in key data center corridors, combined with growing grid congestion, is becoming a critical constraint. AI-optimized campuses often require hundreds of megawatts of additional capacity, placing pressure on utilities and leading to longer connection queues as regulators scrutinize environmental and community impacts. In regions like Northern Virginia, developers are already facing extended lead times for power allocation and substation upgrades, which delay or reduce the scale of planned facilities and increase project risk.

Rising Construction Costs, Supply Chain, and Labor Shortages

Escalating costs for critical equipment, specialized materials, and skilled labor are a structural headwind for the U.S. data center construction market. Inflationary pressures, lingering supply chain disruptions for items such as high-capacity transformers, switchgear, and advanced cooling systems, and a shortage of experienced mission-critical trades increase project budgets and risk of schedule overruns. According to a study, persistent deficits in specialized design-build talent, commissioning engineers, and technicians are forcing contractors and operators to lengthen timelines or phase projects more cautiously, which in turn moderate annualized construction volumes even when long-term demand fundamentals remain robust.

Opportunity - Hyperscale and GPU-Optimized Campus Developments

The rapid scaling of hyperscale cloud and AI training/inference workloads opens substantial opportunities for contractors and infrastructure providers focused on very-large campuses and high-density white space. As hyperscalers deploy multi-gigawatt roadmaps across the U.S., there is a growing need for advanced electrical distribution, liquid and immersion cooling, and modularized power rooms tailored to racks drawing tens of kilowatts each. Providers that design and deliver repeatable, standardized hyperscale blocks with integrated sustainability features like heat reuse and on-site renewables are well-positioned to capture a disproportionate share of upcoming awards, especially as AI workloads are forecast to contribute more than 50% of incremental construction spending in the medium term.

Edge Data Centers, Sustainable Designs, and Brownfield Retrofits

Rising deployment of 5G, IoT, and low-latency applications is creating significant opportunities in edge data centers, modular facilities, and retrofits of existing enterprise sites that need modernization to Tier III/IV reliability levels. Telecom and content providers are increasingly investing in distributed infrastructure near population centers and network aggregation points, enabling contractors that specialize in compact, energy-efficient builds with rapid deployment cycles to expand their addressable market. Pressure to meet sustainability and ESG targets is accelerating demand for high-efficiency cooling, PUE optimization, and renewable-linked designs, encouraging upgrades of older data centers; this creates recurring retrofit and expansion workstreams beyond greenfield megaprojects.

Category-wise Analysis

Infrastructure Insights

IT infrastructure capturing more than 38% market share in 2026 with a value exceeding US$ 32.4 Bn, due to the growing need for high-performance computing environments to support AI, cloud, and big data workloads. Enterprises are demanding scalable server racks, advanced networking equipment, and storage systems to handle rising data traffic and low-latency requirements. Rapid digital transformation across sectors is increasing the need for secure, high-capacity IT deployments. Hybrid and multi-cloud strategies are pushing organizations to invest heavily in robust core IT architecture within new and expanded data center facilities.

Power & cooling infrastructure demonstrates the highest growth due to the rising energy demands of high-performance servers and hyperscale data centers. Efficient cooling systems are critical to prevent overheating, reduce downtime, and maintain optimal server performance. Increasing adoption of AI, cloud computing, and storage-intensive applications is driving the need for advanced, energy-efficient power distribution and cooling solutions. Sustainability goals push for greener, low-power cooling technologies, further accelerating investment in this segment.

Tier Insights

Tier 3 holds over 45% market share in 2026, with a value exceeding US$ 38.4 Bn, as they balance high reliability ~99.982% uptime with cost-efficiency, meeting most enterprise and cloud provider needs without the premium expense of Tier 4. They support N+1 redundancy, which aligns with growing demands for business continuity, scalability, and disaster resilience. This makes Tier 3 ideal for organizations requiring robust performance for critical workloads while controlling construction and operational costs.

Tier 4 is expected to grow at the highest rate, with a CAGR of 12.7%, as it offers fully redundant systems with zero single points of failure, meeting the needs of industries requiring maximum uptime. Growing demands from cloud services, financial institutions, and critical government operations drive the need for fault-tolerant infrastructure. Increasing reliance on 24/7 digital services and stricter compliance for data reliability also boost Tier 4 adoption. Enterprises seeking long-term operational resilience prefer investing in the highest-tier facilities despite higher upfront costs.

Data Center Size Insights

Large data centers command the largest market share at over 63% in 2026, with a value exceeding US$ 53.8 Bn, due to their ability to handle massive enterprises and cloud workloads efficiently. They provide high scalability, advanced redundancy, and robust security, meeting growing demands for AI, big data, and hyperscale computing. Their centralized infrastructure reduces operational costs per unit of computing power, while supporting extensive interconnectivity and disaster recovery requirements. These factors make large facilities essential for businesses requiring continuous uptime and high-performance IT services.

Small and medium-sized data centers are expected to grow at a significant rate due to the rising demand for localized computing and low-latency services. Businesses increasingly require flexible, scalable facilities to support cloud adoption, edge computing, and hybrid IT architectures. These centers are easier and faster to deploy, require lower upfront capital, and efficiently handle growing data traffic from IoT, remote work, and digital services. Their agility meets the need for tailored, cost-effective, and resilient infrastructure in a rapidly evolving market.

Vertical Insights

IT and Telecom commands the largest market share at over 40% in 2026, with a value exceeding US$ 34.1 Bn, as these industries demand massive, reliable infrastructure to support cloud computing, 5G networks, and high-speed connectivity. Continuous data growth, low-latency requirements, and redundancy needs push companies to invest in large-scale, resilient facilities. Telecom operators and IT firms require advanced cooling, power, and security systems to ensure uninterrupted service, making this segment the primary driver of construction activity. Robust interconnectivity and scalability further reinforce their dominance in the market.

Healthcare is expected to grow rapidly due to the surge in digital patient records, telemedicine, and remote diagnostics. Hospitals and clinics require secure, high-performance infrastructure to handle large volumes of sensitive data. Compliance with HIPAA and other regulations further demands robust, redundant systems. The adoption of AI-driven healthcare analytics and IoT medical devices is increasing storage and computing needs, fueling investment in modern data centers.

Competitive Landscape

The U.S. data center construction market is moderately concentrated at the top but remains broadly fragmented, with a mix of global EPCs, specialist mission-critical contractors, design firms, and infrastructure OEMs competing for projects of varying scales. Companies are emphasizing sustainability credentials, prefabricated modular solutions, and strong local partnerships to expedite approvals and utility interconnections. Collaboration between construction firms and hyperscalers, the use of digital twins for project planning, and investment in advanced cooling technologies are increasingly being used to reduce operational costs and carbon footprints.

Key Industry Developments

- In February 2026, AES Corp signed a 20-year agreement to supply power to Google’s new data center in Wilbarger County, Texas. The deal includes co-located energy generation to support Google’s expansion and ensure reliable operations for its core services.

- In October 2025, DataBank increased its credit facility from $725 million to $1.6 billion to fund ongoing and future data center construction projects totaling over 100MW across key U.S. markets. The financing, involving 20 lenders, lowers interest rates, extends maturity, and qualifies as a green loan supporting carbon-neutral goals by 2030.

Companies Covered in U.S. Data Center Construction Market

- AECOM

- Vertiv Group Corp.

- Equinix, Inc.

- Gensler

- Turner Construction Company

- Jacobs Solutions Inc.

- Cisco Systems, Inc.

- IPXON Networks

- HITT Contracting Inc.

- Fluor Corporation

- HostDime Global Corp.

- ABB

- Others

Frequently Asked Questions

The U.S. data center construction market is projected to be valued at US$85.3 Bn in 2026.

The growing need for high-speed data storage, reliable cloud services, and robust infrastructure to support AI, IoT, and increasing enterprise digital workloads are key driver of the market.

The U.S. data center construction market is expected to witness a CAGR of 9.8% from 2026 to 2033.

Expanding hyperscale and edge data centers, adopting energy-efficient designs, and integrating advanced cooling and high-density storage solutions to meet surging digital demand are creating strong growth opportunities.

AECOM, Vertiv Group Corp., Equinix, Inc., Gensler, Turner Construction Company, Jacobs Solutions Inc., Cisco Systems, Inc., IPXON Networks, HITT Contracting Inc. are among the leading key players.