- Pharmaceuticals

- U.S. Antipsychotic Drugs Market

U.S. Antipsychotic Drugs Market Size, Trends, Share, and Growth Forecast, 2026 - 2033

U.S. Antipsychotic Drugs Market by Disease (Schizophrenia, Bipolar Disorder, Others), Therapeutic Class (First Generation, Second Generation, Third Generation), Distribution Channel (Hospital Pharmacies, Others), and Zone Analysis 2026 – 2033

U.S. Antipsychotic Drugs Market Share and Trends Analysis

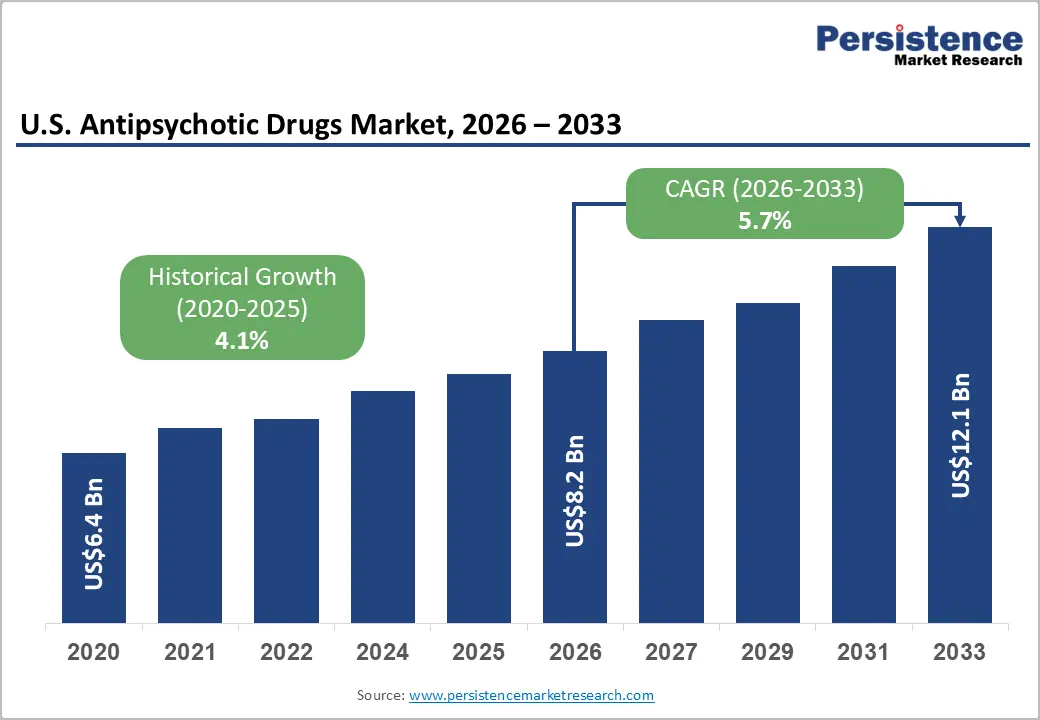

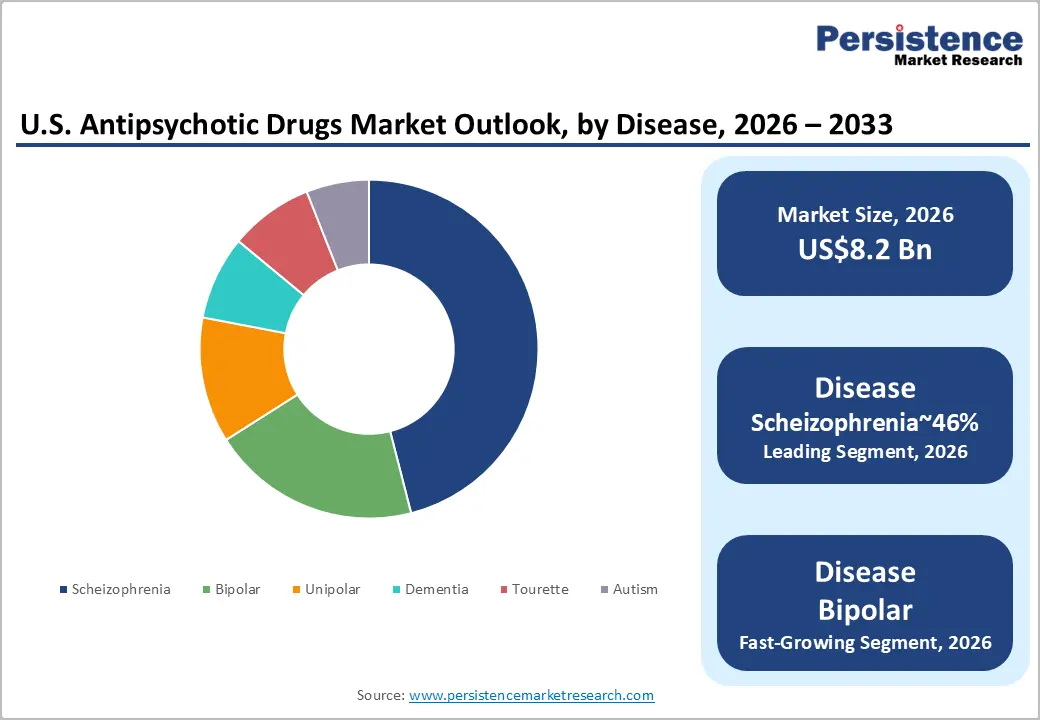

The U.S. antipsychotic drugs market size is likely to be valued at US$8.2 billion in 2026 and is projected to reach US$12.1 billion by 2033, growing at a CAGR of 5.7% between 2026 and 2033. This steady growth is underpinned by the rising prevalence of mental health disorders and a shift toward Long-Acting Injectable (LAI) formulations that enhance patient adherence.

The market is transitioning from traditional dopaminergic blockers to novel muscarinic agonists, which offer improved safety profiles and reduced metabolic side effects. Furthermore, expanded coverage under Medicare Part D reforms and increased federal funding for community mental health centers are providing stable institutional support for market expansion.

Key Industry Highlights:

- Leading Disease: Schizophrenia is expected to lead, accounting for approximately 46% share in 2026 through its entrenched role within long-term psychiatric treatment pathways, sustained pharmacological maintenance requirements, and strong clinical adoption across hospital and specialty mental health programs.

- Fastest-Growing Disease: Bipolar Disorder is anticipated to grow fastest due to expanding clinical recognition of mood spectrum disorders, increasing integration of atypical antipsychotics into mood stabilization strategies, and rising adoption across outpatient psychiatric care networks.

- Leading Therapeutic Class: Second Generation is projected to dominate for broad-spectrum clinical efficacy, reduced extrapyramidal side effects, strong physician familiarity, and extensive integration within psychiatric treatment formularies, holding approximately 67% share in 2026.

| Key Insights | Details |

|---|---|

| U.S. Antipsychotic Drugs Market Size (2026E) | US$8.2 Bn |

| Market Value Forecast (2033F) | US$12.1 Bn |

| Projected Growth (CAGR 2026 to 2033) | 5.7% |

| Historical Market Growth (CAGR 2019 to 2025) | 4.1% |

Market Factors – Growth, Barriers, and Opportunity Analysis

Growth Analysis – Rising Burden of Chronic Psychiatric Disorders Expanding Long-Term Antipsychotic Therapy Demand

The expanding clinical burden of severe psychiatric disorders is strengthening sustained demand for antipsychotic pharmacotherapy across the healthcare system. Schizophrenia and bipolar spectrum conditions require continuous therapeutic management to stabilize neurological signaling and prevent relapse episodes. Growing diagnostic accuracy, supported by standardized psychiatric evaluation frameworks, is broadening patient identification within formal treatment pathways. Reduced stigma surrounding mental illness has further increased willingness among patients to seek professional psychiatric intervention. These dynamics expand the treated population requiring continuous pharmacological stabilization across inpatient psychiatric units and outpatient care settings. As treatment adherence becomes central to relapse prevention strategies, chronic prescription utilization continues shaping consistent antipsychotic demand.

The structural nature of these disorders creates long-duration treatment cycles requiring sustained medication access across healthcare networks. Clinical management increasingly integrates pharmacotherapy with digital monitoring tools that track adherence and symptom progression. Healthcare systems are reinforcing psychiatric service infrastructure, strengthening prescription continuity through specialized mental health programs. Regulatory oversight emphasizing early intervention and long-term disease management is expanding formal treatment pathways. Aging demographics also contribute to broader neuropsychiatric vulnerability, reinforcing demand for antipsychotic therapies within complex care environments.

Clinical Adoption of Long-Acting Injectable Antipsychotics Improving Treatment Adherence

The antipsychotic drugs market increasingly benefits from rapid clinical adoption of long-acting injectable therapies. Medication nonadherence remains a persistent barrier across schizophrenia treatment pathways relying on daily oral regimens. Clinical evidence indicates nonadherence affects up to 50% schizophrenia patients receiving conventional oral therapies. Long-acting injectable formulations address this gap through extended dosing intervals, replacing daily medication administration. Products such as UZEDY received regulatory approval during April 2023 with strong relapse reduction outcomes. Pandemic disruptions further accelerated adoption as providers prioritized stable medication delivery across reduced clinical visits.

Pharmaceutical developers increasingly prioritize extended duration injectable platforms supporting two-month or multi-month dosing intervals. Flagship therapies, including Abilify Asimtufii and Invega Hafyera, illustrate this transition toward long interval treatment models. These formulations enable clinicians to monitor adherence while minimizing relapse risk within complex psychiatric care settings. Hospital pharmacies remain primary distribution hubs supporting administration, monitoring, and integrated psychiatric treatment services. Improved adherence reduces emergency interventions and limits costly hospitalization cycles associated with untreated psychosis. Healthcare payers increasingly recognize long-acting injectables as cost-stabilizing interventions across chronic psychiatric care programs. Consequently, extended-release antipsychotic platforms support premium pricing structures and sustained market expansion.

Barrier Analysis – Metabolic Adverse Effects Limiting Long-Term Antipsychotic Treatment Continuity

Second-generation antipsychotics present clinically significant metabolic risks that complicate long-term psychiatric treatment pathways. Regulatory evaluations from the U.S. Food and Drug Administration highlight weight gain and metabolic disturbances across several widely prescribed therapies. These adverse reactions include elevated glucose levels, insulin resistance, and progressive cardiometabolic complications. Such physiological burdens create clinical hesitation among prescribers managing vulnerable psychiatric patient populations. Patients frequently experience diminished treatment tolerance, particularly when metabolic symptoms worsen during maintenance therapy phases. This safety profile complicates medication adherence within chronic schizophrenia and bipolar disorder management frameworks.

The antipsychotic drugs market faces structural demand volatility linked to safety-related therapy discontinuation. Medication switching often occurs when metabolic complications undermine a patient's quality of life and therapeutic tolerance. This cycle of discontinuation and substitution introduces instability across long-term prescription utilization patterns. Healthcare providers must frequently introduce adjunct pharmacological interventions to mitigate metabolic side effects. These additional therapies increase overall treatment complexity within psychiatric care delivery environments. Payers and clinical systems consequently absorb higher care costs associated with monitoring and complication management. Such structural treatment friction constrains sustained therapeutic adherence across the antipsychotic drugs market.

Patent Expiries and Accelerating Generic Competition Compressing Market Value

The antipsychotic drugs market faces sustained pricing pressure from patent expiries across major branded therapies. Loss of exclusivity rapidly enables generic manufacturers to introduce lower-cost alternatives across national pharmacy networks. This transition typically shifts prescription volumes away from originator brands toward competitively priced therapeutic equivalents. Patent expiration of Latuda significantly altered revenue structures across branded antipsychotic treatment portfolios. Generic producers, including Lupin and Dr. Reddy’s Laboratories, rapidly expanded supply following market entry. Broader generic availability increases treatment accessibility across public insurance systems and price-sensitive patient populations. Declining branded prescription shares compresses revenue realization across the innovator segment of the market.

These competitive dynamics reshape industry margins by shifting pricing leverage toward high-volume generic suppliers. Branded pharmaceutical developers consequently face reduced lifecycle profitability following exclusivity loss across flagship molecules. This environment compels originator companies to prioritize differentiated formulations and protected drug delivery technologies. Research pipelines increasingly emphasize complex injectable systems and extended-release pharmacological platforms. Such innovation strategies aim to preserve pricing power through regulatory exclusivity and technical formulation barriers. However, development costs and regulatory review cycles introduce additional financial risk across innovation portfolios. The patent expiries embed structural pricing pressure throughout the antipsychotic drugs' competitive landscape.

Opportunity Analysis – Integration of Digital Therapeutics with Antipsychotic Pharmacotherapy

The antipsychotic drugs market is witnessing emerging opportunities through integration with digital therapeutic platforms. Regulatory progress from the Centers for Medicare & Medicaid Services supports reimbursement pathways for prescription digital health tools. This policy shift enables pharmaceutical therapies to be paired with clinically validated monitoring applications. These digital platforms track patient adherence, behavioral symptoms, and relapse indicators across outpatient psychiatric care settings. Artificial intelligence-driven analytics strengthen clinical oversight by identifying early deterioration in patient mental health status. Such capabilities support proactive treatment adjustments and structured medication adherence monitoring within community-based care networks. Consequently, digital augmentation expands the functional scope of antipsychotic pharmacotherapy beyond conventional prescription delivery models.

Pharmaceutical developers increasingly explore integrated drug plus digital platforms to strengthen long-term treatment engagement. Connected monitoring systems generate real-world clinical data reflecting patient behavior and therapeutic outcomes. These datasets improve pharmacovigilance, post-market surveillance, and long-term treatment effectiveness assessments. Healthcare providers gain structured decision support through predictive insights derived from aggregated patient monitoring signals. Simultaneously, pharmaceutical companies obtain strategic data assets supporting therapy optimization and lifecycle management. Integrated digital ecosystems, therefore, expand commercial models across psychiatric care delivery infrastructure. This convergence of pharmacology and digital health establishes new value creation pathways across the antipsychotic drugs market.

Convergence of Long-Acting Injectable Therapies with Pharmacogenomics Guided Personalization

The antipsychotic drugs market is witnessing an emerging opportunity through the integration of long-acting injectables with pharmacogenomics. Personalized prescribing frameworks enable clinicians to match antipsychotic therapies with patient-specific genetic profiles. This alignment improves therapeutic tolerability and reduces adverse metabolic reactions frequently associated with conventional treatment. Long-acting injectable platforms further reinforce adherence by stabilizing drug exposure across extended dosing intervals. These combined advantages strengthen treatment continuity within schizophrenia and bipolar disorder management pathways. Integrated precision psychiatry models expand treatment reach across a largely underserved psychiatric population segment.

Policy frameworks increasingly encourage patient-centric drug development, integrating genomic diagnostics with therapeutic design strategies. Regulatory momentum following recent healthcare reforms emphasizes individualized treatment pathways across complex psychiatric disorders. Precision-aligned injectable therapies, therefore, gain strategic positioning within evolving clinical and reimbursement structures. Healthcare systems recognize improved tolerability as a mechanism for reducing relapse-driven hospitalization cycles. Pharmaceutical developers benefit from differentiated product positioning supported by clinically guided therapy personalization. This convergence also supports premium pricing structures within specialized psychiatric treatment markets.

Category-wise Analysis

Disease Insights

Schizophrenia is expected to lead, accounting for approximately 46% share in 2026, reflecting its entrenched role within long-term psychiatric treatment pathways across hospital and specialty care settings. Clinical management requires lifelong pharmacological maintenance due to persistent positive and negative symptom clusters, reinforcing sustained prescription demand across institutional providers. Treatment protocols increasingly rely on high-value long-acting injectable therapies to stabilize relapse-prone patient populations while improving adherence across outpatient psychiatric programs.

Major pharmaceutical portfolios from Johnson & Johnson, AbbVie, and Otsuka Pharmaceutical anchor the segment through therapies such as Invega Hafyera, Vraylar, and Abilify Maintena. These therapies combine durable efficacy with extended dosing intervals, enabling workflow stability within psychiatric hospitals and community mental health clinics.

Bipolar disorder is expected to be the fastest-growing segment, supported by expanding clinical recognition of mood spectrum disorders and the evolving role of atypical antipsychotics in mood stabilization strategies. Psychiatric practice increasingly integrates modern antipsychotic agents as first-line interventions addressing both manic and depressive phases, gradually reducing reliance on legacy lithium-centric regimens.

Pharmaceutical innovation has accelerated with portfolio expansion by companies such as Bristol Myers Squibb and Johnson & Johnson, advancing therapies including Caplyta and emerging agents such as Cobenfy targeting alternative neurochemical pathways. Long-acting injectable technologies and precision psychiatry frameworks are also expanding treatment customization across diverse bipolar patient profiles. These dynamics collectively strengthen prescription uptake across outpatient psychiatry networks.

Therapeutic Class Insights

Second-generation antipsychotics are anticipated to lead, accounting for approximately 67% share, supported by their entrenched role as first-line pharmacotherapy across psychiatric hospitals and outpatient mental health programs. These atypical agents demonstrate broad-spectrum efficacy across positive and negative schizophrenia symptoms while presenting lower extrapyramidal risk compared with legacy dopamine antagonists. Their deep integration within clinical formularies and reimbursement protocols reinforces recurring utilization across high-volume psychiatric treatment settings.

Major therapies, including Seroquel XR and Invega, anchor treatment pathways through durable safety profiles and flexible dosing formats. Pharmaceutical portfolios from Johnson & Johnson, AstraZeneca, and AbbVie maintain strong prescribing familiarity among clinicians.

Third-generation antipsychotics are expected to be the fastest-growing segment, reflecting rising clinical interest in dopamine D2 partial agonist activity that modulates dopaminergic signaling rather than full receptor blockade. This pharmacological modulation improves tolerability while addressing treatment gaps associated with negative symptoms and relapse-prone schizophrenia populations. Rapid clinical adoption is supported by therapies such as Abilify and Rexulti, which demonstrate balanced efficacy across mood and psychotic symptom domains.

Pharmaceutical innovation from Otsuka Pharmaceutical and Lundbeck continues expanding this therapeutic class through advanced receptor targeting strategies. As psychiatric practice prioritizes improved metabolic safety and cognitive outcomes, third-generation antipsychotics are positioned to expand rapidly within evolving treatment protocols.

Competitive Landscape

The U.S. antipsychotic drugs market is moderately consolidated, with leadership concentrated among major pharmaceutical developers such as Otsuka Holdings, Johnson & Johnson, and AbbVie. These firms maintain strong market influence through established antipsychotic portfolios, extensive clinical adoption, and durable distribution relationships across hospital and outpatient psychiatric networks. Their flagship therapies, including Abilify Maintena, Invega Hafyera, and Vraylar, anchor treatment protocols within schizophrenia and bipolar disorder management frameworks. Competitive positioning increasingly centers on long-acting injectable platforms, differentiated receptor pharmacology, and integrated lifecycle management strategies that reinforce physician familiarity and treatment continuity. Strategic acquisitions, neuroscience portfolio expansion, and continued innovation in extended-release delivery systems are reshaping competitive dynamics across the U.S. antipsychotic therapeutic landscape.

Key Industry Developments:

- In February 2026, Vanda Pharmaceuticals received FDA approval for Bysanti (milsaperidone) as a first-line treatment for schizophrenia and bipolar I disorder. This approval provides a new therapeutic choice with a rapid interconversion to its active metabolite, potentially improving the management of acute manic and mixed episodes. It introduces a New Chemical Entity (NCE) that expands treatment options for millions of Americans while securing a long-term competitive runway with patent protection extending into the mid-2030s.

- In February 2026, Teva Pharmaceuticals announced the FDA acceptance of its New Drug Application (NDA) for TEV-749, a once-monthly subcutaneous long-acting injection of olanzapine. This development aims to address a critical treatment gap by providing a viable long-acting formulation of a highly effective drug, significantly boosting patient adherence. EV-'749 is critical because it aims to be the first long-acting olanzapine that eliminates the FDA-mandated 3-hour post-injection monitoring period, significantly improving patient adherence and market accessibility.

Companies Covered in U.S. Antipsychotic Drugs Market

- Otsuka Pharmaceutical Co., Ltd.

- Janssen Pharmaceuticals

- AbbVie Inc.

- Bristol Myers Squibb

- Eli Lilly and Company

- Pfizer Inc.

- Teva Pharmaceutical Industries Ltd.

- Alkermes plc

- H. Lundbeck A/S

- Sumitomo Pharma

- Dr. Reddy’s Laboratories Ltd.

- AstraZeneca plc

- GlaxoSmithKline plc

- Vanda Pharmaceuticals Inc.

- Johnson & Johnson

Frequently Asked Questions

The U.S. antipsychotic drugs market is projected to reach US$12.1 billion by 2033, rising from US$8.2 billion in 2026. Market expansion reflects sustained demand for long-term psychiatric pharmacotherapy across schizophrenia and bipolar disorder treatment pathways.

Long-acting injectable antipsychotics are transforming psychiatric treatment models by improving medication adherence and reducing relapse risk among chronic patients. Extended dosing intervals allow clinicians to maintain therapeutic stability while minimizing the challenges associated with daily oral medication regimens.

The market is structured around three therapeutic classes: First Generation, Second Generation, and Third Generation antipsychotics. Second-generation antipsychotics remain the dominant class due to broad clinical efficacy and reduced neurological side effects. Third-generation agents are gaining traction through partial dopamine agonist mechanisms that provide improved tolerability and enhanced symptom control across treatment-resistant psychiatric populations.

Schizophrenia remains the leading disease segment because the condition requires lifelong pharmacological management to control persistent psychotic symptoms and prevent relapse episodes. Treatment protocols frequently incorporate advanced therapies such as long-acting injectable formulations, which reinforce medication adherence across outpatient and institutional psychiatric care programs. The chronic nature of the disorder sustains continuous prescription demand across healthcare systems.

Key market leaders include Otsuka Pharmaceutical Co., Ltd., Johnson & Johnson, AbbVie Inc., Bristol Myers Squibb, and Teva Pharmaceutical Industries Ltd. These companies strengthen their market position through established antipsychotic portfolios, ongoing R&D investments, and advanced drug delivery technologies that enhance treatment adherence and outcomes.