- Home Care & Utilities

- uPVC Windows and Doors Market

uPVC Windows and Doors Market Size, Share, and Growth Forecast 2026 - 2033

uPVC Windows and Doors Market by Product Type (Windows [Casement Windows, Sliding Windows, Tilt & Turn Windows, Fixed Windows, Others], Doors [Sliding Doors, French Doors, Casement Doors, Others]), End-user (Residential, Non-residential), and Regional Analysis, 2026 - 2033

uPVC Windows and Doors Market Size and Trend Analysis

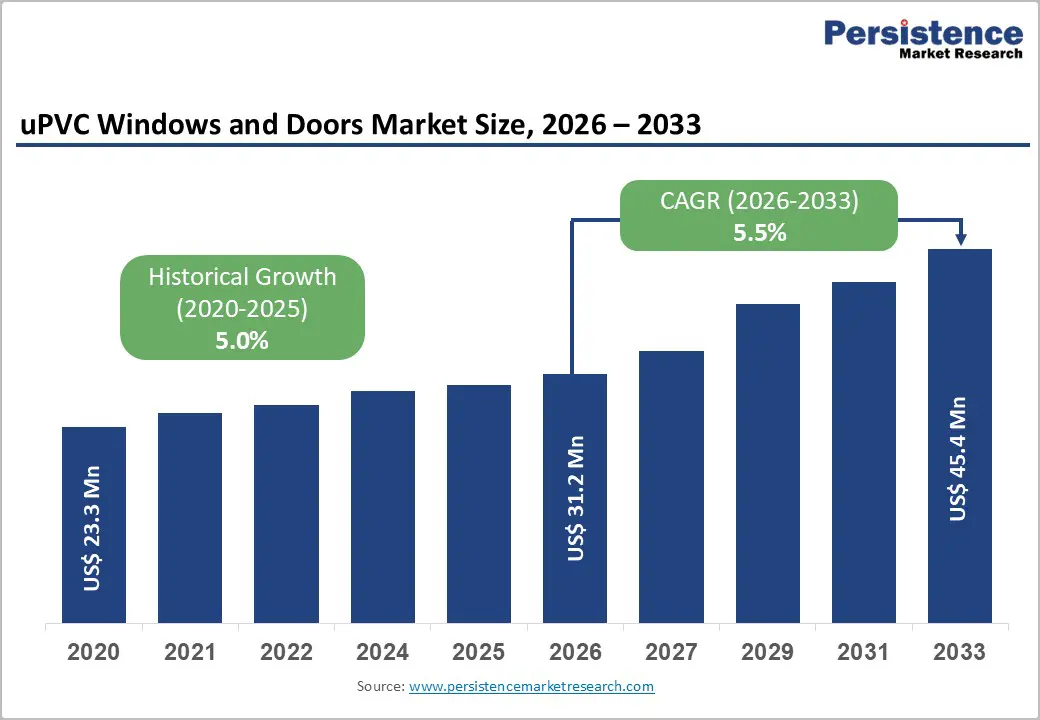

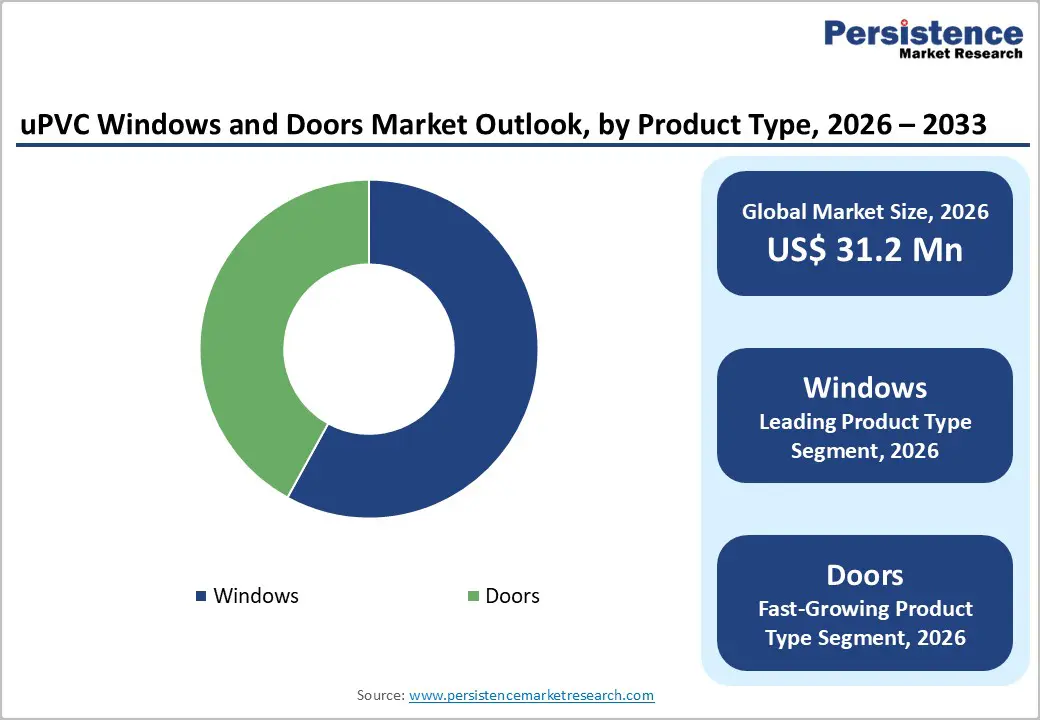

The global uPVC windows and doors market size is expected to be valued at US$ 31.2 billion in 2026 and projected to reach US$ 45.4 billion by 2033, growing at a CAGR of 5.5% between 2026 and 2033.

The market’s sustained growth trajectory is primarily underpinned by escalating demand for energy-efficient building materials across residential and commercial construction sectors. Stringent building energy codes, including the European Union’s Energy Performance of Buildings Directive (EPBD) and ASHRAE 90.1 standards in North America, are compelling architects, builders, and homeowners to adopt uPVC fenestration solutions offering superior thermal insulation, weather resistance, and sound attenuation compared to traditional aluminum or wood alternatives. Global construction output is projected to approach approximately US$ 15.2 trillion by 2030 per Global Construction Perspectives and Oxford Economics, further reinforcing downstream demand for high-performance uPVC fenestration across both new construction and retrofit segments.

Key Industry Highlights:

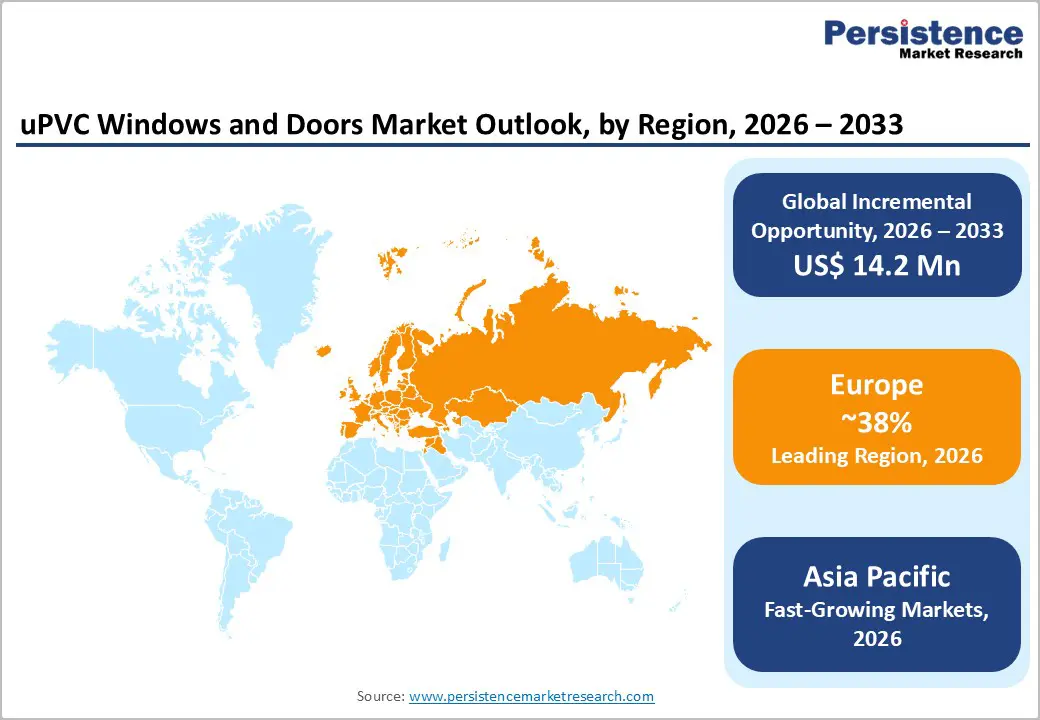

- Leading Region: Europe leads the global uPVC Windows and Doors market with approximately 38% revenue share in 2025, driven by stringent EU EPBD mandates, mature and active renovation markets, and established manufacturing hubs in Germany, Belgium, and the UK, supporting long-term structural demand stability across the region.

- Fastest Growing Region: Asia Pacific is the fastest growing regional market, propelled by large-scale urbanization across China, India, and ASEAN, supportive government housing policies including India’s PMAY and China’s 14th Five-Year Plan, and increasing consumer preference for energy-efficient and low-maintenance uPVC fenestration over traditional alternatives.

- Dominant Segment: Windows dominate the product type segment with approximately 58% market share in 2025, driven by higher installation volumes per residential unit, stringent regulatory thermal performance compliance requirements, and robust renovation demand in both mature European markets and emerging Asian construction markets.

- Fastest Growing Segment: Sliding Windows represent the fastest growing sub-segment within the product type category, reflecting growing architect and end-user preference for contemporary minimalist aesthetics, space-saving functionality, and compatibility with modern open-plan and floor-to-ceiling glazing architectural design trends.

- Key Opportunity: The EU Renovation Wave strategy targeting 35 million building retrofits by 2030 and U.S. IRA Section 25C energy efficiency tax credits of up to 30% represent transformative policy-driven opportunities for uPVC fenestration manufacturers to capture sustained, predictable replacement and retrofit demand across the world’s largest mature construction markets.

| Key Insights | Details |

|---|---|

| uPVC Windows and Doors Market Size (2026E) | US$ 31.2 Billion |

| Market Value Forecast (2033F) | US$ 45.4 Billion |

| Projected Growth CAGR (2026 - 2033) | 5.5% |

| Historical Market Growth (2020 - 2025) | 5.0% |

DRO Analysis

Market Growth Drivers

Stringent Energy Efficiency Regulations and Green Building Standards

Government-mandated energy efficiency regulations represent one of the most consequential tailwinds for the uPVC windows and doors market. The European Union’s revised Energy Performance of Buildings Directive (EPBD 2024), which requires all new buildings to achieve zero-emission standards by 2030, has catalyzed unprecedented demand for high-performance fenestration products. uPVC windows, with U-values as low as 0.8 W/m²K for triple-glazed configurations, substantially outperform conventional single-glazed aluminum counterparts in thermal performance. In the United States, the Department of Energy (DOE) estimates that fenestration accounts for approximately 25-30% of residential heating and cooling energy losses, driving renovation and retrofit activity toward thermally efficient uPVC systems. Similar mandates in Japan, South Korea, and Australia, where the National Construction Code (NCC) 2022 raised energy efficiency requirements for residential buildings, are amplifying adoption across geographically diverse markets, creating a broad and sustained regulatory demand base.

Rapid Urbanization and Residential Construction Boom in Emerging Economies

Accelerating urbanization across emerging economies is creating structural demand for cost-effective, durable, and low-maintenance fenestration solutions, positioning uPVC windows and doors favorably against competing materials. According to the United Nations Department of Economic and Social Affairs (UN DESA), approximately 2.5 billion additional people are projected to live in urban areas by 2050, with the majority of this growth concentrated in Asia, Africa, and Latin America. India’s Pradhan Mantri Awas Yojana (PMAY), targeting the construction of 20 million affordable urban housing units, and China’s ongoing new-town development projects are generating massive downstream demand for uPVC fenestration. uPVC’s price competitiveness versus aluminum, estimated at 15-20% lower lifecycle costs per the Construction Products Association, makes it the preferred material for mid-to-affordable housing segments in high-growth markets.

Restraints - Volatile Raw Material Prices and Supply Chain Disruptions

The uPVC windows and doors industry is significantly exposed to fluctuations in polyvinyl chloride (PVC) resin prices, which are intrinsically tied to ethylene and chlorine feedstock costs, derivatives of crude oil and natural gas. PVC resin prices surged by approximately 40% between 2020 and 2022, driven by pandemic-induced supply disruptions and energy market volatility, severely compressing manufacturer margins. The European Chemical Industry Council (CEFIC) has flagged ongoing energy cost pressures in European PVC production as a structural concern. Supply chain dependencies on chlorine, largely produced through energy-intensive chlor-alkali electrolysis, expose manufacturers to persistent input cost volatility, making long-term pricing commitments to construction contractors challenging and constraining the market’s ability to scale profitably during periods of feedstock instability.

Growing Environmental Concerns Around PVC Recyclability and End-of-Life Management

Despite uPVC’s operational energy efficiency benefits, mounting regulatory and consumer scrutiny over its end-of-life environmental footprint poses a restraint on market expansion, particularly in environmentally conscious markets. The European Commission’s Circular Economy Action Plan and the Regulation on Construction Products (RCP) impose stricter recyclability and environmental disclosure requirements on building materials. While Recovinyl, the PVC industry recycling network, reported recycling over 800,000 tonnes of PVC in 2022, critics argue that uPVC window frames containing legacy lead-based heat stabilizers present recycling challenges. This perception risk is pushing some specifiers toward alternative materials including aluminum with thermal breaks or fiberglass composites in premium project segments, creating substitution risk for uPVC manufacturers.

Opportunities - Smart Window Integration and Technological Innovation in uPVC Fenestration

The convergence of uPVC fenestration with smart building technologies presents a transformative opportunity for market participants. Integration of electrochromic glazing, sensor-embedded frames, and IoT-enabled actuators into uPVC window and door systems aligns with the global smart home solutions market, valued at approximately US$ 113.4 billion in 2025, offering significant cross-selling potential and margin enhancement. Manufacturers who incorporate features such as automated ventilation control, integrated noise sensors, and real-time thermal performance monitoring into their uPVC product lines can command 15-25% price premiums over standard offerings. The German Federal Ministry for Economic Affairs and Climate Action’s funding programs for smart retrofitting of existing building stock signal strong policy support for this innovation direction. Companies including REHAU Group and VEKA Group have already initiated R&D collaborations with advanced glazing technology firms, reinforcing the commercial viability of technologically enhanced uPVC fenestration systems.

Renovation and Retrofit Wave in Aging European and North American Building Stock

The vast aging building stock across Europe and North America represents a multi-decade retrofit opportunity for uPVC window and door manufacturers. According to the European Commission, approximately 75% of buildings in the EU are energy-inefficient, and only 0.2% of the building stock undergoes deep renovation annually, highlighting the enormous untapped retrofit potential. Programs such as the EU’s Renovation Wave strategy, targeting the renovation of 35 million buildings by 2030, and the U.S. Inflation Reduction Act (IRA) provisions offering tax credits of up to 30% on qualifying energy-efficient home improvements under Section 25C, including windows and doors, are expected to unlock sustained replacement demand. The average installed lifespan of windows being 20-30 years means that a substantial share of post-1990s residential building stock across mature markets is approaching replacement cycles, creating predictable, policy-reinforced long-term demand for uPVC fenestration manufacturers.

Category-wise Analysis

Product Type Insights

Windows dominate the uPVC Windows and Doors market, commanding approximately 58% of the overall revenue share in 2025. This leadership is attributable to the significantly higher volume of window installations per building unit compared to doors, as well as the greater diversity of window typologies addressing specific architectural, ventilation, and aesthetic requirements. Casement windows represent the largest sub-segment within the windows category, valued for their airtight seal and unobstructed ventilation capability, characteristics that directly support compliance with thermal performance standards including Passive House (Passivhaus) certification and the EU’s EPBD. Globally, new residential construction typically incorporates 8-12 window units per dwelling, compared to 2-4 door units, reinforcing the structural volume advantage of the windows category. The segment is further supported by growing renovation activity in mature markets across Europe and North America and rapid new-build construction in emerging economies across Asia Pacific.

End-user Insights

The residential segment leads the uPVC Windows and Doors market, accounting for approximately 65% of total market revenue in 2025. Residential construction, encompassing new builds and renovation activity, consistently generates the highest volume of fenestration demand globally, driven by household formation rates, urbanization dynamics, and government housing programs. The National Association of Home Builders (NAHB) in the United States reported approximately 1.4 million new housing starts in 2023, each representing a direct demand opportunity for uPVC fenestration. In Europe, where Euroconstruct estimates residential renovation accounts for over 55% of total construction output in key markets like Germany and France, uPVC windows and doors benefit from both regulatory mandates and homeowner preference for energy-saving upgrades. The residential segment’s market leadership is further reinforced by comparatively lower price sensitivity in homeowner procurement compared to large-scale commercial tenders, enabling manufacturers to sustain healthier margin profiles.

Regional Insights

North America uPVC Windows and Doors Market Trends and Insights

North America represents a significant and structurally growing market for uPVC windows and doors, anchored by the United States, where residential renovation expenditure exceeded US$ 480 billion in 2023 per the Joint Center for Housing Studies of Harvard University. The U.S. Department of Energy (DOE) ENERGY STAR® program certifies fenestration products meeting specific U-factor and Solar Heat Gain Coefficient (SHGC) thresholds, with ENERGY STAR-certified windows estimated to save homeowners between US$ 101 and US$ 583 annually in energy costs, a compelling consumer value proposition driving product upgrade demand. Canada’s National Energy Code for Buildings (NECB) similarly mandates improved window thermal performance in new construction across provincial jurisdictions.

The U.S. Inflation Reduction Act (IRA) has introduced tax credits of up to 30% for qualifying energy-efficient windows and exterior doors under Section 25C, directly stimulating the replacement market. The Efficient Windows Collaborative (EWC), a consortium of government agencies and industry participants, continues to drive consumer education and specification upgrades across the region. uPVC’s market penetration in North America remains below European levels, where wood and aluminum composites have historically dominated specification preferences, indicating significant headroom for growth as cost-benefit awareness among contractors and homeowners continues to improve through government-supported outreach programs.

Europe uPVC Windows and Doors Market Trends and Insights

Europe remains the dominant region in the global uPVC Windows and Doors market, holding approximately 38% of global revenue share in 2025. Germany, the United Kingdom, and France collectively represent the core demand centers, underpinned by mature renovation markets and some of the world’s most stringent building energy regulations. Germany’s Building Energy Act (Gebäudeenergiegesetz - GEG), which came into full effect in 2024, mandates near-zero energy standards for new buildings and incentivizes thermal envelope upgrades in existing stock through KfW Bank’s federal grant programs, offering grants of up to €60,000 per household for comprehensive energy refurbishment. The UK’s Social Housing Decarbonization Fund is channeling investment toward fenestration upgrades across publicly owned residential housing stock.

Major European uPVC manufacturers, including VEKA Group, Rehau Group, Aluplast, and Deceuninck NV, maintain significant production and R&D presence in Germany and Belgium, benefiting from proximity to demand centers and established recycling infrastructure through networks such as Recovinyl. The RAL quality mark for uPVC windows and doors, administered by the RAL German Institute for Quality Assurance and Certification, ensures product quality standardization across European markets, serving as a trusted specification benchmark. Spain, Poland, and Czech Republic represent high-growth sub-markets within the region, driven by EU Cohesion Fund-backed residential construction and renovation programs supporting convergence with Western European energy efficiency standards.

Asia Pacific uPVC Windows and Doors Market Trends and Insights

Asia Pacific is the fastest growing regional market for uPVC windows and doors, propelled by China, India, and ASEAN economies, where large-scale urbanization and infrastructure investment are generating structural fenestration demand. China, as the world’s largest construction market, continues to drive uPVC consumption, with the country’s 14th Five-Year Plan (2021-2025) emphasizing green building standards and energy conservation in new urban developments. China’s Green Building Evaluation Standard (GB/T 50378) has encouraged widespread adoption of thermally efficient fenestration systems in both commercial and residential projects, creating a regulatory environment increasingly comparable to European EPBD mandates in its scope and enforcement.

India represents one of the most dynamic growth opportunities in the region, with the government’s Smart Cities Mission covering 100 cities and the Real Estate Regulatory Authority (RERA) driving quality consciousness among developers and homebuyers. LG Hausys Ltd. and Fenesta Building Systems, a subsidiary of DCM Shriram, have significantly expanded their manufacturing and distribution footprints across India’s rapidly urbanizing Tier-1 and Tier-2 cities. ASEAN markets, particularly Vietnam, Indonesia, and Malaysia, are witnessing accelerating uPVC adoption driven by tourism-linked hospitality construction, rising middle-class housing aspirations, and improving raw material supply chains that are reducing cost barriers for regional manufacturers and fabricators.

Competitive Landscape

The global uPVC windows and doors market demonstrates a moderately consolidated structure, characterized by the presence of strong regional players alongside a limited number of globally integrated manufacturers. Regional leaders maintain dominance in domestic markets through established distribution networks and localized fabrication capabilities, while larger multinational participants compete across geographies with standardized product portfolios and scalable operations.

Competition is primarily driven by product differentiation, particularly in thermal insulation performance, acoustic efficiency, and customization capabilities supported by digital configuration tools. Leading players are increasingly adopting vertically integrated models, encompassing compounding, extrusion, and fabrication, to enhance cost efficiency and supply chain control. Meanwhile, mid-sized companies rely on strategic partnerships with regional distributors and fabricators to expand market reach. Sustainability is becoming a key competitive parameter, with growing emphasis on recycled material usage and certified environmental performance to strengthen positioning in commercial and institutional projects.

Key Developments

- February 2025: VEKA Germany acquired full ownership of its Indian joint venture and announced plans to invest INR100 crore over six years to expand manufacturing capacity, develop export hubs, and strengthen its presence in the growing construction market.

- July 2025: Apollo Pipes Limited launched uPVC doors and windows, adding over 250 SKUs with an annual capacity of 4,000 tonnes, marking its entry into building materials expansion and strengthening its product portfolio in the construction segment.

- July 2025: SBM Gold announced its expansion into uPVC doors and windows, diversifying beyond HDPE pipes to offer integrated building solutions, strengthening its position in India’s infrastructure sector with a broader, multi-product portfolio.

Companies Covered in uPVC Windows and Doors Market

- Fenesta Building Systems

- Prominance Window Systems

- Koemmerling (Profine Group)

- VEKA Group

- Rehau Group

- Internorm International

- Eurocell PLC

- Aluplast

- LG Hausys Ltd.

- Pella Corporation

- Andersen Corporation

- Deceuninck NV

- JELD-WEN Holding, Inc.

- Crystal Windows and Doors

- Simonton Windows and Doors

- Schüco International KG

- Gealan Fenster-Systeme GmbH

- KOMMERLING Chemische Fabrik GmbH

Frequently Asked Questions

The uPVC windows and doors market is expected to reach US$ 31.2 billion in 2026.

Demand is driven by energy efficiency regulations, urbanization, construction growth, and low-maintenance benefits.

Europe leads the uPVC windows and doors market with the largest revenue share.

Opportunities lie in retrofit projects, energy-efficiency incentives, and smart building integration.

The uPVC windows and doors market includes a mix of global manufacturers and strong regional players.