- Renewable Energy

- Ultra-thin Solar Cells Market

Ultra-thin Solar Cells Market Size, Share, and Growth Forecast 2026 - 2033

Ultra-thin Solar Cells Market by Material (Cadmium Telluride, Copper Indium Gallium Selenide, Perovskite Solar Cell), Installation (On-grid, Off-grid), End-user (Residential, Commercial), and Regional Analysis, 2026 - 2033

Ultra-thin Solar Cells Market Size and Trends Analysis

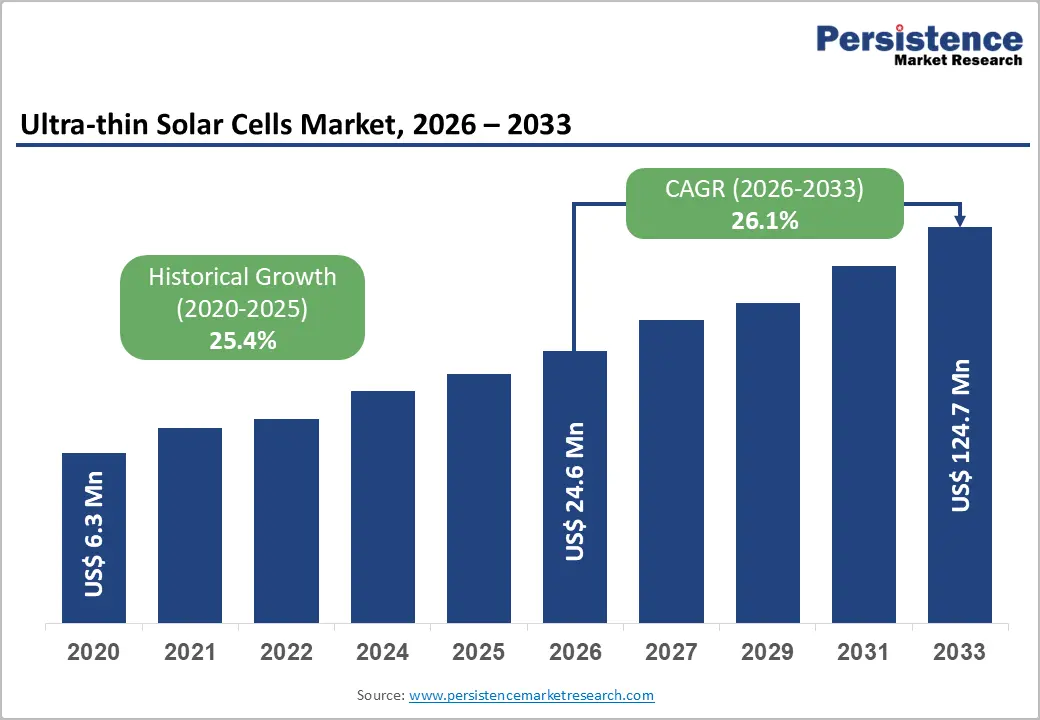

The global ultra-thin solar cells market size is likely to be valued at US$24.6 million in 2026 and is expected to reach US$124.7 million by 2033, growing at a CAGR of 26.1% during the forecast period from 2026 to 2033, driven by increasing investments in perovskite and tandem solar technologies aimed at improving efficiency and reducing material usage. Rising demand for lightweight and flexible solar solutions in portable electronics, electric vehicles, and building-integrated photovoltaics is further spurring adoption.

Key Industry Highlights:

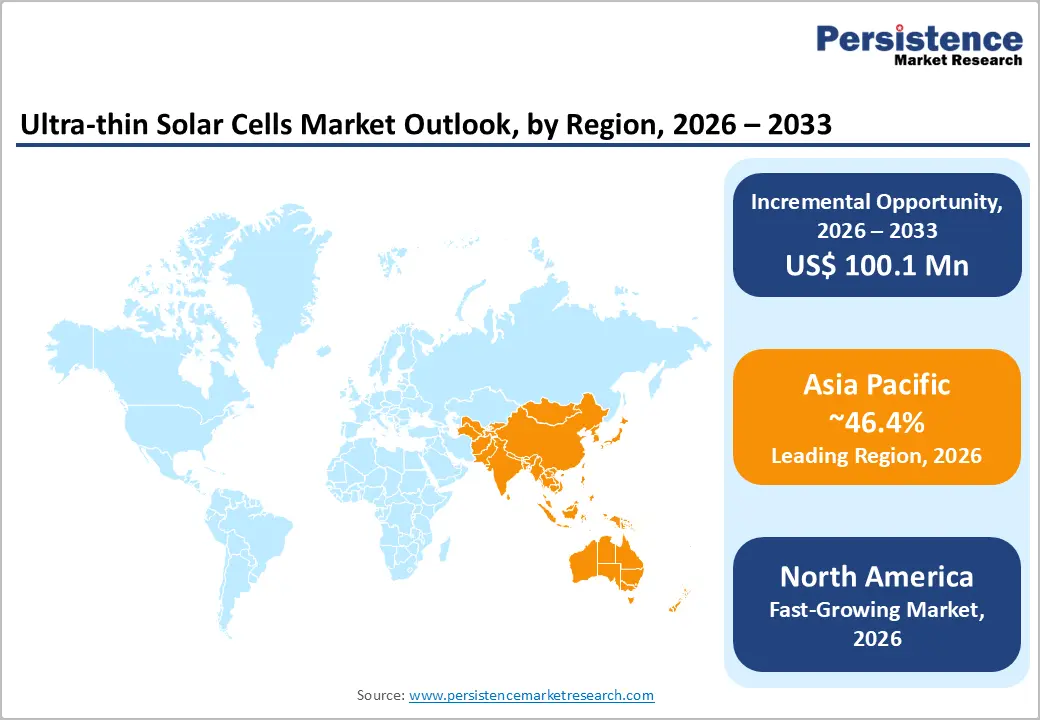

- Leading Region: Asia Pacific, with about 46.4% share in 2026, spurred by a strong manufacturing base in countries such as South Korea and China.

- Fast-growing Region: North America, fueled by rising federal funding from agencies such as the U.S. Department of Energy.

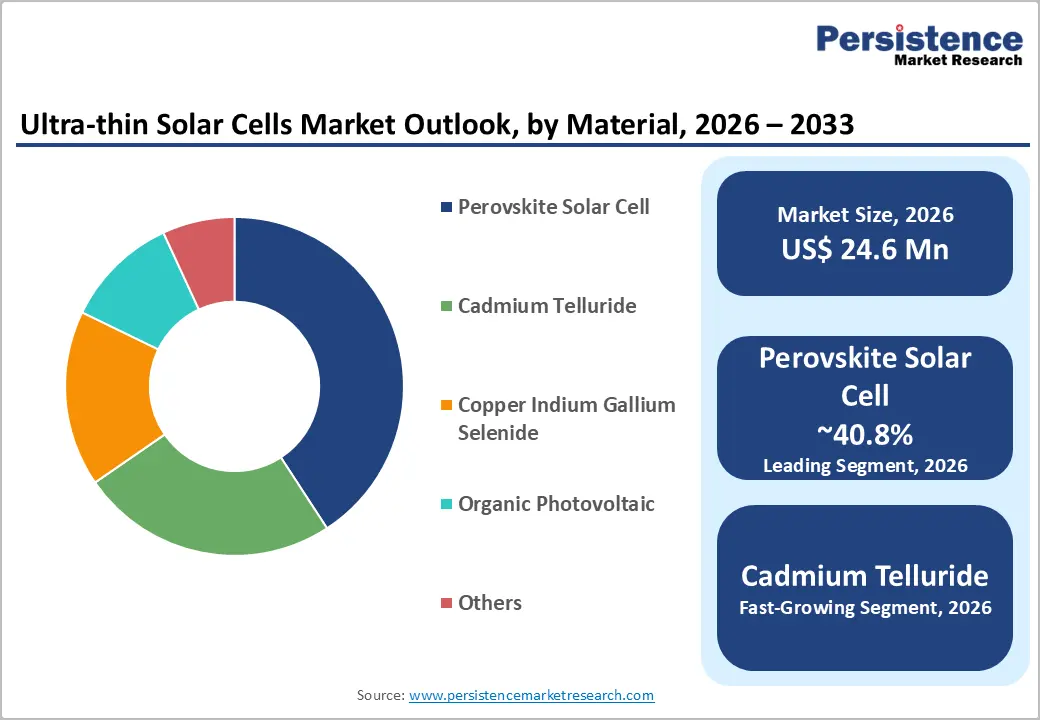

- Leading Material: Perovskite solar cell, approximately 40.8% share in 2026, as it supports low-cost and flexible manufacturing methods, including roll-to-roll printing.

- Dominant End-user: Commercial, nearly 66.3% in 2026, as companies are adopting ultra-thin solar for building-integrated solutions such as facades and rooftops to meet sustainability targets.

- Latest Agreement: In November 2025, Ascent Solar Technologies and CisLunar Industries signed a teaming agreement to combine Ascent's flexible thin-film photovoltaic technology with CisLunar's high-efficiency power conversion and conditioning systems. The partnership targets U.S. space customers, including NASA, the Department of Defense, and the Space Force.

DRO Analysis

Driver - Policy Push to Boost Adoption of Next-Gen Solar Materials

Governments are now funding ultra-thin solar research as part of energy transition plans, not just conventional silicon. The U.S. Department of Energy’s Solar Energy Technologies Office has backed perovskite and thin-film research and development with multi-year grants, focusing on flexible and lightweight modules for building integration. In 2024, the European Commission expanded funding under Horizon Europe for tandem and ultra-thin photovoltaics to improve efficiency while reducing material use.

India is also supporting advanced PV under its National Green Hydrogen Mission, where lightweight solar is useful for decentralized hydrogen production. These policies are not just subsidies. They focus on pilot-scale validation and commercialization. This reduces risk for manufacturers and speeds up deployment in niche areas such as curved surfaces and portable energy systems.

Rising Demand for Portable and Off-Grid Energy Solutions

Ultra-thin solar cells are gaining traction where traditional panels fail due to weight and rigidity. Their flexibility allows integration into tents, backpacks, and temporary shelters. The U.S. Army has tested flexible solar blankets to reduce battery load for soldiers, improving mobility during field operations. Disaster response agencies are also adopting lightweight solar kits for quick deployment after cyclones and earthquakes.

A 2023 report from the International Renewable Energy Agency highlighted that portable solar solutions are increasingly used in remote healthcare units across Africa and Southeast Asia. These cells can be rolled, transported easily, and installed without heavy infrastructure. This makes them suitable for remote telecom towers, refugee camps, and rural electrification projects where logistics remain a challenge.

Restraint - Efficiency Limitations to Affect Large-Scale Energy Output

Ultra-thin solar cells still struggle to match the performance of crystalline silicon panels. Their reduced thickness limits light absorption, which directly affects power output. Research published in journals such as Nature Energy shows that while perovskite ultra-thin cells are improving, stability and efficiency drop under real-world conditions such as heat and humidity.

For example, several flexible perovskite cells degrade faster when exposed to moisture, requiring advanced encapsulation. This adds cost and complexity. The National Renewable Energy Laboratory has also noted that extending lab efficiencies to commercial modules remains a challenge. Hence, more surface area is required to generate the same electricity. This makes them less practical for utility-scale projects where space and long-term reliability are the main factors.

Opportunity - Emergence of See-Through Solar Materials for Building Integration

Transparent ultra-thin solar cells are creating new use cases in urban infrastructure. Researchers at Nanyang Technological University developed near-invisible perovskite cells that are thousands of times thinner than a human hair. These cells allow visible light to pass through while still generating electricity, with reported efficiencies between 7% and 12%. It makes them suitable for windows, glass facades, and even car sunroofs.

The concept is associated with building-integrated photovoltaics, where surfaces double as energy generators. The U.S. Department of Energy has also supported similar projects to turn skyscraper glass into power sources. This approach reduces reliance on rooftop panels and uses existing surfaces, especially in dense cities where space is limited.

Developments in Mass Manufacturing to Improve Commercial Viability

New production methods are addressing one of the most prominent barriers, i.e., mass manufacturing. Vacuum-based deposition techniques now allow ultra-thin absorber layers, sometimes as thin as 10 nanometers, to be produced with high uniformity. Research backed by institutions such as MIT and published in peer-reviewed journals shows that these methods can improve film quality and reduce defects.

In 2024, several pilot lines in Europe demonstrated roll-to-roll processing for flexible solar films, which lowers production costs compared to traditional wafer-based methods. This shift is important as it supports continuous manufacturing rather than batch processing. As expandability improves, ultra-thin solar cells are moving closer to commercial deployment in sectors such as wearables, automotive surfaces, and lightweight electronics.

Category-wise Analysis

Material Insights

The perovskite solar cell segment is predicted to dominate with nearly 40.8% of the share in 2026. It provides high efficiency with low production costs, which no other thin-film material has managed at this level. Its exceptional optoelectronic properties, low manufacturing costs, high power conversion efficiencies, and potential for lightweight as well as flexible applications also augment demand. Manufacturing flexibility adds another key advantage. Techniques such as vacuum flash evaporation, blade coating, slot-die coating, and roll-to-roll processing have emerged as promising approaches.

Cadmium telluride (CdTe) is expected to remain in the second position in the forecast period. It has earned its place as a commercially proven thin-film material due to its unique physical properties and cost advantage. First Solar, the dominant CdTe player, continues to raise the bar. Its CdTe-based CuRe semiconductor platform delivered initial modules to customers in 2025 following a limited commercial production run. Laboratory and field testing demonstrated advantages in temperature coefficient, degradation behavior, and bifaciality.

End-user Insights

The commercial segment is projected to lead with a share of approximately 66.3% in 2026, as large buildings provide the ideal canvas for ultra-thin solar integration. Office towers, retail centers, and campuses have expansive facades and rooftops that conventional rigid panels cannot easily cover.

The segment is also being pushed by businesses seeking lightweight and space-efficient solar solutions for retrofitting and new construction. Ultra-thin solar cells are now integrated into building facades, glass windows, and rooftops through Building-Integrated Photovoltaics (BIPV). It is due to their ability to blend with architectural designs while contributing to LEED and other sustainability certifications, making them attractive in dense urban markets.

The residential segment is anticipated to be the fastest-growing over the forecast period. Homeowners are increasingly drawn to ultra-thin solar cells as they solve the aesthetic problem that kept many from adopting rooftop solar in the first place. Thin, flexible panels blend into rooflines and irregular surfaces without the bulky frames of traditional panels. Policy mandates are also accelerating this shift. In March 2025, for example, Tokyo's municipal government approved an ordinance requiring solar panel installation on all new detached houses from April 2025 onwards. It significantly catalyzed residential BIPV adoption in Japan and set a model that had spread nationally and across Asia Pacific.

Regional Insights

Asia Pacific Ultra-thin Solar Cells Market Trends

In 2026, Asia Pacific is expected to dominate with nearly 46.4% of the share. It houses the world’s largest solar manufacturing base. Growth is also spurred by increasing government support for renewable energy adoption, large-scale solar installations, and expanding manufacturing capabilities across countries such as China, India, and Japan. These countries are racing to lead on next-generation solar. This means ultra-thin cells, especially perovskite, are receiving targeted national funding alongside an established industrial ecosystem that can quickly extend production.

China Ultra-thin Solar Cells Market Trends

China is in a league of its own when it comes to ultra-thin solar expansion. The country holds around 757 GW of operating wind and solar power plants and an additional 750 GW under construction, anticipated to commence by 2025. It is also moving into manufacturing. China held over 33,300 patents related to perovskite technology by October 2025. In February 2025, UtmoLight launched a 1 GW production line in Wuxi capable of churning out 1.8 million modules annually, while Renshine Solar secured US$171 million to construct an 80,000-square-meter factory in Changshu. The government further allocated RMB 20 billion to its Solar Innovation Program in 2024, focused on perovskite solar cell research and infrastructure development.

South Korea Ultra-thin Solar Cells Market Trends

South Korea is positioning itself as the precision engineering hub for ultra-high-efficiency thin-film tandem cells. Rather than competing on volume, it is competing on performance. The country’s Ministry of Economy and Finance announced a KRW 33.6 billion plan to help the domestic PV industry develop commercial perovskite-silicon tandem solar products by 2030, to commercialize 28%-efficient modules. Qcells also announced a US$100 million investment to build a pilot tandem-cell production line at its Jincheon factory in South Korea. The firm developed a perovskite-silicon tandem solar cell with 28.6% efficiency.

North America Ultra-thin Solar Cells Market Trends

North America is predicted to be the fastest-growing market in the forecast period. It is attributed to federal funding, tax incentives, and a strategic push to build a domestic thin-film supply chain independent of China-based manufacturing. From the Inflation Reduction Act's enactment in Q3 2022 through Q1 2025, actual investments in U.S.-based manufacturing of clean energy technologies totaled US$115 billion. It was a dramatic increase from the US$21 billion invested in the same period preceding the law.

U.S. Ultra-thin Solar Cells Market Trends

The U.S. is the most active market for ultra-thin solar research and development. It is increasingly converting research into production. Research institutions and start-ups across California, Massachusetts, and New York are spearheading perovskite commercialization efforts, supported by federal grants and the Department of Energy (DOE) innovation programs targeting next-generation photovoltaics. Perovskite materials are enabling ultra-thin and low-cost solar cells via extendable roll-to-roll manufacturing that complies with U.S. goals for domestic clean energy supply chains.

Europe Ultra-thin Solar Cells Market Trends

Europe's growth is anchored in research leadership, favorable climate policy, and early commercialization by key players. Growth is also fueled by leading research institutions, government funding programs, and surging renewable energy targets, with domestic companies leading commercialization efforts. Oxford PV, for instance, achieved the milestone of first commercial tandem module shipments to international markets. The region benefits from Fraunhofer institutes, Imperial College London, and the University of Oxford, all producing high-impact perovskite research, giving key firms a steady pipeline of advances to commercialize.

Germany Ultra-thin Solar Cells Market Trends

Germany is the manufacturing home of Europe's most commercially advanced ultra-thin solar producer. Oxford PV's facility in the country operates at 100 MW annual capacity, solidifying its position as a key player in industrial-scale perovskite production. The company has ambitious plans ahead. Its current module series reaches 25% module efficiency, with plans to launch a 26% product in 2026. Qcells' local research and development center has already produced modules that passed IEC 61215 stress testing for UV exposure, thermal cycling, humidity freeze, and damp heat, verified by TÜV Rheinland.

U.K. Ultra-thin Solar Cells Market Trends

The U.K.’s global leadership in perovskite-silicon tandem cell technology stems from decades of materials science research at institutions such as the University of Oxford and Imperial College London. These have produced over 600 high-impact perovskite publications since 2020. National targets are creating a runway for thin-film deployment. The U.K. Department for Energy Security and Net Zero aims to deploy 70 GW of solar by 2035, with tandem cells expected to supply 30% of new installations due to their land use efficiency.

Competitive Landscape

The global ultra-thin solar cells market is fragmented, with the presence of start-ups, university spin-offs, thin-film specialists, and established solar manufacturers competing to commercialize next-generation technologies. Companies such as Oxford PV, First Solar, Renshine Solar, Heliatek, and Ascent Solar Technologies are among the notable participants investing in ultra-thin and flexible photovoltaic technologies. Competition is centered on improving efficiency, flexibility, durability, and mass manufacturing.

Another important feature of the market is the key role of research institutions and public-private collaborations. Several technologies are still transitioning from pilot scale to mass production. Europe’s projects supported by Horizon Europe are focusing on bendable and roll-to-roll manufactured solar films to improve stability and lower production costs. A few players are also racing to secure intellectual property rights as commercialization depends heavily on patented materials and deposition techniques.

Key Industry Developments:

- In March 2026, GCL Optoelectronics secured China's first commercial perovskite-silicon tandem module order, winning a 1.2 MW procurement project launched by Huaneng Clean Energy Research Institute. The tender required modules with a mass-production conversion efficiency of at least 26%, full IEC 61215 and IEC 61730 certification, and supply capability from a production line of at least 100 MW.

- In January 2026, UtmoLight won the bid for the Phase IV PV project at the National PV and Energy Storage Demonstration Platform (Daqing Base), led by SPIC. It will supply 1 MW of large-format perovskite modules, each measuring 2.81 square meters.

- In January 2026, UtmoLight partnered with the University of New South Wales (UNSW) to jointly establish an International Joint Perovskite Laboratory. In the laboratory, partners are expected to conduct collaborative research on new perovskite technologies as well as jointly promote the industrialization of perovskite PV technologies.

Companies Covered in Ultra-thin Solar Cells Market

- Greatcell Solar Limited

- Exeger Operations AB

- Fujikura Europe Ltd.

- G24 Power Ltd.

- Konica Minolta Sensing Europe B.V.

- Merck KGaA

- Oxford PV

- Peccell Technologies, Inc.

- Sharp Corporation

- Solaronix SA

Frequently Asked Questions

The global ultra-thin solar cells market is projected to be valued at US$24.6 million in 2026.

The ultra-thin solar cells market is expected to reach US$124.7 million by 2033.

Shift toward transparent solar panels and the emergence of roll-to-roll expandable manufacturing technologies are a few key market trends.

Perovskite solar cells are expected to be the leading material with a share of nearly 40.8% in 2026, backed by their high efficiency even in ultra-thin form.

The ultra-thin solar cells market is expected to grow at a CAGR of 26.1% from 2026 to 2033.

Greatcell Solar Limited, Exeger Operations AB, Fujikura Europe Ltd., and G24 Power Ltd. are a few key market players.