- Automation & Robotics

- Tunnel Construction Market

Tunnel Construction Market Size, Share, and Growth Forecast 2026 - 2033

Tunnel Construction Market by Technology (Ground Penetrating Radar (GPR), In-tunnel Scouting Robots, Ground Robots, Surface Seismic Systems, Microgravity Detection Systems (MDSs), UGV-based Systems, Resistive & Tomography, Electromagnetic Systems (excluding GPR), Others), End-use, and Regional Analysis, 2026 - 2033

Tunnel Construction Market Size and Trend Analysis

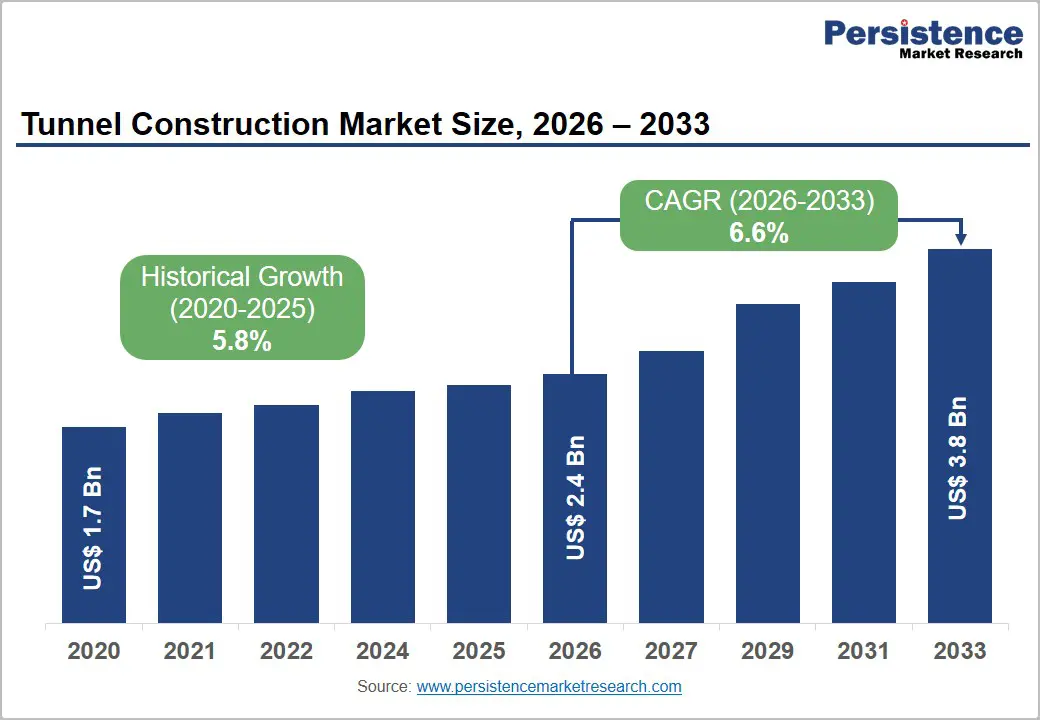

The global tunnel construction market is expected to be valued at US$ 2.4 billion in 2026 and projected to reach US$ 3.8 billion by 2033, growing at a CAGR of 6.6% between 2026 and 2033.

Rising global investments in underground infrastructure, driven by rapid urbanization, metro rail expansion, and the push for resilient utilities networks, are the primary forces propelling market growth.

Advanced detection and survey technologies, such as Ground-Penetrating Radar (GPR) and UGV-based systems, are increasingly integrated into tunneling projects, enhancing safety and construction efficiency while shortening project timelines, further accelerating adoption across both public and private sectors.

Key Industry Highlights

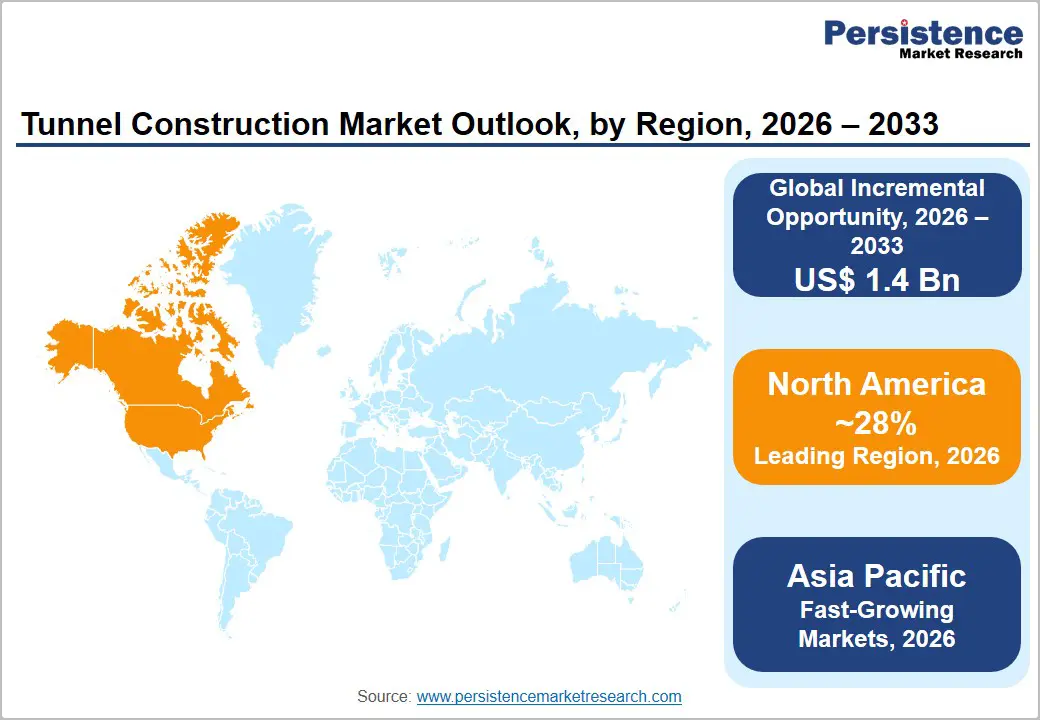

- Leading Region: North America is likely to dominate with a 28% share in 2026, driven by federal infrastructure funding under the IIJA and mandatory national tunnel inspection programs managed by the FHWA.

- Fastest Growing Market: Asia Pacific is the fast-growing market at 8% CAGR, propelled by China's metro network expansion, India's NIP investments, and rising Southeast Asian infrastructure development activity.

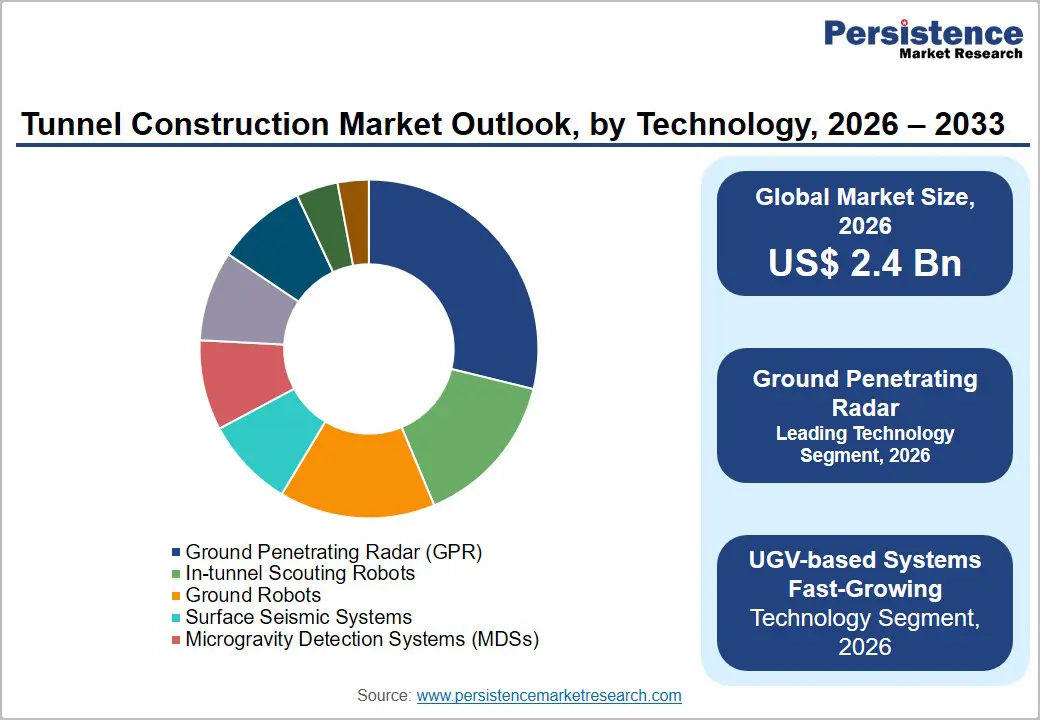

- Dominant Technology Segment: Ground Penetrating Radar (GPR) leads the Technology category with 23% market share in 2026, underpinned by regulatory mandates for pre-construction subsurface mapping and non-destructive tunnel inspection.

- Fastest Growing Technology Segment: UGV-based Systems are the fastest-growing technology at 7% CAGR, driven by automation mandates, aging infrastructure rehabilitation needs, and autonomous inspection efficiency gains of up to 60%.

- Key Opportunity: Mining sector digitalization and regulatory-driven safety compliance are creating high-value, recurring procurement opportunities for integrated underground sensing and robotic platforms, with global mining technology investment exceeding US$ 15 billion in 2023.

DRO Analysis

Drivers - Rising Global Investment in Underground Urban Infrastructure

The accelerating pace of urbanization worldwide is creating unprecedented demand for underground transit and utility networks. According to the United Nations, nearly 68% of the global population is projected to live in urban areas by 2050, compelling governments to develop metro rail, road tunnels, and underground utility corridors. The International Tunneling and Underground Space Association (ITA-AITES) estimates that global investment in underground infrastructure has exceeded US$200 billion annually in recent years.

Major programs such as the European Union's TEN-T network and national rail modernization plans in the U.S., India, and China are channeling significant capital into tunnel construction. Emerging demand for underground energy transmission and water management systems adds further volume, sustaining a robust multi-year order pipeline for contractors and technology providers alike.

Integration of Advanced Sensing and Robotic Technologies in Tunneling

The adoption of intelligent surveys and monitoring technologies is fundamentally reshaping the economics of tunnel construction and safety standards. Ground-penetrating radar (GPR) systems now enable non-invasive subsurface mapping with up to 30% higher resolution than legacy methods, significantly reducing unexpected geological encounters. Concurrently, the deployment of Unmanned Ground Vehicles (UGVs) and in-tunnel scouting robots is growing rapidly, driven by stringent worker safety regulations, including the Occupational Safety and Health Administration (OSHA) in the U.S. and equivalent directives in Europe.

According to the International Labor Organization (ILO), construction remains among the highest-risk sectors globally, accelerating the mandatory shift toward remote and automated inspection tools. This technology transition directly expands market revenue per project across both greenfield and rehabilitation tunnel programs.

Restraints - High Capital Expenditure and Complex Project Financing

Tunnel construction projects are among the most capital-intensive civil engineering undertakings, with per-kilometer costs for urban metro tunnels commonly ranging between US$ 50 million and US$ 300 million depending on geology and depth, as documented by the McKinsey Global Infrastructure Initiative and various government audit bodies.

This scale of investment creates significant barriers for smaller economies and project owners in developing nations who face limited access to long-term infrastructure financing. Cost overruns, historically averaging 45% above initial estimates on megaprojects, per Oxford University's Saïd Business School research, deter private investment and slow project approvals, constraining the overall market pipeline.

Skilled Labor Shortages and Geotechnical Risk Uncertainty

The global shortage of qualified tunneling engineers and specialized operators represents a structural restraint on market growth. The European Federation of Engineering Consultancy Associations (EFCA) has documented a widening skills gap in geotechnical and underground construction disciplines across Europe, with vacancy rates for senior tunnel engineers exceeding 20% in several countries.

Opportunities - Expansion of UGV-based Systems for Autonomous Tunnel Inspection

The fastest-growing technology segment, UGV-based systems, projected at a CAGR of 7% between 2026 and 2033, presents a compelling commercial opportunity for technology developers and system integrators. Governments across North America, Europe, and the Asia Pacific are mandating periodic structural health monitoring of aging tunnel infrastructure. In the United States, the Federal Highway Administration (FHWA) requires biennial inspections of all tunnels on the National Highway System, covering over 400 tunnels nationwide.

Autonomous UGV platforms capable of LiDAR scanning, crack detection, and thermal imaging reduce inspection time by up to 60% compared to manual methods, according to pilot programs in Japan and Germany. As tunnel inventories globally grow and aging infrastructure rehabilitation becomes urgent, recurring inspection service contracts represent a high-margin, recurring revenue opportunity for market participants.

Emerging Demand from Mining Sector Digitalization and Safety Compliance

Mining companies, among the most rapidly digitizing end-user segments, are increasingly adopting advanced underground sensing and mapping technologies to comply with stricter safety mandates and improve operational efficiency. The International Council on Mining & Metals (ICMM) has committed to eliminating fatalities through enhanced technology adoption, including underground sensing and robotic systems.

Nations such as Australia, Canada, and Chile have tightened underground mining safety legislation since 2022, directly creating procurement budgets for tunnel survey and monitoring equipment. The global mining sector invested over US$ 15 billion in technology and automation in 2023, according to the World Gold Council and sector reports. This creates a substantial addressable opportunity for technology vendors offering integrated sensing, communication, and robotic platforms.

Category-wise Analysis

Technology Insights

Ground-Penetrating Radar (GPR) leads the technology segment with an approximately 23% share in 2026, making it the dominant detection and survey technology for tunnel construction and inspection. GPR's supremacy is underpinned by its unmatched ability to provide non-destructive, real-time subsurface imaging without excavation or service disruption. The technology is widely mandated in pre-construction site surveys across Europe, North America, and Asia Pacific, where dense urban underground utilities require precise mapping before any boring or drilling activities.

Key infrastructure programs, such as the UK's HS2 high-speed rail project and multiple metro expansion programs in India and China, have extensively utilized GPR systems for ground assessment. Technology’s growing integration with AI-based data interpretation platforms further enhances its diagnostic accuracy, reinforcing GPR's leading market position through the forecast period.

End-use Insights

The government segment holds the leading position in the end-user category, accounting for approximately 32% share in 2026. National and regional governments globally are the largest procurers of tunnel construction services, driven by massive public infrastructure investment programs encompassing road tunnels, metro systems, water management channels, and military installations.

In the United States, the Infrastructure Investment and Jobs Act (IIJA) of 2021 allocated over US$ 110 billion for roads, bridges, and transit, a significant share of which flows to underground construction projects. Similarly, the European Union's Cohesion Fund and China's Belt and Road Initiative (BRI) continue to channel enormous public capital into tunneling projects across emerging economies, cementing the government segment's dominance through 2033.

Regional Analysis

North America Tunnel Construction Market Trends and Insights

North America leads the global tunnel construction market with a 28% share in 2026, supported by sustained federal infrastructure funding under the IIJA and active metro expansion programs in cities including New York, Los Angeles, and Toronto. The region benefits from advanced adoption of GPR, UGV inspection, and seismic survey technologies, alongside a mature regulatory framework mandating regular tunnel inspection cycles.

U.S. Tunnel Construction Market Size

The United States accounts for approximately 78% of the North American market in 2026, underpinned by the FHWA's National Tunnel Inspection Program and large-scale transit projects. Federal allocations exceeding US$ 39 billion for transit in the IIJA directly stimulate demand for tunnel construction, positioning the U.S. as the world's largest single national market.

Europe Tunnel Construction Market Trends and Insights

Europe represents a mature and innovation-driven market, characterized by significant rail tunnel rehabilitation programs and cross-border infrastructure corridors under the TEN-T network. Stringent EU safety and environmental directives accelerate the adoption of non-invasive survey technologies. Countries including Germany, the UK, France, Austria, and Switzerland are leading regional spending, particularly on high-speed rail and road tunnel upgrades.

Germany Tunnel Construction Market Size

Germany holds a leading position in Europe, contributing roughly 18% of the region's revenue in 2026. Ongoing investments under the Federal Transport Infrastructure Plan (Bundesverkehrswegeplan 2030), totaling over EUR 270 billion, allocate significant budgets for rail and road tunneling projects, with advanced GPR and structural monitoring technology procurement embedded in project specifications.

U.K. Tunnel Construction Market Size

The United Kingdom accounts for approximately 14% of the European market in 2026. The HS2 high-speed rail project and Crossrail (Elizabeth Line) have been major demand generators. Upcoming urban transit expansions and ongoing road tunnel maintenance programs supported by Highways England continue to sustain procurement of advanced tunneling survey and inspection equipment.

France Tunnel Construction Market Size

France contributes approximately 12% to European market revenues in 2026, driven by the Grand Paris Express, one of Europe's largest metro expansion programs, and ongoing maintenance obligations for Alpine Road and rail tunnels. SNCF Réseau's infrastructure investment programs further underpin demand for GPR and structural health monitoring solutions.

Asia Pacific Tunnel Construction Market Trends and Insights

Asia Pacific is the fastest-growing regional market, projected at a CAGR of 8% from 2026 to 2033, fueled by China's continued metro network expansion across tier-1 and tier-2 cities, India's ambitious metro and highway tunnel programs, and Southeast Asia's rising infrastructure investment. China alone operates the world's largest metro network by total length, necessitating both new construction and the procurement of inspection technology at scale.

India Tunnel Construction Market Size

India is among the highest-growth national markets in Asia Pacific, expected to account for approximately 15% of regional revenues by 2027. The National Infrastructure Pipeline (NIP), targeting over US$ 1.4 trillion in infrastructure investment through 2025, includes numerous tunneling projects across metro, highway, and hydroelectric programs, driving strong demand for GPR and robotic inspection systems.

Japan Tunnel Construction Market Size

Japan holds a mature yet significant share of around 17% in the Asia-Pacific market in 2026. With over 10,000 km of road tunnels requiring periodic inspection under the Ministry of Land, Infrastructure, Transport and Tourism (MLIT) framework, demand for advanced non-destructive evaluation technologies including UGV-based inspection systems is strong and recurring.

Southeast Asia Tunnel Construction Market Size

Southeast Asia is an emerging high-potential market, contributing approximately 10% of Asia Pacific revenues in 2026. Rapid metro rail buildouts in Vietnam, Thailand, Indonesia, and the Philippines, supported by multilateral development bank financing from the Asian Development Bank (ADB), are generating new project pipelines, creating first-time procurement demand for tunnel survey and monitoring technologies.

Competitive Landscape

The global tunnel construction market exhibits a moderately fragmented competitive structure, with a mix of large multinational construction and technology firms alongside specialized niche players. Market leaders such as Hexagon AB, STRABAG, and Keller Group leverage scale, integrated service offerings, and proprietary technology portfolios to sustain competitive advantage.

Key strategies include R&D investment in AI-enhanced subsurface imaging, strategic acquisitions of sensing technology firms, and long-term framework agreements with government transport authorities. Emerging players increasingly differentiate through modular, robotics-driven inspection platforms targeting the growing asset management and rehabilitation sub-market.

Key Developments:

- In January 2025, Hexagon AB announced the launch of an enhanced AI-integrated GPR data analytics platform designed to accelerate subsurface mapping turnaround times for tunnel pre-construction surveys by up to 40%.

- In September 2024, STRABAG was awarded a major contract under the Austrian Federal Railways (ÖBB) expansion program for a new alpine rail tunnel, deploying advanced UGV-based structural monitoring throughout the construction phase.

- In March 2024, GeoRadar (Geophysical Survey Systems, Inc.) introduced a next-generation 3D GPR system specifically optimized for real-time tunnel lining assessment, targeting metro operators across North America and Europe.

Companies Covered in Tunnel Construction Market

- Hexagon AB

- Rocscience

- STRABAG

- MST Global

- Keller Group

- IBAK Helmut Hunger

- Geospace Technologies

- GeoRadar

- GEOInstruments

- Minova

- OCTX

- SENNING GmbH

- FLIR Systems

- Hitachi High-Technologies

- Nova Metrix

Frequently Asked Questions

The global tunnel construction market is estimated at US$ 2.4 billion in 2026. The market is driven by expanding urban metro networks, government infrastructure investment programs, and the growing adoption of advanced subsurface survey technologies including Ground Penetrating Radar (GPR) and robotic inspection systems worldwide.

The primary demand drivers include rising urbanization necessitating underground transit and utility infrastructure, accelerating government capital expenditure under programs such as the U.S. Infrastructure Investment and Jobs Act (IIJA) and the EU's TEN-T network, and the mandatory integration of advanced sensing and robotic technologies to enhance worker safety and construction precision.

North America is the leading region, holding approximately 28% of global market share in 2026. The region's leadership is supported by robust federal infrastructure funding, the FHWA's National Tunnel Inspection Program, and strong private-sector participation in metro and highway tunnel construction projects.

Key opportunities include the rapid commercialization of UGV-based autonomous inspection systems for aging tunnel infrastructure rehabilitation, and the growing demand from the mining sector for integrated underground sensing solutions driven by tightening safety regulations under frameworks endorsed by the International Council on Mining & Metals (ICMM). Both represent high-margin, recurring revenue streams for market participants.

The leading companies operating in the global tunnel construction market include Hexagon AB, STRABAG, Keller Group, GeoRadar, Herrenknecht AG, FLIR Systems, Hitachi High-Technologies, Trimble Inc., and Nova Metrix, among others.